zorazhuang

Thesis

Baidu (NASDAQ:BIDU) reported excellent Q3 2022 results, beating analyst estimates with regards to both revenue and earnings. Moreover, with the tailwind of an improving COVID situation in China, management also gave an upbeat outlook for Q4 and going into 2023.

Personally, I remain super bullish on Baidu stock – both as a function of valuation and future potential anchored on AI business initiatives. And on the backdrop of EPS upgrades, I raise my target price for Baidu stock to $256.90/share, as compared to $237.80/share prior.

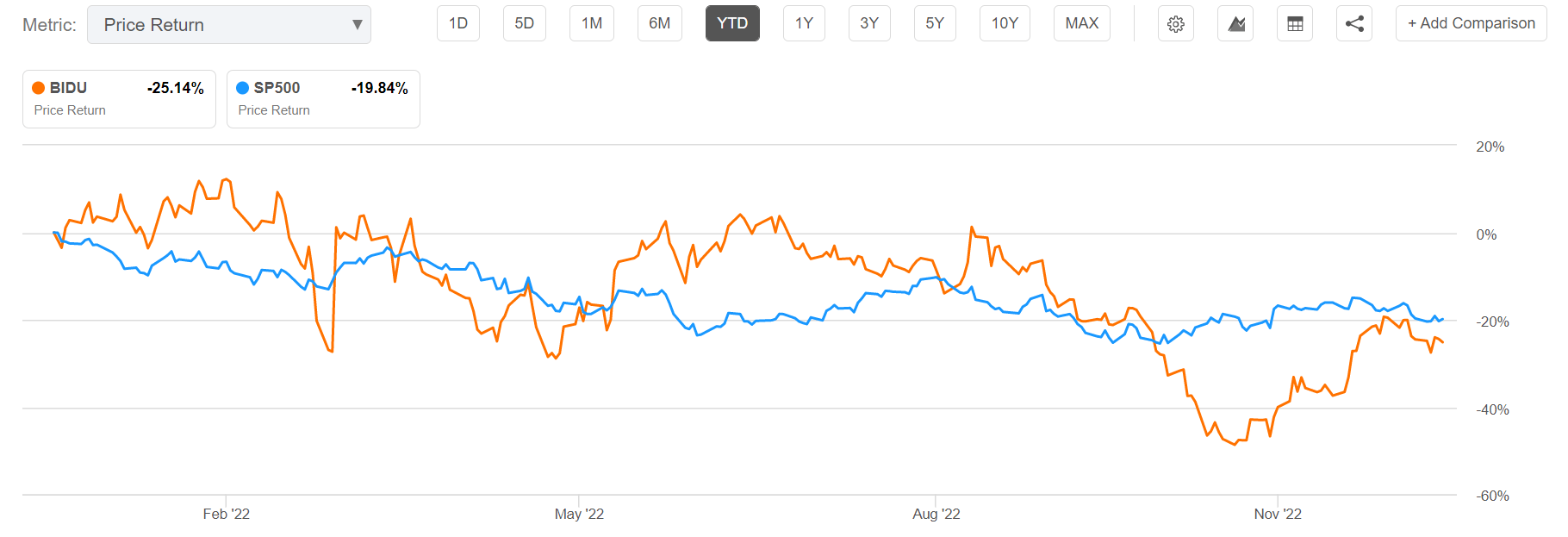

For reference, Baidu stock is down about 25% YTD, as compared to a loss of approximately 20% for the S&P 500 (SP500).

Seeking Alpha

Stronger Than Expected Q3 Results

Although Baidu’s September quarter was still pressured by COVID headwinds and other macroeconomic challenges, the internet giant posted strong results – beating analyst consensus estimates with regards to both revenue and earnings.

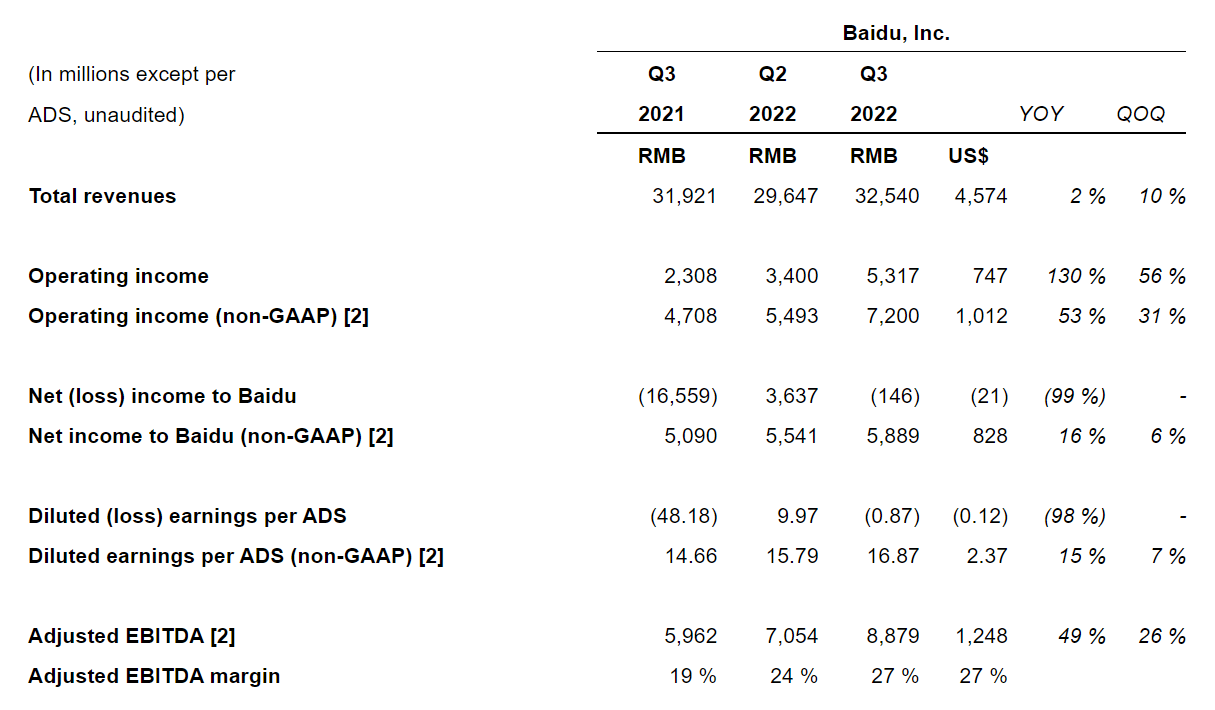

During the period from July to the end of September, Baidu generated total revenues of approximately $4.57 billion, which compares to about $4.48 billion for the same period one year earlier (10% year over year growth), and $4.15 billion for Q2 2022 (10% quarter over quarter growth). Analyst had expected revenue of about $4.51 billion ($60 million beat)

During Q3, Baidu also improved profitability and reported operating income of $747 million, representing a 130% year-over-year growth versus the same period one year earlier, and a 56% quarter over quarter growth as compared to Q2.

Adjusted net income expanded about 4.5% year-over-year, to $4.2 billion; and EPS came in at 96 cents, which is approximately 6 cents more than what analyst consensus expected. Earnings per ADS came in at $2.37, which beat analyst consensus estimates by 12 cents.

Baidu Q3 2022 Results

Other highlights for the quarter include:

Share buy-backs: During the September quarter, Baidu returned $272 million to shareholders, which translates into an annualized equity yield of approximately 2.5%.

AI Cloud revenue expanded by approximately 25% year over year and now accounts for almost 30% of the internet giant’s total revenues. Moreover, Baidu reported that the company’s ACE smart transportation solutions are now adopted in 63 cities, and have reached a cumulative contract value of about RMB630 million.

Intelligent Driving: Baidu’s robo-taxi platform Apollo Go completed approximately 474K rides in Q3 2022, which reflects a 311% year over year growth and a 65% quarter over quarter growth.

Mobile Ecosystem: In Q3, Baidu App’s MAUs grew to 634 million, which is a 5% year over year increase versus Q3 2021.

Reflecting on strong Q3 results, Baidu co-founder and CEO Robin Li commented: (emphasis added)

Baidu Core delivered a solid set of financial and operational results in the third quarter, despite the continued challenges posed by the COVID-19 resurgence. Baidu Core’s revenue resumed positive growth, driven by a gradual recovery of our online marketing business and the steady growth of our AI Cloud revenue. Notably, we continued to make significant progress in intelligent driving. On the one hand, Baidu Apollo’s auto solutions continued gaining popularity amongst leading automakers. On the other hand, Apollo Go continued scaling up its operation, completing more than 474,000 rides in the quarter, further strengthening its leading position in the global autonomous ride-hailing market

Looking ahead, we expect our mobile ecosystem to continue generating strong cash flow and fund our investment in AI Cloud and intelligent driving, which will help maintain our leadership in the new AI business and drive long term business growth.

Confidently Stepping Into Q4 And Early 2023

With the COVID lockdowns easing, Baidu management voiced a positive outlook for Q4 2022 and early 2023. In the analyst Q&A session following Q3 results, Baidu CEO Robin Li said:

In Q3, Baidu Core ad revenue was down 4% year-over-year, but improved from the second quarter’s 10% year-over-year decline, as macro has improved gradually since June. Encouragingly, revenues from healthcare and retail recorded positive year-over-year growth in the quarter.

And following a question from Alicia Yap (Citigroup) how analysts should think about the recovery in advertising revenue, Robin Li added:

I think the short-term will probably still be quite volatile, but the economy should improve in the mid-term and beyond. China has been fighting against this COVID for almost three years and the country has been gaining experience.

Our revenues are very sensitive to COVID control measures …

… So, once COVID and macro situations improve, our ad revenues from different verticals such as travel, franchising or local services should rebound.

Baidu’s confidence around Q4 and 2023 is in line with what analyses of major investment banks. With zero-COVID restrictions lifting, Goldman Sachs sees China’s economy expand by 4.5% in 2023, and Morgan Stanley estimates GDP growth for 2023 at 5.4%.

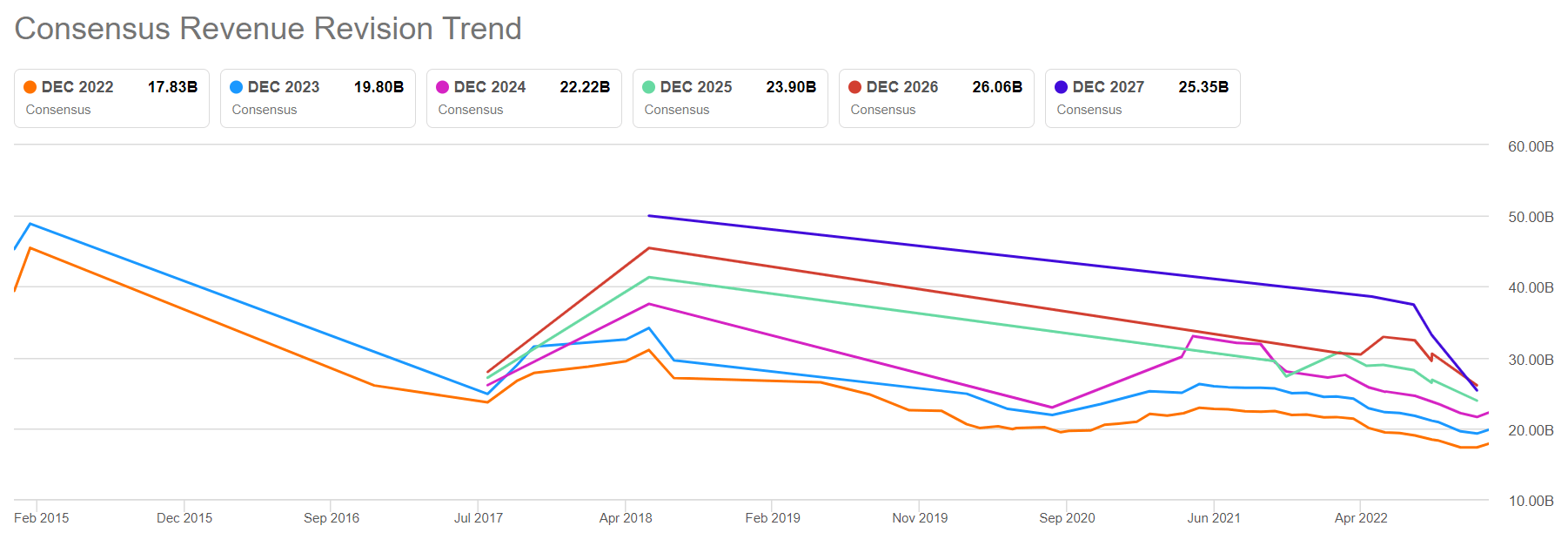

Although analysts are gradually becoming more and more bullish on China’s macro outlook, estimates for Baidu remain – in my opinion unreasonably – depressed, and have only recently started to tick upwards.

Seeking Alpha

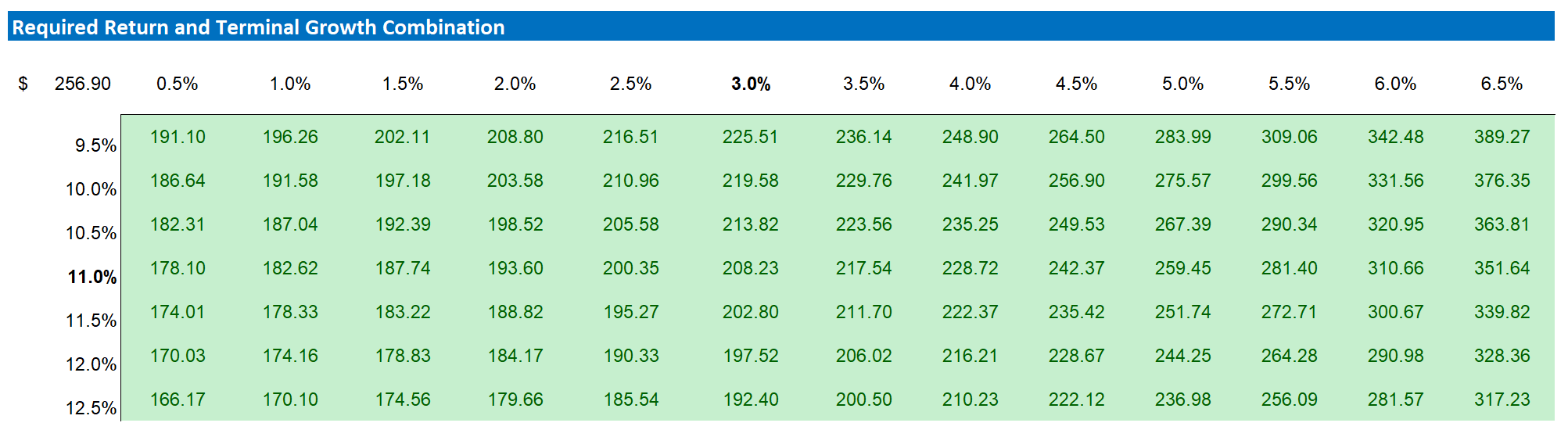

Target Price: Raise To $256.90

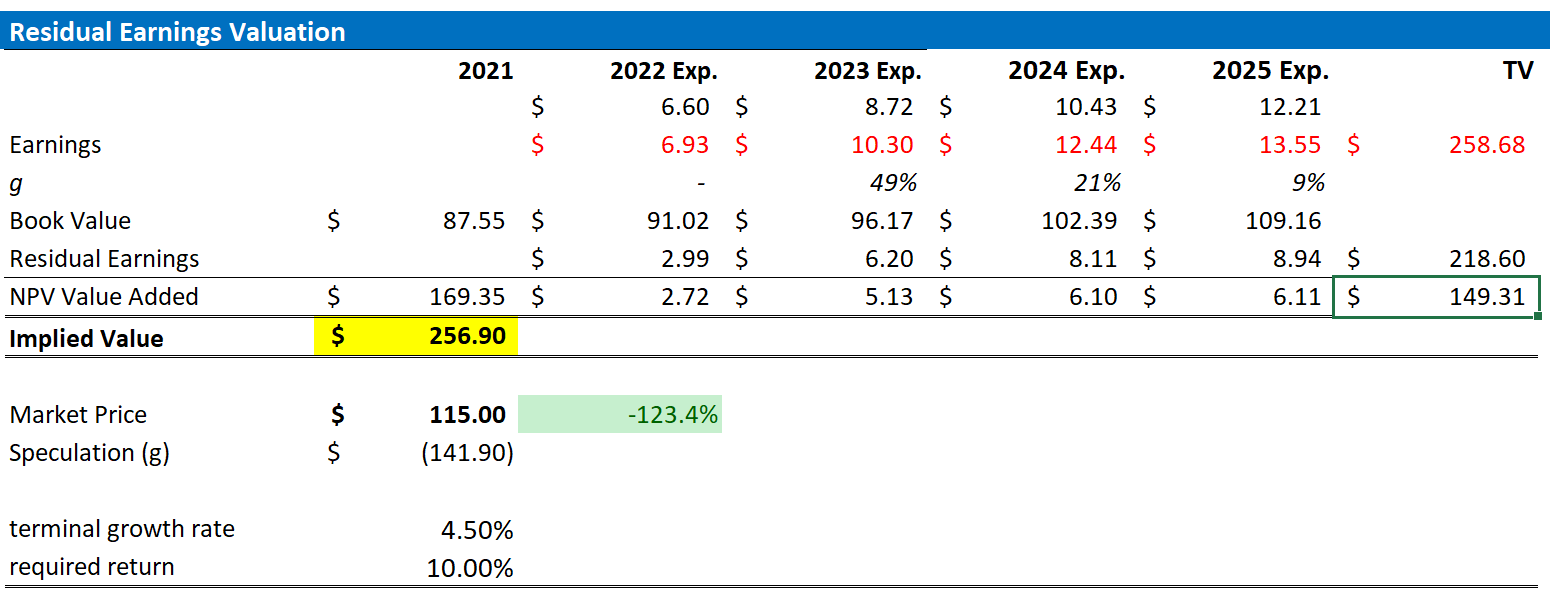

Expecting a sharp economic rebound in China, which strongly supports Baidu’s advertising business, I estimate that Baidu’s EPS in 2023 will likely expand to somewhere between $9.80 and $11.20. Moreover, I also raise my EPS expectations for 2024 and 2025 to $12.44 and $13.55, respectively.

I continue to anchor on a 4.5% terminal growth rate, as well as on a 10% cost of equity.

Given the EPS upgrades as highlighted below, I now calculate a fair implied share price of $256.90

Author’s EPS Estimates; Author’s Calculation

Below is also the updated sensitivity table.

Author’s EPS Estimates; Author’s Calculation

Risks and Headwinds

As I see it, there has been no major risk update since I initiated coverage on Baidu stock. Thus, I would like to highlight what I have written before. However, although the headwinds persist to some extent, please note that sentiment surrounding to all of these risk buckets appears to be improving.

First, the economy in China is currently pressured by multiple headwinds including inflation, real-estate crisis and COVID-19 lockdowns. If the Chinese economy would slow more than what is expected and priced in, investors should adjust expectations for Baidu’s short/mid-term business monetization accordingly.

Second, China’s internet/tech companies are strongly exposed to regulatory risk. While the worst seems to be behind us, the elevated risk exposure persists.

Third, much of Baidu’s share price volatility is currently driven by investor sentiment towards Chinese ADRs and risk assets. Thus, Baidu stock price might show strong price volatility even though the company’s business fundamentals remain unchanged.

Conclusion

Baidu stock is up approximately 31% since I have argued that the stock could rebound fast and aggressively. Although this performance is considerable, Baidu stock has still more room to go – especially with the COVID reopening in China supporting the company with a strong fundamental tailwind.

Anchored on a strong Q3, as well as confident management commentary for Q4 2022 and early 2023, I am confident to reiterate a ‘Buy’ recommendation for BIDU.

Be the first to comment