Frazer Harrison/Getty Images Entertainment

Who can forget the Tom Cruise and Renée Zellweger movie, “Jerry Maguire”, in which the latter said “You Had Me At Hello” at the end of the movie? This classic is definitely worth re-watching every now and then, and as someone wisely told me once, you have to watch it from beginning to end and not skip around to fully appreciate the ending.

But I digress, as in addition to classic movies, I also have a soft spot for beaten down high-yielders like Blackstone Mortgage Trust (NYSE:BXMT). BXMT is currently trading close to its 52-week low of $20.87, and currently yields 10.9%, giving income investors a good opportunity to layer into this name. Let’s explore what makes BXMT an appealing buy at present.

Why BXMT?

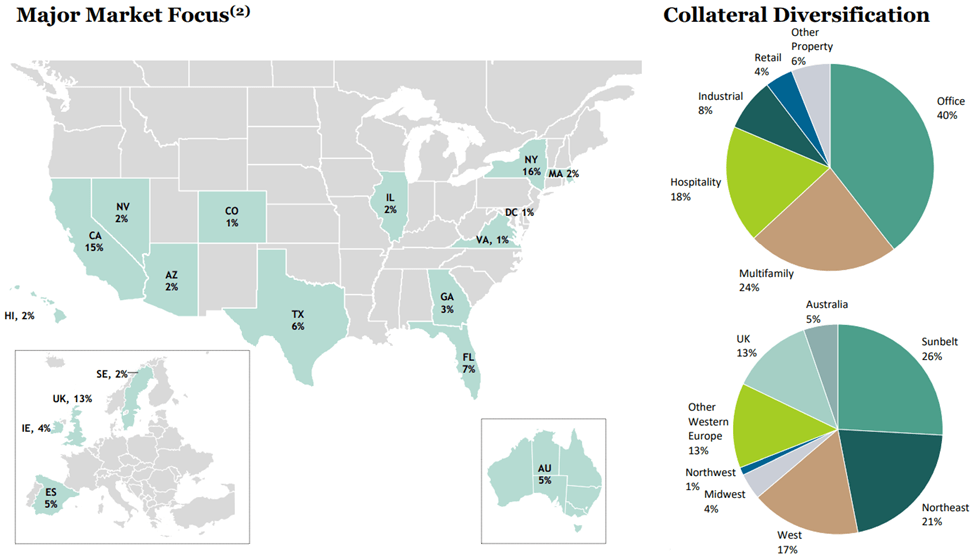

Blackstone Mortgage Trust is a giant in the commercial mortgage REIT space, generating senior loans collateralized by real estate in three continents, in North America, Europe, and Australia.

It’s externally managed by Blackstone (BX), one of the largest asset managers in the world, with over $200 billion worth of real estate assets under management. This affiliation benefits BXMT in that it provides it with a deal pipeline and valuable line of sight into the commercial real estate space.

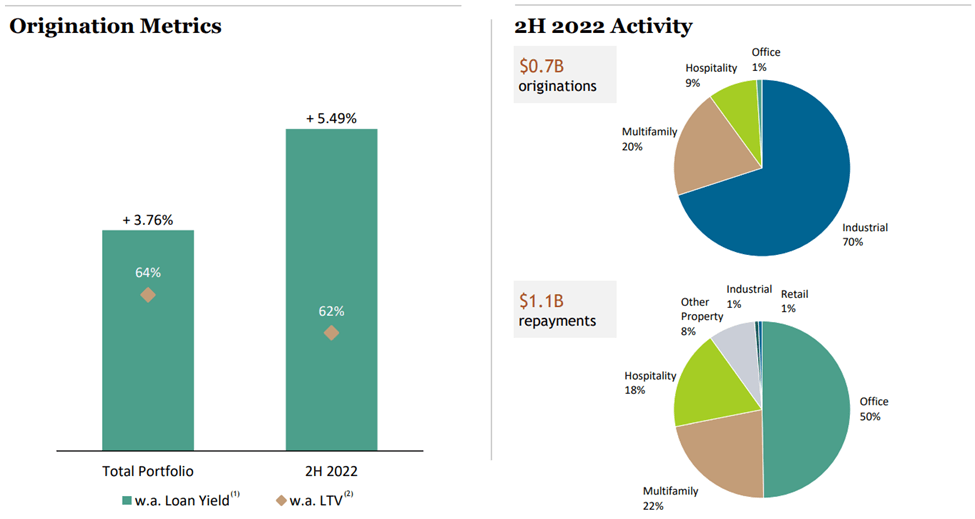

BXMT carries significant size and scale with its $26.8 billion senior loan portfolio, making it one of the biggest players in the commercial mREIT space. Management adopts a conservative lending practice with average origination LTV of 64% and by investing in loans backed by institutional quality real estate as collateral.

Moreover, BXMT is diversified across 203 loans and is able to leverage Blackstone breadth and presence to invest attractive opportunities internationally. As shown below, BXMT has meaningful exposure to Europe and Asia, and its top 3 sectors consist of office, multifamily, and hospitality.

Investor Presentation

While such high exposure to office properties may give some investors pause, it’s worth noting that many CEOs have requested that employees return to the office on at least a part time basis, noting the value of in-person engagement.

This makes the future of work more likely to be hybrid rather than fully remote. Plus, 88% of BXMT’s office loans are to properties that are new and efficient buildings with modern amenities, low leverage with significant sponsor equity, and/or are located in the fast-growing Sunbelt region of the U.S.

It’s also worth noting that most of BXMT’s loans have durations of just a few years, giving management the opportunity to pivot into other property classes. This is reflected by $1.7 billion of office repayments in 2022, giving management the opportunity to deploy capital into better positioned asset classes such as industrial and multifamily, which comprised 90% BXMT’s second half 2022 origination activity, as shown below.

Investor Presentation

Notably, BXMT does have higher leverage than some of its commercial mREIT peers, with a debt to equity ratio of 3.8x at the end of 2022, and is higher than the 3.6x from the third quarter. However, this was the result of BXMT raising its CECL (current expected credit loss) reserve, which reduced its GAAP equity, rather than actually increasing leverage.

In addition, BXMT’s liabilities are term matched to its asset maturities, and has a significant $1.6 billion worth of liquidity, after raising $1.2 billion of capital on attractive terms during 2022. Management expects to repay $220 million worth of maturities this year with existing liquidity and has no other debt maturities until 2026, thereby mitigating the impacts of higher interest rates in the near term.

Importantly, BXMT is benefitting from higher interest rates, with distributable EPS of $0.80 during the fourth quarter, resulting in 1.29x dividend coverage.

BXMT is also fairly easy to value, considering its plain vanilla senior loan portfolio with no physical real estate assets that have depreciation considerations. At the current price of $22.69, BXMT appears to be in value territory.

As shown below, this sits well below its historical trading range over the past 5-years outside of the 2020 timeframe. Analysts also have a consensus Buy rating with an average price target of $24.86, which equates to a potential one-year 20% total return.

Seeking Alpha

Investor Takeaway

BXMT offers investors exposure to a conservative lending practice with institutional quality real estate as collateral, significant size and scale, and strong presence in both the U.S. and international markets.

While BXMT does carry higher leverage than some of its peers, BXMT’s mix of scale, access to credit markets, discount to book value and high and well-covered dividend yield make it an attractive buy for income investors with potential for capital appreciation to boot.

Be the first to comment