nambitomo/iStock via Getty Images

Avidity Biosciences (NASDAQ:RNA) is a small (volatile and currently below $1 billion market cap) biopharmaceutical company focusing on RNA therapeutics, On Dec. 14, the Avidity announced positive preliminary data from MARINA, the first-in-human trial of AOC 1001, its lead drug candidate. In September, the Food and Drug Administration (FDA) placed a partial clinical hold on new patient enrollment. Once resolved, investors can look forward to more positive topline data from this drug and possibly others in 2023 with confidence.

Avidity’s platform brand of antibody-drug conjugates is called Antibody Oligonucleotide Conjugates (AOCs). Oligonucleotides are small nucleic acids that interact with their target molecules via complementary Watson-Crick base pairing, so candidates may be specifically designed based on knowledge of the primary sequence of a target gene alone and rapidly screened. There are 14 FDA-approved oligonucleotides; Sarepta Therapeutics (SRPT) markets 3 of them: Exondys, Vyondys, and Amondys, all of which are also phosphorodiamidate morpholino oligomers (PMOs). Avidity found that monoclonal antibodies (mAbs) were the best way to deliver the oligonucleotides.

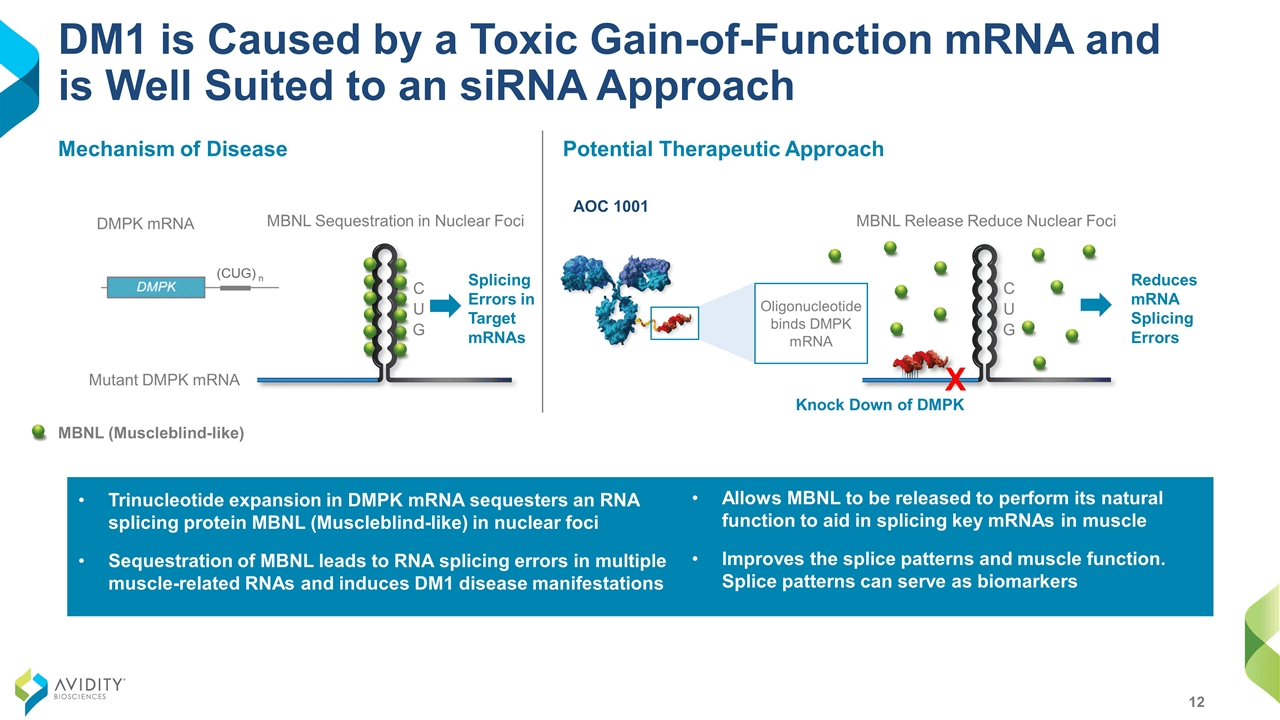

AOC 1001 consists of a mAb that binds to the transferrin receptor 1 (TfR1) conjugated with a small interfering RNA (siRNA, the oligonucleotide). Its target is messenger RNA (“mRNA”) that codes for the protein called myotonic dystrophy protein kinase (DMPK). Mutant DMPK mRNA is thought of as the root cause of myotonic dystrophy type 1 (DM1), a progressive and often fatal neuromuscular disease with no approved therapies. By reducing DMPK mRNA and subsequently, DMPK production, AOC 1001 could impact the underlying mechanism of the disease and provide a biomarker of its progress (Figure 1).

A recent genetic analysis in the ethnically and racially diverse population of New York state revealed a high 4.8 per 10,000 prevalence of DM1, more than double that of previous estimates, because most of these individuals are asymptomatic and go undetected. However, even the undiagnosed carry an increased risk for sudden cardiac death and other DM1 complications. The FDA and European Medicines Agency have granted Orphan Designation for AOC 1001. The FDA has also granted Fast Track Designation to AOC 1001 for the treatment of DM1.

Figure 1. Figures 1 to 3 are from Avidity’s Virtual Investor & Analyst Event Series – VOL 6.:

AOC 1001 MARINA Phase 1/2 Trial Preliminary Data Assessment

Avidity

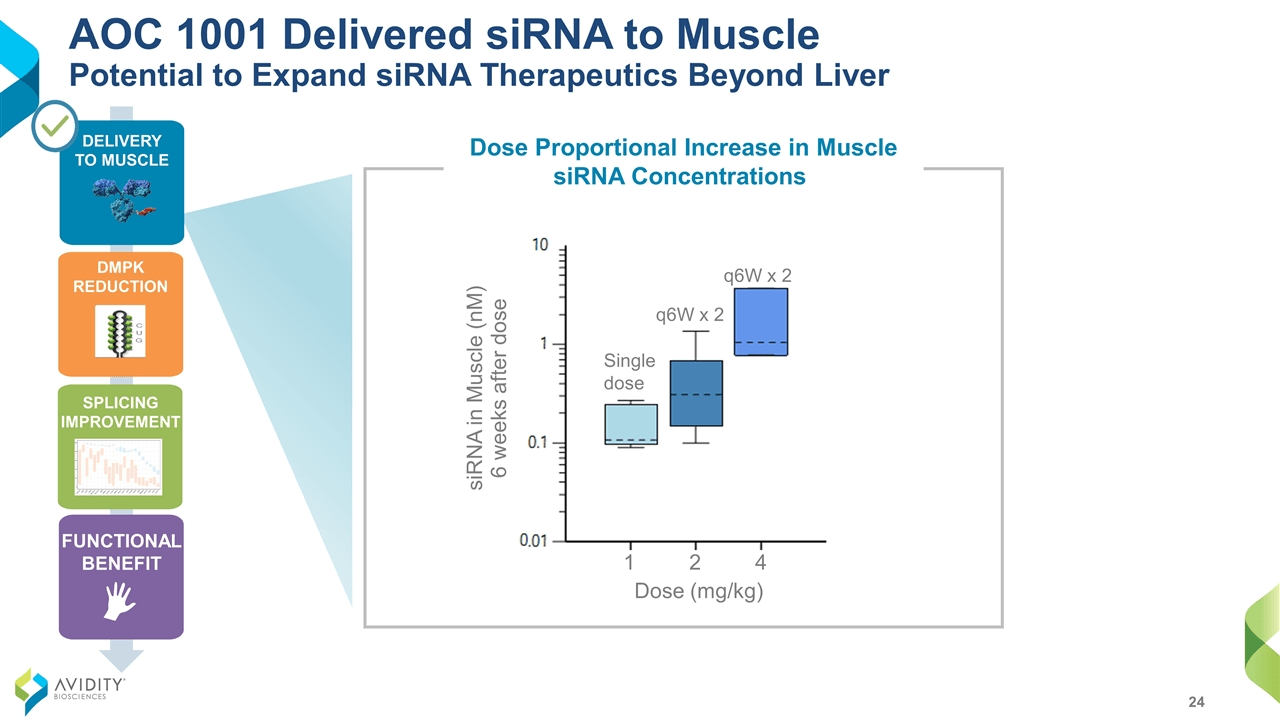

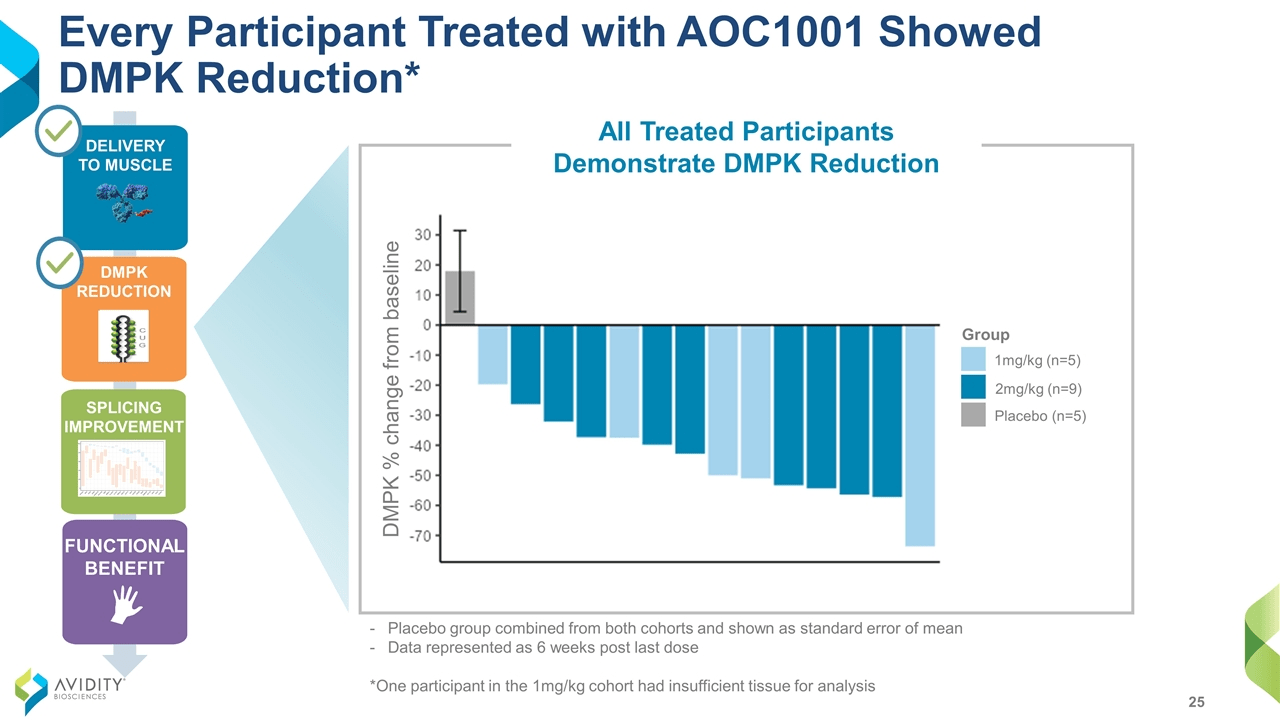

Most oligonucleotide therapeutics have previously focused on either direct injection to local tissues or delivery to the liver. However, DMPK is most heavily expressed in the heart and not the liver. In MARINA, a Phase 1/2 double-blind, randomized, placebo-controlled trial (“RCT”) in adults with DM1, AOC 1001 went where it was supposed to (Figure 2) and did what it was supposed to, reducing DMPK by an average of 45% (Figure 3). Although MARINA’s outcome measures are on safety and pharmacokinetics, some video of clinical benefits to finger mobility and grip strength were highlighted in 3 of the 14 patients on AOC 1001 after 1 to 3 doses. The FDA hold was due to a serious adverse event reported in a single participant in the 4 mg/kg highest dose cohort. It doesn’t apply to current participants, and 100% of patients who had completed the MARINA trial have opted to roll over into the open label extension, MARINA-OLE.

Figure 2.

Avidity

Figure 3.

Avidity

Avidity has 2 other rare disease programs in the clinic. AOC 1020, another siRNA, will be advancing in the Phase 1/2 FORTITUDE trial for the treatment of facioscapulohumeral muscular dystrophy, for which there is no disease-specific treatment. Preliminary assessment in approximately half of participants is expected in the first half of 2024. Second, AOC 1044 will be evaluated in the Phase 1/2 EXPLORE44 trial for the treatment of Duchenne muscular dystrophy (DMD) mutations amenable to Exon 44 skipping (DMD44). AOC 1044 is Avidity’s first PMO candidate. DMD44 appears in 9.7% of individuals in the Duchenne Registry, a large database of phenotypic and genetic data for DMD. However, Avidity states that DMD44 occurs in 7% of DMD patients, approximately 900 of whom live in the U.S. Results from Part A in healthy volunteers are anticipated in the second half of 2023. If there is no safety concern, it may be smooth sailing through the approval process if the history is any indication.

Exondys received FDA fast track designation, priority review, and orphan drug designation, and in 2016, it controversially became the first drug for DMD after the FDA went against the wishes of its own Peripheral and Central Nervous System Drugs Advisory Committee. The Committee voted 7-3 against approval, with three abstaining, and 7-6 against the accelerated approval, which was based on a surrogate endpoint, defined as the increase in production of the dystrophin protein in skeletal muscle. While everyone agreed Exondys was safe, its pivotal trial sequence consisted of 25 total patients, didn’t measure pre-treatment dystrophin levels in 2 of the 3 studies, employed historical controls as part of placebo, and showed no benefit in the clinical outcome, the 6-minute walk test. The third study that had pre-treatment levels only demonstrated a mean change from baseline (“CFB”) 0.28% after 48 weeks (from 0.16% to 0.44%). The median improvement was even worse, 0.1%.

Vyondys’ path to become the second exon-skipping, disease-modifying drug to treat DMD was similarly dramatic. Its uncontrolled NCT02310906 study in 13 patients didn’t bother with a clinical benefit outcome, just the dystrophin CFB endpoint after 48 weeks. It took a little over 4-1/2 years from the dosing of the study’s first patient on January 14, 2015 to the FDA action date of August 19, 2019. However, the Agency handed down a Complete Response Letter for safety reasons: the risk of infection linked to intravenous infusion ports and kidney toxicity only seen in animal studies. After only 4 months, the they reversed course and suddenly granted accelerated approval. Unlike the earlier pair, Amondys was compared to an actual placebo group in one of its pivotal trial cohorts, but the FDA okayed it based on one interim analysis of dystrophin CFB at Week 48 in 43 patients. The wait was similar from the dosing of first patient in the Essence study for Amondys on September 28, 2016 until approval on February 25, 2021.

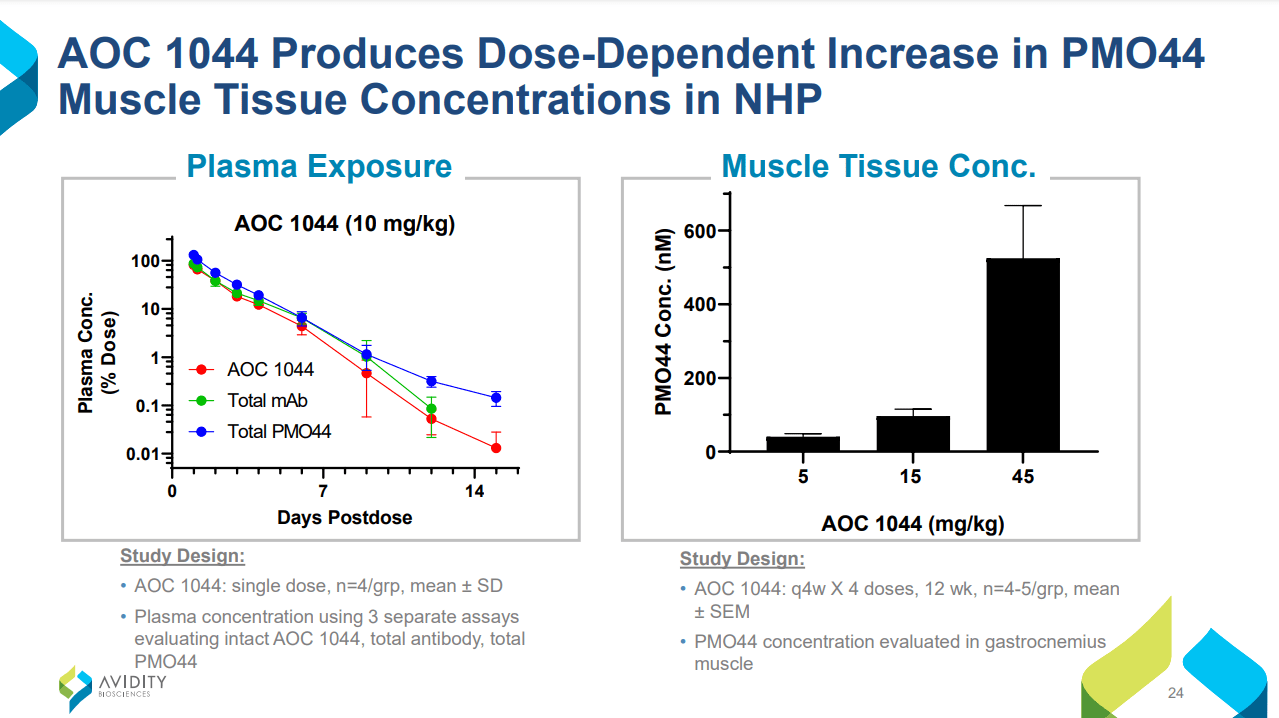

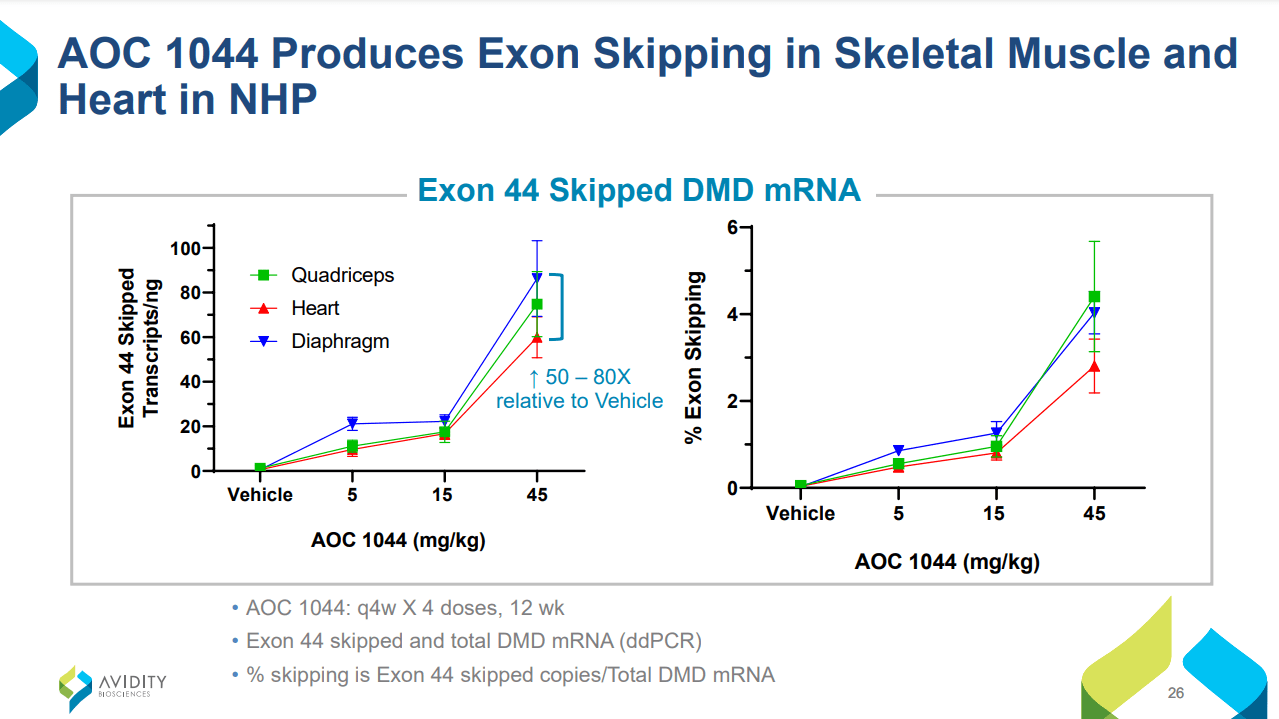

Going by Sarepta’s DMD experience, AOC 1044 would be largely de-risked if Phase 1 Part A results in no safety signals. Furthermore, success is likely for the future Part B in participants amenable to Exon 44 skipping because of several supporting factors: MARINA demonstrated the first-ever successful targeted delivery of RNA into muscle, AOC 1044 shares the same mAb+linker vehicle as AOC 1020, and pre-clinical studies in non-human primates show that 1044 was delivered into the muscle (Figure 4) and induced exon 44 skipping (Figure 5). EXPLORE44 by itself should be all that’s necessary for approval. Because PMOs are now mainstream DMD treatments and COVID-19 isn’t as bad as in 2020, one can only hope the process will be shorter due to quicker enrollment; if not, expect approval in late 2026/early 2027.

Figure 4. Figures 4 and 5 are from Avidity Biosciences Virtual Investor & Analyst Event Series – VOL. 5:

Advancing AOC 1044 into the clinic

Avidity

Figure 5.

Avidity

Further down Avidity’s pipeline are planned programs targeting exon 51 and exon 45 dystrophin. These future candidates will be developed to compete against Exondys and Amondys, respectively. A wise strategy, since the largest DMD group consists of individuals amenable to exon 51 therapy (13.8%). Together with AOC 1044, they would potentially cover approximately 30% of DMD patients.

Currently, Avidity’s cash and securities stand at $631.9 million after a $207 million offering on the 15th. Their revenues the past 3 years range from $2 to $2.5 million quarterly, mostly from the 2019 research collaboration and license agreement with Eli Lilly and Company (LLY). Research and Development make up the bulk of expenses in 2022, averaging $35 million per quarter. Operational losses to the end of Q3 were $125.7 million. Therefore, Avidity shouldn’t need more financing until 2024.

Risks

Avidity isn’t the ideal biotech for a bear market because it has no commercial products and no consistent source of revenue. The hold on 1001 is confined to the high doses, it might put a ceiling on treatment effects. Alternatively, it not be resolved in a timely manner and exhaust the cash runway. The unlikely but worst case is if the safety issue lies with the mAb or linker, which would affect the entire pipeline. Dodging safety bullets isn’t a sure thing even in DMD. This week, Entrada Therapeutics (TRDA) exon-44 skipping candidate fell further behind after it was hit by an FDA clinical hold as well. Even aside from Sarepta, other competitors exist that may come to market ahead of Avidity’s candidates, although several products could coexist if their mechanisms of action are different.

Takeaways

Avidity presents investors with an opportunity in the coming year because it is small and not well-known, but have a delivery system no one else has. Buying the dip as the broad stock market declines due to inflation and recession fears, as well as out-of-the-money call options with strikes in late 2023 are both viable. Of their clinical agents, AOC 1044 has the most concrete marketing potential. Amondys product sales for the first 4 full quarters since its U.S. launch totaled $112 million in a similarly-sized DMD population with prospective AOC 1044 patients. Some analysts see Exondys peak sales topping $1 billion, while Amondys could “bring in $300 million by 2025“.

To conclude, lifting of the 1001 clinical hold is the catalyst that will likely occur first. A Phase 1 catalyst is rare, especially ones in healthy subjects, but it applies with 1044 because scrutiny will be safety and penetration into the muscle. Beyond 2023, MARINA-OLE could show clinical benefits with repeat dosing of 1001. The same with 1044 in Part B of its trial. However, Avidity can survive even if the trends aren’t found to be statistically significant, because that still puts them on par and on track with those drugs that were granted accelerated approval on biomarkers alone. And should 1044 pull through with even a hint of clinical efficacy and Sarepta’s products don’t in their confirmatory trials (Essence reads out in 2025 while Exondys’ is in 2026), then it will surely surpass Amondys’ launch numbers.

Be the first to comment