Leonid Sukala/iStock via Getty Images

Something big is happening in decentralized finance (DeFi). In the last two years, the growth of NFTs (or “non-fungible tokens”), decentralized applications, stablecoins, and cryptocurrencies has been very hard to miss. Bitcoin (BTC-USD) has gained institutional adoption. The ProShares Bitcoin Strategy ETF (BITO), a Bitcoin futures-based ETF, has seen consistent inflows. More and more people are talking about Bitcoin’s implications for the global monetary system.

Recently, the Terra blockchain (LUNA-USD) has announced it will be building a reserve of up to $10 billion worth of Bitcoin. Terra’s native cryptocurrency LUNA is consistently ranked in the top 10 largest coins by market cap. It is one of the largest blockchains which developers can build decentralized applications on, after Ethereum, Binance Chain, Solana, and Cardano. Terra is unique in that it is a layer 1 protocol for algorithmic stablecoins which can imitate the price of fiat currencies without being backed by fiat. By dynamically changing the supply of LUNA and Terra stablecoin, the stablecoin’s price can be pegged to the fiat currency it is imitating. Details of how it works can be found here.

Terra critics have pointed out that LUNA and Terra stablecoins can possibly enter a reflexive process (or “death spiral”) where the selling pressures for both coins are so strong that the stablecoin peg would break irrecoverably. The process can be summarized as:

- Stablecoin, UST, price goes below the peg, $1 per UST. This causes traders to buy N UST and use Terra’s built-in mechanism to destroy N UST and create N dollars’ worth of LUNA.

- LUNA supply increases as a result. Traders will sell the LUNA, which puts downward pressure on LUNA’s price. This makes people nervous about the peg breaking so people continue selling UST, which pushes it again below the peg.

- Traders repeat step 1, until the supply of LUNA swells to the point that each LUNA is practically worthless.

- The system collapses because of the negative feedback loop which mutually reinforces selling of both UST and LUNA.

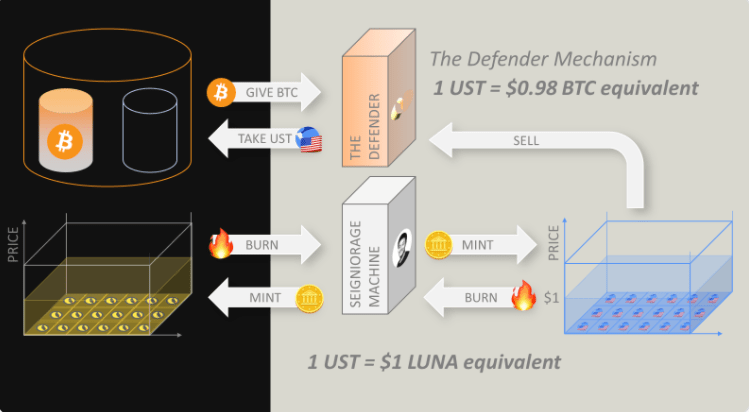

Since January, Terra has been accumulating Bitcoin. It was only recently that they have announced the purpose. Terra’s solution for avoiding the death spiral scenario above is to use the Bitcoin reserve as a last resort buyer. Functionally, the reserve will only be used when UST has over a 2% break to the downside. At this point, traders can use UST to buy $0.98 Bitcoin, ensuring a worst-case hard peg of $0.98 per UST. This will hold until the Bitcoin reserve is depleted. But the idea is that this last resort will alleviate the stress in the market and dramatically halt an accelerating selloff that would be characteristic of a true death spiral event.

Terra’s Bitcoin reserve function (Twitter)

In the words of Terra’s creator Do Kwon:

The reason why we are particularly interested in Bitcoin is because we believe that [it] is the strongest digital reserve asset… UST is going to be the first internet native currency that implements the Bitcoin standard as part of its monetary policy.

Terra plans to become the largest holder of Bitcoin after Satoshi Nakamoto (Bitcoin’s founder(s)). Therefore, Terra stablecoins are functionally backed by the utility of LUNA as the native coin of the Terra blockchain but will also be protected by the value of Bitcoin. The argument for the stability of Terra is now simple: Terra fails only if Bitcoin fails. This is a very powerful statement because it presupposes the utility of Bitcoin as a store of value within the context of DeFi. Stated differently, Bitcoin and DeFi are unilaterally and unalterably connected.

Money, Credit, and Narratives

If Do Kwon is correct, the “Bitcoin standard” for digital assets and DeFi will gain more traction over time. This is probably the strongest thesis for a long-term Bitcoin investment—if one believes in the growth of DeFi, then Bitcoin is a strong buy and hold. The next step is thinking through whether a Bitcoin standard of sorts will be used by governments and central banks, as if bridging traditional and decentralized finance within the global monetary system. I believe this is more likely than what Bitcoin’s price implies.

“Gold is money. Everything else is credit” – JP Morgan, 1912.

This was true in the US and Europe in 1912. Gold was stored in vaults and paper currencies were issued to represent the gold. Morgan recognized that everything else was a result of banks creating loans, therefore credit.

By 1945, the US had most of the world’s gold because it had been paid by the other countries in gold for the first two World Wars. After the Second World War, the US also had the world’s largest manufacturing base. So, it was agreed at Bretton Woods that the world’s currencies would be pegged to the dollar and the dollar would be pegged to gold. The global monetary system existed on this quasi-gold standard until 1971. Today most currencies are on a floating exchange rate.

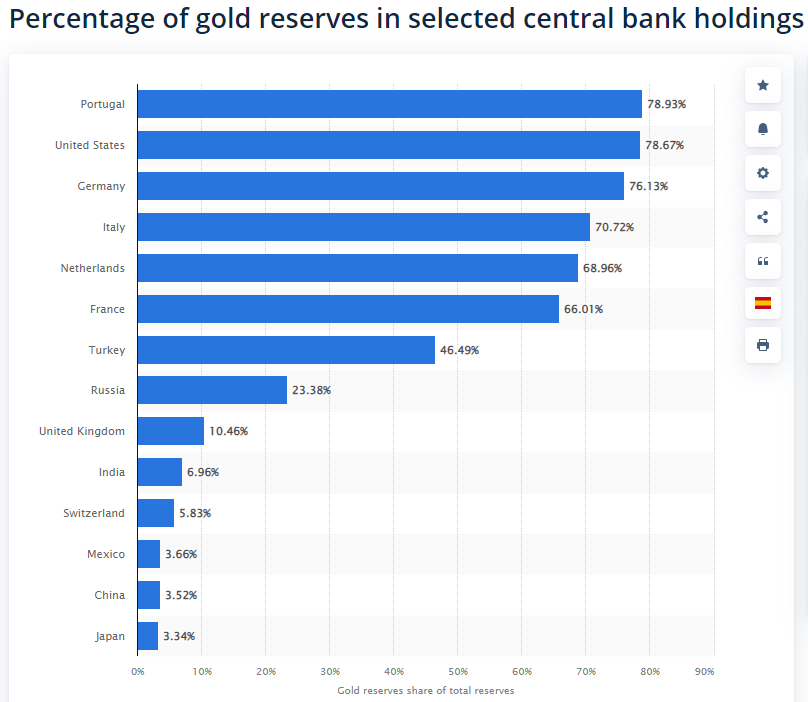

However, central banks still have gold reserves—about a fifth of all gold ever mined are held by central banks—along with foreign currencies and other precious metals. “Gold is money,” or at least “gold is a store of value,” persists as a truism among central bankers.

Percent of gold reserves (Statistica)

But why is gold money? Humans have used numerous materials as money over millennia. Gold happens to be a material which is both durable and hard to produce (high stock-to-flow ratio). This combination means supply is rather fixed, allowing things to be steadily priced against it over time. It is simply more convenient to use something with these qualities as a monetary base. And it happens that gold and silver has beaten out most other materials in fulfilling these criteria, and that gold beats silver. Here’s an article which goes more in depth.

Bitcoin beats gold on these criteria. Its supply is known by design to be no more than 21 million Bitcoin. A hard fork involving a majority of users agreeing to the change is required to change this supply ceiling. The ledger which records Bitcoin ownership is immutable. If internet exists, the network continues, and the digital coin remains durable. It is also much easier to move Bitcoin than gold.

We also live in an age where narratives carry supreme importance. Narratives are the means for making sense of the true reality which we observe. Today, there are too many ways to “observe” that people increasingly rely on narratives to shape their understanding of reality, and by extension their thoughts and actions. I’ve shown why Bitcoin theoretically works as money (fixed supply, durable, convenience of use), or at least as a monetary base the way gold has been and, in some way, still is (by being such large portion of central bank reserves). The importance of narratives is why I believe Bitcoin could, like gold, see adoption in central bank reserves.

The prevailing narrative is that Bitcoin is the champion of decentralized money and freedom, a libertarian paradise. An equally strong, though largely a strawman, narrative is that it is the go-to for money launderers. Therefore, most people see Bitcoin as inherently threatening to governmental power and many conclude that a serious Bitcoin crackdown is inevitable. But each action taken by governments of liberal democracies incurs a narrative. This is where it gets interesting. If there is already the narrative that governments’ tendency towards control creates the need for a decentralized currency, then a widespread crackdown in the West will only strengthen this point. People and institutions who own Bitcoin will obviously be against such an action.

Anyone who does a little research will discover that those who own Bitcoin became victims of the autocratic monetary control they were trying to protect themselves against. Politically, a baseless ban is a bad move. Banning something legitimizes it as a threat and draws more scrutiny from neutral citizens while peaking the ire of citizens with skin in the game (Note: I’m talking only about liberal democracies; authoritarian regimes like China can ban it without worrying about public perception). Therefore, the only way to do a ban is to manufacture a good reason.

However, besides illicit dealings, there is no evidence Bitcoin poses any threat to anyone. Recently, Bitcoin critics have turned to raising environmental concerns related to mining, but this is an argument which can apply to the limitless amounts of environmental hazards that a ban predicated on this would be regarded as unfounded. With that, democratic governments have either ignore or adopt as options. I think either one is bullish for Bitcoin but adopt is far more likely (and bullish).

As Bitcoin becomes more familiar to the public, the government will have a larger interest in taxing it. It makes no sense to ignore it entirely when there is tax revenue to be collected. Furthermore, greater publicity makes banning even more politically unwise. The only narrative left for democratic governments is to show that they do not mind Bitcoin and will try to adopt it. This accomplishes the objectives of holding some control (thereby saving face) while receiving a tax revenue (thereby profiting).

Past a certain threshold of Bitcoin’s publicity, this move will even be regarded as “innovative” and “bold” by the public, and the political party which implements it will be praised. We are moving towards that threshold each day as DeFi’s prevalence grows. When that threshold is reached, the controlling parties can easily implement adoption and take credit for making favorable changes. What else can they do if banning and ignoring are off the table?

When that happens, they need to determine how adoption will work. The best way for a government to adopt is to build central bank Bitcoin reserves. Bitcoin’s high network fees makes it hard to compete with centralized payment services, so it is unlikely to supplant fiat as a medium of exchange, much like how no one uses gold coins for transactions. The place for gold, and for Bitcoin, is in vaults. With Bitcoin, a “vault” is the private key to a government-owned address on the blockchain.

This movement has already started. When President Biden issued the executive order to look into crypto, it marked a milestone along the journey toward governmental adoption of DeFi. I believe they will find that there is no better way to “control” Bitcoin than by buying and locking much of it in an on-chain address while clarifying the auditing standards of out-of-vault Bitcoin transactions for tax purposes. After all, it is the same playbook for gold.

Lastly, enter central bank digital currency (or CBDC). Here, central banks have a much more compelling narrative by backing CBDC with Bitcoin reserves. Bitcoin in the reserve’s address is viewable on-chain, so the transparency of such a system would be enticing to the public. Central banks can transparently and easily move reserves amongst themselves. And having Bitcoin, the model of decentralization, backed CBDCs severely weakens the narrative that CBDCs are a way for governments to increase their control.

Bitcoin will probably not replace gold, but gold’s valuation as a function of the global monetary base is useful in estimating a reasonable Bitcoin valuation. VanEck has an article on this exact topic, estimating an upside of 33x and 16x for Bitcoin and gold, respectively. If we reduced this and assume gold to be at fair value, then by the same method, Bitcoin has a 33/16 = 2.06x upside. This estimate gets much larger as more M0 or systemic instability is introduced. The fact that it is superior to gold in terms of stock-to-flow and convenience of transaction is also a huge benefit.

The Bottom Line

It is reasonable to buy and hold some Bitcoin exposure. DeFi is taking off, and Bitcoin will only be pushed higher as people move toward using it as the de facto reserve asset of DeFi. While Terra’s move is extraordinary, it probably will not be the first as so much of DeFi is built by imitating what works and improving. Whether Bitcoin will see governmental sponsorship as a reserve asset is also something to watch. If gold has held its place in central bank reserves, it seems inevitable that the move by governments will be to adopt Bitcoin under a similar use case.

I explain here that BITO is now a good way to track Bitcoin because the contango in Bitcoin futures have subsided due to the ease of arbitrage between the spot and future markets. BITO also has a liquid options chain, allowing investors to sell covered calls on a weekly basis. Grayscale Bitcoin Trust (OTC:GBTC) is another source of exposure. However, the fund has a high expense ratio, and its non-redeemable structure allows very steep discounts to NAV.

Publicly traded Bitcoin miners offer exposure as well. However, many of them dilute by selling shares to finance mining equipment. Finally, one can always purchase Bitcoin directly from crypto exchanges like Coinbase, Binance, or FTX and transfer to a personal wallet. Bitcoin is obviously very volatile and has no chance of generating intermittent cash flows, so allocation should not exceed what one would have in commodities.

Be the first to comment