Andrii Yalanskyi/iStock via Getty Images

Investors that want diversified MLP exposure without the hassle of a Schedule K-1 are likely to prefer MLP products that issue a Form 1099. However, it is important for investors to understand the tax treatment of these investments and how it compares to directly owning individual MLPs. This piece discusses tax considerations for funds that largely own MLPs, while next week’s note will round out this series with an overview of exchange-traded notes and funds that own MLPs alongside corporations.

As a reminder, VettaFi is not an accounting firm or tax consultant, and this piece does not constitute tax advice. For details specific to your situation and investment, please consult your tax advisor.

The two types of MLP funds

Most investment funds are structured as Regulated Investment Companies (RICs), which function as pass-throughs, but RICs cannot own more than 25% MLPs. If any fund (mutual fund, closed-end fund, or ETF) owns more than 25% MLPs, the fund will be taxed as a corporation. Accordingly, there are two types of MLP funds – those structured as RICs, which own up to 25% MLPs, and those structured as corporations (or C-Corp funds), which tend to be 90-100% MLPs.

Given tax considerations, it is suboptimal to have a fund with just 50% or 60% MLPs, so investors are forced to choose between ~25% MLP exposure or predominantly MLP exposure. There are benefits to both types of MLP funds, and suitability ultimately depends on the needs of the investor as will be discussed more next week in explaining RICs and exchange-traded notes.

Tax considerations for C-Corp funds vs. direct investment in an MLP

The primary attraction of investing in MLPs through a C-Corp fund is achieving diversified exposure with a Form 1099 (no K-1), while enjoying many of the tax benefits associated with direct MLP investment. The trade-off is the potential tax drag caused by fund-level taxation as discussed below. Distributions from funds typically retain the tax character of the distributions received from their holdings.

As such, a C-Corp fund that predominantly owns MLPs will typically provide a higher and more tax-advantaged yield than a RIC. To put it another way, a C-Corp fund is likely to have a greater portion of its distribution be considered a tax-deferred return of capital (reported in box 3 on Form 1099-DIV), with any remainder taxed as a qualified dividend (box 1b on Form 1099-DIV).

Similar to direct MLP investment, return of capital distributions from a C-Corp fund lower an investor’s basis, and taxes are not paid on those return of capital distributions until the position is sold. If an investor’s basis falls to zero, future distributions are taxed at the long-term capital gains rate in the current year. An important difference between direct MLP investment and a C-Corp fund is the taxation of basis reductions at sale.

As discussed last week, basis reductions are taxed at ordinary income rates with a 20% deduction for investors that own individual MLPs (read more). For investors in C-Corp funds, the difference between the sales price and lowered basis is taxed at the long-term capital gains rate when held for more than a year. Additionally, investors in MLP ETFs or funds do not have to worry about potentially generating unrelated business taxable income in a tax-advantaged account (read more).

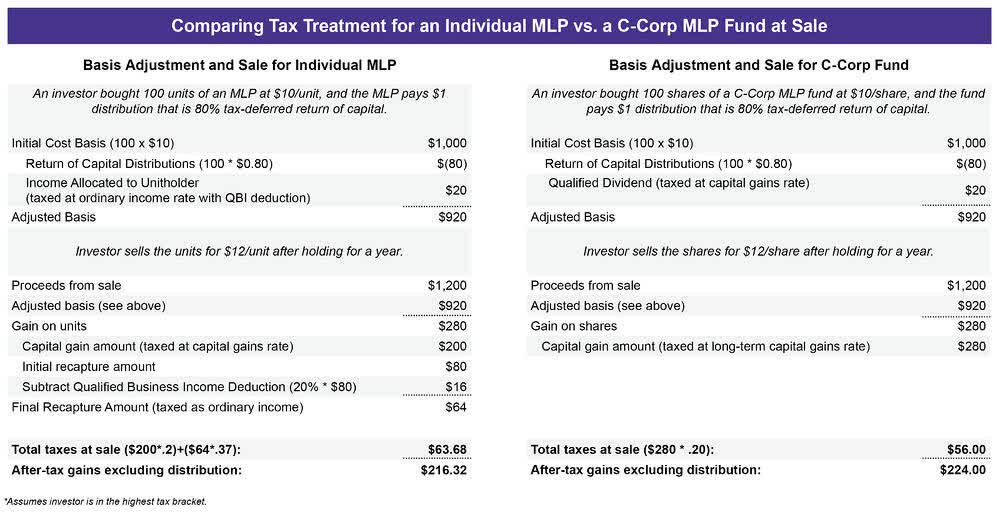

The example below compares the tax treatment for investment in an individual MLP with investment in a C-Corp MLP fund under similar circumstances. In addition to the taxation for basis reductions, another key difference is the tax treatment for the portion of the distribution not considered a tax-deferred return of capital.

When owning an individual MLP and in the highest tax bracket, the effective tax rate on the $20 in income (i.e., the portion of the distribution not considered a tax-deferred return of capital) and the basis reductions (recapture) would be 29.6%, which incorporates a 37% personal tax rate and the 20% qualified business income (QBI) deduction. An owner of a C-Corp fund would pay long-term capital gains rates on the qualified dividend (i.e., the portion of the distribution not considered a return of capital) and basis reductions at 20%.

Note that the C-Corp fund and its investors are not eligible for the 20% QBI deduction. On the surface, the C-Corp fund appears advantaged based on the bottom-line number, but there are other nuances to keep in mind.

One disadvantage of investing in a C-Corp fund instead of individual MLPs is the potential for tax drag to weigh on fund performance relative to its underlying holdings. C-Corp funds accrue a deferred tax liability for the portion of distributions considered to be a tax-deferred return of capital and for gains in underlying holdings. When a fund is in a net deferred tax liability status, a 10% increase in the underlying holdings may only result in a 7.7% increase in the fund given a 21% corporate tax rate and approximately 2% for state income taxes.

If a C-Corp fund is in a net deferred tax liability status with 23% tax drag, the 20% gain in the fund corresponds to a 26% gain in the underlying holdings [(0.26*(1-0.23))=0.20]. In other words, without the tax drag, the sales price could be $12.60 instead of $12 assuming the fund was in a net deferred tax liability status for the entire period owned. The websites for C-Corp funds will typically list their deferred tax liability or asset/valuation allowance.

So what?

A fund that predominantly owns MLPs provides the potential for tax-deferred income with additional conveniences relative to direct investment in an MLP, namely diversified exposure, a Form 1099 instead of a K-1 and no need to worry about UBTI in tax-advantaged accounts. Depending on the tax position of the MLP fund, tax drag can offset some of those benefits. For a US taxable investor (1) comfortable with filing K-1s and state taxes and willing to do research to choose individual MLPs, the most tax-efficient way to own MLPs is to buy them directly.

Stay tuned for next week’s note, which will discuss other ways to access the MLP space (RICs, ETNs) and the trade-offs between these different types of products.

Footnotes(1) This means an investor who is taxed in the US and investing in a taxable account – not an IRA, 401(K) or other tax-advantaged vehicle. |

Disclosure© Alerian 2022. All rights reserved. This material is reproduced with the prior consent of Alerian. It is provided as general information only and should not be taken as investment advice. Employees of Alerian are prohibited from owning individual MLPs. For more information on Alerian and to see our full disclaimer, visit http://www.alerian.com/disclaimers. |

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Be the first to comment