zorazhuang

Thesis

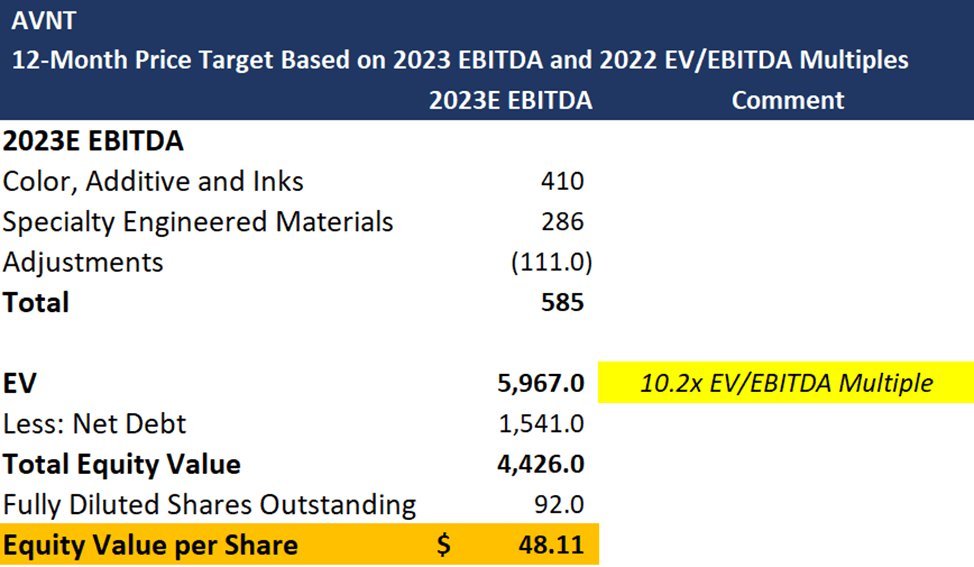

Avient Corporation’s (NYSE:AVNT) shares are down 40.2% YTD versus 11.7% for the S&P Chemicals Index primarily due to concerns over the company’s European exposure (35% of sales), leverage and how it will perform in a recession as Q3 result missed estimates and 2022 guidance reduction highlighted that the company is not immune to slowing demand. While understandable, I believe these concerns are overdone and fully reflected in the share price – which also discounts a moderate recession, in my view. Looking ahead, with cost pressures coming down and healthy growth prospects, I believe Avient offers one of the more attractive risk / rewards in chemicals today. I keep a 2023 December target price of $48.11 on the stock derived from an assumed 2023 EV/EBITDA of 10.2x (current EV/EBITDA multiple).

AVNT stock price movement YTD (Ycharts)

Company Overview

Headquartered in Avon Lake, OH, Avient is a leading formulator of specialized chemical additives, advanced composites, and specialty-engineered polymer materials. Including the recently completed Dyneema acquisition and the soon-tobe-completed Distribution divestiture, Avient operates 108 manufacturing facilities located across 6 continents. By region, Avient generates 40% of pro forma sales in the US & Canada, 35% in EMEA, 20% in Asia and 5% in Latin America. Avient also has ~2,500 patents, including ~1,300 from Dyneema. Avient is organized into 2 segments: Color, Additives and Inks (65% of total sales), Specialty Engineered Materials (35% of total sales).

Why am I bullish on Avient?

Favorable price / cost dynamics in 2023

Raw material costs comprise ~80% of Avient’s cost of goods sold. Since the beginning of 2021, Avient has experienced significant raw material cost inflation, with hydrocarbon based raw materials (40% of total raw material costs) up 50% in 2021 and non-hydrocarbon based raw materials up 12%. Exacerbating these raw material cost headwinds have been persistent supply chain issues which have resulted in increased raw material spot purchases, freight constraints, and productivity losses.

Looking ahead, due to its highly specified product portfolio, I expect Avient to retain a significant portion of its selling price increases if / when raw material prices roll over. With the prices of hydrocarbon based raw materials (polyethylene, nylon, polypropylene, styrenic block monomer) already coming down and prices for the majority of its non-hydrocarbon based raw materials (performance additives, pigments, TiO2, dyestuffs) plateauing if not already declining, I believe this favorable price / cost dynamic will result in significant margin expansion for Avient in 2023 and 2024.

Significant margin expansion opportunity

Similar to its peers, Avient has experienced significant raw material cost inflation since the beginning of 2021. As these raw material costs roll over, I expect Avient to retain a significant portion of its selling price increases. As this occurs, Avient should realize a favorable price/ cost dynamic and significant margin expansion. Coupled with remaining Clariant Masterbatch cost synergies, mix upgrades, and the integration of the higher margin Dyneema business, I forecast Avient’s EBITDA margins will expand from 16.5% in 2022E to 18% in 2023E, 19% in 2024E, and 20% in 2025E.

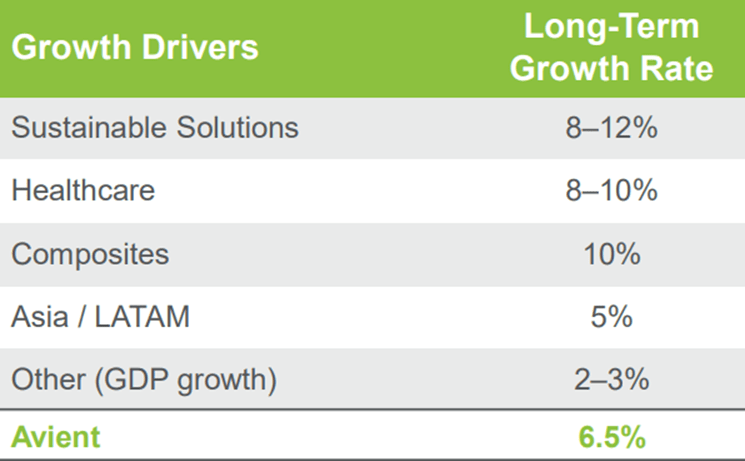

Attractive long-term growth

We believe Avient’s transformed portfolio is well positioned to achieve its targeted 7% long-term sales growth driven by 8-12% growth from Sustainable Solutions, 8-10% growth from Healthcare, 10% growth from Composites, and a 5% growth from Asia/Latin America. This 7% sales growth is expected to drive 10%-plus EBITDA growth and 15%-plus EPS growth.

The largest growth platform for Avient is Sustainable Solutions. From a base of $340 million of sales in 2016, Sustainable Solutions has grown at a 12% compound rate over the last 5 years to $915 million in 2021. Driving this growth have been megatrends around sustainability, recycling, and circularity, increasing sustainability commitments from brand owners in packaging and consumer goods, evolving customer requirements for higher performance and durability, and Avient’s commercial investments and innovations.

Another key growth platform for Avient is Healthcare (8% of sales). After a strong 2021 and 1H 2022, we expect Avient to continue to grow Healthcare in-line with its long-term target of 8- 10%. This highly resilient growth is driven by Avient’s expansive material portfolio, innovative solutions, long-standing relationships with key manufacturers, and differentiated services that enables close partnership with customers through the entire product development cycle.

Avient growth targets (Company Presentation)

Resilient end markets

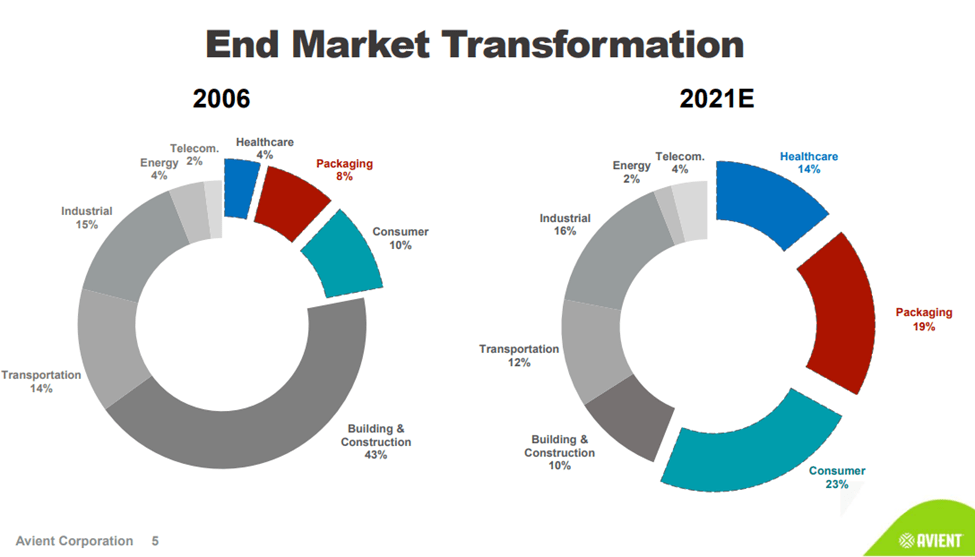

Over the last 15 years, Avient has transformed itself from a highly cyclical and commodity centric chemical company with just 7% of EBITDA generated from specialty businesses (in 2005) to specialty chemical formulator with a high degree of earnings resiliency and roughly 60% of EBITDA generated from less cyclical end markets (in 2022). Highlighting this transformation and enhanced resiliency is Avient’s building & construction exposure, arguably its most cyclical business, which today comprises just 10% of sales.

Avient’s transformed portfolio is highly defensive (Company Presentation)

Dyneema enhances composites portfolio

The recent $1.5B Dyneema acquisition (closed on September 1) more than doubled the size of Avient’s Composites platform and expanded its portfolio into highly specialty and resilient end-markets, including personal protection (52% of Dyneema sales) and marine & sustainable infrastructure (31% of Dyneema sales). In addition, the new Composites platform will have stronger innovation driven growth opportunities due to Dyneema’s technology expertise, deep history of customer centric application development, and strong revenue synergy opportunities between Dyneema and Avient’s existing portfolio.

Financials

Revenue

I forecast Avient’s sales will fall 1% in 2022 to $3.7 billion on a 1% decline in CAI and a 3% decline in SEM. In 2023, I forecast sales will decrease 8% to $3.4 billion on an 8% decline in CAI and a 7% decline in SEM. Underpinning my forecast is the expectation of a moderate recession in 2023 (lower volumes, weaker pricing, FX headwinds). Thereafter, the forecasted sales will rise 8% in 2024 to $3.7 billion on 8% growth in both CAI and SEM, and 7% in 2025 to $3.9 billion driven by a 6% growth in CAI and a 10% growth in SEM (including 3% growth from acquisitions).

Valuation

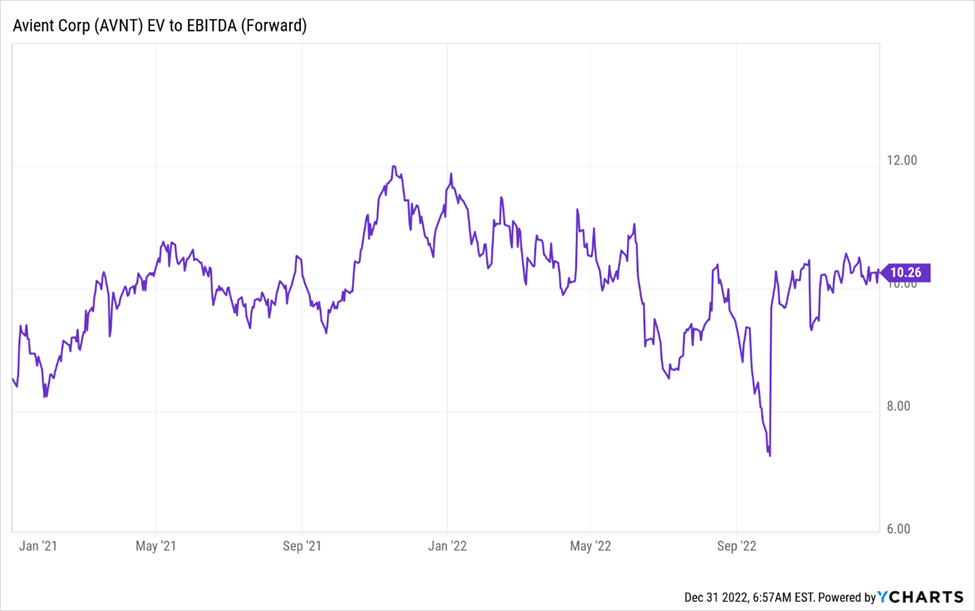

My $48.11 price target implies Avient trading at 10.2x 2024e EBITDA in 12 months, in-line with current forward year (2023) multiple. Avient has expanded its multiple recently, and I believe this expansion is justified by what I expect to be the delivery of consistent earnings growth that demonstrate a high degree of resiliency and sustained pricing power (selling prices holding as raw material costs decline).

AVNT’S forward EV/EBITDA (Ycharts) AVNT’s price target calculation (my estimates)

Risks

High leverage

Following 2 major acquisitions in the last 2 years (the $1.4B acquisition of Clariant’s Masterbatch business in ’20 and the $1.5B acquisition of Dyneema in September) and even after the ~$1B sale of its distribution business, Avient is one of the more levered companies in the chemical sector with a forecasted year-end ’22 net debt/EBITDA ratio of 2.9x. While I do not consider 3x to be an overly high amount leverage, given where we are in the economic cycle (potentially heading into a recession in the US and Europe), it is higher than most chemical investors prefer. Instead, a level of closer to 2x is the preferred amount of leverage, in my view, at this point in the cycle.

High European exposure

With the Dyneema acquisition and the Distribution divestiture, Avient’s EMEA exposure has increased from 25% of sales to 35% of sales, with the vast majority of this exposure in Europe. This places Avient in the upper quartile of European sales exposures amongst US chemical and with Europe forecasted to be in a recession in 1H’23, coupled with an elevated exposure in this region to cyclical industrial and transportation markets, I believe Avient will face (continuing) earnings headwinds from this region through at least 2023.

Final Thoughts

With the $1.5 billion acquisition of Dyneema and the $1B sale of its distribution business, Avient has completed its 15-year journey from a commodity centric, and volume focused chemical company with a high degree of earnings volatility to a specialty chemical formulator with strong earnings resiliency (60% of sales are to less cyclical end markets), focused on sustainable solutions and with ~2x GDP growth prospects. With its transformation complete, all that is left now is for Avient to deliver on its target of consistent, 10%-plus EBITDA growth (and 15%-plus EPS growth) driven by innovation, sustainable solutions, and high growth end markets (composites, health care, emerging markets). Therefore, I keep a buy rating on the stock with a December 2023 target price of $48.11.

Be the first to comment