Sascha Schuermann

Investment Thesis

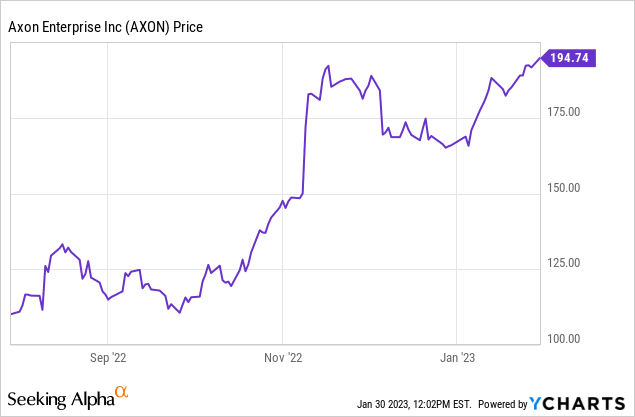

Axon Enterprise (NASDAQ:AXON) has been outstanding in the past 5 years, with shares up over 650% during the period. Unlike most high-growth companies that got hammered during the last 2 years, the company is currently trading near its 52-week high. Despite the massive growth in the past few years, it has only captured a small portion of its TAM (total addressable market) and has ample room for further expansion, especially outside of the US. Ongoing tailwinds such as digital transformation and transition to SaaS should continue to drive growth. However, after the 70% gain over the past six months, the current valuation is quite expensive and a lot of optimism is already baked in, which limits the potential upside. I like the company but I think it is a hold here and investors should be patient and wait for a pullback.

Introduction

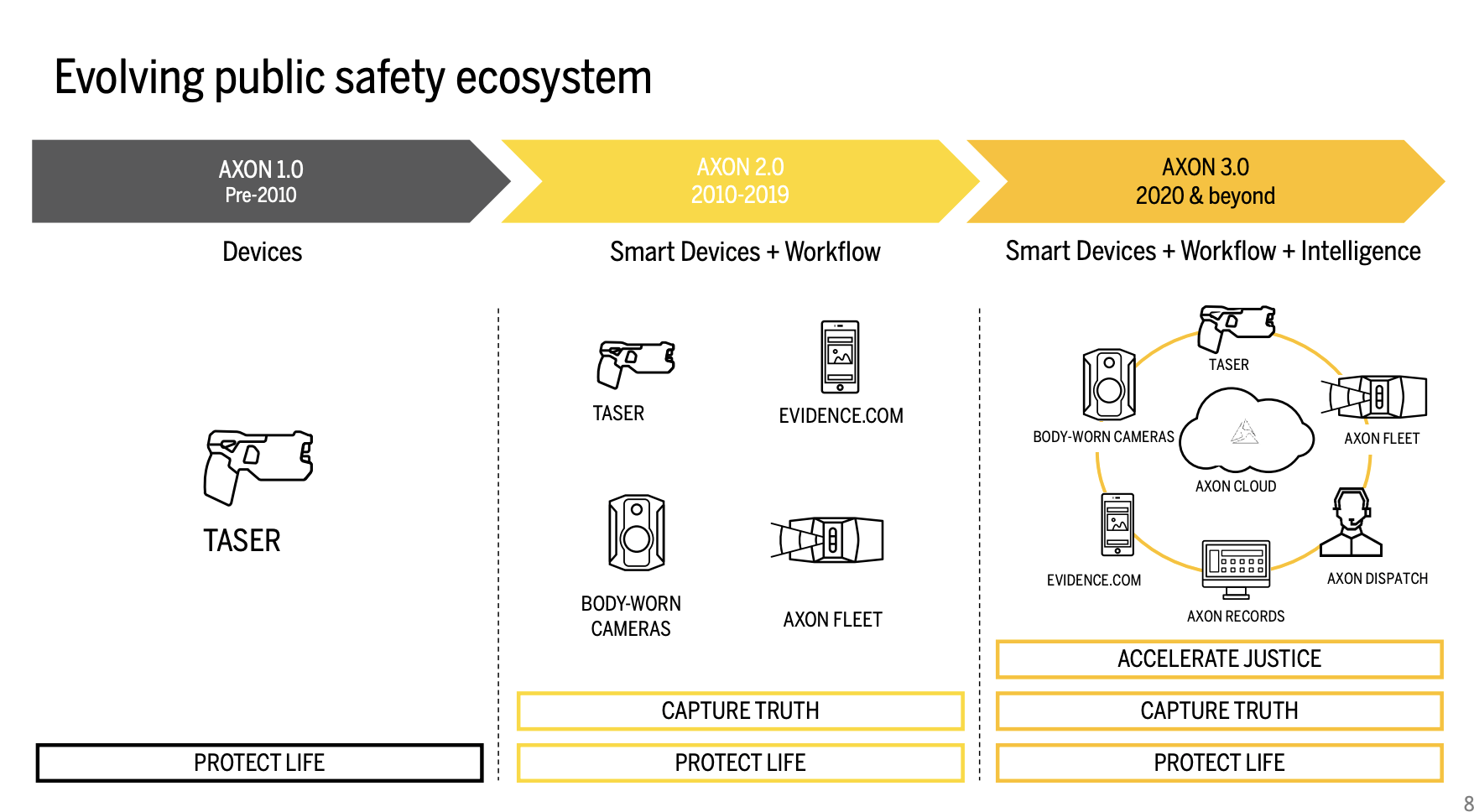

For those unfamiliar with the company, Axon is a US-based defense company. It offers products such as Tasers, body cameras, and vehicle cameras to law enforcement, federal agencies, etc. It also hooped on the trend and went digital with its own cloud offering Axon Cloud, which has been a strong growth driver lately.

Axon’s product has been seeing strong traction due to increasing controversies in regard to how law enforcement makes decisions. Tasers are an alternative to guns as they can freeze offenders without doing lethal damage, vastly reducing the costs of mistakes from officers. There are currently over 880,000+ Taser devices already in use globally. On the other hand, body cameras are able to record video and voice of incidents that can offer fair and unbiased evidence if needed. Axon Cloud is a software platform that ties things together for digital evidence management. The company is also actively adopting new technologies such as Drones and AR/VR for a more effective training process.

Axon

Market Opportunities

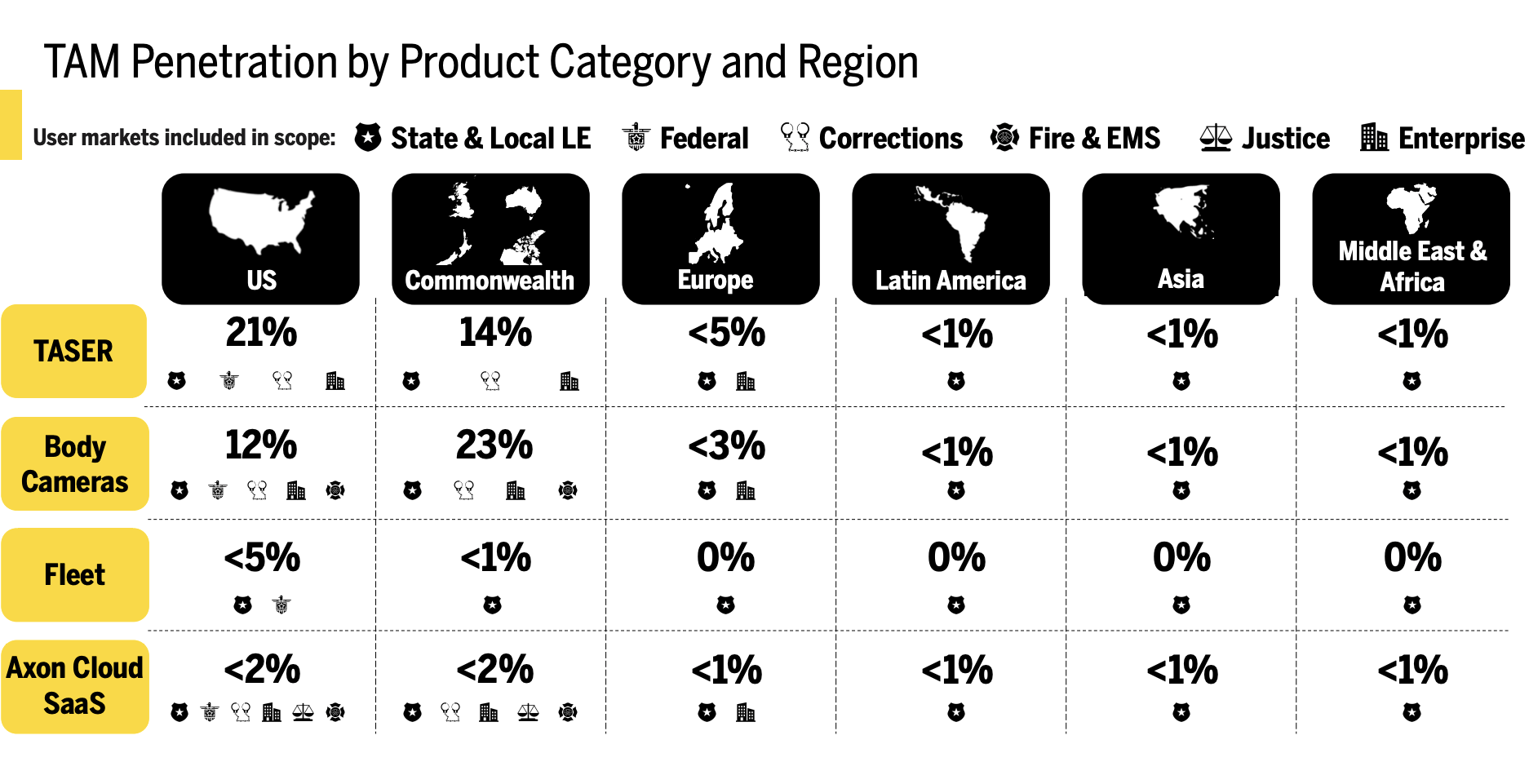

The market Axon operates in is huge. The current TAM is estimated to be around $52 billion, with consumer safety accounting for the most at $17.8 billion (or 34%) and digital evidence at second with $13.4 billion (or 26%). Despite the growth in the past few years, the current adoption rate of Axon’s products is still pretty low. In the US, Taser and body cameras have a penetration rate of 21% and 12% respectively, while Axon Cloud is only at less than 2%. This presents a huge opportunity for expansion, especially in the international market as it has an even lower penetration rate. For instance, the penetration rate of all Axon’s products is below 1% in Asia.

Josh Isner, COO, on growth runway

We want to make it super clear that our state and local law enforcement business is nowhere near saturated, and we see a long and wide runway for continued growth. We believe that in the next 5 years, you will see Axon emerge as the leading operating system for public safety, strengthened by our strategy of focusing on the customer experience and not cobbling together point solutions that don’t work well together, which is the current state of the industry outside of Axon.

Axon

Why Axon?

All of Axon’s products are now digitally connected thanks to digital transformation and IoT (internet of things). This provided a massive tailwind as it allows Axon Cloud to combine different products and improve law enforcement’s productivity and efficiency.

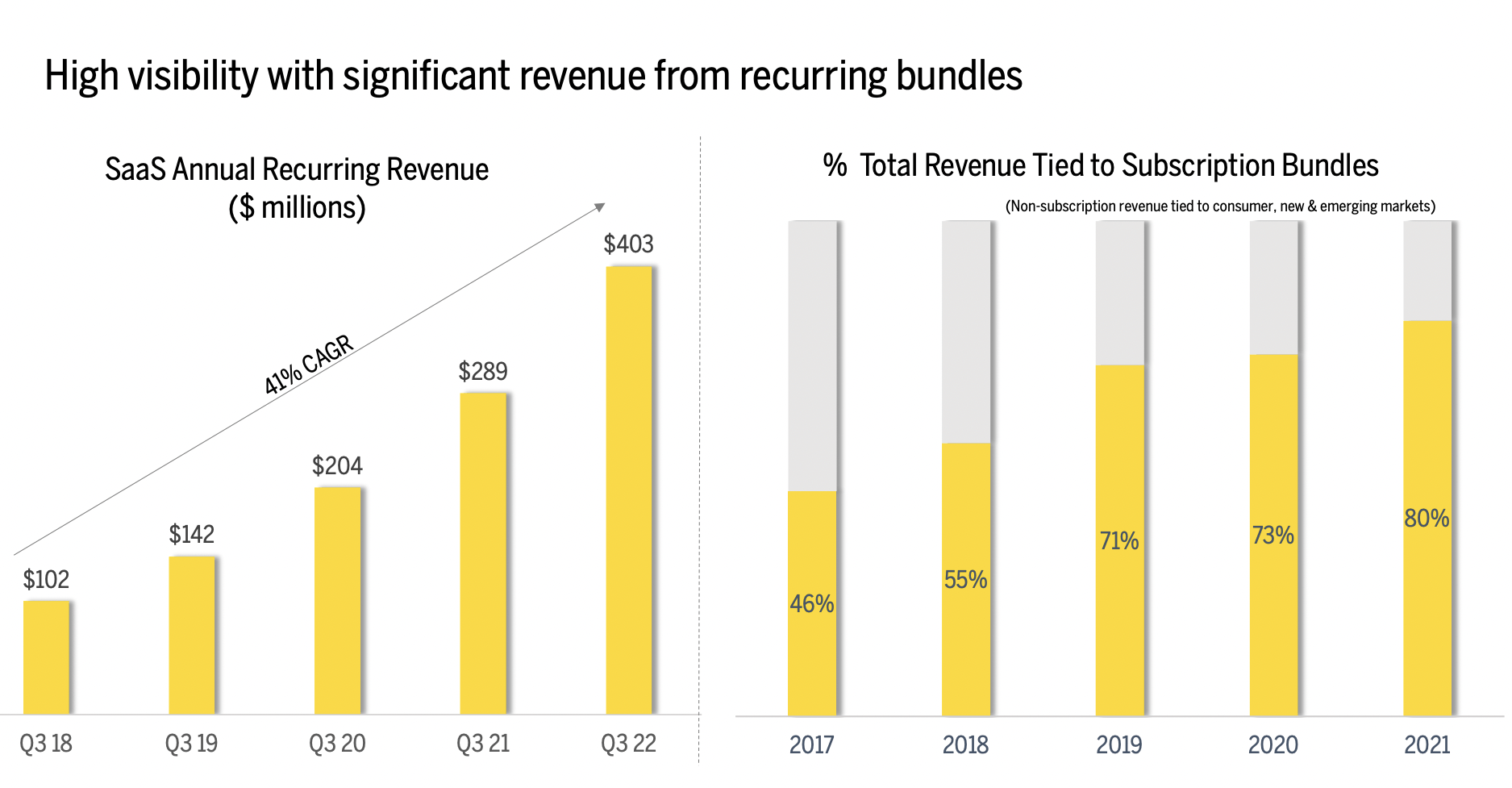

For example, operators can now see the real-time locations of officers and devices. It also enables better management and storage of digital evidence and data. Axon Cloud has been gaining popularity as it can consolidate all the devices and data together and provide a more cohesive experience. From 2017 to 2021, Axon Cloud revenue grew at a whopping CAGR (compounded annual growth rate) of 42%. I believe this will continue to be a strong growth driver.

Axon also has a strong moat thanks to its dominant market position. The Taser is patented and therefore cannot be replicated. More importantly, it is trusted by governments so even if other alternatives arise it will be nearly impossible for them to win over contracts. Axon also has a more complete suite of products that offers unmatched efficiency. This leading market position gives the company strong pricing power and operating leverage.

The company is also switching to a SaaS (subscription as a service) based model which has been seeing huge success. Annual SaaS recurring revenue has grown at a CAGR of 41% from 2018 to 2022, while the adjusted EBITDA margin also increased from 15% to 21%. Currently, 80% of revenue is tied to subscription bundles, up from just 46% in 2017. The ongoing transition should continue to improve profitability and revenue visibility.

Axon

Investors Takeaway

I think Axon is a unique company that will see huge success over the long term. Axon’s products are seeing strong demand with Axon Cloud leading the pack. The TAM for the company is huge and it has only captured a tiny portion of it, especially in international markets. It is also transitioning to a SaaS-based business model which should continue to improve margins and operational leverage. Besides, the company’s presence in the defense space provided it with much more stability compared to other growth companies that have been affected by the macro environment.

However, valuation is an issue here. After the massive run-up in the past six months, the current multiple seems very elevated. It is now trading at a fwd PE ratio of 71.8x which is expensive even if we factor in its impressive growth rate. On a PS (price to sales) basis, it is trading at 12.8x, meaningfully above its 5-year historical average of 9.6x. I don’t think there is much potential upside left in current levels as growth and catalysts are likely already priced in. Therefore, I rate the company as a Hold.

Be the first to comment