It’s time to talk about one of the best dividend growth stocks on my radar. That company is Automatic Data Processing (NASDAQ:ADP).

Founded in 1949, ADP is not only a mature company with Dividend Aristocrat status but also a company that has figured out how to stay on top of its peers.

My most recent article on this company was written on November 26, when I went with the title “Dividend Investors Take Note: Automatic Data Processing Has It All!”

Since then, shares have returned 9%, which is roughly in line with the performance of the S&P 500.

In this article, I get to update my thesis as the company just reported its earnings.

The company confirmed the bull case, as it benefited from significant growth in key areas and is able to maintain strong guidance.

Not only does this bode well for its valuation, but it is also great news for its dividend, which should continue to enjoy consistent elevated dividend growth.

With all of this in mind, let’s dive into the details!

The Place For Dividends And Growth

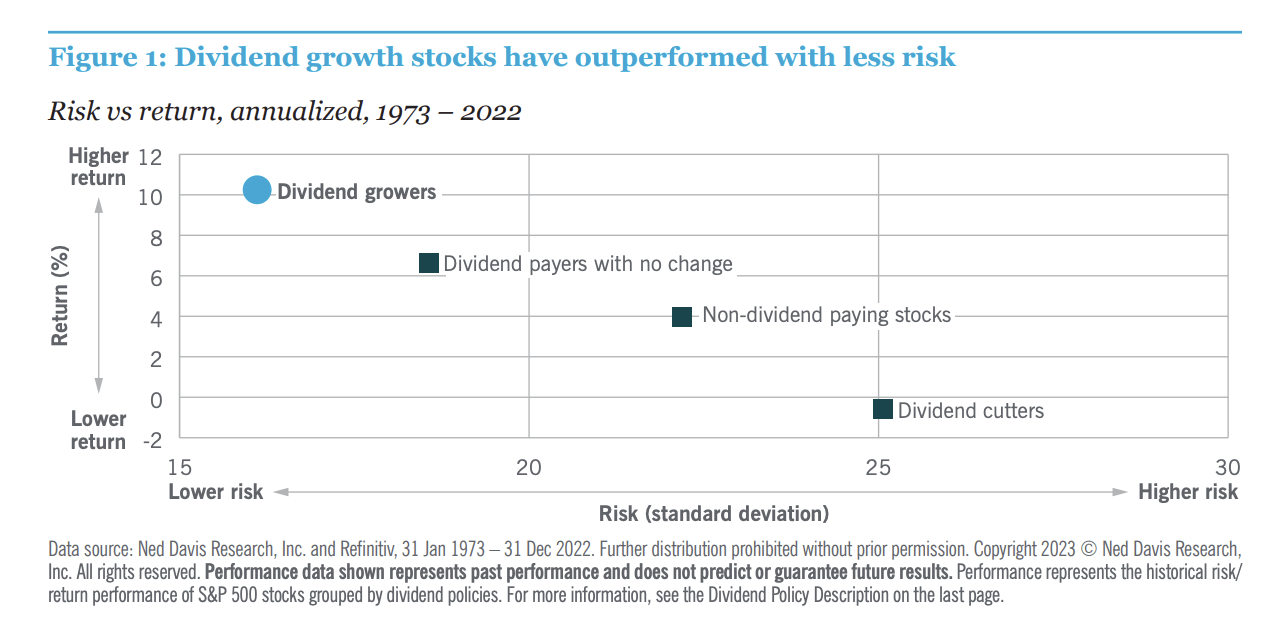

In my prior article, I started by explaining why dividend growth stocks are among the best financial assets someone can own to build wealth with a fantastic risk/reward profile.

While individual preferences vary, I think investors are looking for businesses with wide moats, plenty of growth opportunities, proven business models, healthy balance sheets, decent yields, consistent dividend growth, and the ability to outperform the market with subdued volatility.

In other words, we try to find businesses that give us elevated returns with subdued risks – the holy grail of dividend investing.

Nuveen

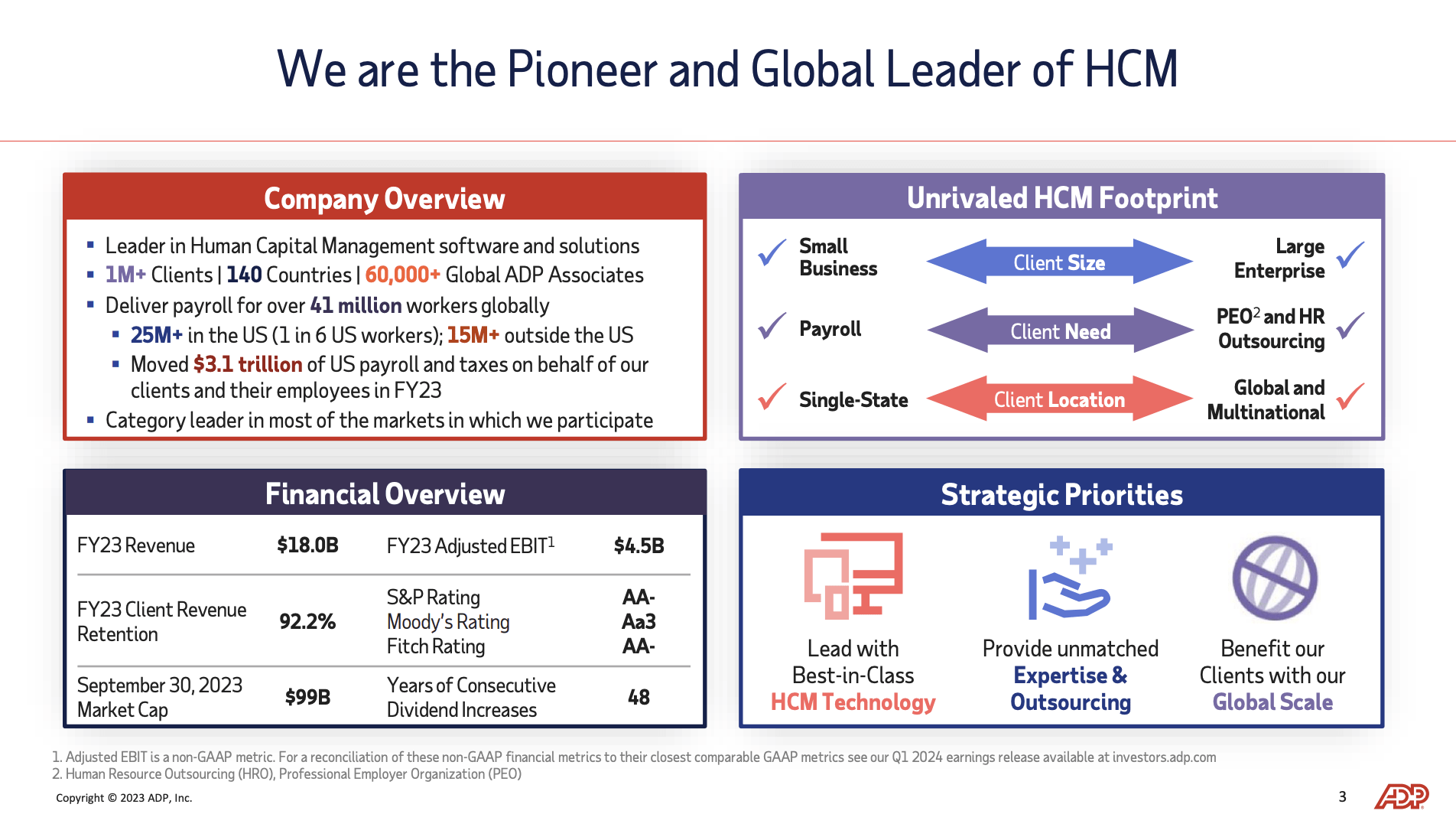

ADP, founded a few years after the end of the Second World War, has it all.

With services covering payroll, HR outsourcing, time, and attendance in 140 countries and close to a million clients, this company has an excellent track record of delivering shareholder returns.

Automatic Data Processing

As I wrote in my prior article, since 1986, ADP shares have returned 14.0% per year, beating the S&P 500’s annual performance of 10.5% by a wide margin.

The company currently yields 2.3%, backed by a 60% payout ratio.

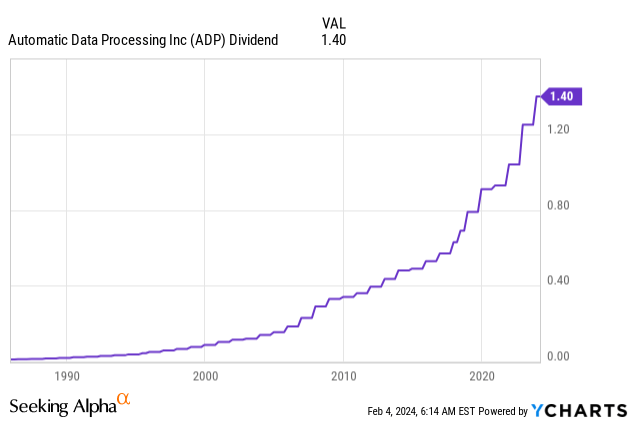

The dividend has been hiked for 49 consecutive years, which means it is just one year away from becoming a Dividend King!

The five-year dividend CAGR is 13%, which is elevated for a company as old as ADP – especially given its almost-King status.

It also has a credit rating of AA- from all major rating agencies, which is one of the best ratings on the market.

The company’s most recent hike was 12% on November 8.

ADP’s Firing On All Cylinders

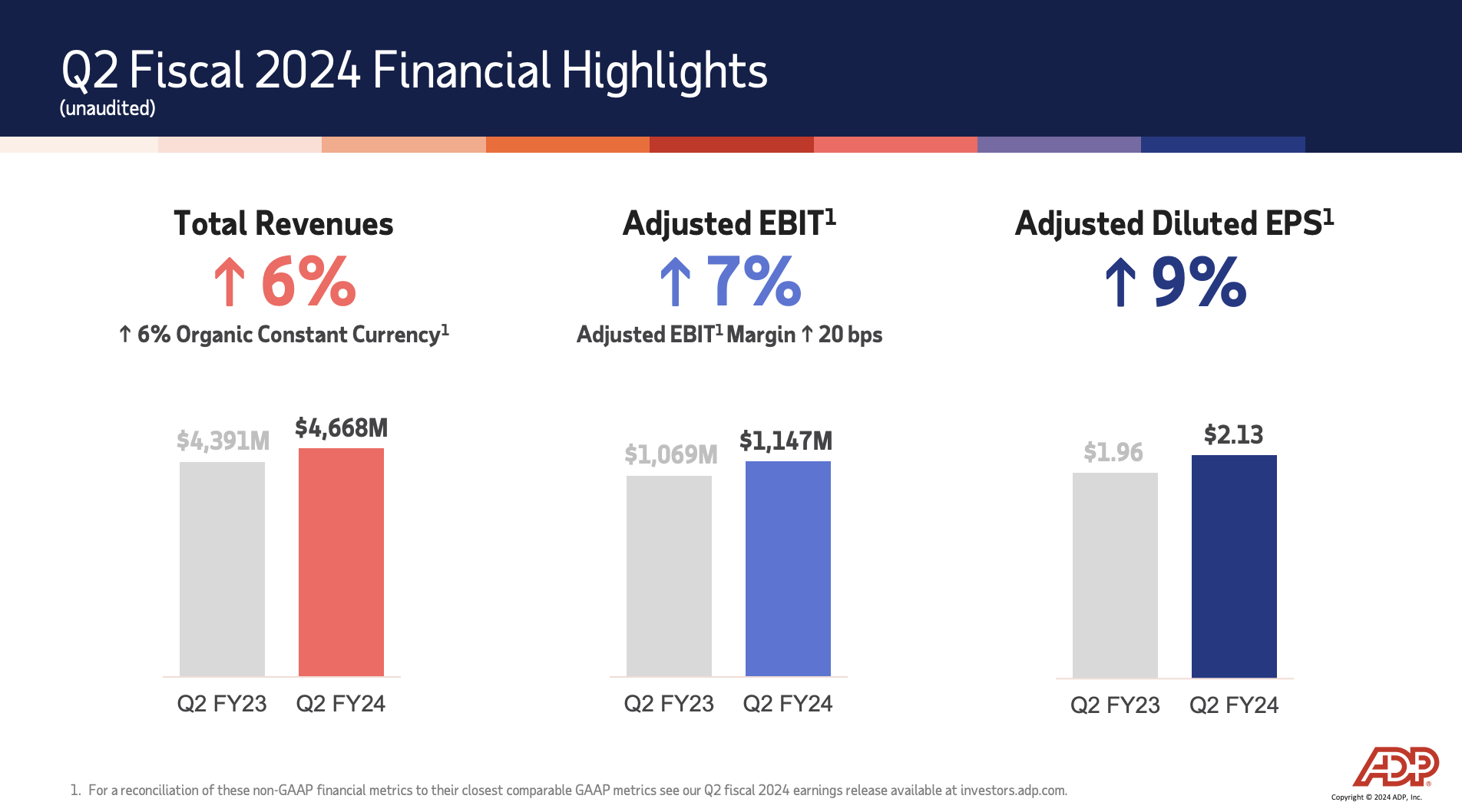

On January 31, ADP reported its second-quarter earnings of its 2024 fiscal year.

Despite some economic headwinds like poor sentiment in the manufacturing sector and subdued consumer sentiment, ADP’s business remains robust, marked by a 6% improvement in revenue and a substantial 9% increase in adjusted earnings per share.

Automatic Data Processing

Diving a bit deeper, we find that growth was supported by all major segments.

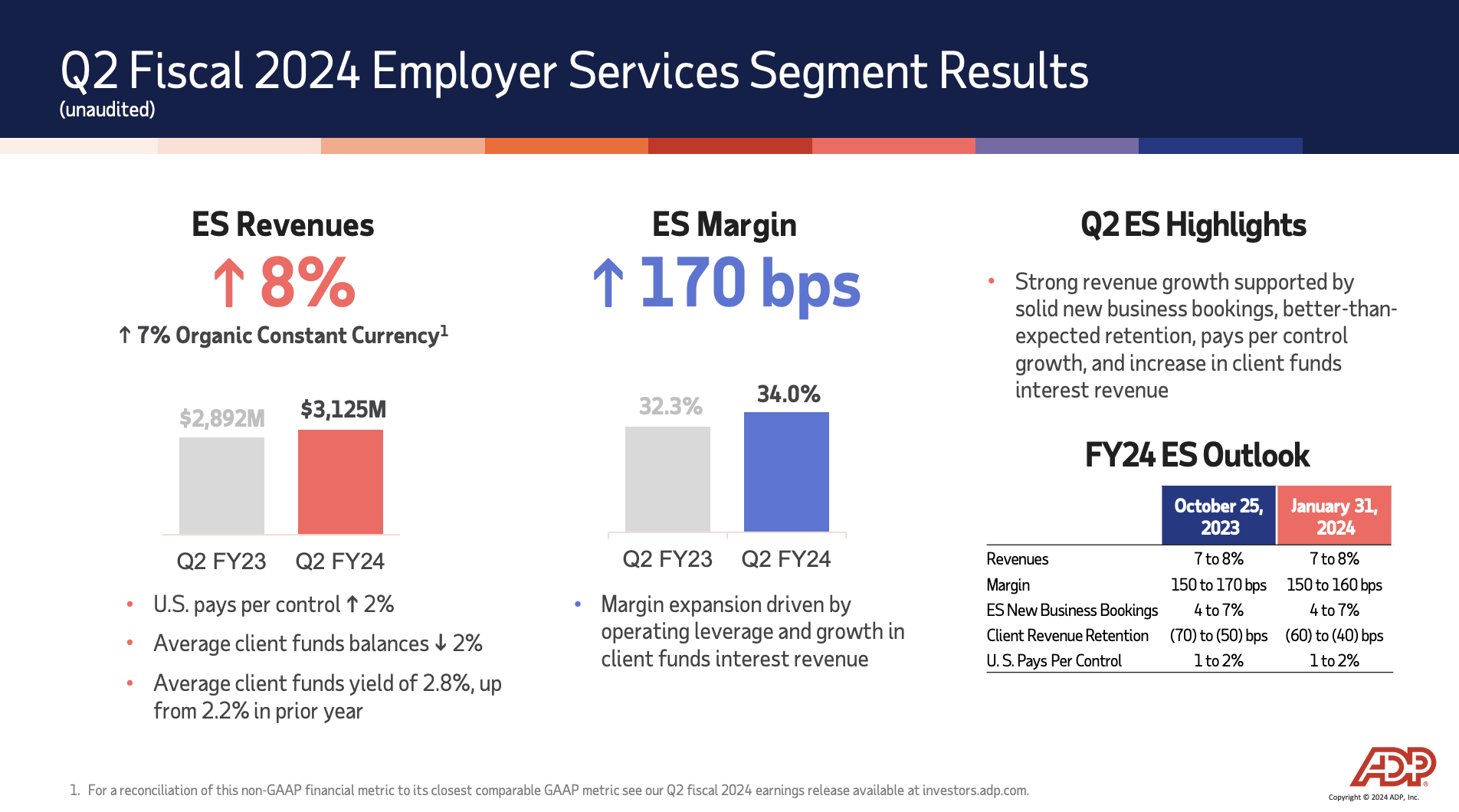

For example, in the second quarter, ADP’s Employer Services (“ES”) segment showed a robust performance, reporting an 8% increase in revenue on a reported basis and a 7% growth organically, slightly surpassing expectations.

This growth was attributed to a number of factors, with particular strength noted in the small business portfolio and international business, both contributing significantly to the overall quarterly revenue.

Furthermore, the company made the case that ES has shown its ability to capture market demand, resulting in a record second-quarter booking volume.

Automatic Data Processing

Despite a marginal decline in retention during Q2 compared to the previous year, the segment’s performance exceeded expectations.

This led to an upward revision of the full-year retention outlook, with an anticipated 40 to 60 basis point decline, ten basis points better than the previous forecast.

The pay-per-control growth for ES was reported at 2% in Q2, aligning with expectations. The full-year outlook for pay-per-control growth is maintained at 1% to 2%, indicating a steady trajectory.

Furthermore, client funds interest revenue, a significant component of ES, increased in line with expectations during Q2. However, the company revised its full-year outlook to reflect changes in prevailing interest rates since the last update.

The fiscal 2024 client funds interest revenue is now expected to be in the range of $985 to $995 million, with a net impact from the client funds extended investment strategy adjusted to $835 to $845 million.

Automatic Data Processing

Moving over to the company’s Professional Employer Organization (“PEO”) segment, we find that it reported a 3% revenue growth in Q2, primarily driven by a 2% growth in average worksite employees.

This performance was in line with expectations, and the company used its earnings call to express optimism about the signs of stabilization in PEO pay-per-control growth.

Notably, PEO’s new business bookings in Q2 were strong, indicating continued healthy activity levels within the segment.

Despite the positive performance, PEO margins experienced a decrease of 50 basis points in Q2. This was attributed to the assumption that this year’s workers’ compensation reserve release benefit would be lower than the previous year’s, leading to a further narrowing of the PEO margin expectation for the ongoing fiscal year.

Going forward, the company anticipates a gradual ramp-up in worksite employee growth in the latter half of this fiscal year, allowing it to maintain the full-year growth outlook of 2% to 3%.

What’s Next?

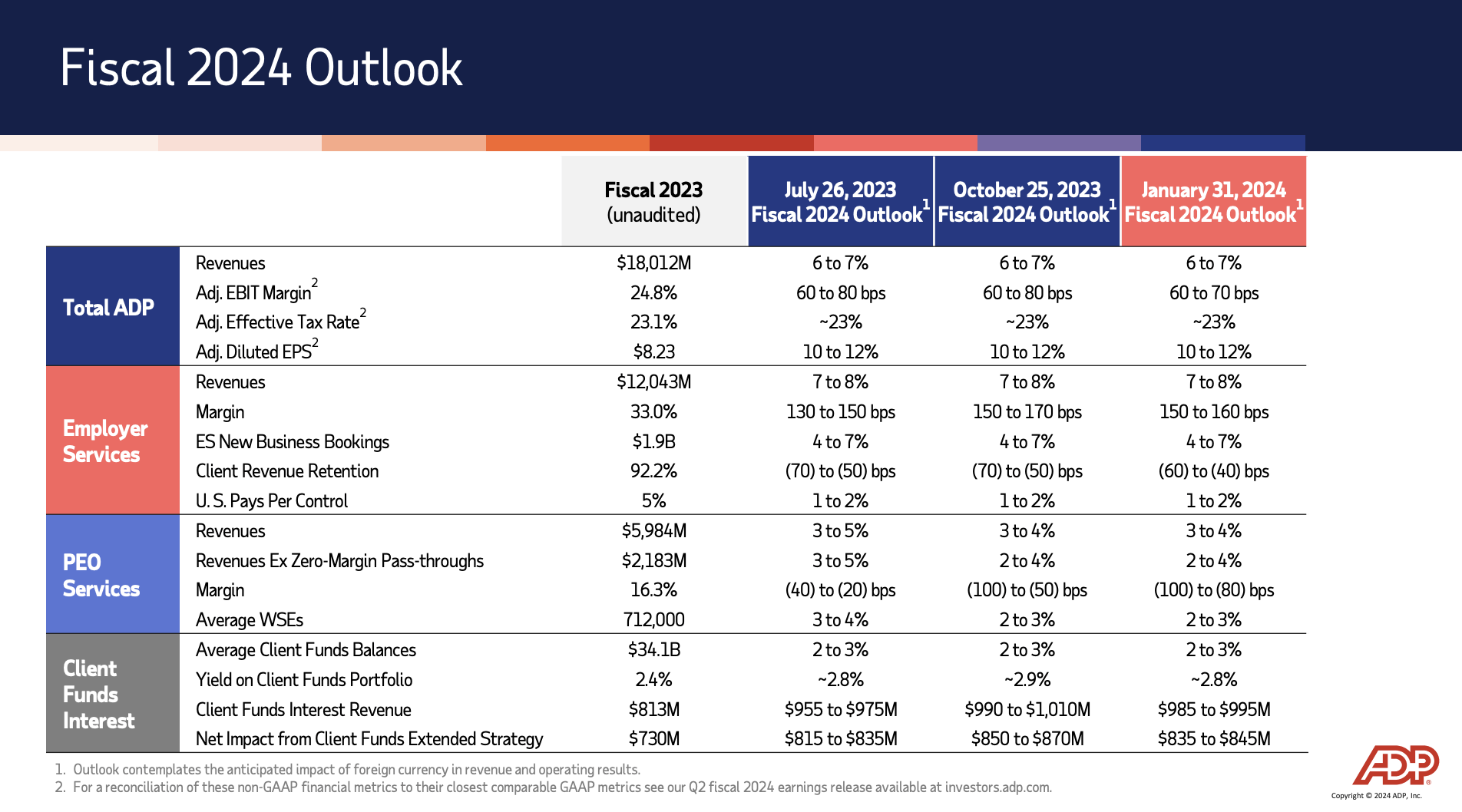

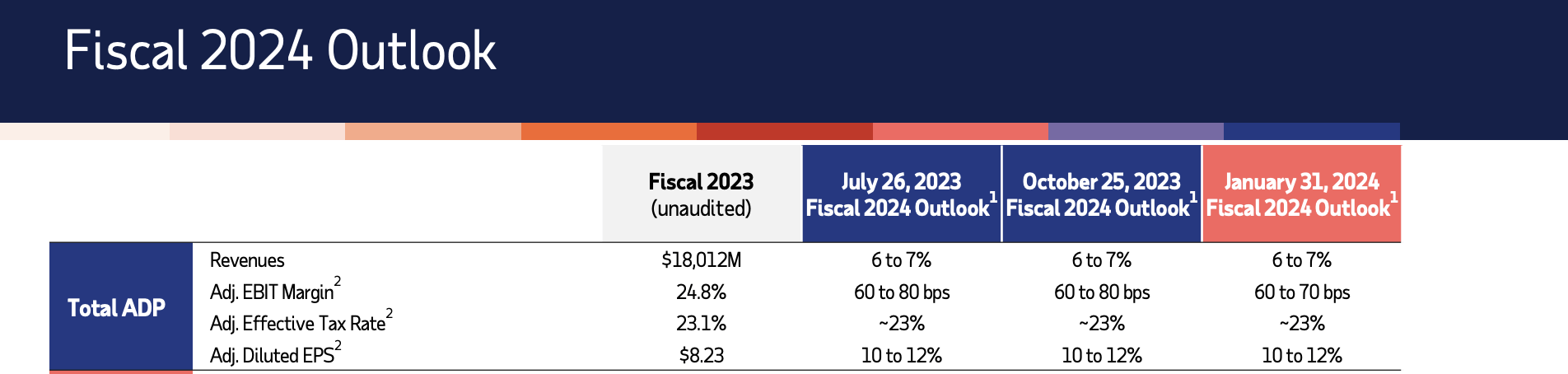

I already gave it away using the overview above, but by combining both segments, ADP’s consolidated outlook for 2024 remains stable, with no changes to the revenue growth forecast of 6% to 7%.

Despite adjustments in segment margins, the adjusted EBIT margin is now expected to increase by 60 to 70 basis points, a slight adjustment from the initial outlook of 60 to 80 basis points.

Automatic Data Processing

During its earnings call, the company also mentioned a few developments that support its leadership position.

For example, ADP received accolades for its product leadership from major industry analysts during the second quarter.

Everest Group recognized ADP as the highest leader among 27 providers in its multi-country payroll solutions report.

Nelson Hall identified ADP as a leader in its payroll services vendor evaluation.

Ventana Research acknowledged ADP as an exemplary leader in its payroll management buyers guide.

In general, ADP’s strategic collaborations and initiatives position it to capitalize on long-term tailwinds and opportunities in the market.

The expansion of global collaborations, such as a strategic partnership with Convera for streamlined global payroll and cross-border payments, shows ADP’s commitment to providing comprehensive solutions for its clients operating in diverse regions, which could help it achieve its ambitious long-term goals.

In 2021, the company revealed that it was looking for 7% to 8% annual revenue growth. When adding potential margin enhancements, the company aims for at least 11% annual EPS growth.

Automatic Data Processing

On top of that, the launch of ADP Retirement Trust services reflects the company’s aim to address the growing demand for retirement services.

By standing up its own trust services entity, ADP positions itself as a trusted player in the financial industry, offering long-term benefits to both the company and its clients.

In general, this move aligns with the broader trend of businesses seeking integrated solutions from a single trusted provider.

So, what does this mean for its valuation?

Valuation

As I just mentioned, on a long-term basis, ADP expects to grow its EPS by 11% to 13% per year.

When adding its 2%-ish yield, the company could return 13% to 15% per year, which is in line with its long-term performance mentioned at the start of this article.

The only problem is that the valuation matters as well. After all, the brief calculation above is based on an unchanged valuation.

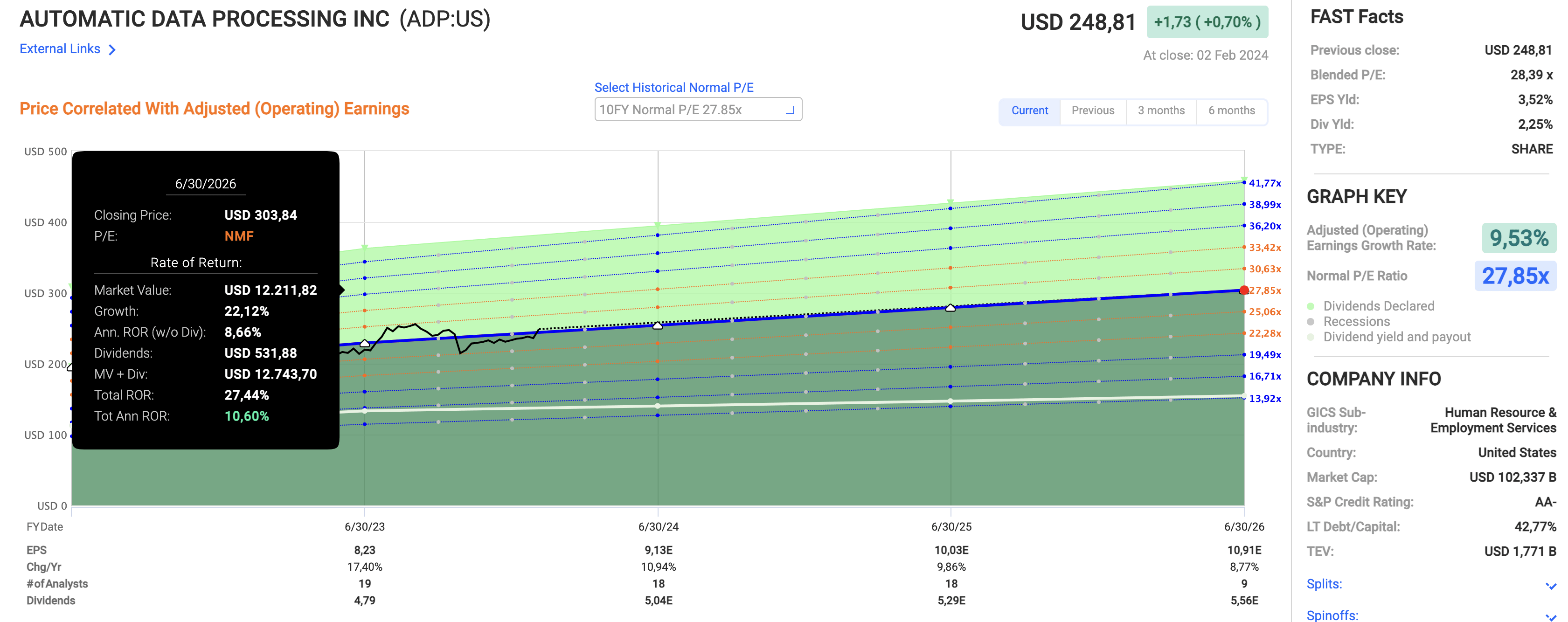

Using the data in the chart below:

ADP is currently trading at a blended P/E ratio of 28.4x, which is slightly below its 5-year average of 29x EPS.

Over the past ten years, the normalized valuation is 27.8x.

Going back to 2003, the normalized valuation is 25x EPS, which shows that over the past few years, investors have consistently applied a higher multiple to APD’s business.

Regarding its earnings, analysts agree with the company, as they see 11% growth in 2024, 10% growth in 2025, and 9% growth in 2026.

While these numbers are subject to change, they hint at a >10% annual return if the company maintains a 27.9x earnings multiple.

FAST Graphs

With that said, I remain bullish on the company, expecting that it will continue to generate very strong long-term returns.

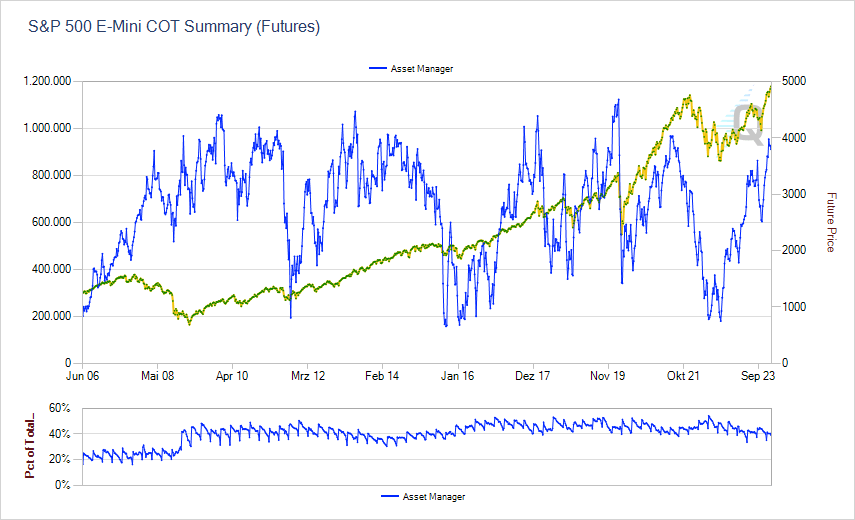

The only reason why I am not a buyer is my general belief that the market is overbought.

Asset manager net positioning in S&P 500 futures is close to “peak” levels, and I have mentioned in multiple articles (like this one) that I somewhat dislike the overall valuation of the market.

CME Group

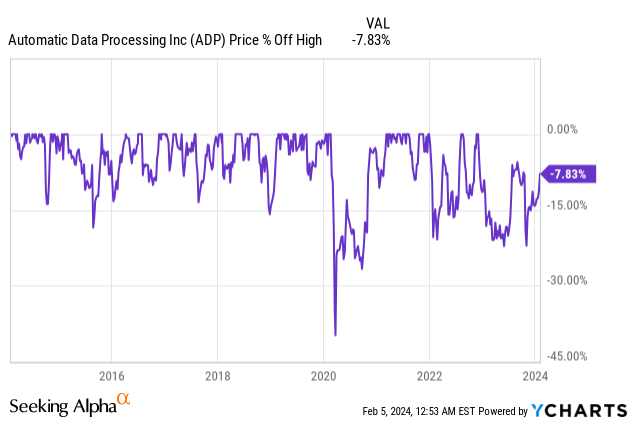

Hence, I keep ADP on my watchlist as a potential target when I start to deploy more cash from my reserves.

Generally speaking, I look for 8-12% declines before buying high-quality stocks, which tends to happen quite a lot in the case of ADP, as we can see below.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment