Zerbor/iStock via Getty Images

Since becoming public, BlackLine, Inc. (NASDAQ:BL) has been the perfect example of consistent and steady growth. Between 2016 and 2019, the business enjoyed around 120% of price appreciation without much volatility. Now that we have moved past the craziness of the COVID years (when the stock price more than doubled in just a few months), the price is basically back to where it was in 2019. In the meantime, though, I argue that the business has managed to improve its position, consistently proving that it is approaching meaningful scale and operational leverage. With a P/S ratio back down to earth, the stock increasingly looks like a very interesting idea.

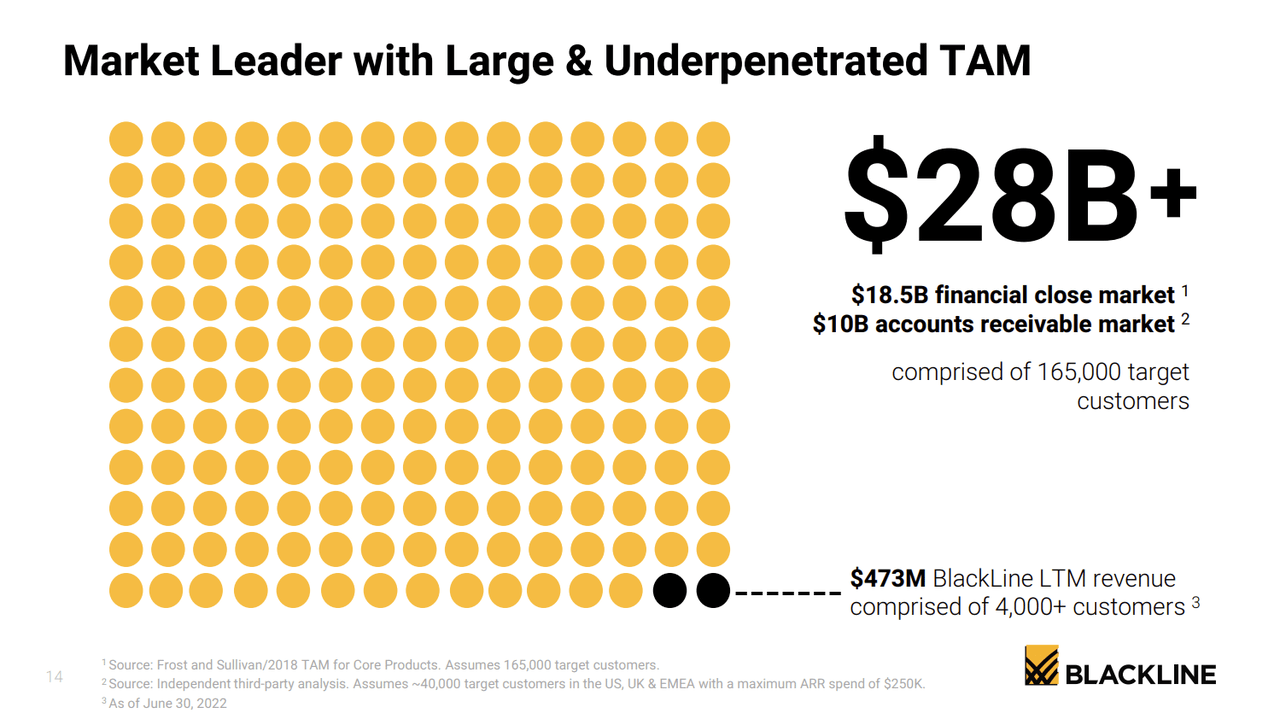

Good Business Chasing A Large Total Addressable Market

BlackLine operates in the business-to-business software market, providing a cloud-based digital offering with the intent of simplifying accounting practices as well as making sure that they are more reliable. Many companies nowadays still manage monthly or quarterly financial reports through the use of manual and error-prone processes such as Excel spreadsheets. BlackLine’s mission, as highlighted on the company’s annual report, is to transform how accounting and finance departments operate. Most importantly, BlackLine operates by integrating itself to over 30 different traditional business software tools such as NetSuite, SAP, Workday, Oracle and others in order to effectively manage the data coming in from multiple different sources.

BlackLine 2021 Annual Report

Over the last few years BlackLine also completed a few acquisitions meant to expand its software capabilities: in 2020, the company acquired Rimilia Holdings in order to add accounts receivable automation, and in 2022, FourQ Systems was acquired for enhancing BlackLine’s intercompany accounting automation capabilities. BlackLine had to take on some debt in the past few years, especially to cover these acquisitions, and as of the latest report the company had $1.3 billion in debt (convertible notes maturing in 2024 and 2026). The company has over $1 billion of cash and short-term investment, therefore, the debt profiling does not appear too concerning.

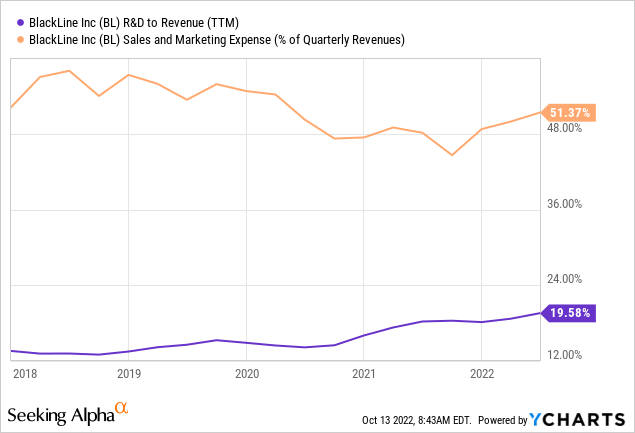

As with any other software company, BlackLine needs to keep innovating to drive its growth. As mentioned above, the company has acquired some other businesses in the past few years in order to enhance its offerings, however, it will be crucial to always drive some growth, at least organically. The company is increasing year over year the contribution of R&D to total Revenue, which is not that worrying by itself if the product will benefit from such investments.

The same is true for marketing expenses, which in relation to revenue have been declining over the years (despite a meaningful jump in 2022) but still account for around 50% of total sales, which is quite high.

YCharts – Seeking Alpha

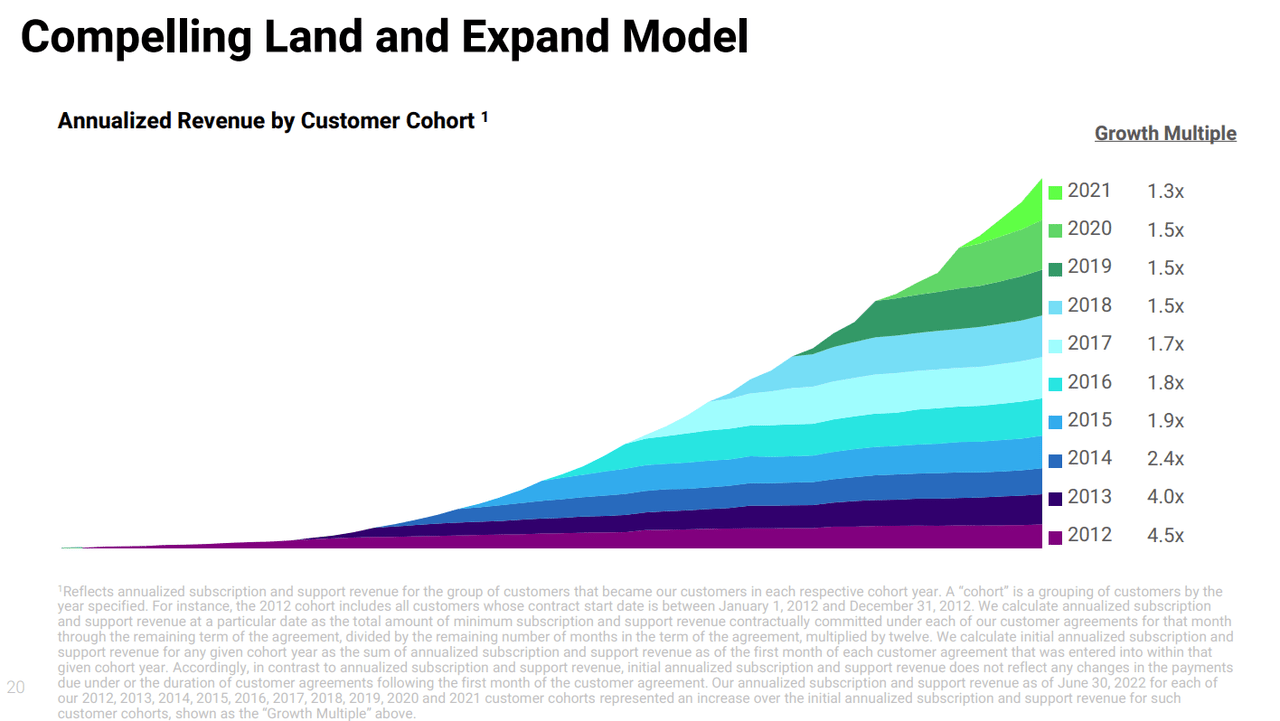

However, the reason why these expenses appear as good investments is exemplified in the following chart provided by the company in their latest annual report. As of now, the numbers show that BlackLine is able to retain a very high number of customers, a good portion of which keeps spending more and more, which is an indication that every dollar spent in marketing and R&D goes a long way. Overall, the company managed to retain every year around 97% of their customers, and overall, its Dollar-Based Net Revenue Retention Rate is consistently around 106-110%, which means that existing customers end up adopting more products and spending more.

BlackLine 2021 Annual Report

BlackLine has also experienced a healthy growth in customers over the years. 13% CAGR grows in overall customers, while those generating at least $250,000 of Annual Recurring Revenue grew even faster at 28% CAGR since 2016.

Recent Performance

In the latest quarterly report, the company reported healthy revenue growth of 25.8% to $128.4 million, GAAP gross margins of 74% down from 76% in 2Q 2021 and from 79% posted in 2Q 2020. The drop in gross margin is probably related to the acquired businesses, which might have had lower gross margins in the first place. In the latest call, management mentioned how the company is also trying to shift some of the low-margin services to its partners. Some service revenue will therefore be lost (around 1% revenue), however this is revenue generated at a very low gross margin of about 20%. By leveraging partnerships, the margin profile of the entire business should benefit. As of now, the consistent drop in gross margins is a little bit worrying, but 74% is still a healthy margin. Definitely something to monitor for the future.

On the bottom line, BlackLine posted negative Net Income consistently every quarter. This is due to stock-based compensation, which has been growing over the years and in the latest quarter accounted for $20.6 million. This equates to shares dilution of about 2% CAGR since 2018, which does not seem too much as it allows the company to retain more cash and invest it directly into the growth of the business. Pretty standard practices for companies operating still in growth mode.

Over the years, the company has grown free cash flow quite consistently: after a few years with marginally negative free cash flow, BlackLine has posted since 2018 positive free cash flow, growing at 41% YoY CAGR since 2019. In the latest quarter, free cash flow (“FCF”) turned negative (-$5.1) due to higher CapEx. Management highlighted how CapEx should normalize with the historical trends and FCF should continue to improve.

Valuation And Key Takeaways

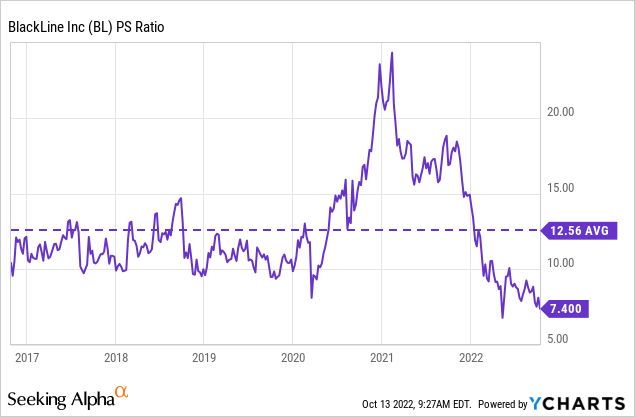

Valuation wise, the business is not yet optimized for profitability as explained above, and as such many of the usual metrics do not seem very useful. Both P/E and P/FCF are completely skewed due to high investments by the company into its operation in an attempt to fund its growth. On a P/S ratio, the stock is now trading at 7.4, which is still on the high side but considerably lower than the historic average since the company became public as shown below.

YCharts – Seeking Alpha

I built a quick Discounted Cash Flow (“DCF”) model projecting into the next 5 years 25% FCF growth and 15% for the following 5 years. The growth is lower than the 41% CAGR posted by the company in the last 3 years. However, this was from a smaller nominal number and it is better to be conservative. With a 10% discount and 20 terminal value for P/FCF, the company would be valued at $3.3 billion, in line with the current valuation. If BlackLine will be able to maintain steady FCF growth in the future, in the ballpark of 20/25% CAGR growth, then the current valuation suggests that an investment today might generate around 10% return.

For a good, growing business this seems like an acceptable price to pay for me. Of course, lower is better, and as such the thesis might become more interesting if the stock were to drop in the near future due to negative market sentiment.

Be the first to comment