CHUNYIP WONG/iStock via Getty Images

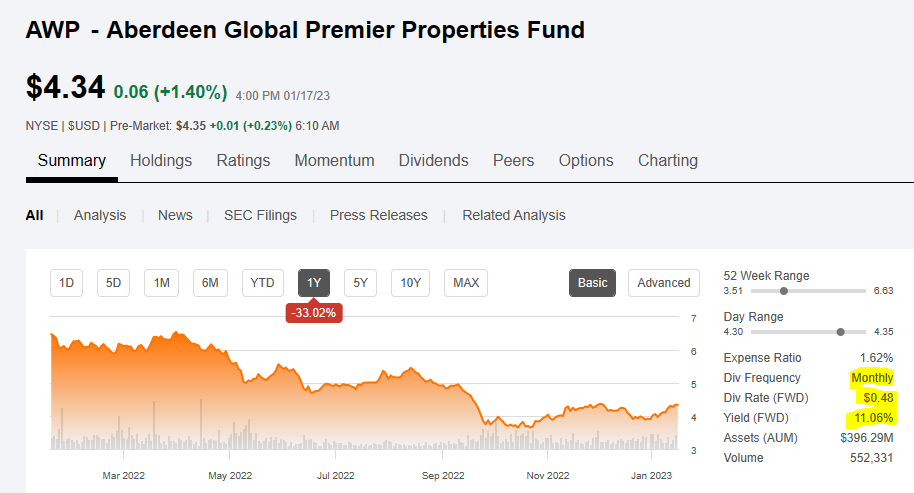

Aberdeen Global Premier Properties Fund (NYSE:AWP) is a real estate favorite on Seeking Alpha. The fund’s primary, and some might argue only, claim to fame comes from its whopping distribution. At 4 cents a month, the fund does get the juices flowing because it translates into an 11% yield.

Seeking Alpha

In the REIT space you generally will not find double digit yields outside of the mortgage REIT sector. So if you want a solid income play there is AWP staring you in the face. Unfortunately the reality of being involved with this fund from the long side, outside of a few tactical plays, has been gruesome. Today we will document this performance over some different time frames and tell you why it happened. We will also share why we think it gets worse from here and why your yield on cost will fall another 50% from here. Finally we will share what are tradeable points for this fund. Let’s get started.

The Fund

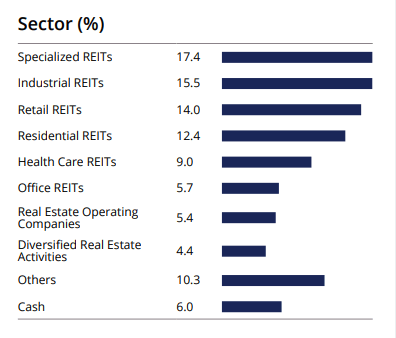

AWP’s primary objective is to seek high current income and capital appreciation. A vast majority of its holdings are REITs, with some holdings in real estate operating companies.

AWP Fact Card

AWP has been around since April 2007 and that gives us a long history to compare.

Performance

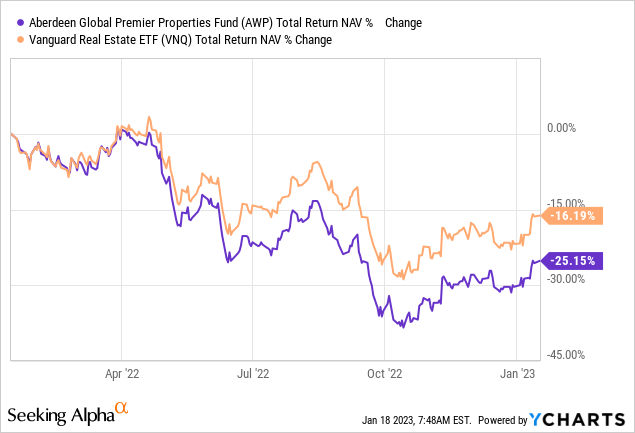

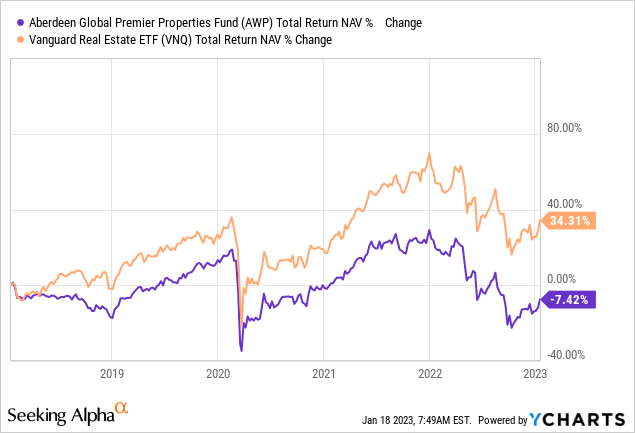

Who can honestly say that 2022 was easy? Whether you bought bonds or stocks, it was tough to make money. REITs had a particularly tough time. AWP’s total return on NAV (which includes distributions) was a negative 25.15% over the last 12 months. Vanguard Real Estate ETF (VNQ) which doled out far smaller dividends, managed to get to a negative 16.19% total return.

NASDAQ

Ok, so the chart below looks rough.

But perhaps it was an anomaly of a tough year. Let’s look at three years of performance. Over the last three years VNQ has outperformed by about 24%.

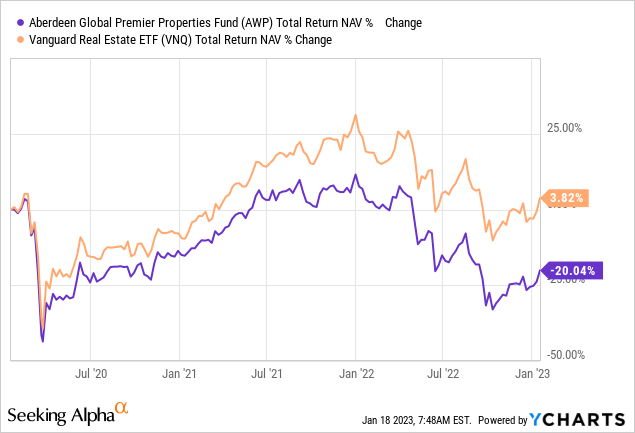

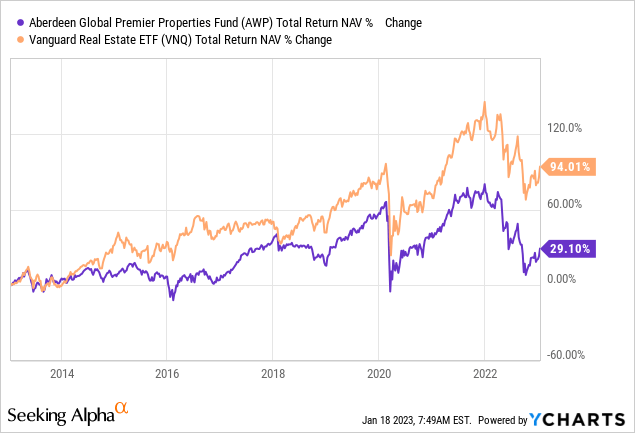

Of course, the common response is “I did not buy three years back”, so let’s try another timeframe. Over five years we are looking at 42% of outperformance by VNQ.

10 years is even rougher, with VNQ clobbering AWP by 65%.

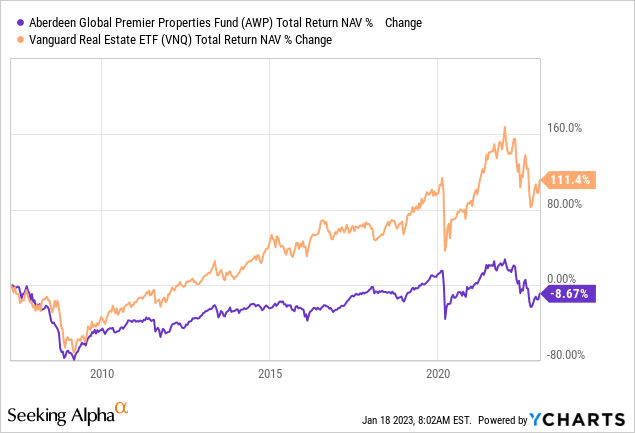

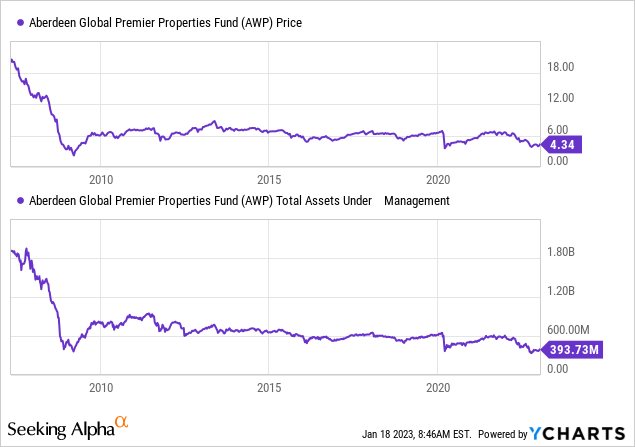

A final chart for those that want to see this from inception of AWP. Total returns including distributions reinvested is negative 8.67%. AWP has lagged VNQ by 120% since AWP’s inception.

There is some interesting math that pops up here when one considers that the inception of AWP was about 16 years back. Almost on every time frame, AWP is lagging by about 7-8% a year. What’s going on?

The Reasons

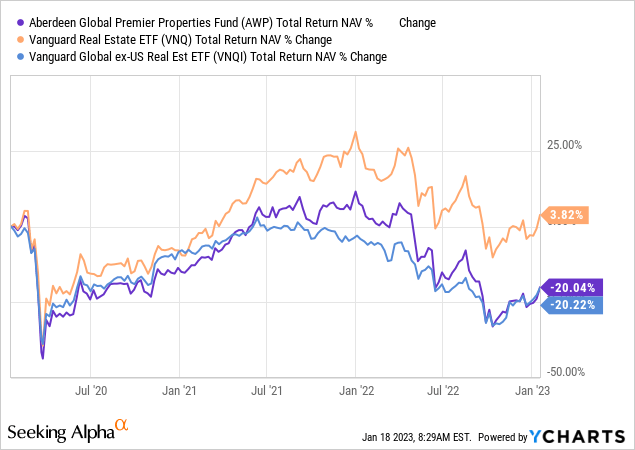

This is a two part answer. The first being that outside of the US has been a horrible place to be for REIT investing. AWP is a global fund and generally holds one-third of its assets outside of the US. A good way to look at some of the drag that AWP gets for global exposure is to compare performance of Vanguard Global ex-U.S. Real Estate (VNQI) vs AWP and VNQ.

In the chart above you can see AWP moving more or less with VNQI over the last three years. REITs outside of US have fared far worse and AWP suffers because of that. Still, in an ideal world, AWP should be about midway between VNQ and VNQI. Actually it should be a lot closer to VNQ as it generally has two-thirds invested in US assets. So even adjusted for the global component, things are not so rosy.

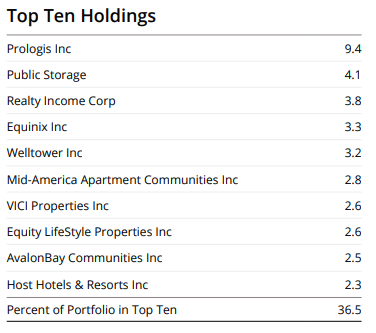

That brings us to the second reason and in our opinion this is all about the yield chasing. AWP pays a very hefty distribution that has generally never been covered. This is pretty easy to grasp if you can get fourth grade math. The holdings below are AWP’s top 10.

AWP Fact Card

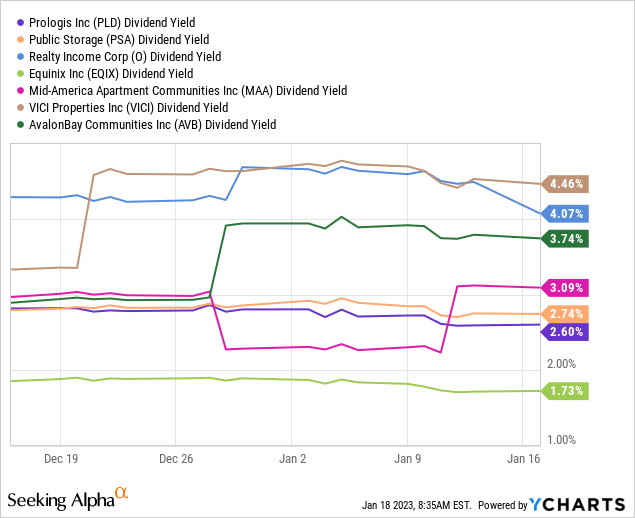

Here are some of their dividends yields. The median is 3.09%.

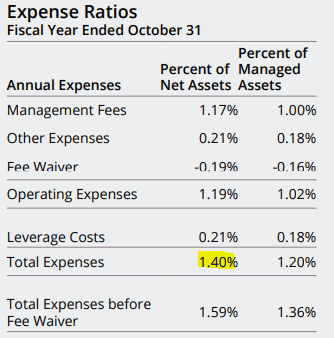

So getting from 3.09% to 11% is a big hurdle. Coincidentally that works out to that 8% annual lag that we talked about. Sure, the fund uses some leverage. But 10-20% leverage on a 3.09% yield does not even begin to move the needle. When you consider that AWP’s interest costs now dwarf that 3.09%, leverage actually works in the reverse. AWP’s real underlying yield after expenses is very close to 1.75%-2.00% in our estimation. You can get there by withdrawing the expense ratio from the underlying holdings’ yield.

AWP Fact Card

So to get to that 11%, AWP is constantly selling assets. That is a problem as you are forced to sell at almost every single point. That works out like this.

Verdict

Our outlook for 2023 remains decidedly bearish. We believe the market is underestimating how long the Federal Reserve will wait before it cuts and we also think the market is overestimating how aggressive these cuts will be. REIT repricing is not done and the high multiple growth names are most vulnerable here. That is our outlook and if you don’t buy it, you are free to disagree.

We see funds like AWP particularly vulnerable as they get the trifecta of problems. First from the sector moving lower, second from forced selling to pay distributions and finally from a likely blowup of the NAV discount at some point. Visualize a year of negative 20-25% returns for VNQ where AWP’s discount moves to a negative 20%.

Add in that 8% annual lag. It could get tough.

So where would we buy this? Generally for AWP we would need at least two of three things to make a tactical buy.

1) A very favorable REIT outlook.

2) A very wide discount to NAV expected to narrow.

3) A very bearish outlook on the US Dollar.

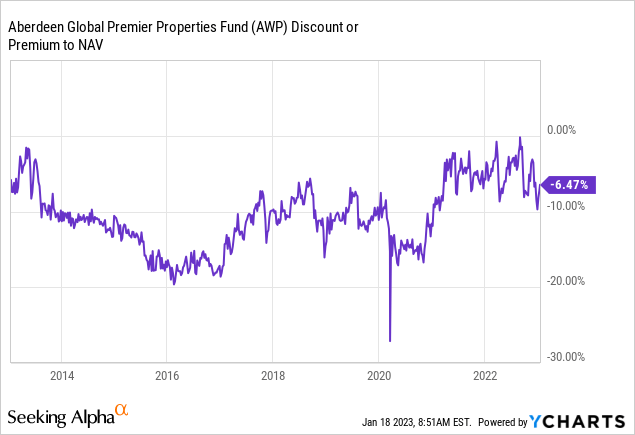

We did have all three (maybe 2.5 on 3.0, to be exact) in November 2020, where we did put a buy rating on it. REITs looked poised to do better back then in our view. The discount at that date was a mouthwatering 16.6% and we were slightly bearish on the US dollar.

From Article “AWP Poised To Outperform”

At present, we have none of the three and we are maintaining our Sell rating on the CEF.

Be the first to comment