Ronald Martinez/Getty Images News

AT&T Inc. (NYSE:T) is finally free of its ill-fated romance with WarnerMedia (WBD). The bean counters at AT&T never seemed to have a grasp for managing a Hollywood studio, and the broader production of creative content. But it is over, and now AT&T can provide more focused attention to its defensive core business, as well as its financial performance. This increased clarity and focus should bode well for equity performance in the second half of 2022.

There was a serious issue in combining AT&T with WarnerMedia. AT&T’s core shareholders allocated there for the capital return, and primarily in the form of a dividend. The hit-or-miss nature of movie and television production not only added volatility but also added a division that required substantial capital to create new content.

Worse yet, the development of a streaming service, like HBO Max, also required capital that might have otherwise been distributed. This not only happened to AT&T but also to Disney (DIS), which suspended its dividend around two years ago and still hasn’t reinstated it. Going forward for AT&T, the dividend is likely to be the main priority.

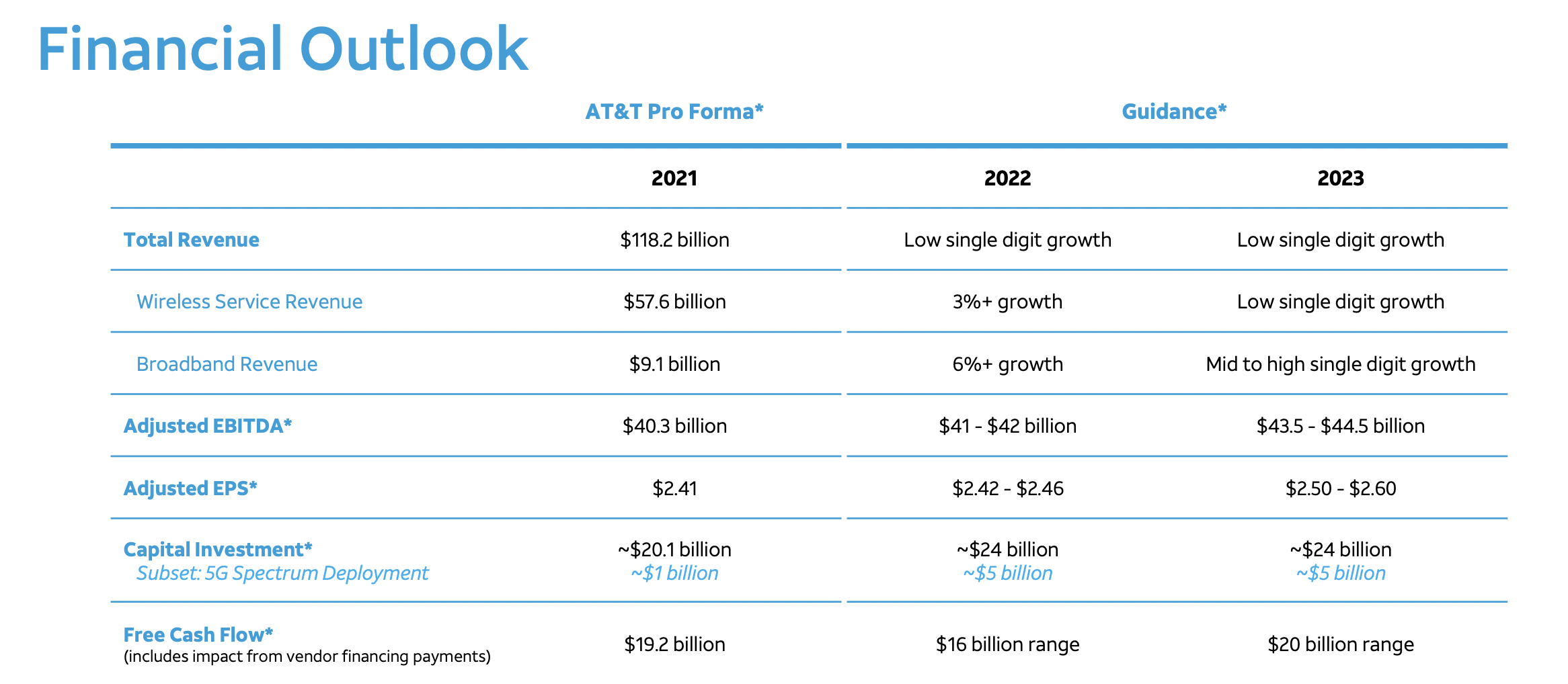

AT&T’s current guidance presumes free cash flow will increase next year and going forward due to increasing profitability, or at least EBITDA, as well as reducing CapEx. Of course, AT&T will still have significant capital expenditures to make associated with its continued 5G build-out, but the removal of costs related to creating content and a new streaming service will be gone. The company anticipates EBITDA growth of about three percent this year, and around six percent next year.

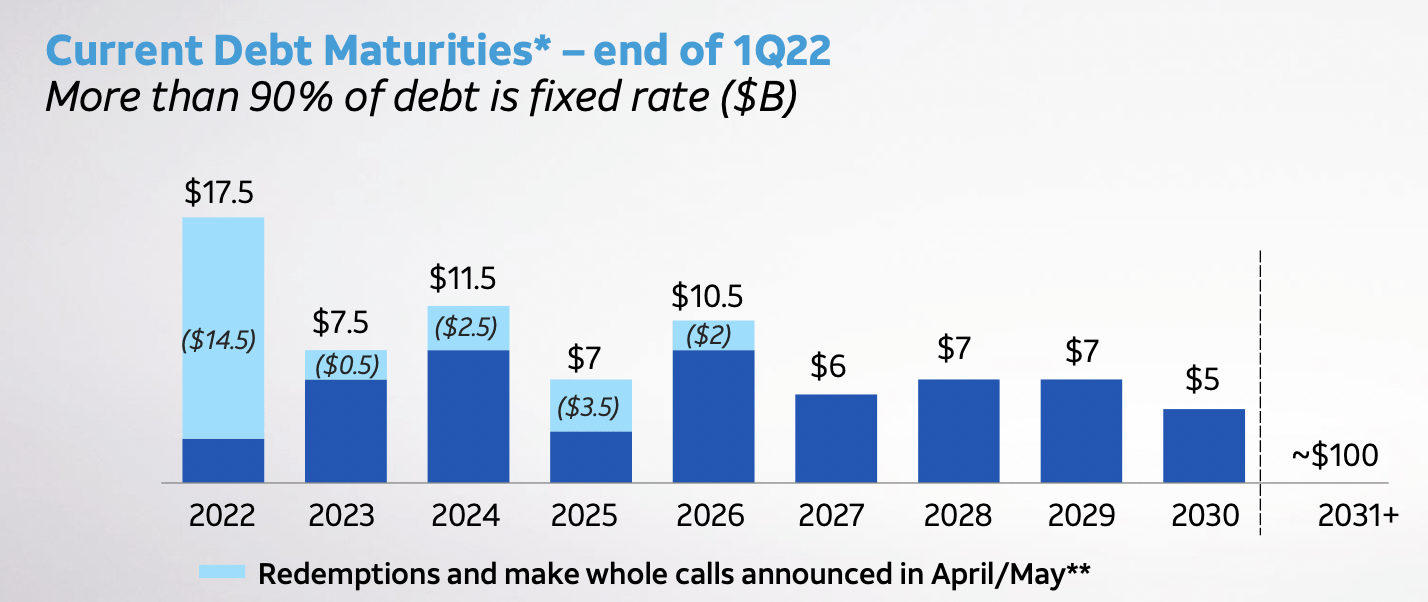

AT&T appears likely to be through much of its 5G-related expenses by 2025, but it will likely spend in excess of $60 billion between now and then. Simultaneously, AT&T plans to deleverage from its substantial debt load. So far, in 2022, AT&T initiated a tender offer for about $8.7 billion in debt. Such offerings may have been well received by the market this quarter, since bonds were plummeting in value. The reduction of its sizable debt load will help reduce interest expenses.

AT&T’s debt maturities (AT&T Q1 2022 presentation)

AT&T’s next earnings report is scheduled for July 21, at which time we will be provided with can update on their deleveraging progress. It appears probable that the company will report a $20-30 billion reduction in debt since Q1, including the effect from the above-mentioned tender offer. AT&T’s P/E of about 8 is substantially below the S&P 500 mean P/E of around 16. While further multiple contraction is possible, AT&T’s relative valuation is likely to improve as compared to the broader market. Effective deleveraging could also support possible multiple expansion, even if the broader market continues to contract.

Given the substantial divestiture that just occurred, it is unlikely that AT&T will engage in any substantial acquisitions in the next several quarters. Some smaller bolt-on deals are possible, but it is unlikely that AT&T could acquire anything for more than $10 billion and still achieve its 5G rollout and deleveraging goals. Simultaneously, smaller deals are likely to add more complexity than value, so the company seems better off attacking the debt load.

AT&T’s roughly 5% dividend is likely why most allocate into the telecom. AT&T’s dividend is also reasonably well covered, with a payout ratio of about 40% of free cash flow. If the company’s deleveraging initiative is effective, free cash flow should increase. It is probable that 40-50% of every dollar that is added to FCF will end up as a return of capital to shareholders in the form of further deleveraging, share repurchasing, and dividend increases.

AT&T’s guidance (AT&T March 11, 2022, investor day presentation)

AT&T’s poor performance over the last several years has likely placed a heavy discount onto AT&T’s valuation, and this may take a while to change. Nonetheless, the possibility of a slowing economy could have further impacts on AT&T and Verizon (VZ), whose business is at least partially fueled by retail sales at traditional stores. Both broadband and wireless sales, including upgrading, benefitted from the pandemic pull forward, and it is probable that demand for such products will be weaker in coming quarters. Similarly, some of those more recent additions may end up churning off the books

Competition between AT&T, Verizon, and T-Mobile US (TMUS) has been intense for years, and AT&T is seen as behind both those competitors in 5G development. T-Mobile is still digesting Sprint, whose customers are being moved onto T-Mobile’s network. Once T-Mobile has completed that in-house migration, it may once again pay greater attention on acquiring customers from Verizon and AT&T. Such competition could put a cap on margins, and make it difficult for any of these companies to implement price increases.

Conclusion

After years of experimenting with new businesses, AT&T is finally back to focusing on its core business. Similarly, AT&T’s shareholder base has likely seen a significant amount of turnover, with the remaining base being in it for the long haul. If AT&T can effectively reduce its debt load and increase its free cash flow, analyst estimates should improve. Simultaneously, AT&T’s defensive characteristics, including its significant dividend are attractive characteristics in this current market. AT&T likely set a bottom during Q2 of 2022, and slight multiple expansion appears reasonable in the coming quarters.

Be the first to comment