Banking is a game of protecting from the downside. It appears Brian Moynihan’s got some catching up to do, but his bank is increasing efficiencies as more and more consumers gravitate to its online platforms. The formula is simple: buy back shares, reduce costs, and benefit from a resilient U.S. consumer. This should lead shareholders to long-term returns of 10% per annum and beat the S&P 500.

CEO Talk And Stress Tests

We’ve noticed a strange phenomenon on Wall Street. Analysts listen intently to quarterly earnings calls, and small remarks by CEO’s often swing market caps by the tens of billions. For example, Jamie Dimon and his CFO have discussed the possibility of an economic hurricane, as well as a Paul Volcker style recession, sending JPMorgan Chase (JPM) shares plummeting. Meanwhile, in our opinion, Brian Moynihan’s pretended everything’s fine and dandy on earnings calls. Moynihan’s a constant cheerleader for BAC shares, the U.S. consumer, and the CNBC crowd. At the same time, he seems to dodge questions about what could go wrong and about Bank of America’s poor results on the Fed stress test. Reuters reported:

“Shares in the biggest U.S. banks rallied on Friday after they passed the Federal Reserve’s annual health check, but Bank of America (NYSE:BAC) underperformed with test results implying it needs a larger-than-expected capital buffer, which could limit share buybacks and dividends.”

It appears Bank of America is behind the curb in building loan-loss provisions and capital buffers when compared to its peers. This could cause BAC’s earnings to underperform in the quarters ahead.

Warren Buffett has often said that he prefers honest management, but his two largest positions are run by Tim Cook at Apple (AAPL) and Brain Moynihan at Bank of America. In our opinion, these CEO’s are constantly championing their stocks.

The Digitalization Of Operations

The digitalization of Bank of America’s operations is a huge boon for the company’s profits. The more consumers use online banking, the less staff and retail locations Bank of America needs. This is a huge factor in reducing costs over time. The company has a fantastic mobile banking experience. Their app has a nearly 5 star rating on both the App Store and Google Play. And, consumers are favoring mobile banking more and more. Bank of America reported:

“The bank’s clients logged in to its digital platforms a record 10.5 billion times in 2021, a year-over-year increase of 15%.

Mobile Banking (Bank Of America)

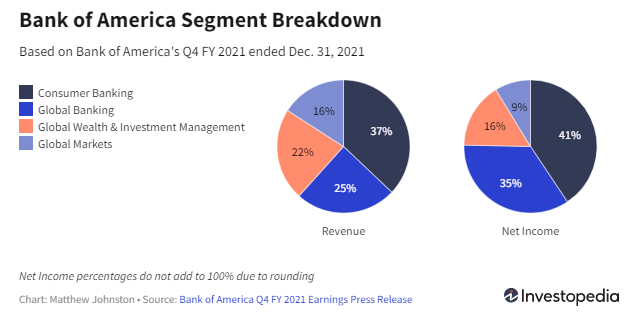

The Asset Breakdown

Segment Breakdown (Investopedia)

It’s important to note here that Bank of America is more exposed to investment banking than many believe. Global Wealth Management and Global Markets made up 25% of the company’s net income in 2021. The company purchased Merrill Lynch for $50 billion back in 2008.

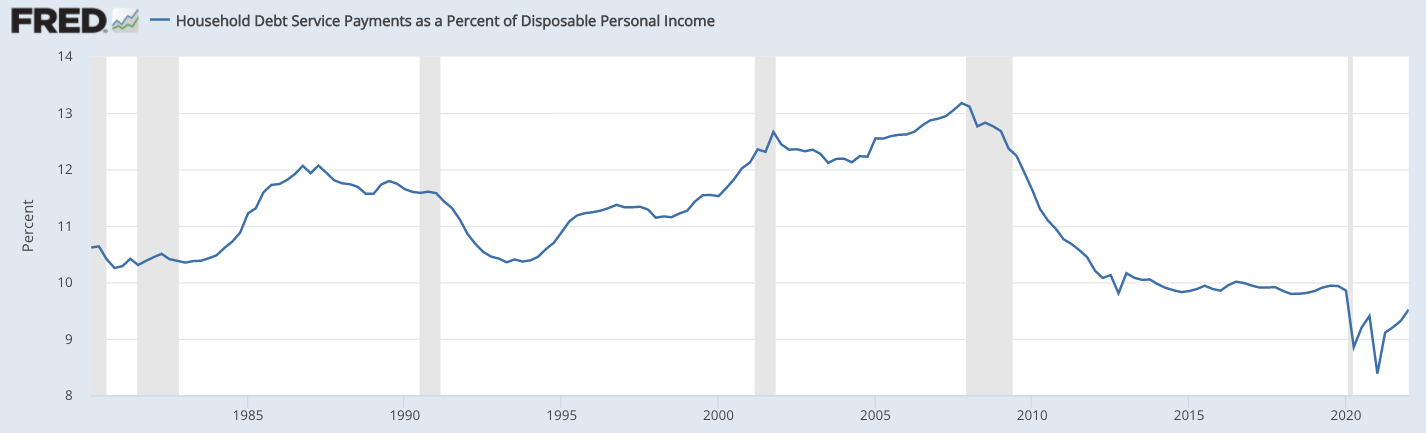

Bank of America’s largest segment, Consumer Banking, provides bank accounts, debit cards, credit cards, mortgages, and other loans to U.S. consumers and small businesses. We believe the American consumer is financially resilient, especially compared to consumers around the world, struggling with high levels of household debt. Debt payments relative to income are still sitting around historic lows in the United States:

U.S. Household Debt Service Payments As % Of Disposable Income [FRED]

Household debt to GDP has also come way down since the Global Financial Crisis:

U.S. Household Debt To GDP (Trading Economics)

Long-term Returns

We’re sticking to our 2032 price target that we outlined in our article: Bank of America: A Bear Market Buy. The stock is up almost 8% since that time. Our 2032 price target was and still is $73 per share, implying returns of 10% per annum with dividends reinvested.

We think BAC’s normalized earnings are around $3 per share, and that the company can grow those earnings at 6% per annum as it benefits from reduced costs, higher interest rates, share buybacks, and the growth of the U.S. economy. This gives you 2032 EPS of $5.4 per share. We’ve applied a terminal multiple of 13.5x earnings.

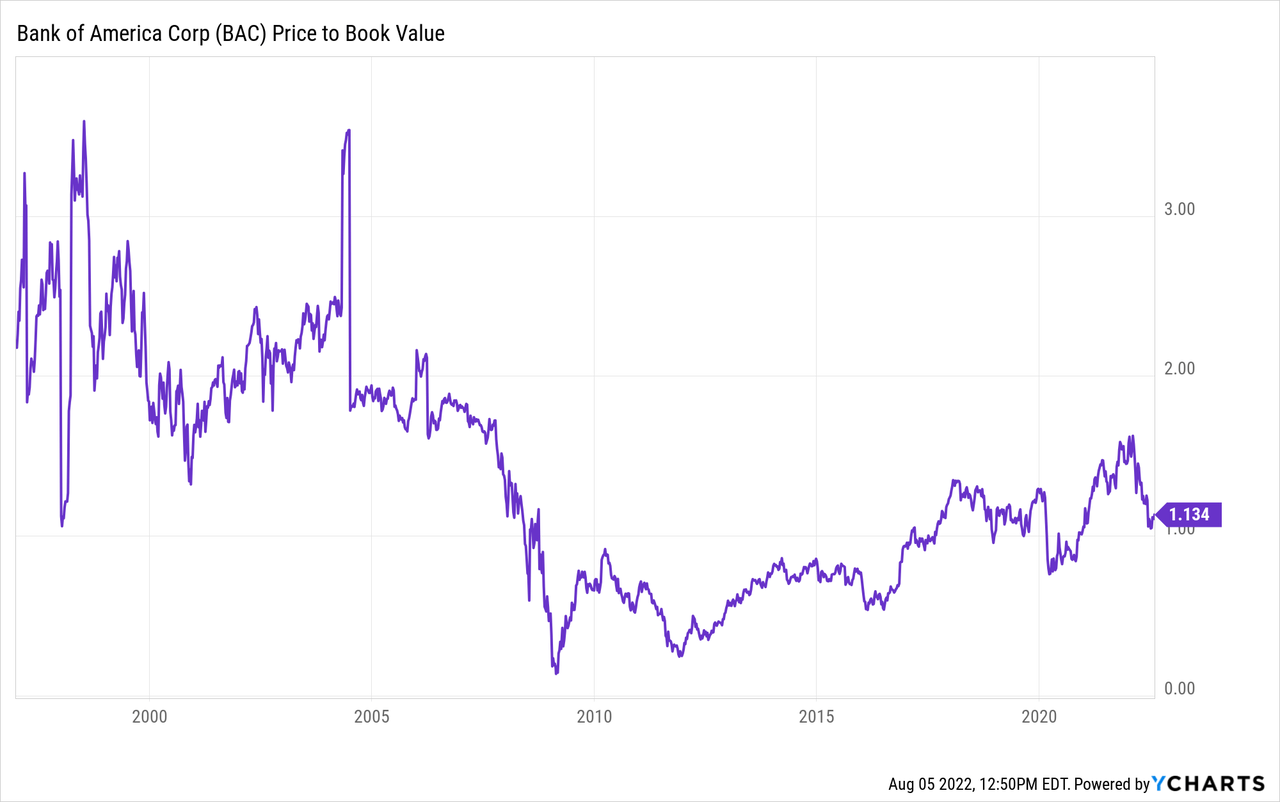

At 1.1x book value, there’s no way we’d consider selling Bank of America. It’s not out of the realm of possibilities that the company trades at 2x book in 5 to 10 years as it did in the early 2000’s:

Stanley Druckenmiller is warning of a recession and further stock market declines in 2023. Given the large rallies in asset prices through 2020 and 2021, this should be expected. Unemployment tends to reach extremely low levels right before it spikes. This will put the strength of BAC’s assets to the test, and like we said before, Bank of America should build more loan-loss provisions. While this could cause a decrease in short-term earnings, we’d encourage investors to focus on normalized earnings.

In the long-term, Bank of America is dependent on what interest rates do. We believe interest rates will settle around 5%, which would benefit the bank. But if they drop back to zero or spike too high, it could adversely affect BAC. High interest rates hurt demand and low interest rates create indebted stagnation like we’ve seen in Europe and Japan.

Conclusion

Bank of America is a great investment, with strong prospects of beating the S&P 500 in the decade ahead, but it’s time to prepare for the worst. As consumers gravitate to online banking, BAC is leading the industry and reducing costs. The company has a simple and effective formula for increasing EPS and should benefit from multiple expansion as the market realizes the enduring nature of its business. At the same time, the company has more investment banking exposure than people think. As a recession looms, BAC needs to build capital. We wouldn’t even think about selling at 1.1x book, and have a “buy” rating on the shares.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment