Berkut_34

Investment Thesis

Baker Hughes Company (NASDAQ:BKR) is a large oilfield services company. With oilfield stocks performing very strongly into this earnings season, investors had hoped to be blown away.

However, that was not to be. The main culprit here is the impact of expected inflation and working capital is a headwind in 2023.

Put another way, even though Baker Hughes’ guidance points to revenues being up as much as 20% y/y, its bottom line free cash flow will not sizzle quite as much.

Altogether, this is a mixed investment opportunity.

BKRQ4 Earnings Less Than Expected

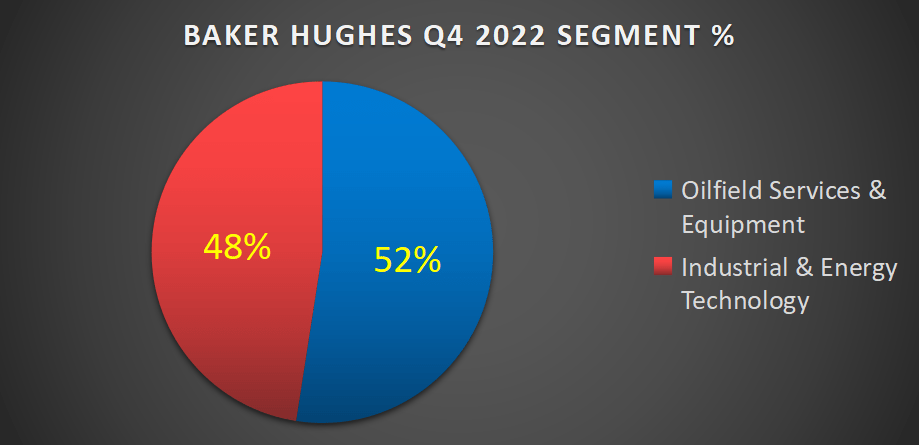

As a reminder, Baker Hughes now has only two segments, down from 4 segments in Q3 2022 after the company opted to restructure and re-segment its business.

Accordingly, this means that its operating profits are split roughly 50/50.

BKR operating income Q4 2022

Or more accurately put, they are now approximately equally split. And that’s because Baker Hughes’ Oilfield Services & Equipment (”OFSE”) increased nearly 50% y/y.

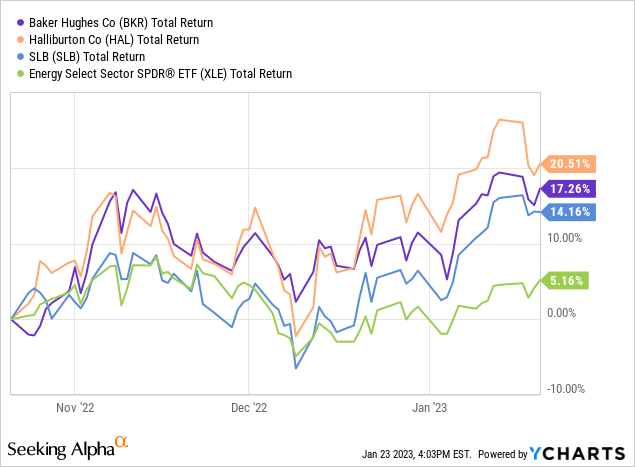

Nonetheless, beyond its re-segmentation, investors had wanted more. Particularly when you consider that the oilfield sector had been on fire in the past 3 months.

Also, keep in mind that each one of the main companies in this space not only outperformed the Energy ETF (XLE), but also the S&P500 (not shown).

As Baker Hughes’ management held its earnings call from Italy, its management described the impact that inflation continues to have on its operations, most notably within its Industrial & Energy Technology (”IET”) segment, which saw its operating income drop 5% y/y in Q4.

Needless to say given the strong performance of BKR into its earnings print, the one thing that investors didn’t want to hear was a slowdown anywhere.

After all, investors have been fearful for a while that either high inflation or a potential global economic slowdown could weigh on its near-term prospects. Or in the worst case, both of these headwinds coming together in 2023.

Baker Hughes’ Balance Sheet Gets in The Way of the Bull Case

At the surface level, it could be said that the highly cash flow generative Baker Hughes brings in more than enough cash flows to support the debt on its balance sheet, and at the same time allowing the company to be rated investment grade. And still, on top of that also return significant capital back to its shareholders.

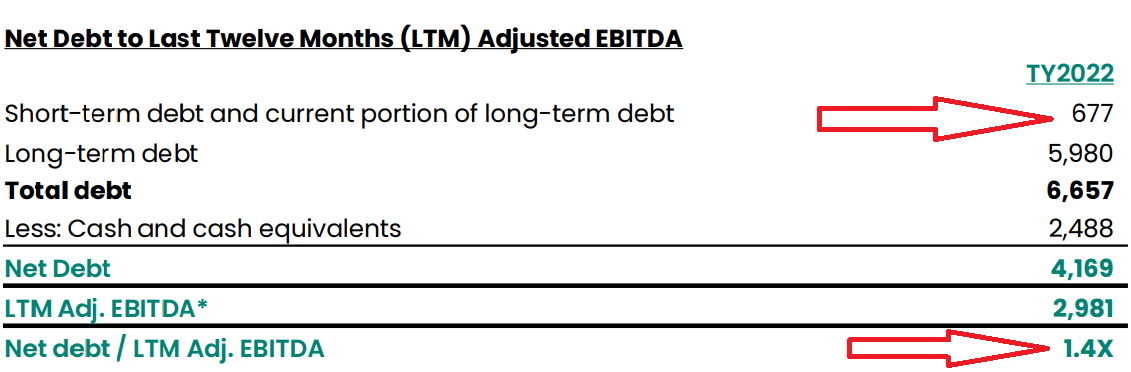

The more nuanced discussion points to the two red arrows seen below.

Baker Hughes Q4 presentation

What the top arrow points to is Baker Hughes’ more than $640 million of debt due in December 2023. This will get in the way of Barker Hughes increasing its commitment to returning capital to shareholders.

Meanwhile, the second arrow is a reminder that we are now approaching the mid-cycle in the oil market, and Baker Hughes still is fairly leveraged. At this stage, Baker Hughes needs to start being aggressive and chip away at its debt.

2023 Free Cash Flow Guidance, Discussed

For 2022, Baker Hughes’s free cash flow was $1.1 billion, down from $1.8 billion in 2021.

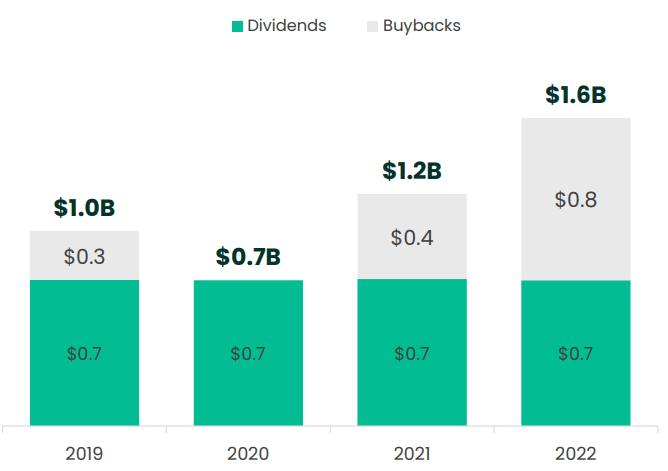

That being said, despite its free cash flow being down y/y, this didn’t get in the way of Baker Hughes returning significant capital back to shareholders.

Baker Hughes Q4 presentation

In fact, as you can see in the graphic above, Baker Hughes ended 2022 by returning $1.6 billion back to investors, despite only bringing in $1.1 billion of free cash flow in 2022.

Hence, on a trailing basis, Baker Hughes returned a 5.2% yield via dividends and share repurchases. This high combined yield was driven by Baker Hughes returning more capital to shareholders than the free cash flow it produced over the whole of 2022.

Furthermore, during the earnings call, Baker Hughes’ CFO Nancy Buese guided that,

[Baker Hughes] will continue to target 50% free cash flow conversion from adjusted EBITDA on a through cycle basis but expect[s] 2023 to be in the low to mid 40% range.

Consequently, what Buese is declaring is that although Baker Hughes ended 2022 sizzling strong, investors that are now looking ahead to 2023 should expect somewhere close to $1.7 billion of free cash flow, at the high end of its guidance.

However, given that Baker Hughes is only committing to returning 60-80% of free cash flow to shareholders in 2023, that means that in the best case, the 2023 capital return will be around $1.4 billion; a slight drop from 2022.

The Bottom Line

The bad news is that Barker Hughes’ free cash flow and capital return in 2023 won’t be as strong as its capital return program in 2022.

Having said that, an investment in Baker Hughes can be seen to be enticing for investors who have a strong belief in the possibilities of the medium-term oil cycle.

On the other hand, beyond its slightly weaker free cash flow, Baker Hughes Company’s balance sheet is also rather leveraged, in my opinion. Overall, I think there are better opportunities within the oil services industry than Baker Hughes Company.

Be the first to comment