Drew Angerer

One of Thursday’s biggest winners in the market was Beyond Meat (NASDAQ:BYND). The plant based meat company saw its shares rally more than 9% on the day, even after backing a bit off their daily highs, as the company announced a new product offering in partnership with McDonald’s (MCD). While it was nice for longs to see this beaten down name rally a bit in percentage terms, the jump was likely just another opportunity to sell.

Thursday’s announcement was that the Double McPlant burger, featuring two Beyond Meat patties, will be rolled out in all restaurants across the UK & Ireland on January 4th, 2023. Shares were up more than 15% at one point, but ended the day with a gain just short of double digits, percentage wise. Unfortunately, volume was only about 20% above the 3-month average, which isn’t the strongest sign of investor confidence in my opinion.

While adding more sales is usually a good thing, the amount here may not be very material in the short term. In the company’s Q3 2022 earnings report, international food service revenues were just $10 million, or a little more than 12% of the company’s total. Worse yet, the Q3 revenue figure for this segment was down more than 42% from the year ago period. At the end of that period, the international food service had the smallest number of distribution outlets of the company’s four major divisions.

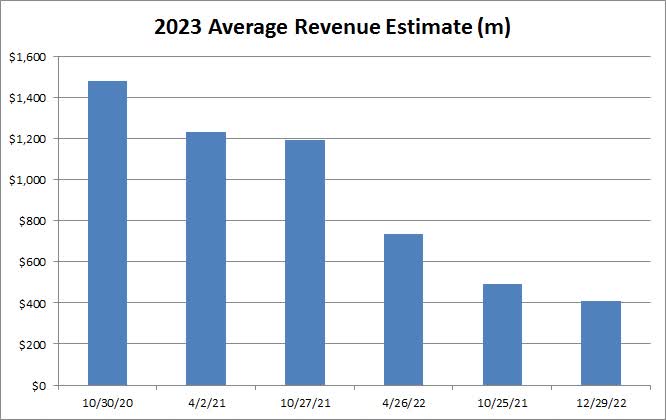

When I discussed that ugly earnings report back in November, I mentioned the company’s very dismal Q4 revenue guidance. Management took down its full year forecast for revenues to a range of $400 million to $425 million versus a street consensus of nearly $427 million. The high end of that guidance was cut by nearly $200 million in just a couple of quarters. In just the past 26 months, revenue estimates for the 2023 year about to start have absolutely cratered, as the chart below shows.

2023 Average Revenue Estimate (Seeking Alpha)

The company has had aggressive growth targets over the years, but this business has failed to take off as investors were hoping. As a result, the expense structure has gotten way out of whack, with gross margin dollars being negative in Q3, including some one-time items. Even still, the net loss was over $100 million, and while 2023 is expected to be better than 2022, the company is still projected to lose a few hundred million.

In the Q3 earnings release, management said it is targeting cash flow positive operations within the second half of 2023. However, the company has burned about half a billion in cash in the last twelve months, ending in September, finishing the period with $390 million. It remains to be seen what will happen in the next few quarters, but I still believe a capital raise is possible. That’s not an appetizing thought with the surge in interest rates combined with the stock’s fall from its 52-week high of $74 to nearly single digits currently.

At this point, the street doesn’t see much upside for the name. Since that Q3 earnings report, the average price target has dropped from $18.30 to $13.00, implying less than 5% of upside from Thursday’s close. Just 16 months ago, the street saw this name being worth more than $120, but another bad quarter or two will probably mean an average price target that will end up in the single digits.

In the short term, I’ll be watching to see if the stock can significantly improve its technical setup. As the chart below shows, shares are currently below their 50-day moving average (orange line). If the stock cannot get above this key technical trend line soon, it likely will pull back further as the 50-day will continue to head lower. For the stock to breakout, we need to see shares get over this line and get the 50-day to move higher.

BYND Last 6 Months (Yahoo! Finance)

In the end, Thursday’s rally in shares of Beyond Meat might just be another chance to sell the stock. The company announced a new Double McPlant burger with McDonald’s, but the rollout is only for the UK and Ireland. The international food service market is rather small right now for the company, and sales in Q3 plunged over year ago levels. As analysts continue to cut 2023 estimates, the name has a lot to prove, and perhaps a capital raise is needed. Unless the business improves significantly in the short term, I still think that single digits are possible here unless the overall market has a big bounce next year.

Be the first to comment