Olivier Le Moal/iStock via Getty Images

BioCryst Pharmaceuticals, Inc. (NASDAQ:BCRX) is a biotechnology company developing complement-mediated and rare disease treatments. The company leverages a structure-guided drug design process that integrates biology and medicinal chemistry to generate therapeutics for diseases with unmet medical needs. BCRX has Orladeyo (berotralstat), which represents 95.8% of total revenues, and royalties from Rapivab (Peramivir) injections. Unfortunately, BCRX is heavily leveraged, but I believe it has a reasonable pathway toward deleveraging through Orladeyo’s future growth, unlocking significant shareholder value. Thus, I rate it a “strong buy” for investors who understand the inherent biotech and financial risks embedded.

Orladeyo: Business Overview

BioCryst Pharmaceuticals was founded in 1986 and headquartered in Durham, North Carolina. The company develops small molecules and protein therapies for complement-mediated and rare diseases. BCRX’s key differentiator is its drug design, which integrates biology and medicinal chemistry to create new molecules for diseases with unmet medical needs.

Source: Corporate Presentation. May 2024.

Currently, BCRX has two FDA-approved drugs, Orladeyo (berotralstat) and Rapivab (Peramivir) injections. The FDA approved Orladeyo in December 2020 as the first oral, once-a-day therapy to prevent attacks of hereditary angioedema [HAE] in patients 12 years and older. HAE is a rare genetic condition generated by mutations in the SERPING1 gene that encodes the C1 inhibitor protein related to regulating inflammation and clotting modulation. This disease produces severe swelling in the extremities, face, and gastrointestinal tract and can cause life-threatening airway obstruction.

Since 2020, Orladeyo has expanded its approvals into the EU as the first oral treatment to prevent HAE attacks. As of 2024, Orladeyo was officially launched in Italy in February. Additionally, the drug continued expanding its approvals into Brazil, Mexico, and Peru. Clearly, Orladeyo is BCRX’s main value driver. This is why management focuses on extending its international market potential. So far, these efforts have paid off, as Orladeyo’s revenues grew 30% in Q1 2024. BCRX projects Orladeyo will generate $390 million to $400 million in revenues in 2024.

Source: BCRX’s latest 10-Q report.

On the other hand, Peramivir was first FDA-approved for influenza in December 2014. Then, in 2017, its approval was extended for pediatric indications. Finally, in 2021, the approval expanded to include children six months and older. Peramivir is a commercially available drug used as an antiviral for acute uncomplicated influenza. Its mechanism of action [MoA] blocks the neuraminidase enzyme on the influenza virus’s surface, limiting infection. However, Peramivir is just a royalty revenue source for BCRX, and as of Q1 2024, Orladeyo represented 95.8% of total revenues.

Source: Corporate Presentation. May 2024.

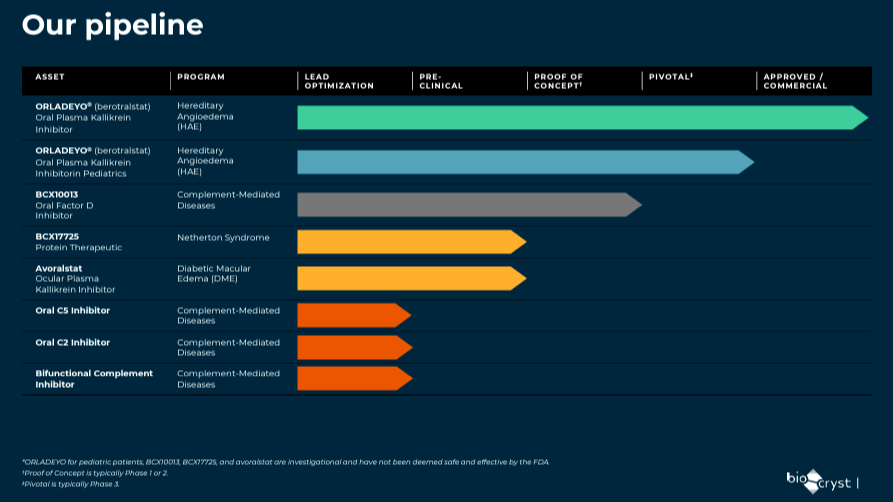

Moreover, BCRX’s pipeline includes Orladeyo in the pivotal phase for HAE in pediatric patients. The company also has BCX10013 as a proof of concept for complement-mediated diseases and BCX17725 in the pre-clinical stage as a protein therapeutic indicated for Netherton Syndrome. BCRX’s pipeline also has Avoralstat as a proof of concept for diabetic macular edema [DME], and early clinical trials are underway. Lastly, the company is also developing an Oral C2 inhibitor, Oral C5 inhibitor, and Bifunctional complement inhibitor for complement-mediated diseases in the “lead optimization” phase.

Enhancing Orladeyo: Clinical Successes and Approvals

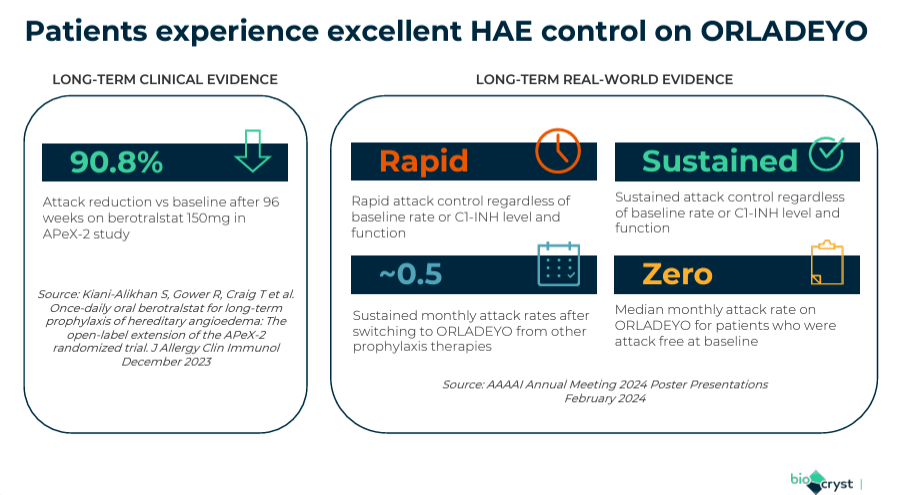

More recently, on June 2, 2024, BCRX presented real-world evidence demonstrating decreases in attack rates using Orladeyo. The results were announced at the European Academy of Allergy and Clinical Immunology [EAACI] Congress in Valencia, Spain. Orladeyo provided rapid and sustained control of HAE attacks.

The takeaway is that patients switching to Orladeyo from other prophylactic treatments had monthly attack rates of around 0.5. Additionally, patients with no attacks at baseline continued to have zero attacks on Orladeyo but with fewer side effects. Thus, this new data corroborates Orladeyo’s efficacy and safety profile for HAE patients 12 years and older. If further verified in future trials, Orladeyo’s C1 inhibitors could become preferable to androgens for long-term prevention.

Source: Corporate Presentation. May 2024.

It’s worth noting that considerable favorable regulatory decisions from countries such as Argentina, Chile, Brazil, Mexico, Peru, and Italy recognize Orladeyo’s benefits. I believe this corroborates BCRX’s IP potential in HAE, especially given its negligible side effects, typical in traditional androgen therapies. Moreover, if BCRX delivers on its Orladeyo revenue growth projections, it could potentially lead the company into operating profits by 2025.

Compelling GARP: Valuation Analysis

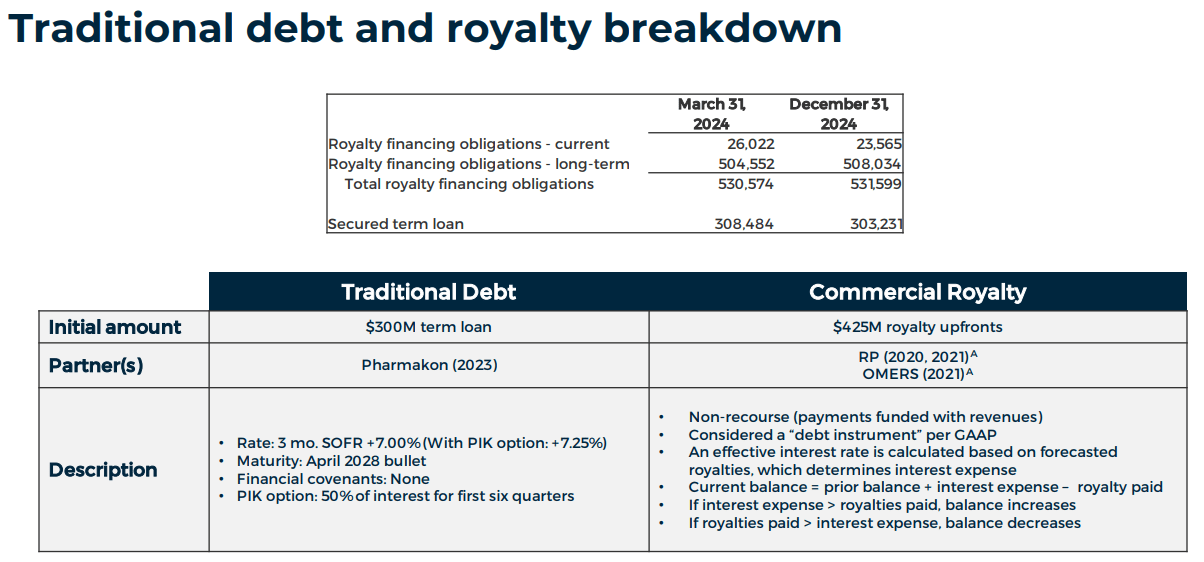

BCRX trades at a $1.5 billion market cap from a valuation perspective, making it a mid-sized biotech. Its balance sheet holds $84.3 million in cash and equivalents and $252.2 million in short-term investments, totaling $336.5 million in available short-term liquidity. BCRX also has $944.1 million in total liabilities, with $530.6 million being royalty obligations collateralized by Orladeyo’s US and some European markets’ future royalty sales. These are sizeable liabilities, which cause BCRX’s negative book value of -$476.2 million. BCRX also has a secured long-term loan of $308.5 million, maturing in 2028.

Source: Corporate Presentation. May 2024.

Using the company’s latest 10-Q data, I calculate that 90.0% of Orladeyo’s total sales come from the US. This explains why BCRX is also working on expanding Orladeyo’s approvals into South America. I also estimate the company’s latest quarterly cash burn was $53.5 million, which is considerable compared to its $336.5 million in available short-term funds. This implies a short cash runway of about 6.3 quarters. However, the company is quickly ramping up its revenues.

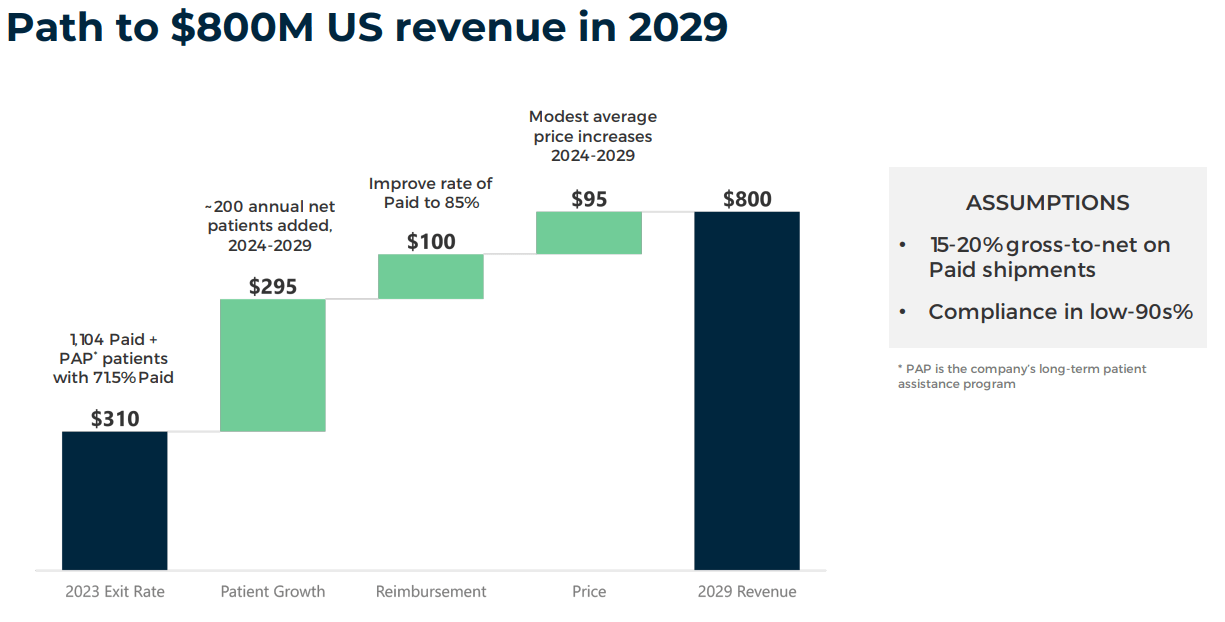

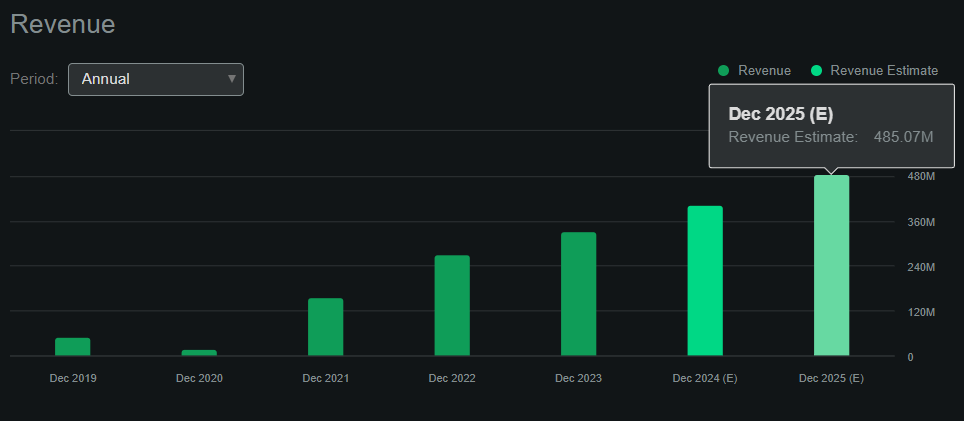

According to Seeking Alpha’s dashboard on BCRX, it’s projected to generate $485.1 million in revenues by 2025 (20.7% YoY growth). In fact, by 2029, the company expects to produce $800.0 million in revenues from the US alone. In Q1 2024, BCRX’s gross margins grew to 48.4% while reducing operating expenses to $59.4 million from $64.0 million in Q4 2023.

Therefore, if operating expenses remain flat, the company’s EBIT should turn positive by 2025. Hence, it’s reasonable to expect BCRX’s cash runway to be sufficient if revenues continue increasing at these margins. For context, my back-of-the-envelope estimate for BCRX’s breakeven EBIT is $120.0 million in quarterly revenues at 50.0% gross margins, which should be enough to offset the current quarterly operating expenses run rate of about $60.0 million. For context, that would be $480.0 million in annualized revenues, which aligns with 2025’s revenue projections.

Source: Seeking Alpha.

Given BCRX’s considerable liabilities, I believe it’s best to value it through its enterprise value. In this calculation, I’ll include its royalty obligations and secured loan. Hence, I estimate BCRX’s EV is approximately $2.0 billion. This means it trades at a forward EV/sales multiple of 4.2. This is slightly higher than the sector’s median forward 3.8 EV/sales ratio. However, BCRX’s projected revenue growth of 21.4% is considerably higher than its sector’s growth of just 8.8%. Thus, BCRX’s slightly higher EV/Sales ratio seems cheap due to its above-average growth. Hence, I believe BCRX is a compelling GARP stock with a solid bull base based on Orladeyo’s prospects, so I rate it a “strong buy” at these levels.

Investment Caveats: Risk Analysis

Naturally, the main risk is BCRX’s high dependency on Orladeyo. If this drug faces any regulatory setbacks or becomes outclassed by new potential competitors, it would be a significant blow to the company’s bull case and main revenue source. This would undoubtedly translate into meaningful shareholder losses. Moreover, Orladeyo’s past revenue growth is not guaranteed to persist. If future growth disappoints, it could delay BioCryst’s efforts toward deleveraging its balance sheet. Biotech is highly dynamic, and the current revenue projections might not materialize if new competitors outclass Orladeyo.

Source: TradingView.

It is also worth mentioning that BCRX currently has a short cash runway of just 6.3 quarters. My bull case assumes that the company’s future revenue growth will solve this issue, but this isn’t guaranteed. If revenue slows down or margins contract, it could also force BCRX to raise additional funds, likely through equity, because it’s already heavily indebted. Nevertheless, I believe that Orladeyo’s prospects are promising based on the data we have available today. If Orladeyo delivers on its potential, the upside potential is significant as it can quickly reduce its liabilities and unlock considerable shareholder value.

Strong Buy: Conclusion

Overall, BCRX is a bet on Orladeyo’s prospects. In my view, this is a reasonable bet because of its proven market adoption, forecasted revenue growth, and multiple favorable regulatory decisions across several jurisdictions. While I recognize this is not without risks, I believe BCRX has a reasonable pathway towards deleveraging its balance sheet through Orladeyo’s future growth, unlocking significant shareholder value. Thus, I rate BCRX as a “strong buy” for investors who understand embedded risks.

Be the first to comment