3D_generator/iStock via Getty Images

When we last covered BlackRock Utility & Infrastructure Trust (NYSE:BUI) and Reaves Utility Income Fund (NYSE:UTG), we had a dour outlook on the utilities sector.

We are hence downgrading UTG to a Sell rating. We see the most likely outcome of a 15% drop in the fund NAV alongside a widening of the discount leading to negative 15-20% total returns. We will revisit when we believe the fundamentals have changed.

Source: UTG Moves To A Sell, BUI To A Hold

While we thought utilities had got overvalued, we did not expect such a rapid reset.

That rapid reset has now required an update to our thinking.

What’s Going On?

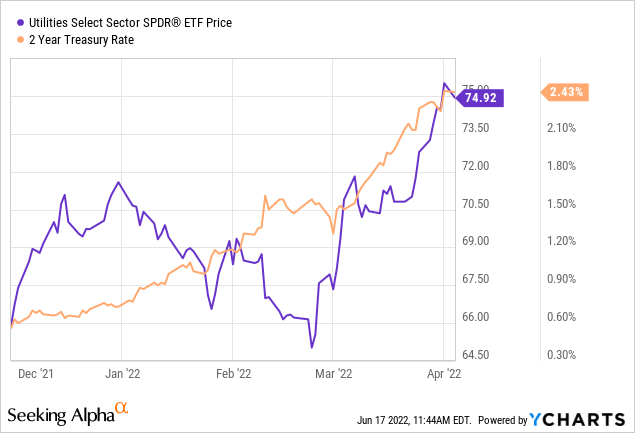

Utilities are easily the most interest rate sensitive sector there is. Their sensitivity runs in an inverse manner and generally rising rates are bad for the sector. Now, there are exceptions of course. Rates rising from very low levels, due to economic optimism, can be good for the sector. Even mild to moderate rises in interest rates can be tolerated. Exceptionally rapid rate rises are very problematic for the sector, just like they are for REITs. The funny aspect here was that we were getting just that, while utilities kept ignoring the warnings. We have pulled up the chart from December 2021 till the date on which we wrote the last article.

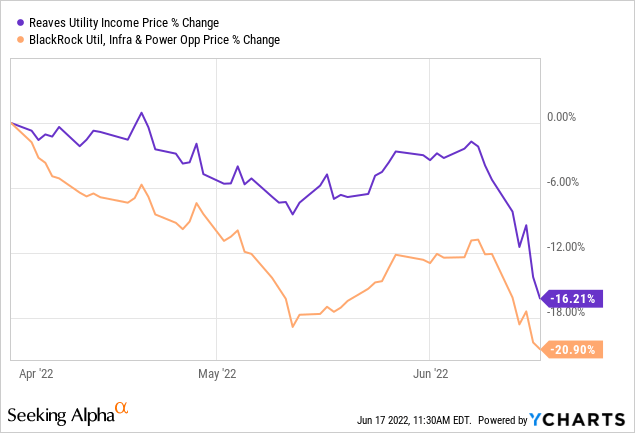

So obviously that was glaring anomaly that forced to ask? Just how much money do utility shareholders want to lose here? Of course since then XLU, BUI and UTG have rapidly been reacquainted with gravity. Are they cheap enough?

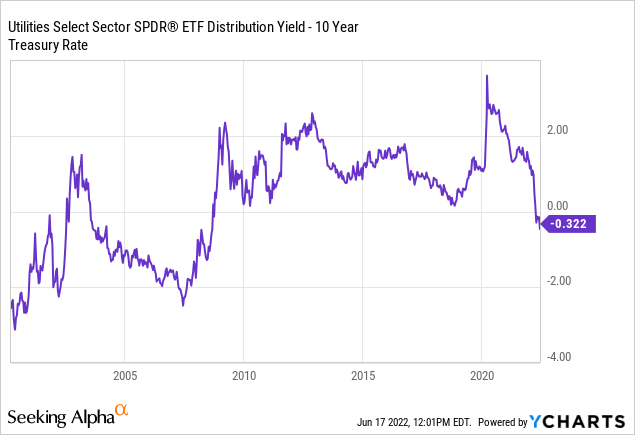

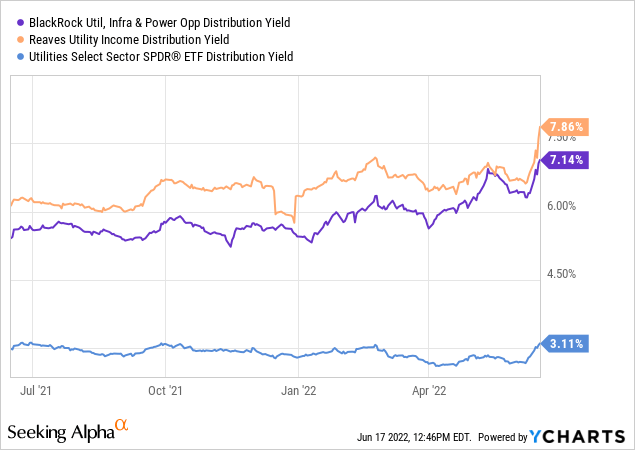

XLU is a good proxy for the sector and is less impacted by special distributions. We hence get a smoother read using this versus using either of the funds. Using the dividend yield for XLU, we can see that the current XLU yield is now 32 basis points lower than that of the 10-Year Treasury note.

This puts XLU at a disadvantage and this level is the lowest since 2009. The sector trades at 20.0X forward earnings. Our approach with this sector is that great buying points come in when you can buy this when you get it for less than 15X. That may sound harsh, but keep in mind that Utilities traded every single year, under a forward P/E of 16 from 1994-2014. So for 20 years you got chances in general to buy it exceptionally cheap. So the current distortions of cheap money aside, utilities have just become better valued, not cheap.

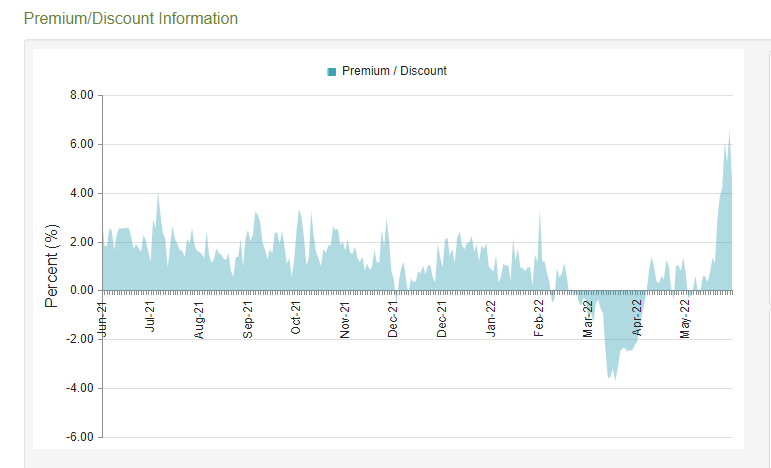

UTG

Having made up minds here that utilities are not exactly being given away, we look at the two funds in more detail. UTG has seen a sharp drop in price, but matched by an even faster drop in NAV.

CEF Connect-UTG

This has actually expanded the premium to NAV, which rings in at one of the highest for the year. The next chart should help you better visualize this.

CEF Connect-UTG

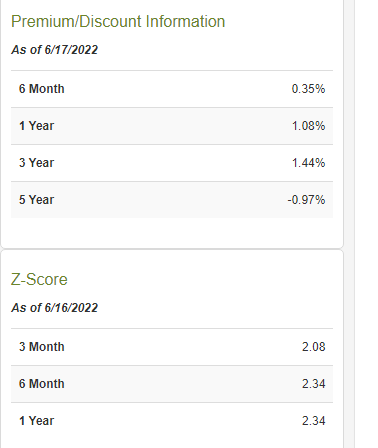

We also have the math on what this means. The popular measure here is the Z-score, which helps investors decide how expensive the fund is in relation to its recent history. Note that this only passes an opinion on the relative price, and has no input on the underlying valuations. Z-scores are positive and in 2 plus range.

CEF Connect-UTG

This again validates the idea that the fund is very expensive on a price basis.

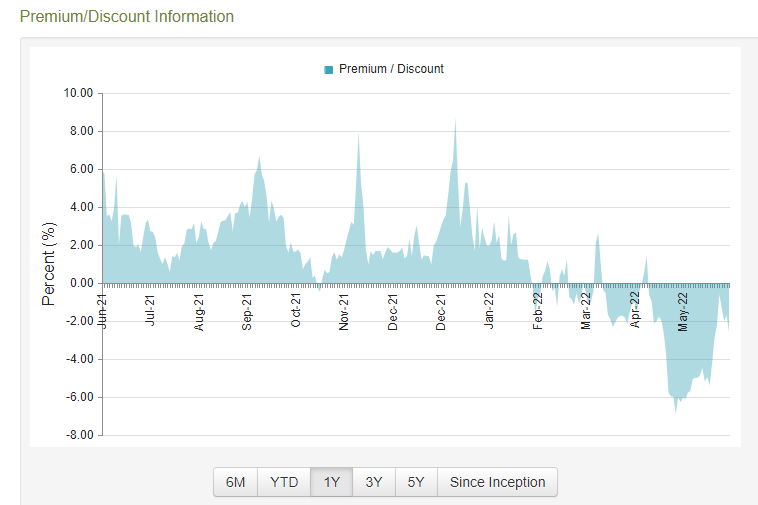

BUI

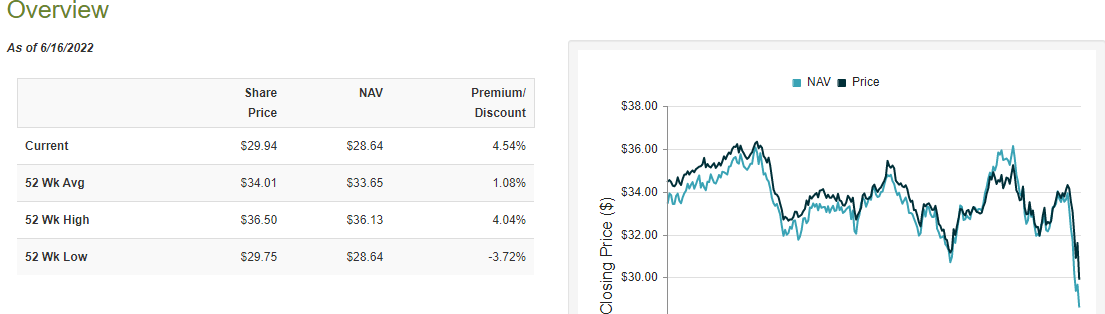

Interestingly enough, BUI’s pricing has gone in the other direction with a discount to NAV.

CEF Connect-BUI

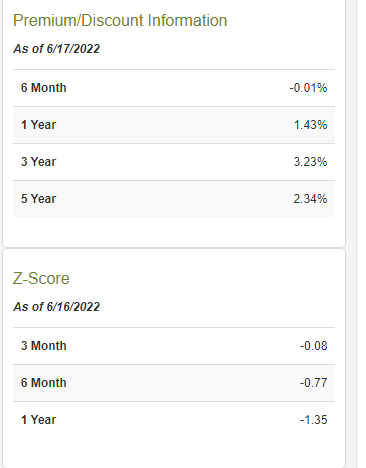

The same Z-score lookup tells us that the fund is modestly cheap on a 1 year price movement.

CEF Connect-BUI

Verdict

Utilities have become cheaper and perhaps a good rally is in the works. We don’t think longer term valuations are compelling, especially considering where interest rates are headed. Both funds offer solid yields and that is perhaps where the appeal lies for them.

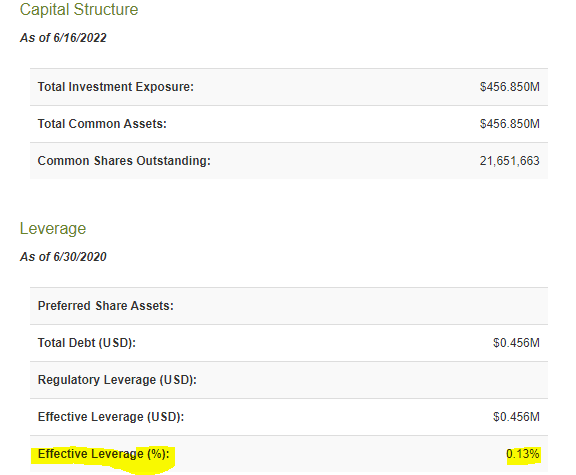

But taking a cursory look at the XLU yield will tell you that neither fund (UTG or BUI) is funding that distribution yield from underlying holdings. So there is a built in capital appreciation requirement that is there to pay distributions while preserving NAV. Here we give the advantage squarely to BUI. BUI is virtually unleveraged (compared to 18.5% for UTG) and we think this will help if valuations press the stocks lower in the short term.

CEF Connect-BUI

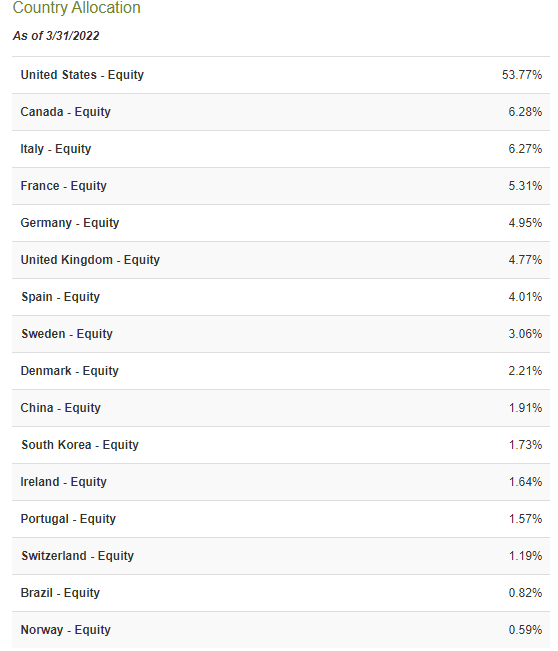

BUI is also quite exposed to Europe, where valuations are far lower.

CEF Connect-BUI

Finally, BUI does sell covered calls on its positions and that will help in the current high volatility environment. So we have 4 points in favor of BUI (including the discount to NAV) and that allows us to stamp this with a buy rating. For UTG, we see the drop in price and valuation compression, but remain overall unimpressed at this point. We are still upgrading it to a hold though, and canceling out the prior Sell/Short Sell call.

Be the first to comment