olm26250

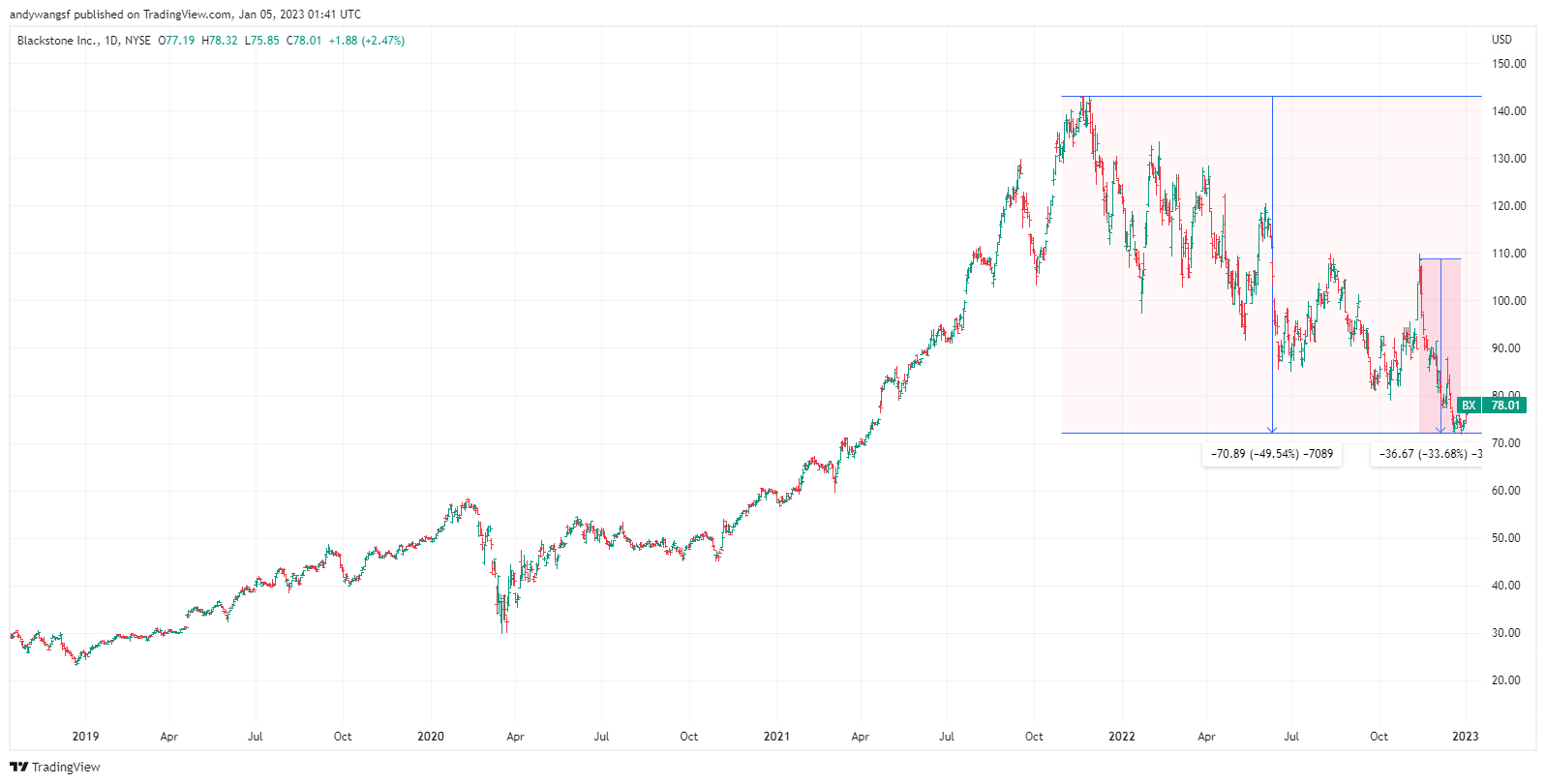

Concerns surrounding the Blackstone Inc. (NYSE:BX) flagship private real estate fund, the US$70 billion Blackstone Real Estate Income Trust (“BREIT”), have weighed heavily on Blackstone’s share price performance after a surge in redemptions forced the company to limit withdrawals in November 2022.

These concerns were further compounded by multiple rating downgrades by Barclays (BCS) and Credit Suisse (CS), culminating in a steep 33.7% decline in Blackstone’s share price from its 11 November peak to its 28 December low. If measured against Blackstone’s all-time peak in 2021, the stock was down 49.5%.

TradingView.com

From our perspective, this steep selloff presents a compelling entry point for investors looking to build a position in Blackstone with a medium-to-long-term investment horizon. Although we appreciate the short-term risks that the high-interest rate environment and reduced fees from its management and advisory business could dampen earnings in 2023, most of the bad news should have already been priced into the stock. Crucially, Blackstone’s business model is fundamentally sound and remains in a great position to continue to deliver superior risk-adjusted returns longer term.

Besides unwarranted fears of a potential real estate crisis and concerns that redemptions on BREIT could accelerate even further, potentially reducing income from fees and forcing the fund to sell its quality real estate assets prematurely, we see no real fundamental reasons justifying the deep selloff in Blackstone.

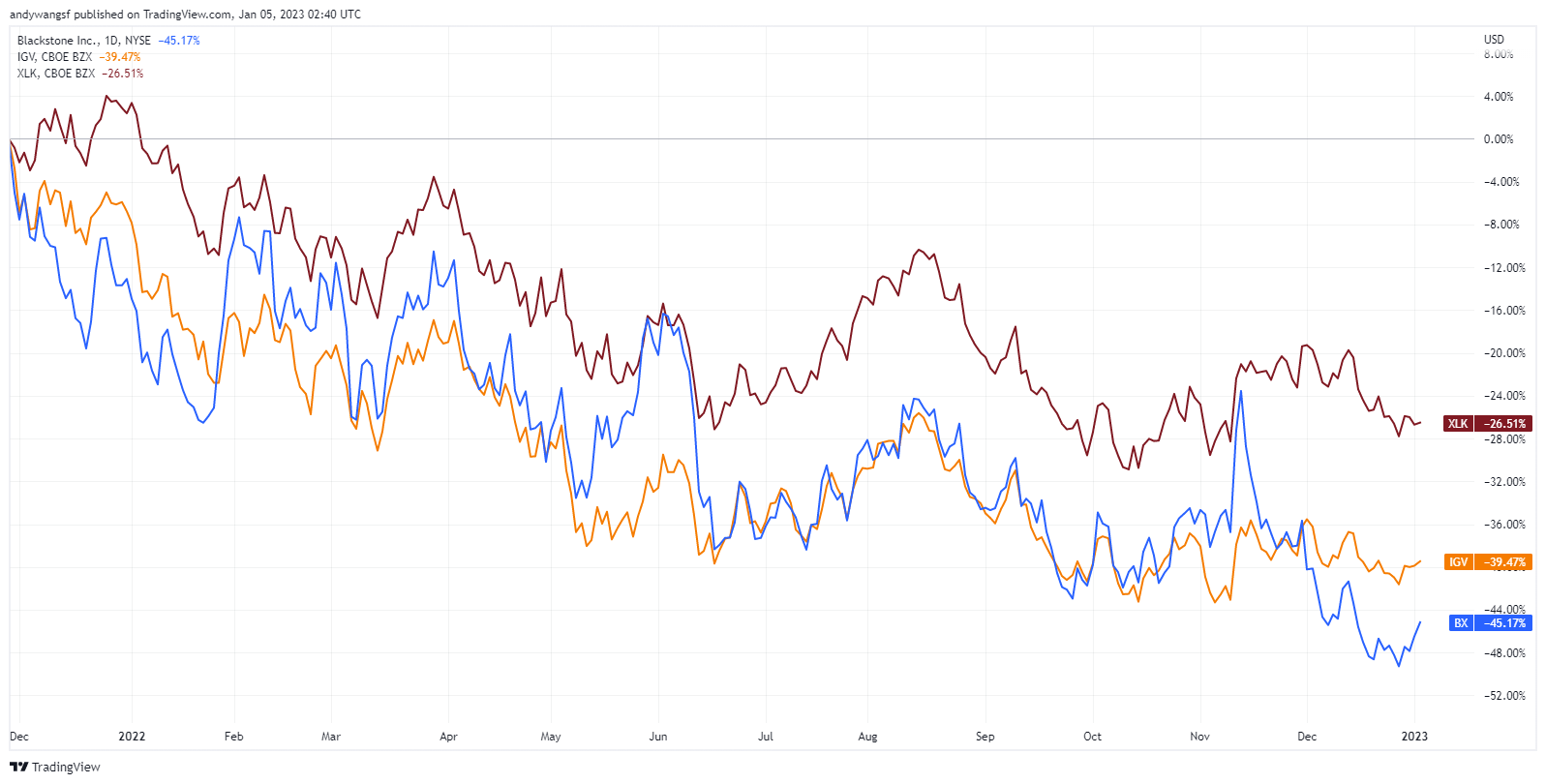

It is also quite puzzling to us that Blackstone is more heavily sold by investors than technology stocks, which typically come with much higher earnings volatility and cutthroat competition. For example, technology exchange-traded funds (“ETFs”) such as (XLK) and (IGV) have both outperformed Blackstone since the equity market peaked in 2021.

TradingView.com

UC Investment Deal A Vote Of Confidence In BREIT

Despite the strong and consistent performance delivered by BREIT over the years (13% annualized returns since inception in 2017), and little evidence that would suggest any form of trouble with the fund, the surge in redemptions may nonetheless force Blackstone to respond by selling some assets to raise cash. Even so, judging from the most recent US$5.5 billion sale of BREIT’s stake in MGM Grand and Mandalay Bay in Las Vegas, the terms of the deal were quite favorable, generating a profit of more than US$700 million in less than three years for BREIT.

The sale was quickly followed by BREIT winning a deal with UC Investments, which manages US$150 billion on behalf of the University of California and its beneficiaries. UC Investments will invest US$4 billion in BREIT, with Blackstone contributing US$1 billion of its own BREIT holdings as part of a strategic venture to support an 11.25% minimum annualized net return for UC Investments over a 6-year holding period. As part of the deal, Blackstone will stand to gain from any returns in excess of the specified minimum, in addition to existing fees charged by BREIT.

The deal not only represents the latest vote of confidence in BREIT by an institutional investor but also highlights management’s confidence to continue to deliver strong returns for BREIT’s investors in the coming years. More importantly, the deal would unlock fresh capital for BREIT and offset fees lost due to the recent surge in redemptions.

Valuations Are Compelling For Long-Term Investors

The recent sell-off in Blackstone has also brought valuations to very attractive levels. At the time of writing, Blackstone is trading at 14.8x Forward P/E and 13.1x TTM P/E with a dividend yield of 6.5%. Given how Blackstone has consistently delivered strong 30% ROEs over the past 5 years, these valuation multiples have become quite compelling in our view.

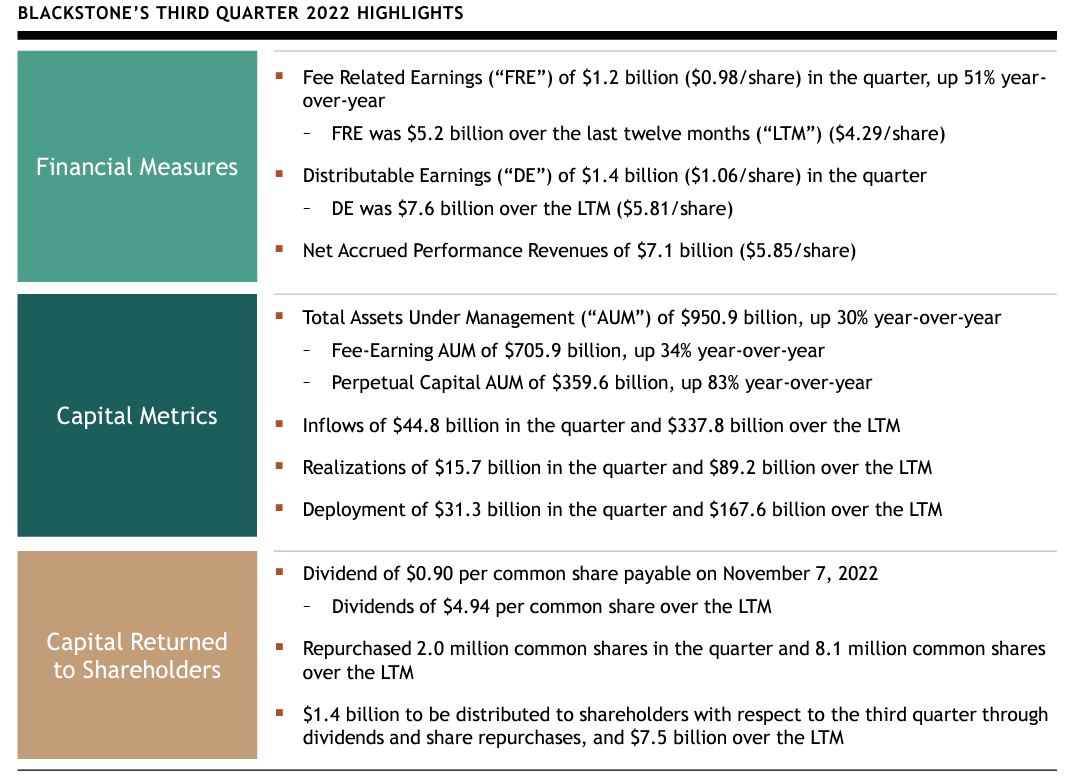

Blackstone’s most recent quarterly results (Q3 2022) also indicate that its overall business continues to attract healthy inflows with total assets under management growing by a staggering 30% year-on-year. Meanwhile, the company has also continued to deploy capital aggressively with US$167.6 billion being deployed in the twelve months ending Q3 2022. This is compared to US$62.9 billion, US$61.7 billion and US$144.4 billion in the years 2019, 2020, and 2021, respectively.

Blackstone Inc

We particularly like Blackstone’s aggressive capital deployment despite the overwhelming pessimism surrounding U.S. real estate. According to Blackstone’s call transcript at the Goldman Sachs 2022 US Financial Services Conference in December, management shared that the company is still sitting on $180 billion of dry powder, even after deploying almost $170 billion over the past 12 months.

Blackstone’s strategic decision to allocate capital more heavily towards the Sunbelt states also aligns with our view that these areas would see the strongest demand for housing, which we elaborated on in an earlier article published on 18 October.

Below are some of the key highlights from the transcript:

In large part, because at the global financial crisis, we only spent half the money to build housing stock in the United States. And so, really shortened housing. So, the beneficiary of that are apartments, because you got to have some place and housing now is being adversely impacted by the very high interest rates.

So, what we did with BREIT is we concentrated it in warehouses and apartments and we avoided almost all the other asset classes. We have 80% of the fund in those terrific-performing asset classes. And we also located them in real estate — another thing that’s important is where is this real estate? Those 70% in BREIT is in the Sunbelt. Just to give you an idea how profound the decision that is, the growth, the population growth in the Sunbelt have been — a bit of the West, it’s five times the population growth in the rest of the country.

…that these redemptions were preponderantly coming from Asia. Same product is in the United States. It’s U.S. real estate. What was going on in Asia? And it didn’t take long to figure out that the Hang Seng Index went down 40% and the Asians tend to use more leverage, more margin debt.

So, if you are an investor who has got margin debt and your market goes down 40%, you can imagine what it was like to be one of those into the pools. You’re under excruciating financial pressure. And so, they were just looking for liquidity. So BREIT, because it was so successful, its returns have averaged 13% a year for the last six years. That’s three times the return of the REIT index.

In Conclusion

Blackstone Inc.’s economies of scale, depth, and strategically crafted real estate exposure fit really well with our own views and outlook view on U.S. real estate. Blackstone Inc. stock’s compelling valuations also present the opportunity for outsized returns over the next few years.

We initiate our coverage of Blackstone with a “Strong Buy” rating.

Be the first to comment