24K-Production/iStock via Getty Images

Shares of RNA therapeutics pioneer Avidity Biosciences (NASDAQ:RNA) are roughly flat since 2020 IPO took place at $18 per share (quite an achievement these days during biotech bear market and overall market downturn). Over the past year, share price performance at its worst neared -60% (since has pared that to-20%).

A week ago the company announced a positive early readout for its antibody oligonucleotide conjugate (AOC) AOC 1001 in patients with DM1 (myotonic dystrophy type 1), representing a potential breakthrough for the field as the first successful targeted delivery of siRNA to muscle in humans. From there, the company was able to raise $207M in an upsized secondary offering, providing them with operational runway of well over 2 years to move forward in early to mid-stage studies.

On the other hand, as I understand it, there are still some potential safety issues to better understand here given prior FDA partial clinical hold for unspecified “serious adverse event”. So, with a skeptical eye, I look forward to digging deeper to determine if there’s enough derisking here to merit consideration in our clinical stage portfolio.

Chart

FinViz

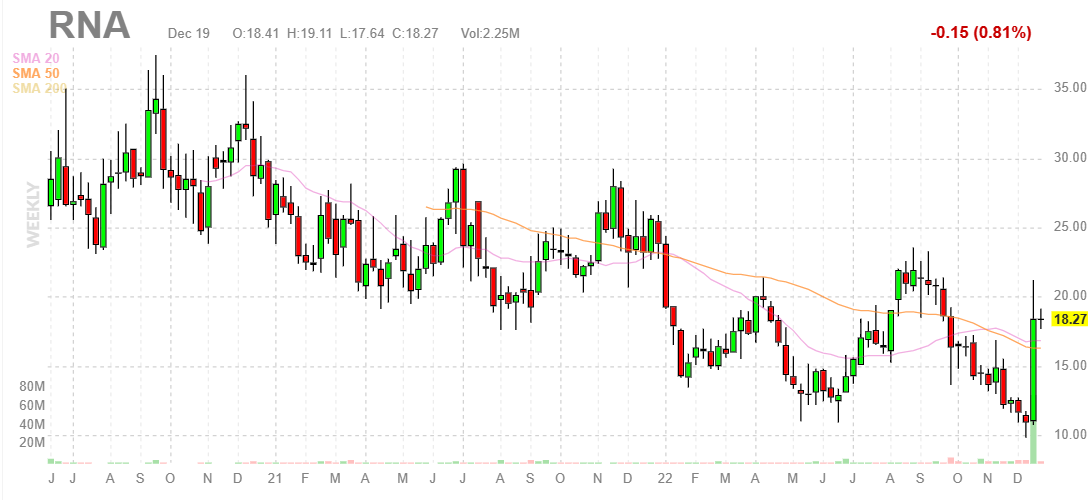

Figure 1: RNA weekly chart (Source: Finviz)

When looking at charts, clarity often comes from taking a look at distinct time frames in order to determine important technical levels and get a feel for what’s going on. In the weekly chart above, we can see share price gradually decline (albeit in an erratic manner) from above $30 to a low $10 in early December. From there, data readout quickly spiked the share price to the high teens and the stock is consolidating quite nicely above the $17.25 price point at which the secondary offering took place. My initial take is that the current range is an ideal point for readers interested in this name to purchase a pilot position. However, a prudent approach could be to wait for additional confirming data before gaining significant exposure.

Overview

Founded in 2013 with headquarters in San Diego (125 employees), Avidity Biosciences currently sports enterprise value of ~$600M EV and pro forma cash position of $600M providing them operational runway for well over 2 years. There are ~66M shares outstanding after the recent secondary offering (no warrants that I am aware of).

At Credit Suisse Healthcare Conference in November, CEO states that Avidity seeks to tackle one of the fundamental challenges in the RNA space which is delivery outside of the liver. In other words, what GalNac has done for the liver, they aim to do that for a whole range of tissues and cell types.

This led to the development of the company’s technology, the antibody oligonucleotide conjugate (AOC) which was entirely developed in-house. Looking at different delivery mechanisms, they chose the antibody approach and looked at the type of oligo as well. The team has much experience in ASOs (antisense oligonucleotides) and chose the siRNA approach for a range of reasons, including degree of potency that can be achieved with small doses. siRNA was also chosen for the durability you can get as well as well-documented safety profile. However, they do use PMO approach for DMD.

Corporate Slides

Figure 2: Each component engineered to deliver optimal AOC for the target (Source: corporate presentation)

They chose to conjugate to a full antibody as opposed to a fragment but note they do have the IP surrounding use of a Fab (antigen binding fragment) as well. Antibody approach was also chosen to lessen technical risk, as there are a lot of monoclonal antibodies approved today and building on that experience from CMC (chemistry, manufacturing, control) as well.

Endosomal escape is often viewed as a problem, but the company decided to take it head on as a solution. If they can modify the therapeutic sufficiently well so it can withstand lysosomal enzymes, this can be used as a controlled release mechanism allowing for long pharmacodynamic half-lives (single dose in single digits will produce pharmacologic effects for well past 3 months). To their knowledge no one else has cracked the problem of how you let the right things escape without having enzymes attached to it (take advantage of natural breathing of endosomal complex allowing small amount to pay out on daily basis).

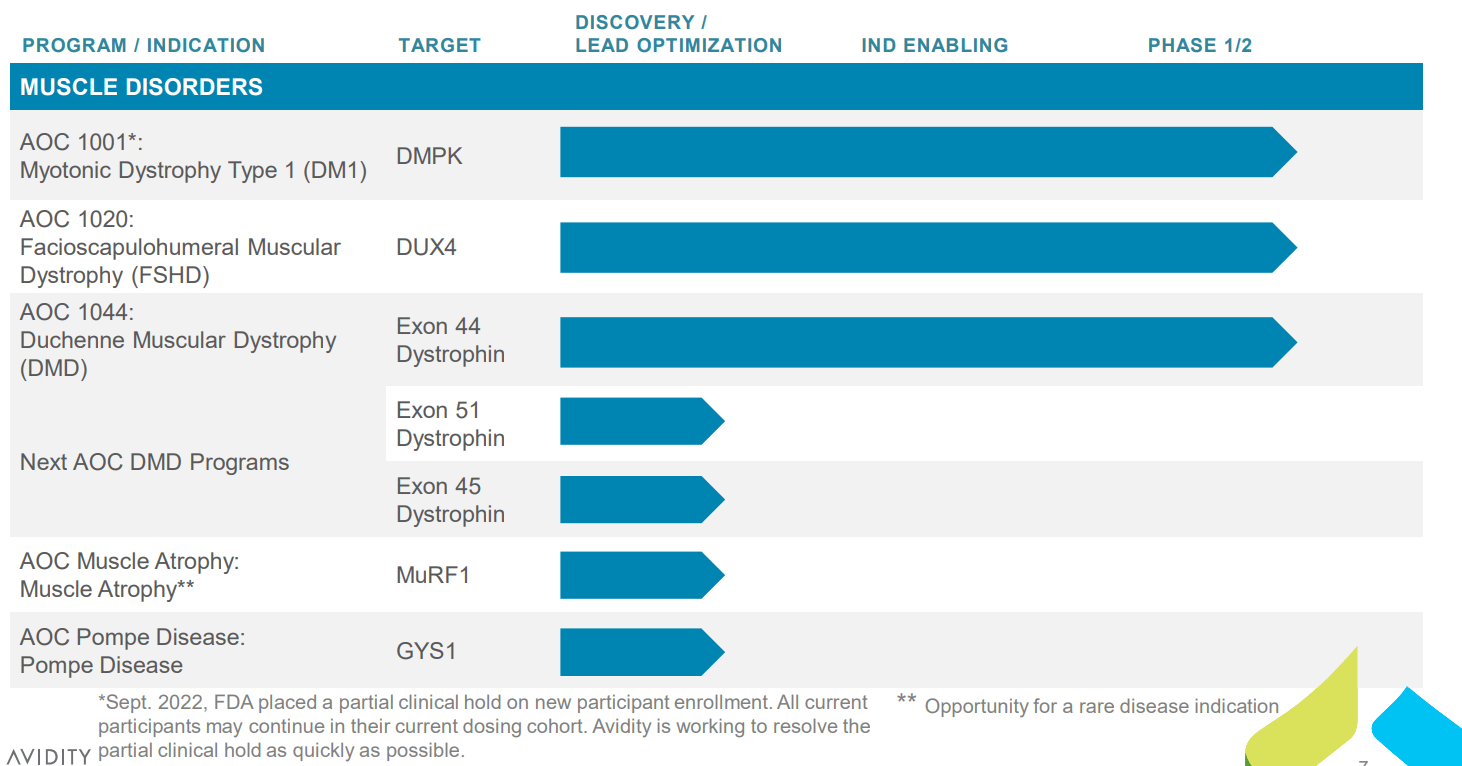

Looking at the pipeline, lead programs are focused on multiple types of muscular dystrophy utilizing this novel technology approach.

Corporate Slides

Figure 3: Pipeline (Source: corporate presentation)

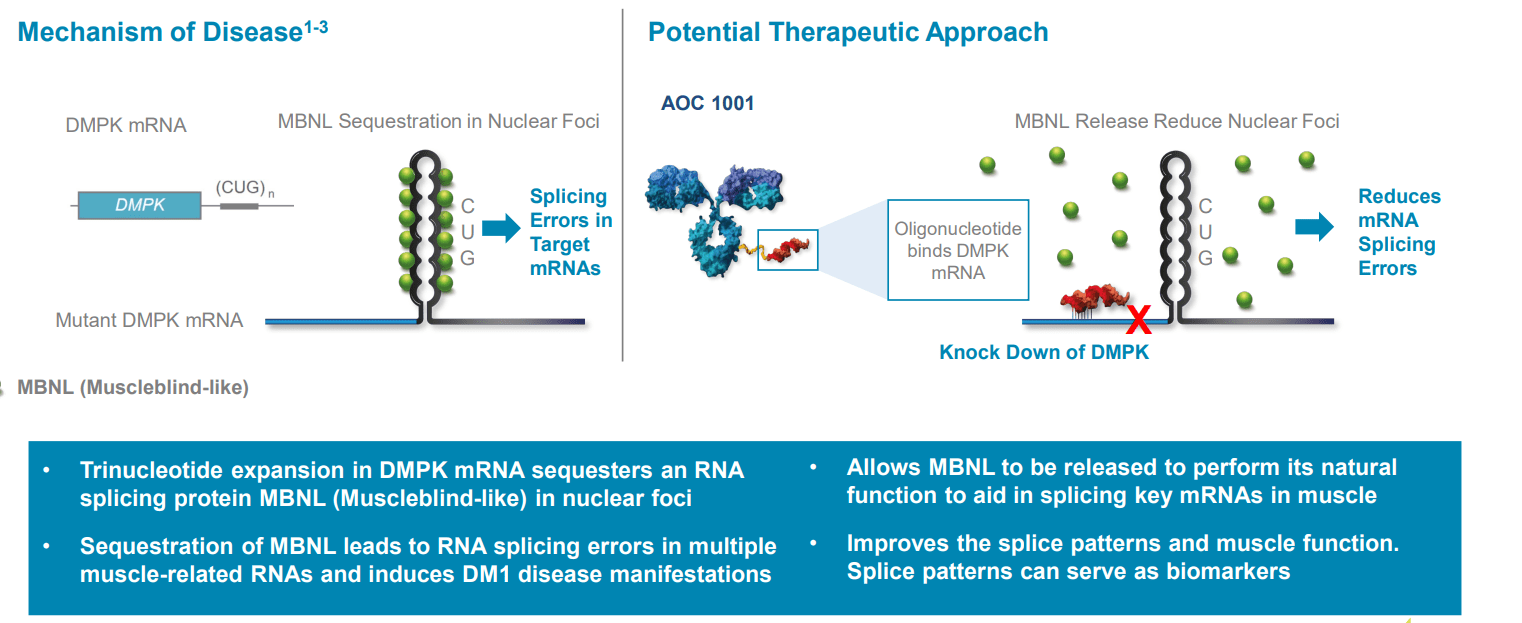

Starting with DM1, it’s a rare disease but more prevalent with about 40,000 to 50,000 people in the US and about the same in Europe with no approved treatments (nothing other than supportive care measures). The condition has been ideal for RNA targeting for many years but no one has been able to effectively deliver an RNA into muscle until now. DMPK is a very specific target they are looking to knock down and is suited to a siRNA approach. Data suggests all machinery for siRNA exists in the nucleus and preclinically in cells from DM1 patients they were able to demonstrate they can get knockdown of nuclear DMPK (and get changes in splice patterns associated from that knockdown). They were also able to demonstrate in animals they get knockdown of nuclear localized messenger RNAs. siRNAs have order of magnitude greater potency than ASOs and longer duration of action.

Corporate Slides

Figure 4: DM1 caused by toxic gain-of-function mRNA and is well-suited to siRNA approach (Source: corporate presentation)

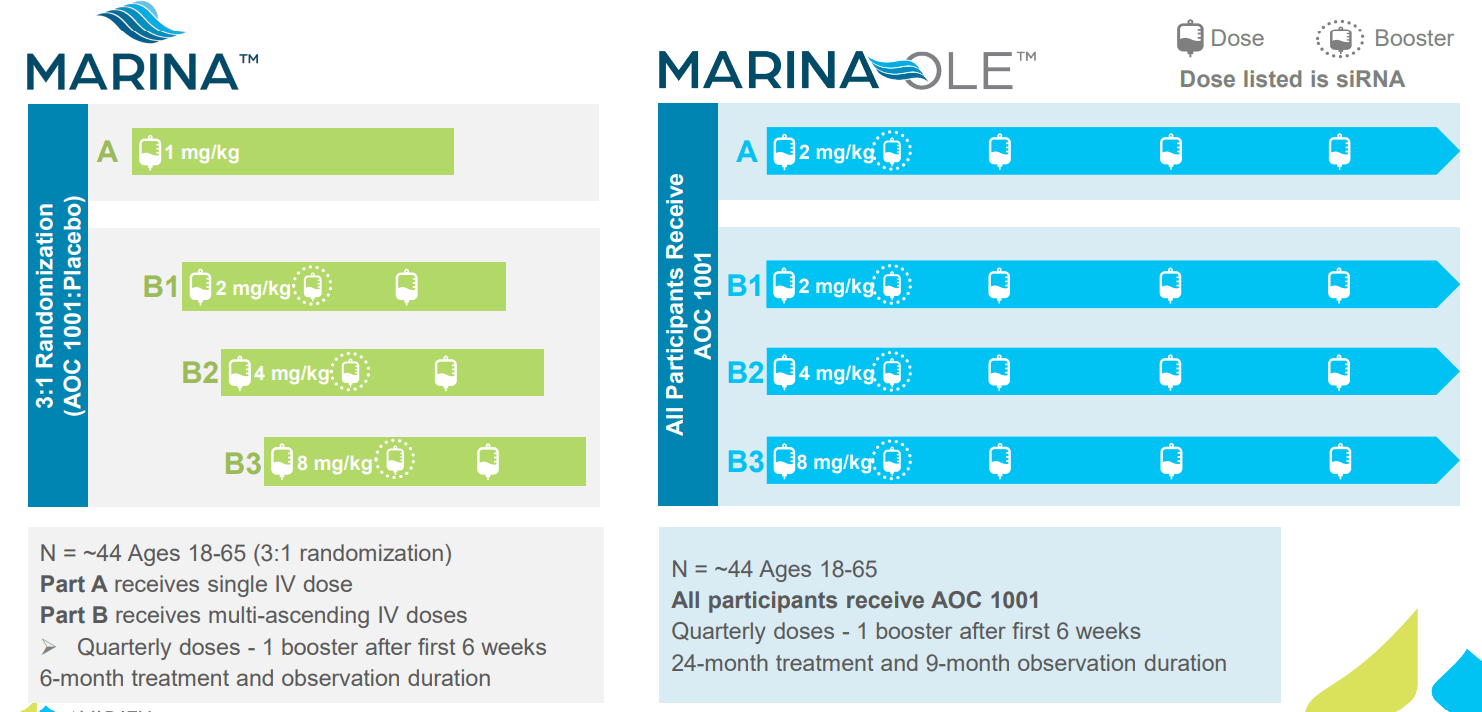

Speaking about the Phase 1/2 MARINA trial (again this was before recent data was presented), it’s divided into A cohort (single dose) and B cohort (participants given 3 doses each). They are followed up for 6 months and then rolled over into open label extension study. At mid-point assessment they are looking at DMPK knockdown and spliceopathy changes (originally thought it was too early to expect anything on clinical endpoints).

Corporate Slides

Figure 5: MARINA trial design (Source: corporate presentation)

As for the bar for later readouts (analyst mentions 50% DMPK knockdown and 25% splice correction), management notes that competitor Biogen has not as of yet disclosed their level of knockdown. Biogen did see some spliceopathy movements in a couple of patients (their best two at the highest dose of 600mg after 8 doses, quite a lot of ASO to be given in a short period of time). As for what we can expect in MARINA, there may be a time-based element to changes so at interim readout they are looking for change in movement heading towards what they would like to see at the end of study (guiding low) and clear separation from placebo with changes in DMPK knockdown and potentially in changes in spliceopathy. Last thing for DMPK knockdown is they want to see consistency of change (active treated subjects showing measurable reductions on the whole). They will follow the data and expect DMPK knockdown would be accompanied with splice changes.

Moving on to their other programs and how the DM1 results could provide readthrough to DMD and FSHD, they are a platform company and using the same antibody so the key question is whether they are truly delivering to muscle (no one has been able to do that before). This accomplishment would be exciting not only for the muscle space but also for other areas they are planning to go into like targeting the heart and the immunology space.

For FSHD, we are reminded there is already a late-stage program in place via Fulcrum Therapeutics (FULC) losmapimod with pivotal results in 2024 per my projections (if there are no delays). Management also anticipated two other companies come into phase 1/2 studies around the same time as them (has not happened so far). Avidity feels they are in a very good shape to enroll their study inside the US and outside (great deal of excitement in the community around this program, which is the first to directly target DUX4, the cause of the disease). They will be looking at changes in MRI (Fulcrum showed this) as well as changes in muscle strength, muscle function and patient reported outcomes among other measures. More generally their strategy as a company is to look for biomarker endpoints wherever possible to see whether a drug is working at an earlier stage and make investment decisions earlier for subsequent clinical trials (also have conversation with regulators for potential accelerated approval in the US).

MARINA Data

On December 14th, the company announced first-ever successful targeted delivery of RNA into muscle with initial data for AOC 1001 in the MARINA study. Keep in mind this provides readthrough to other muscle diseases such as DMD and FSHD they are trying to treat, not to mention efforts to expand into other areas such as cardiac and immunology.

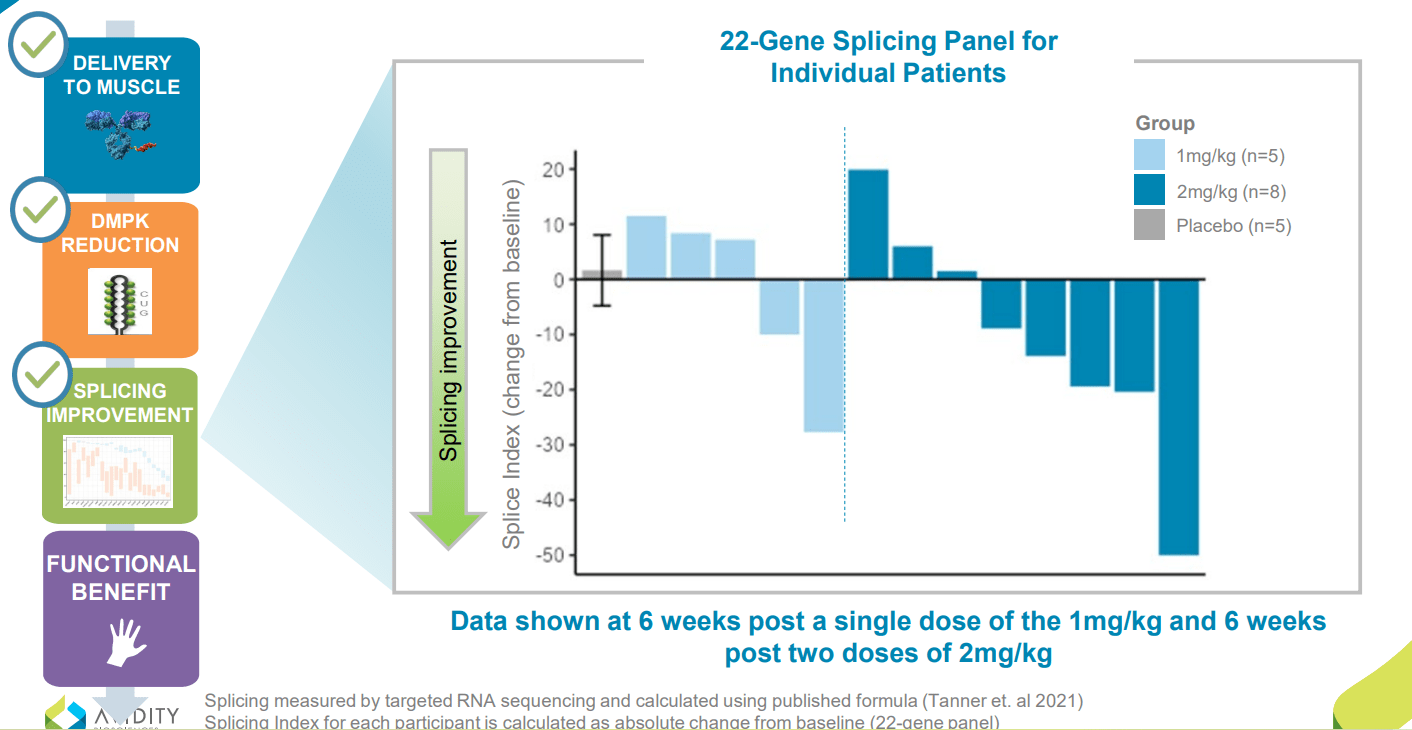

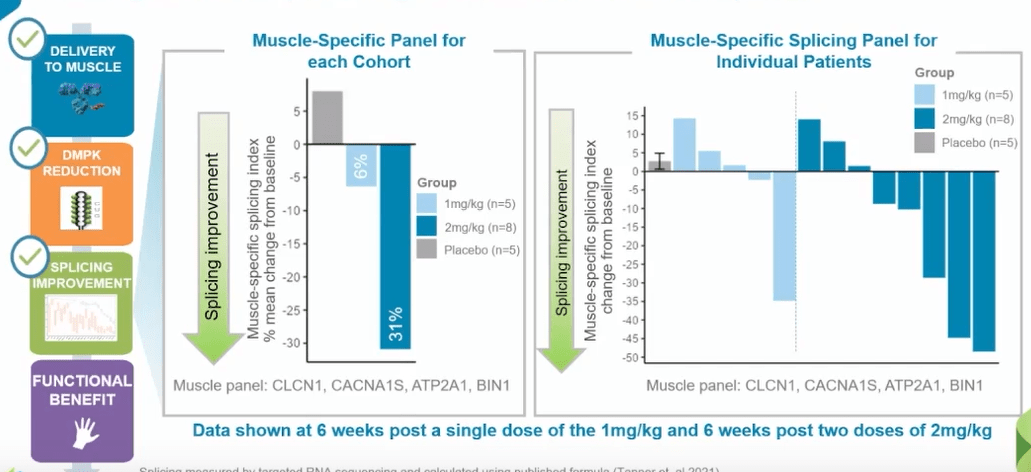

Preliminary assessment looked at safety and tolerability of all 38 participants and key biomarkers in half of them (19). Participants received single dose of 1 mg/kg, two doses of 2 mg/kg AOC 1101 or placebo (again these were the lowest doses of study drug). Meaningful DMPK reduction was observed in ALL AOC 1001-treated patients, with mean reduction of 45% after just a single dose of 1mg/kg or two doses of 2 mg/kg. Also, splicing improvement of 31% was observed in a key set of muscle-specific genes and splicing improvement of 16% across broad 22-gene panel in the 2 mg/kg cohort (demonstrated activity in the nucleus). This latter point is worth emphasizing, as management was not sure they’d see such improvements this early into the trial.

Corporate Slides

Figure 6: Splicing improvements demonstrate impact on disease mechanism (Source: corporate presentation)

Also unexpected were early signs of clinical activity with improvement in myotonia in some participants. Myotonia is where the muscle is unable to relax after contracting, and was measured by video hand opening time (vHOT). It’s important as myotonia is a hallmark of DM1.

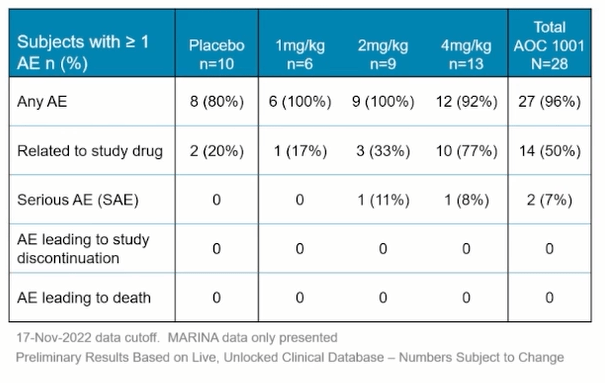

As for the key questions surrounding safety profile, majority of adverse events were mild to moderate and management believes the profile remains favorable. This is in the context of September’s partial clinical hold on new participant enrollment placed by the FDA due to a serious adverse event in a single patient in the 4 mg/kg dose cohort (company continues to work to resolve it “as swiftly as possible” but sounds like we don’t have much visibility there). While it’s just one data point, it’s worth noting that so far 100% of participants completing the MARINA trial have opted to roll over into the open label extension portion.

Corporate Slides

Figure 7: Generally favorable safety & tolerability profile so far (Source: corporate presentation)

Here are a few important nuggets from the associated webcast:

- For the safety data, management notes that high fraction of participants experienced at least 1 adverse event (anticipated for these very high unmet need diseases). These cohorts are very well balanced overall, and in third row, they’ve seen two serious adverse events in the study. One serious AE occurred in 4 mg/kg cohort leading to the partial clinical hold, while the second occurring at 2mg/kg was not related to study drug (reaction to opioid pain medication). Vast majority of AEs were mild to moderate, and there’ve only been 3 serious AEs (two not related to study drug). Most common AEs were Covid-19 (16%) and headache (16%), while others were mild to moderate infusion-related reactions, reductions in hemoglobin and elevations in ASTs/ALTs. They have not seen any changes in bilirubin, no cases of thrombocytopenia and no renal impairment.

- Initial look at MARINA data is only from their two lowest dose levels. More information on the status of the clinical hold will be shared at the end of Q1 2023 (as well as nature of the serious AE). Top-line MARINA results will be shared next year as well.

- Focusing on splicing improvements as observed in Figure 6 above, graph shows change from baseline in splicing index across all 22 genes for each individual patient. One patient at 2 mg/kg shows 50-point improvement in splicing index and several other participants in both cohorts show absolute improvement from 10 to 30 points from baseline. They don’t expect to bring 22 biomarkers into their pivotal study, so based on advice from KOLs and analyzing data they refined their initial panel to a set of 4 muscle-specific transcripts (Figure 8 below). These 4 transcripts are selectively-expressed in muscle, thought to be involved in myotonia and may direct them to early signals of clinical benefit.

Corporate Slides

Figure 8: 4 muscle-specific transcripts to be utilized in pivotal study (Source: corporate presentation)

- In these muscle-specific biomarkers, we see 6% improvement in 1 mg/kg cohort and impressively a 31% improvement in splicing at 2 mg/kg following 2 doses. Lowest doses show 6 of 13 patients with clear improvement in muscle-specific splicing (can’t get improved splicing without getting in the nucleus, knocking down mutant DMPK and allowing free muscleblind-like protein to do its job).

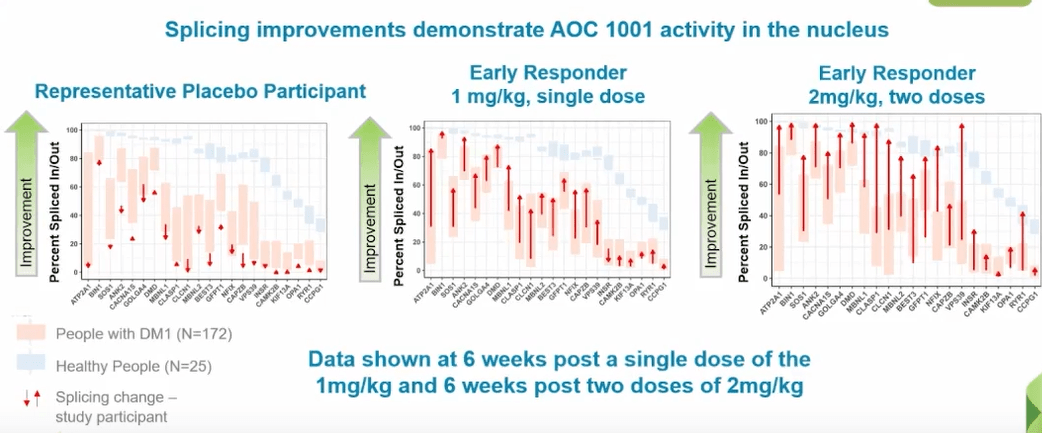

- For 2 early biomarker responders (Figure 9 below), starting with representative placebo participant on the left we can see splicing across 22 genes does not change much. In contrast, middle panel shows early responder dosed 1 time at 1 mg/kg and majority of genes are trending toward splicing found in healthy volunteers. On far right, we can see the panel for early responder at 2mg/kg six weeks after two doses (dramatic improvement in splicing).

Corporate Slides

Figure 9: Improved splicing in 2 early biomarker responders versus representative placebo participant (Source: corporate presentation)

- Looking at myotonia, management never thought they’d see anything this early. For most of us, we can make a fist and then open up our hand very fast. Video shows it’s difficult and challenging for the patient to open their hand when asked to. Day 43 (6 weeks after lowest dose) shows clear improvements in their myotonia. Just as important, by Day 183 (6 months after the single dose) the benefit wanes and their myotonia returns. Video for participant on 2mg/kg dose (3 doses) shows dramatic improvement from baseline all the way through Day 183. CEO explains why this is important for improvement in quality of life, including daily activities like brushing your teeth or combing your hair (opening doorknob, holding on to glass of water, etc.).

- As for implications of success in muscle, keep in mind there are monoclonal antibodies for many other cell surface receptors and the company is building on that knowledge to design this disruptive & useful platform to deliver these therapeutics to cardiac muscle, cells in immunology and other cell & tissue types. Aside from DM1, for we can expect healthy volunteer data in 2H 23, and for FSHD, we can expect preliminary assessment from the FORTITUDE study in 1H 24.

- Moving on to Q&A, on the SAE in 4 mg/kg dose arm analyst wants to know how much more work is needed to fully-characterize the SAE. Management states they are really close to the end, will submit complete response and FDA will have 30 days to review and provide their conclusion (will disclose toward the end of Q1). As for whether myotonia could be used as a pivotal endpoint in phase 3 study, management states it’s too early to speculate before discussion with regulators. KOL states that you do NOT see natural improvement in myotonia the way that was showed in the videos (not seen in clinical practice). You can occasionally use anti-myotonia agents to treat the symptoms but those act on skeletal muscle membrane themselves (don’t reflect impact on underlying disease progression or pathogenesis).

Other Information

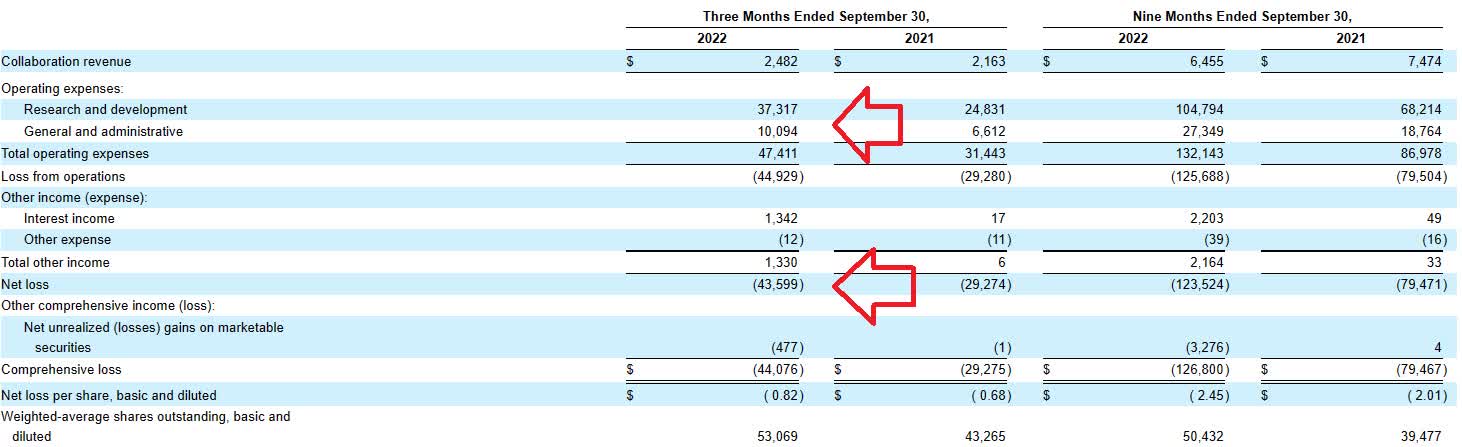

For the third quarter of 2022, the company reported cash and equivalents of $405M (does not include $207M from recent financing). Research and development expenses rose by roughly 50% to $37.3M, while G&A increased to $10.1M. Rounding up to quarterly net loss of $50M or $200M for the year, that seems reasonable for a company at this stage and would put them at well over 2 years of cash.

Quarterly Filing

Figure 10: Net loss, R&D expense and G&A increasing significantly yet within acceptable range (Source: 10-Q filing)

As for competition, there are a LOT of companies with assets targeting these diseases such as DMD and DM1. For the latter, tideglusib is a GSK3-inhibitor in late-stage development by AMO Pharma for the congenital phenotype of DM1 (March 2023 primary completion date). AT466 is an AAV-antisense candidate in preclinical development by Astellas Gene Therapies, while Dyne Therapeutics (DYN) has a Fab linked oligonucleotide currently enrolling patients in a phase 1/2 global study. DYNE-101 will treat 64 adult DM1 patients during 24-week MAD, placebo-controlled period followed by 96-week long term extension. Initial data including safety, tolerability and splicing are expected 2H 23 (will be important to see how that measures up against AOC-1001). Earlier in December, Vertex Pharmaceuticals (VRTX) paid Entrada Therapeutics (TRDA) $224M upfront plus nearly $500M in potential milestones and royalties to gain control of ENTR-701 for DM1. However, I note that just yesterday that Entrada’s DMD program was put on clinical hold (regarding its IND) and perhaps that impacts clinical timeline for DM1 program as well (prior guidance was for IND filing 2H 23).

For FSHD, the first one I think of is Fulcrum Therapeutics’ losmapimod (p38 MAPK inhibitor that appears to modulate DUX4 expression) already in phase 3 study with primary completion date in 2024. Another that comes to mind is Arrowhead Therapeutics’ (ARWR) ligand conjugated oligonucleotide in preclinical development (don’t believe I even saw it mentioned in Q3 report, so perhaps it’s been put on the backburner for now). For DMD, there is much more in the way of competition via approved treatments from PTC Therapeutics and especially Sarepta Therapeutics (SRPT) via its FDA-approved exon skipping drugs including Eteplirsen, golodirsen, casimersen, PPMO in phase 2 and gene therapy programs.

As for institutional investors of note, EcoR1 Capital continues to add to its position last reported at 2.899M shares in November. Cormorant Asset Management owns just over 2M shares. RTW Investments continues to add to its position with nearly 4.8M shares.

As for relevant leadership experience, CEO Sarah Boyce served prior as President of Akcea Therapeutics. Chief Medical Officer Steven Hughes served prior as CMO at Arcturus Therapeutics and Chief Clinical Development Officer at Ionis Pharmaceuticals. CFO Michael MacLean served in the same position at Akcea Therapeutics.

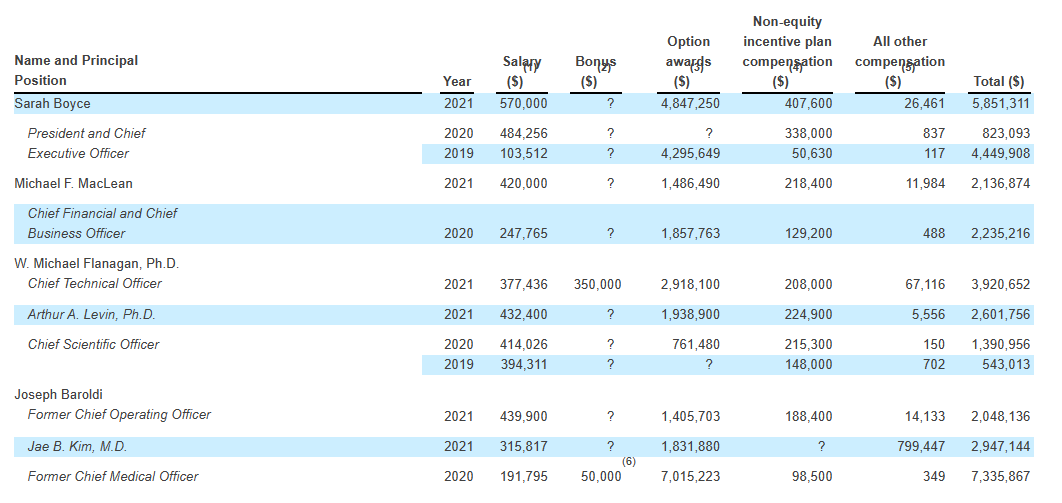

Moving on to executive compensation, cash portion of salaries appears in a reasonable range although options awards do seem a bit on the high side (including $4.847M for President and CEO Sarah Boyce).

Proxy Filing

Figure 11: Executive compensation table (Source: Proxy filing)

As for Twitter nuggets, this thread is interesting on the subject of why splicing for AOC-1001 in DM1 showed dose-dependency but DMPK knockdown didn’t. Much like management’s prior commentary stated, deepening of splicing changes is expected with more doses over time as well as at higher doses (SAEs and tolerability profile remains a key question in that regard as well).

Moving on to IP, the company has 13 issued US patents and 29 pending US patents not to mentioned filed applications for other territories. Focusing specifically on AOC-1001, they have one issued US patent, 9 pending US patent applications and 11 pending patent applications for foreign jurisdictions. These patents include methods of manufacturing, formulations, composition of matter and methods of treating diseases among others (expected expirations in 2038 to 2041 range, not including term extensions). For FSHD AOC candidate, expected patents should expire in 2041 to 2042 range.

Final Thoughts

To conclude, with EV of ~$600M Avidity Biosciences appears reasonably valued after recent proof of concept results in DM1 and accounting for risks involved including questions surrounding SAEs as well as substantial up and coming competition in the field. IF data for DM1 program continues to be encouraging including deepening of splicing changes, I could see significant revaluation higher being warranted (especially when they move into pivotal study with clear line of sight to what approval could look like and what biomarkers/measures specifically the FDA would require).

I definitely appreciate stories such as this one that provide us substantial optionality, as initial data in DM1 reads through to other forms of muscular dystrophy and from there the ability to move into other areas such as heart and immunology.

For readers who are interested in the story and have done their due diligence, RNA is a Buy at present levels. A prudent entry strategy could be to purchase a pilot position, then await clarification on the SAE of interest in late Q1 before considering accumulating further exposure.

As for my personal clinical-stage portfolio, I am likely to await further derisking via the Q1 update on nature of the serious adverse event before I revisit.

While dilution in the near term is not expected given 2+ years of cash on hand, key risks here include high amount of emerging competition across these muscular dystrophies (both from later stage peers like Fulcrum Therapeutics in FSHD as well as big pharmaceutical firms moving into DM1 like Vertex). Disappointing safety update in Q1 or clinical results later in 2023 for DM1 program would negatively impact valuation, as could any delays to currently estimated clinical timelines.

Author’s Note: I greatly appreciate you taking the time to read my work and hope you found it useful. While I post research on many companies that interest me, in ROTY (clinical stage) and Core Biotech (commercial stage) portfolios I own just 15 or fewer names in order to focus on stories that are highest conviction for me.

Be the first to comment