Ran Kyu Park/iStock via Getty Images

Autoliv (NYSE:ALV) is a market leader in manufacturing of safety systems for passenger cars. In the short term Autoliv will benefit from the order backlog of car manufacturers whose production capacity has been constrained by the supply chain interruptions. Autoliv also has a significant exposure to China and the reopening of its economy could boost Autoliv’s business. Autoliv is a brand and technology neutral way to invest into the auto industry.

Although the company had to interrupt its decade-long dividend growth streak in 2020, Autoliv is back at growing the payout again together with stock buybacks. Autoliv is a stock for income investors who want to participate in the auto industry and structural growth of the safety requirements in passenger cars. The strong balance sheet will help to ride through the volatility of the industry and economic turbulence.

Company overview

Autoliv develops, manufactures and sells passive safety systems to car manufacturers. It has an annual revenue of nearly $10 billion and employs over 60 000 people. Autoliv operates globally, generating 28% sales in Europe, 31% in America and 41% in Asia. The origins of the company are in Sweden, where it still has its headquarters. Airbags and other segment represents 65% of the company’s revenues and the rest is seatbelts. The customer base of Autoliv is well diversified covering all the major car manufacturers.

In 2018 Autoliv spun off Veoneer, which is a company specialized in active safety equipment such as radars, sensors and lidars. The spin-off was driven by a notorious activist investor called Cevian Capital which still owns close to 10% of Autoliv. The founder of Cevian Capital Christer Gardell recently commented on the company in an interview by EFN:

Autoliv is an excellent company with a 50% market share. The sales of passenger cars has been on a depressed level for 3-4 years, so there’s pent up demand. Perhaps 2023 is not the year when this demand is realized, but it will be and Autoliv is very well positioned. Autoliv has succeeded in raising prices in difficult conditions and industry where business is conducted in a sphere of long-term contracts. The potential increase of volumes will help with profitability in the future.

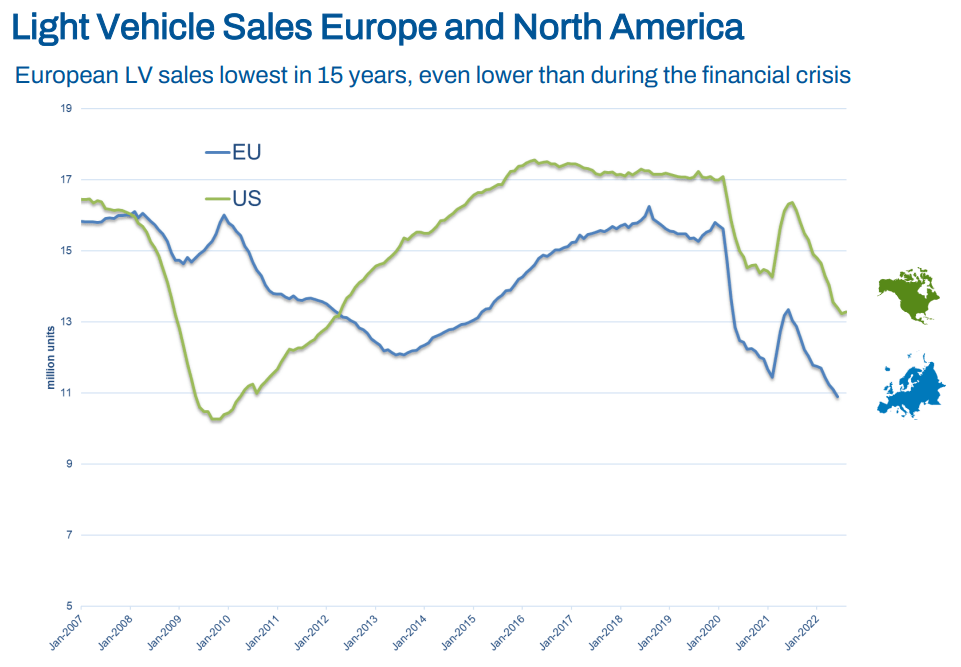

Light vehicle sales trends. (Autoliv’s investor material)

After the spin-off Autoliv most likely positions itself as a cash cow rewarding shareholders with dividends and buybacks. In order to do so, its competitive power must rely on product quality and reliability, price competitiveness and remaining technologically relevant, which is supported by 6400 patents. The importance of the product quality and reliability is showcased by the fate of Japanese Takata which ended up in bankruptcy due to a disastrous product recall in 2018.

The fundamentals are a little controversial

New car sales will most likely falter

The used car market is in dire straits in the U.S. and Europe and most likely the new car market will follow suit. According to J.P. Morgan the average cost to produce a new vehicle rose 116% in 2021. While car prices are increasing, the purchasing power of consumers is decreasing.

“There is demand destruction taking place,” said Brinkman, pointing to indicators such as the University of Michigan’s Buying Conditions for Vehicles survey. Consumers express record low sentiment toward the purchase of a new vehicle, citing high prices and rising interest rates.

The current average price target for Autoliv is $90. The analysts are expecting the earnings to increase this year nearly 60% to $6.92 per share. However, a Swedish bank called Swedbank recently commented that the consensus estimate might be too optimistic due to exchange rates and cost pressures. In its estimates Swedbank has 7% lower EBIT than the consensus. It’s not difficult to agree.

Autoliv has a large exposure to China, which is both an opportunity and a risk. China’s share of global passenger vehicle production is approximately 31% and 20% of Autoliv’s sales is derived from China. As the company states itself, China is an extremely competitive market. However, it’s also a growing market and it would be foolish to think that Chinese car brands would settle themselves only in the domestic market.

The business is recovering and long-term picture is promising

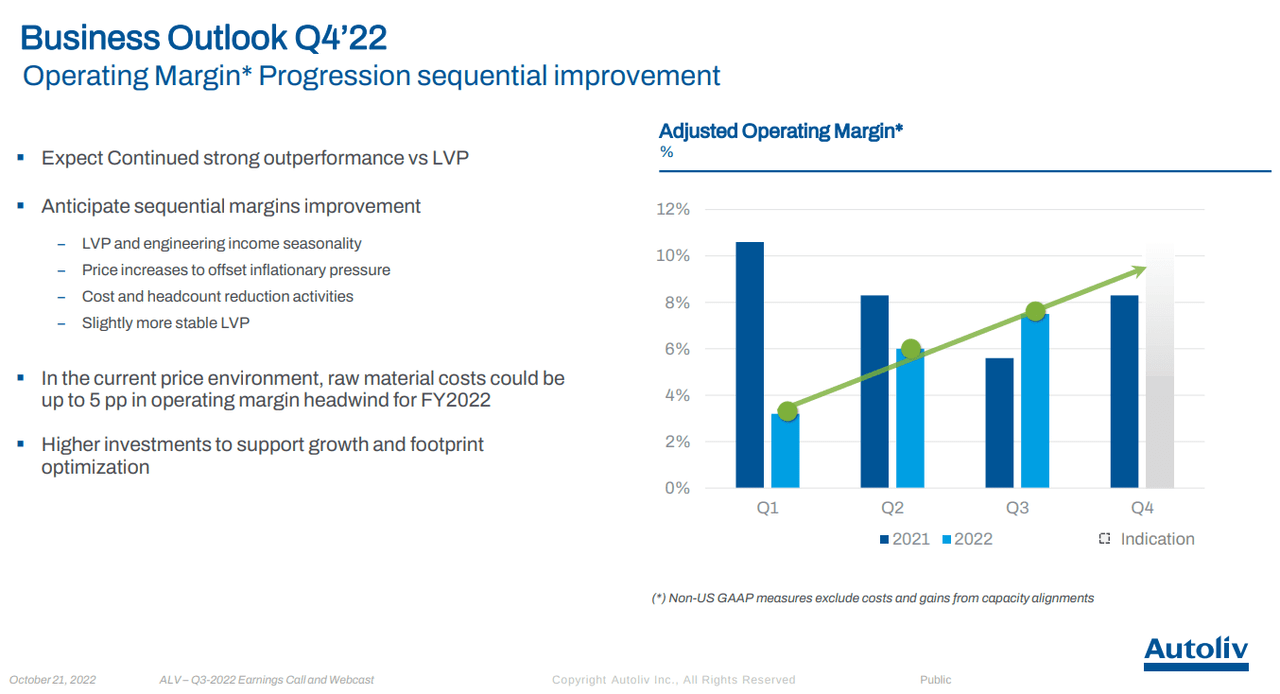

Autoliv had a strong third quarter with a 25% net sales increase and 78% increase in earnings per share. The good performance was a result of the effects of price increases and new product launches. Since the auto industry is going through a period of suppressed capacity it is likely that a couple of following quarters are advantageous to Autoliv. Furthermore, in the medium-term Autoliv will benefit from the fluctuations of auto sales, which sooner or later should raise to a higher level.

Autoliv’s business outlook. (Autoliv’s investor material)

When setting the time horizon further, the investment thesis looks more promising. According to Allied Market Research the size of the airbag market should grow at a CAGR of 5.7% until year 2030. This is nicely exemplified by the news from India where the government is proposing to require six airbags instead of two in passenger vehicles starting from October 2023. The start date was postponed by one year due to lack of production capacity of airbags. There’s still a strong underlying trend of increasing requirements for vehicle safety, and many emerging markets are several years behind of the development in the United States and European Union.

A better buy around $70

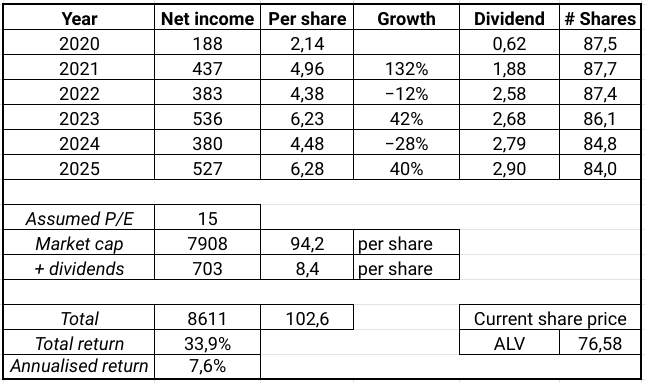

Let’s build a simplified scenario based on the facts, estimates and speculations above. Let’s assume that this year the company lands 10% below consensus analyst estimate at $6.23. Then, in 2024, the effects of a recession become apparent and the earnings decline by 28%, a little less than in 2009 and 2018. Earnings bounce back together with the economy, transition to EVs and pent up demand. All this time the company continues to raise a dividend 4% per year and buys back shares 1-1.5% per year. By 2025 an investor would achieve 7.8% annualized return. Buying the shares at $70 would increase the annualised return to 10%.

One scenario for Autoliv’s valuation. (Author.)

The assumed P/E might be a stretch, as the company is currently trading at around forward P/E of 12.3 when using the estimated EPS of $6.23 presented above. However, the company has been valued substantially higher in the past. It is difficult to benchmark against Autoliv’s competitors, ZF Friedrichshafen and Joyson Safety Systems, which are not publicly traded.

The company is again returning capital to shareholders

Autoliv had a nice dividend growth streak until the pandemic hit the world. In 2020 the company halved the dividend but it’s now on the path to exceed pre-pandemic level. The latest quarterly dividend was raised by 3% to $0.66 and translates into $2.64 annually, representing a dividend yield of approximately 3.4%. With an average EPS estimate of $6.92 for 2023, the dividend payout would be a modest 38%.

In 2022 the company bought back over 1.4 million shares with an average price of 80 dollars. This represents approximately 1.6% shares outstanding. Autoliv’s stock repurchase program continues until 2024 and authorizes the company to buy back an additional 15.6 million shares, 18% of the float. No repurchases were made in 2020 and 2021.

Autoliv’s debt position currently stands at 1.6x EBITDA above its target of 1x. Although Autoliv carries a moderate amount of debt, the maturities of its loans are approaching soon, most of them being due before 2026. The company has been able to borrow at low rates which is unlikely to continue. Autoliv’s cash position of $1.6 billion is strong and helps to pay down and roll-over the debt into the future.

Conclusion

Considering the global macro situation, outlook for the auto industry and the valuation of Autoliv, it’s most likely not an ideal situation to invest in Autoliv. A conservative investor should probably look for a larger margin of safety and carefully judge if the potential headwinds are priced into the stock. At $70 per share the expected return could be worth the risk.

Fundamentally, Autoliv is a solid company and industry leader in its categories. Having an activist investor on board ensures that the shareholder will be rewarded with dividends and buybacks. Due to the industry characteristics share price volatility can be expected and utilized to the advantage of an income investor looking to utilize the long-term safety trend in the passenger vehicle manufacturing.

Be the first to comment