Galeanu Mihai

Atlassian (NASDAQ:TEAM) is an Australian-founded software company that has a mission to “unleash” the power of teams globally. The company’s product Jira was named a leader for agile software development teams by both the State of Agile report (2021) and Gartner in 2022. Its “product-led” growth strategy has been tremendously successful over the years and enabled continued customer growth. In Q2,FY23, Atlassian reported solid financial results as it beat top-line growth estimates. The business did miss on its GAAP earnings estimates, but beat analyst estimates on a non-GAAP basis. In addition, I discovered that despite the company being criticized as “unprofitable”, over 50% of its “expenses” are really investments into Research & Development [R&D]. Even more amazingly, when I adjust or “capitalize” these expenses the company’s operating margin actually rises to over 10%. In this post I’m going to break down the company’s recent financials as well its valuation and expense profile; let’s dive in.

Financial Breakdown

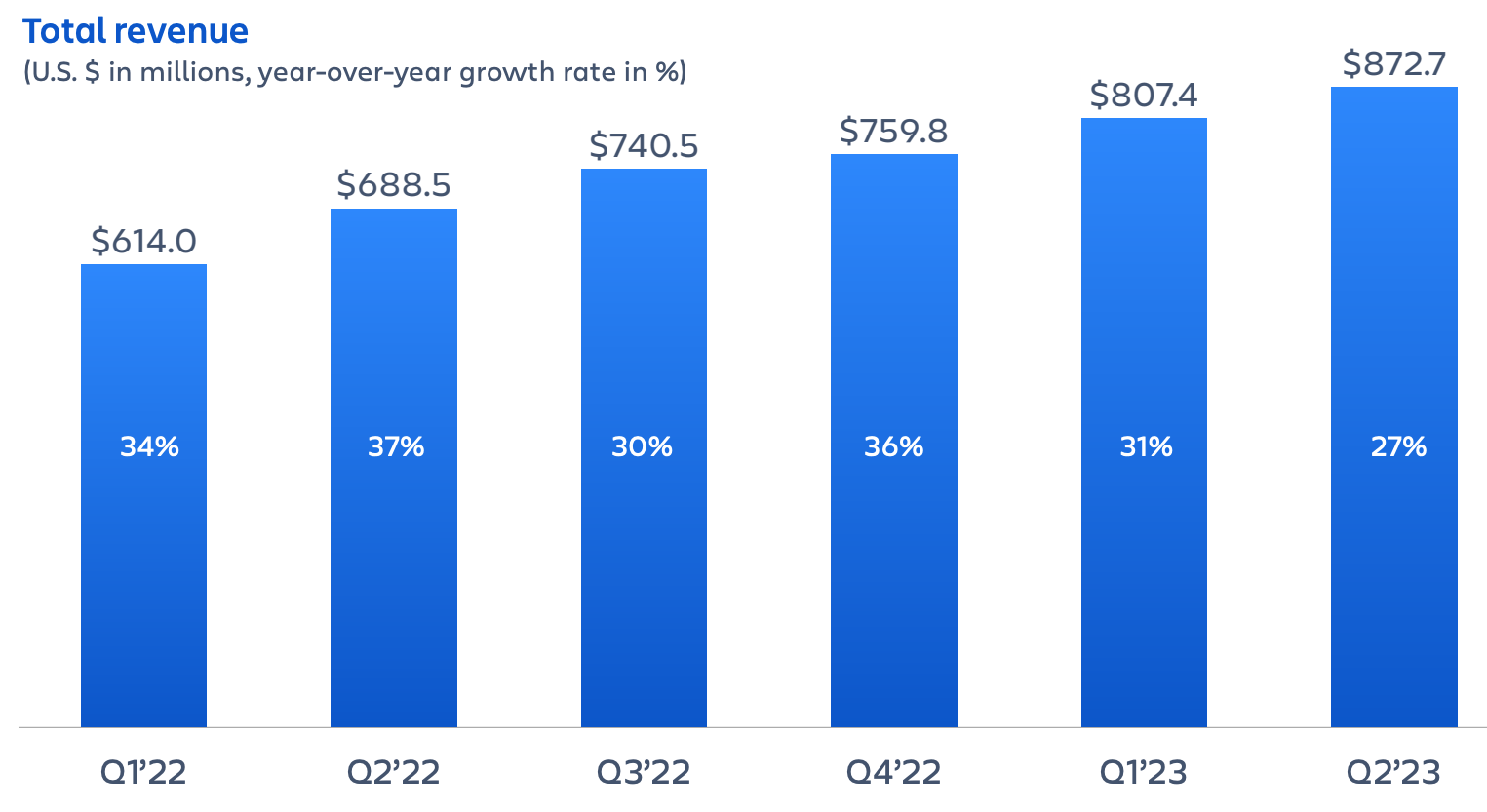

Atlassian reported strong financial results for the second quarter of the fiscal year 2023. Revenue was $873 million which increased by a rapid 27% year over year. This growth rate is slightly slower than the prior quarter’s growth rates of between 30% and 36%, which was expected due to the “recessionary” macroeconomic environment which has caused a slowdown in the number of users transitioning from freemium to paid plans. A positive is Q2, FY23 revenue still beat analyst estimates by $27.14 million.

Revenue (Q2,FY23 report)

Breaking down revenue by region, Atlassian reported strong revenue growth of 30% across EMEA and Asia Pacific regions. The Americas showed signs of weakness with 23% growth, but this wasn’t helped by a strong prior year which made the comparable unfavorable.

Revenue by Region (Atlassian)

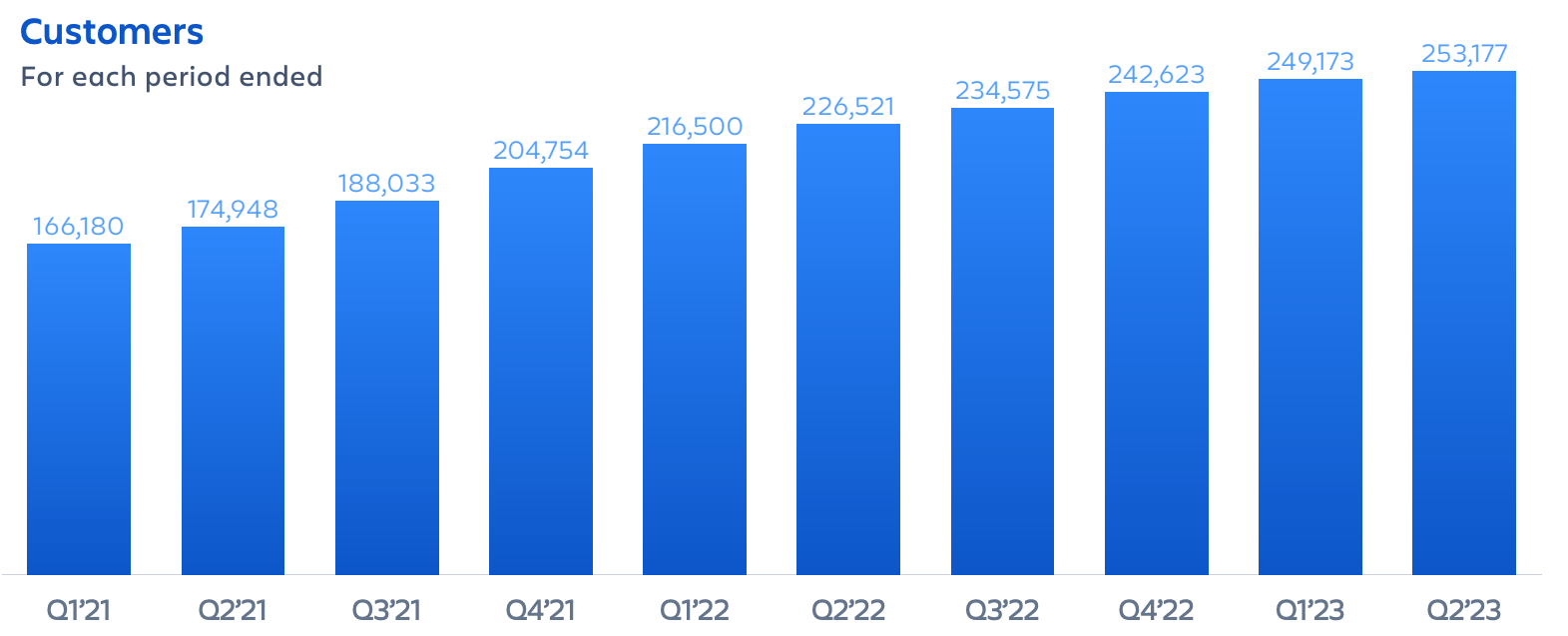

Its overall revenue growth was driven by 4.9% year-over-year customer growth to 253,177.

Customers (Q2,FY23)

On the below graphic you can see an overview of Atlassian’s product line, which includes its flagship Jira for Agile/DevOps, in addition, to an I.T service management tool and work management tools such as Confluence. The company also acquired Trello for team collaboration in 2017 and more recently acquired Chartio now Atlassian analytics for data visualization which I believe is a strong growth market, as organizations visualize their “big data”. I have discussed the business model of Atlassian in more detail in my prior post, so you can read more about it there.

Atlassian platform (Atlassian)

Digital Marketing Analysis | Brand Power

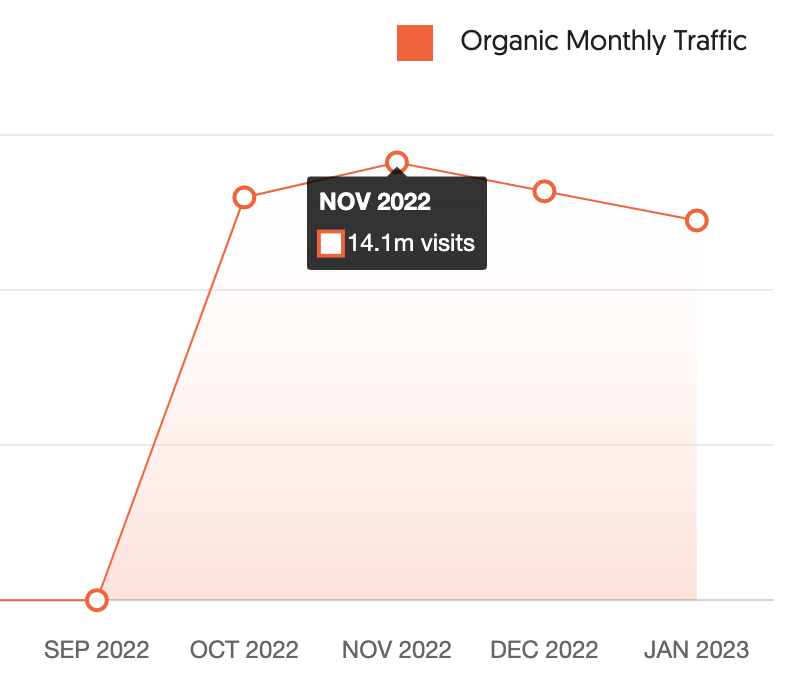

The beautiful thing about Atlassian’s business model is the company can continue to acquire “free users” during tough economic times and then convert these to paid plans at a later date. A leading indicator of interest in Atlassian’s product can be website traffic. Now although the exact google analytics data is unknown I can estimate this using various online tools. In the below chart we can see the company achieved ~14.1 million website visits in November 2022, this was up slightly from the 13 million in October 2022. Thus I am not surprised Atlassian reported a strong quarter (for Q2, FY23 or the Q4 calendar year). However, it should be that since November, website traffic has declined to 13.2 million visits in December and 12.3 million in January 2023. On a percentage basis, this works out as a ~12.9% decline since its peak in November. I expect this is mainly due to the “recessionary” environment which I will discuss in the “Risks” section. However, a positive is the drop in traffic is not substantial, e.g. 30%/40%, which would ring major alarm bells. However, this indicator is still worth watching in the future.

Website Traffic (Author analysis Ubersuggest)

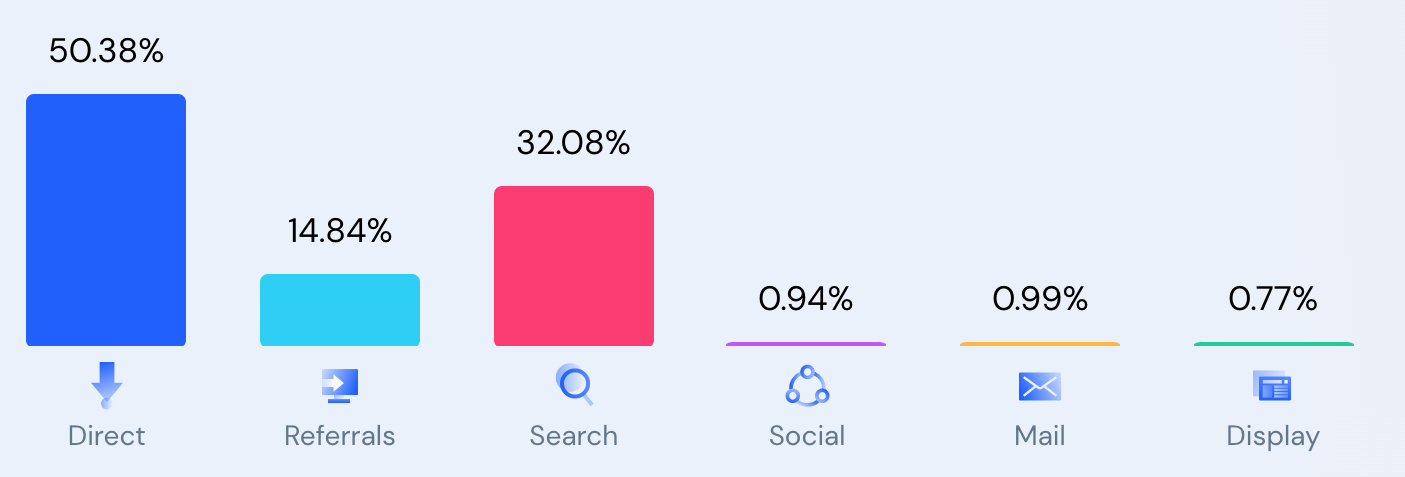

A positive for Atlassian is the company has a strong brand in the world of workplace software. To quantify this I have estimated the percentage of the company’s website traffic from sources using an online tool. In this case, we can see over 50% of the company’s website traffic is from the “direct” method. This basically means over half of Atlassian users are heading straight to Atlassian.com as opposed to entering via search engines or advertising. This is one indicator the company has a strong brand, which will result in lower customer acquisition costs than its competitors. This can also be seen as a competitive advantage against new startups, which may try to enter the space and have to spend substantial amounts on advertising just to obtain users.

Website Traffic Sources (Similarweb)

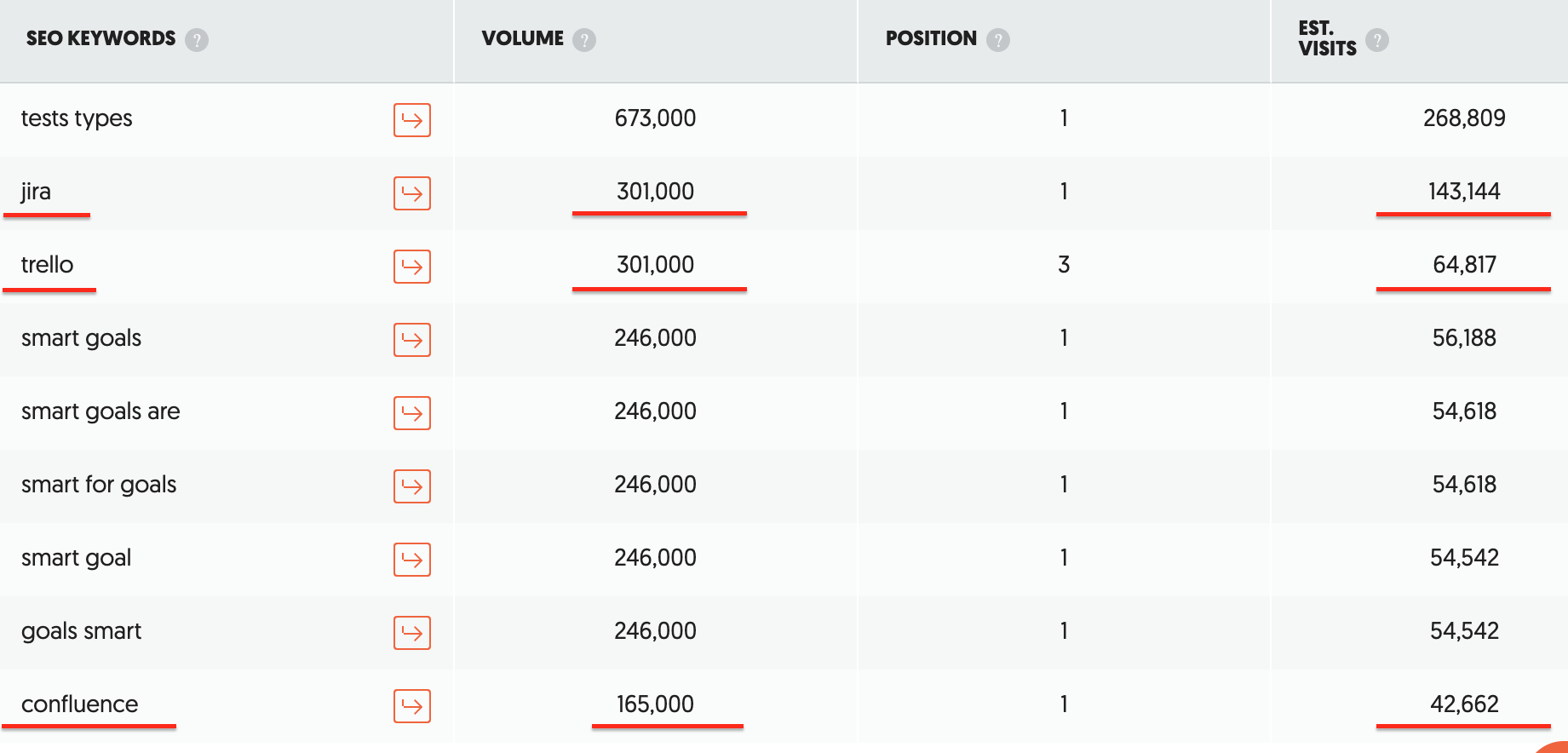

Atlassian also obtains 14.82% of its traffic from referrals and over 32% of its traffic from Search. As a Digital Marketing agency owner, I know SEO (Search Engine Optimization) rankings can be extremely valuable for a business. The reason for this is that if you can rank number one on Google consistently it can again lead to lower acquisition costs and improved marketing. In the tables below, you can see Atlassian ranks number one for over 1.28 million keywords, and its “branded keywords”, Jira, Trello, and Confluence are searched heavily. I deem this similar to “direct traffic”, which is a positive sign.

Keywords (SimilarWeb)

The final chart below you can see, Atlassian also has over 21 billion backlinks, which is the number of other websites linking to it. The Google search engine uses this as a primary indicator of where to rank a website. A new startup website, will not have this backing and thus will have to pay more to acquire customers.

Atlassian keywords (Ubersuggest)

Financials Continued

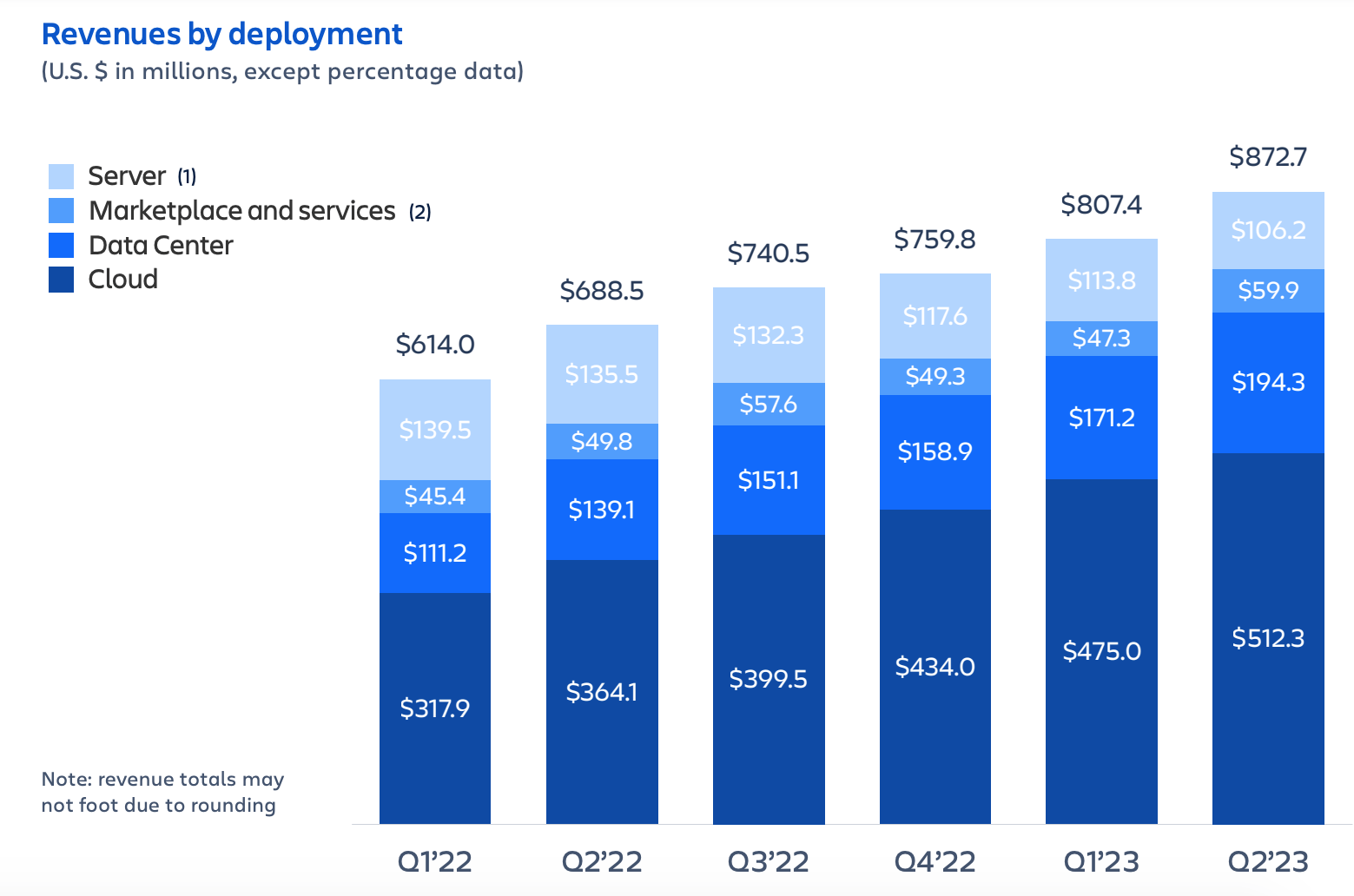

Breaking down revenue by deployment, In Q2, FY23 Atlassian generated 58.7% of its revenue from “Cloud” based deployment. This is up from the 52.9% of revenue generated in Q2,FY22. This is a positive sign as it shows the company’s strategy of moving or “migrating” users to the cloud is working. This is great for the customers as it means, they often will receive faster product updates and access to more advanced features. In addition, Atlassian will benefit, as it will then need to provide less manual people-intensive support to legacy companies that use an on-premises server for their deployment. Atlassian has announced plans to stop its support for server products by February 2024, which should give customers enough time to migrate. Overall this is a positive strategy as it will drive down Atlassian’s operating costs and the company can redirect internal resources toward cloud product improvement.

Revenue by Deployment (Q2,FY23)

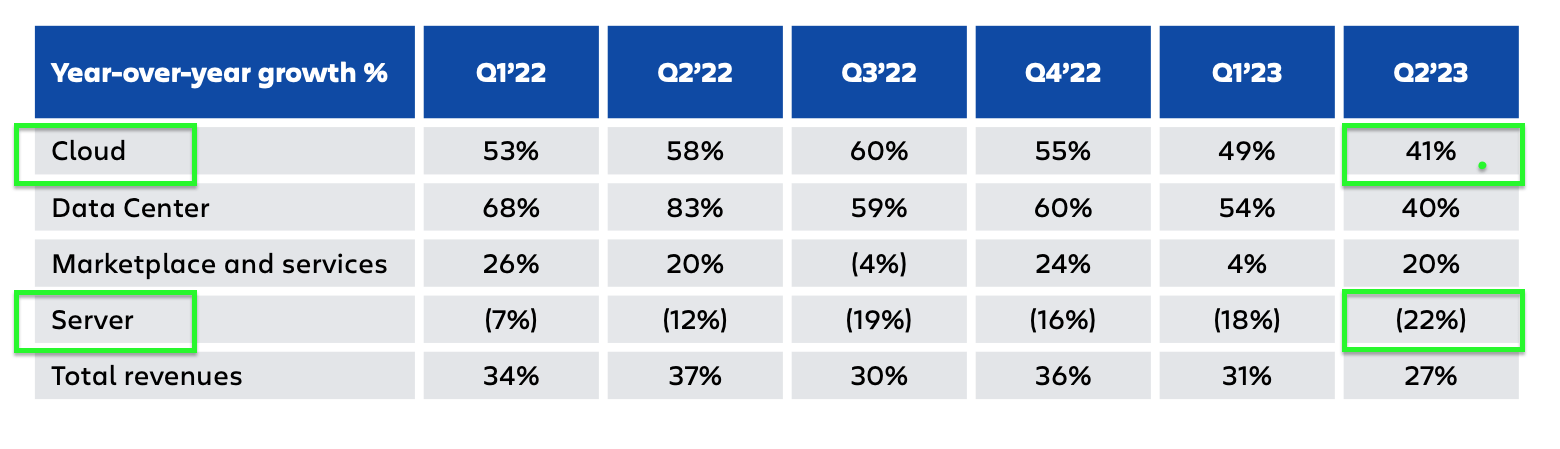

You can see a full breakdown of the positive trends below. Cloud-based deployments have skyrocketed by 41% year over year. While Server revenue has declined by 22% year over year. Without the context I laid out above, an investor may believe this is negative when it’s actually a positive trend.

Deployments (Q2FY23)

Margins and Expenses

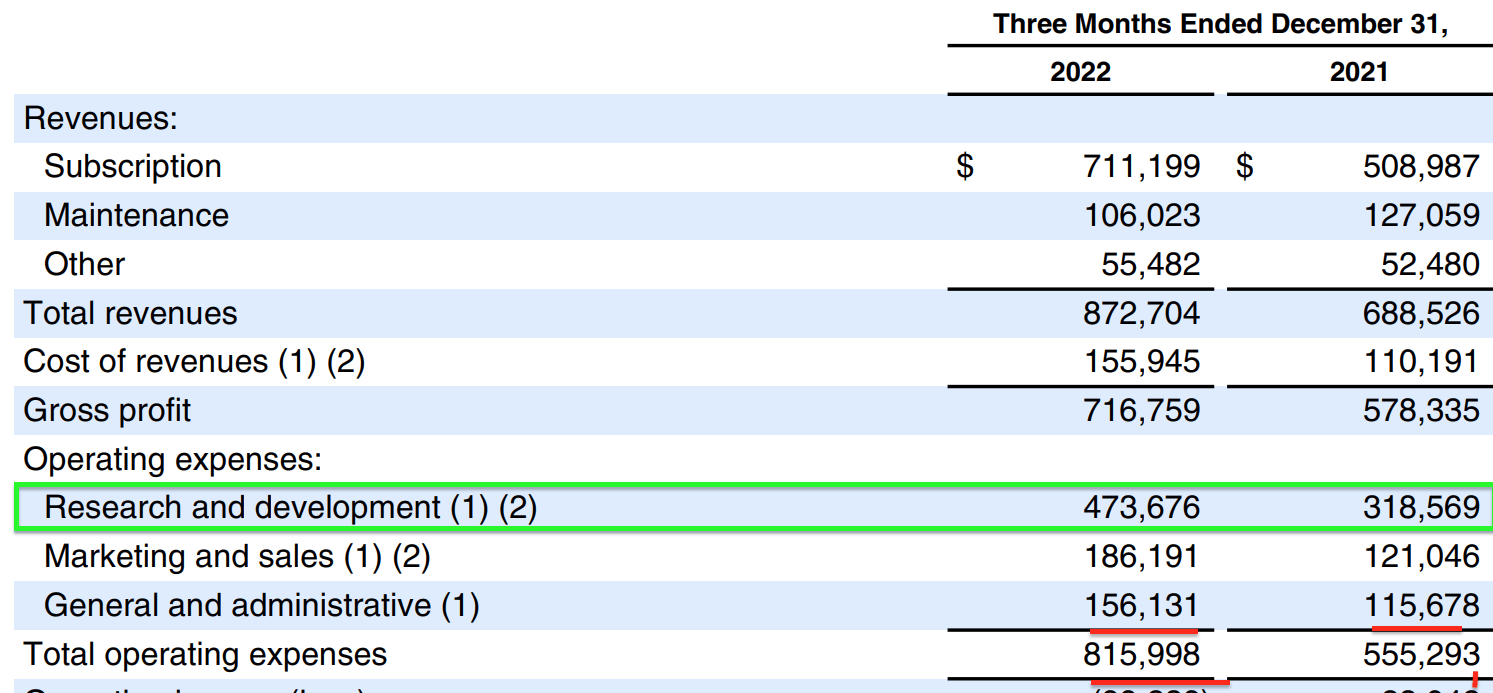

Atlassian reported a super high gross margin of 82%, which declined by 2% year over year. Earnings per share [EPS] was negative $0.80, which missed analyst estimates by negative $0.34. A positive is on a Non-GAAP basis EPS was $0.45, which beat analyst estimates by $0.14.

Atlassian’s main profitability challenges came from an eye-watering 47% increase in GAAP operating expenses. This may seem atrocious at first glance, but when I “pop the hood” on the income statement, I see the majority (58%) of its expenses were driven by Research & Development costs, which increased by 48.7% year over year. Overall I don’t deem this to be a negative as I believe technology companies must continually invest in their product to stay ahead of competitors. Many studies also indicate that companies that invest in R&D tend to create more shareholder value long term.

Expenses (Q2,FY23)

The second major expense for Atlassian is Marketing & Sales, which made up 22.8% of operating expenses and increased by 53.8% year over year. It was interesting to see the company accelerate this expense during a tepid macroeconomic environment. I would personally like to see this decline as a portion of operating expenses moving forward at least for the next year. Overall Marketing and Sales expenses aren’t “bad” assuming an ROI is obtained, but this is harder during a recessionary environment.

The final expense line item is general and administrative [G&A] expenses which contributed to 19% of total expenses to $156 million, up slightly from 20% in the prior year. As Atlassian operates a software company theoretically the business can execute high operating leverage, which should drive margin increase over time. In Atlassian’s Q2,FY23 earnings call, management announced plans to “decelerate” operating expense growth in the second half of 2023, after previously announcing plans to reduce “discretionary” spending and “moderate” headcount growth. I believe this is a positive sign overall for profitability and I will discuss this in more detail in my “valuation and forecasts” section next.

Before diving into that, it should be noted Atlassian has a solid balance sheet with $1.6 billion in cash and cash equivalents, as well as $36 million in marketable securities. Its debt also looks to be manageable with a “term loan” facility equating to $999.5 million, which is “long-term debt” and thus manageable.

Atlassian (Balance Sheet)

Valuation and Forecasts

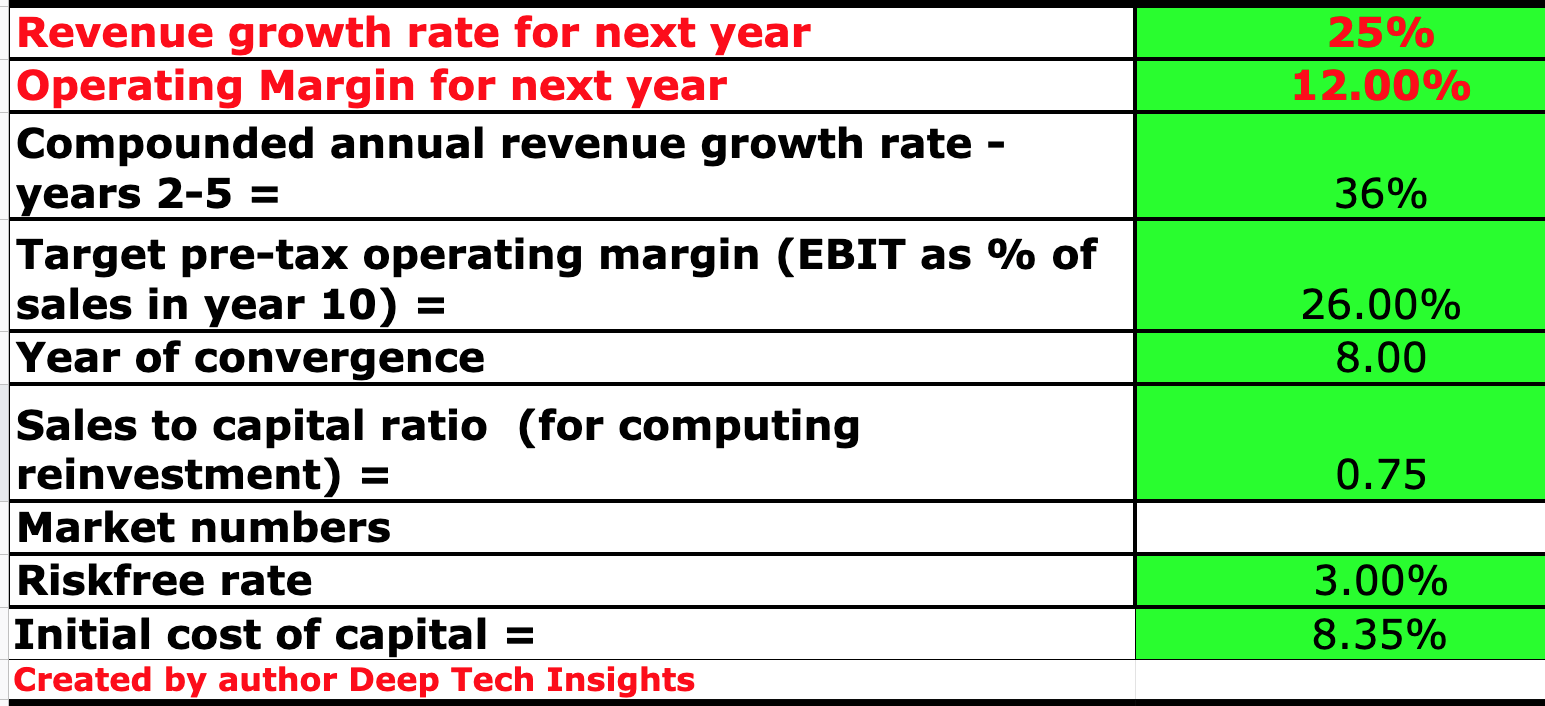

In order to value Atlassian, I have plugged its latest financial data into my discounted cash flow model, with my forecasts for growth. In this case, I have forecast 25% revenue growth for “next year”, which in my model refers to the calendar year 2023. This is in line with management’s guidance of 25%, for the fiscal year 2023, which I have expanded to include the calendar year. Breaking this revenue down by type, Cloud revenue is forecasted to grow by between 35% and 40% year over year. With 10 points of this growth being driven by the aforementioned cloud migrations. In years 2 to 5, I have forecast a greater 36% overall revenue growth per year for the entire business. I expect this to be driven by improving economic conditions, which should result in a greater number of customers converting from free to paid plans. In the recent quarter, Atlassan’s management noted it had seen tepid demand among its SMB customers, with fewer moving to paid tiers. I expect this dynamic to improve post-2023. A positive for Atlassian is in the past few quarters, management has reported minimal issues with churn and upsell for its premium and enterprise customers. This makes complete sense as often large organizations can weather an economic storm much better than smaller businesses.

Atlassian stock valuation model 1 (created by author Deep Tech Insights)

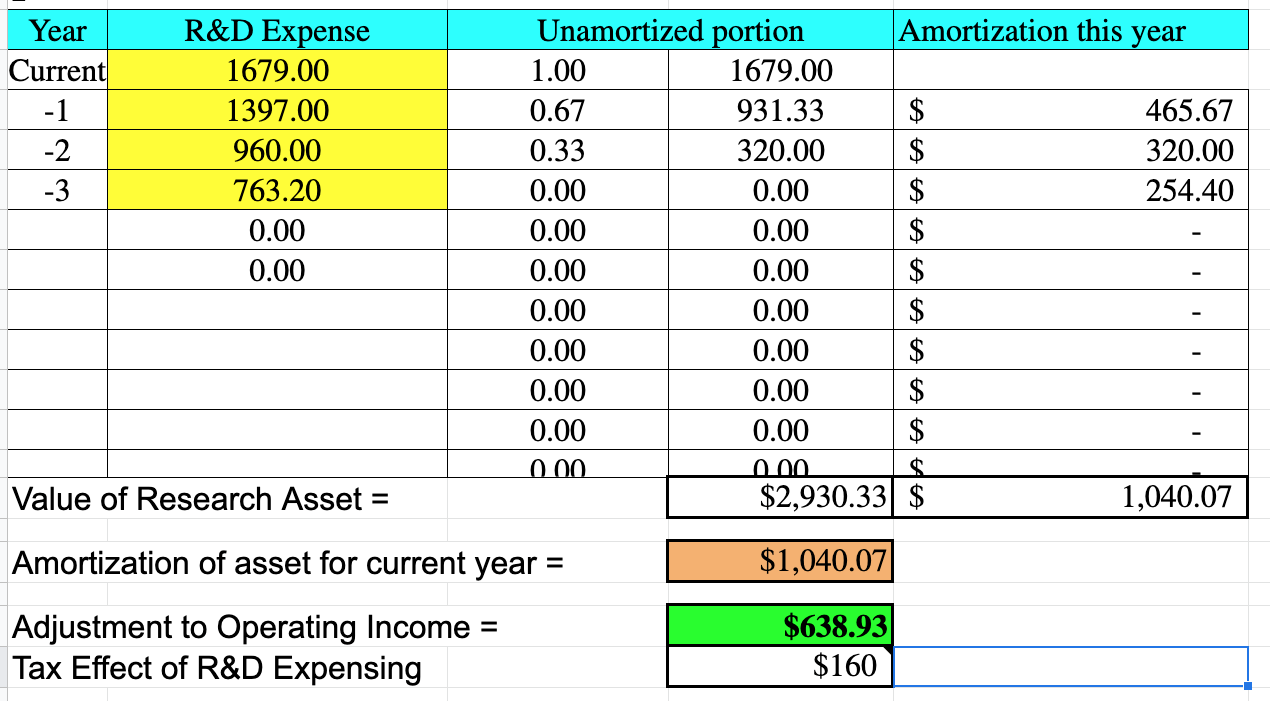

As mentioned prior Atlassian invests a huge amount (~58%) of its expenses into Research & Development. This is cited as an “operating cost”, but to improve the accuracy of the model I have “capitalized” this expense, which has boosted net income slightly and adjusted equity figures through “amortization”, (annual balance sheet write down). I will not go deep into explaining this process, as it’s beyond the scope of this post, but you can read more online. You can see from a screenshot of my model below, I have capitalized R&D expenses over a 3-year period, which has resulted in an adjustment or “boost” in operating income by $638.93 million.

R&D Expenses Capitalization (Author valuation model )

The bottom line is with this accounting adjustment, Atlassian actually posts a positive 10.76% operating margin this year up from negative 10% in the trailing 12 months. Therefore the company can actually be deemed to be “profitable” on an adjusted basis. For “next year” I have estimated this margin to grow slightly more to 12%. I expect this to be driven by the aforementioned plans for the company to reduce its “discretionary” expenses in the second half of 2023. Over the next 8 years, I have been slightly more optimistic and forecast a 26% operating margin. This figure is based on the fact that the average operating margin for a software company is 21.8% (according to industry datasheets). I believe Atlassian is an “above average” company with a strong brand and leadership position (discussed prior), high retention, and a solid list of enterprise customers with plenty of room for upsell and improved cost efficiencies (from moving to a pure cloud model). Thus I have forecast a higher margin than the average for the industry long term.

Atlassian stock valuation 2 (created by author Deep Tech Insights)

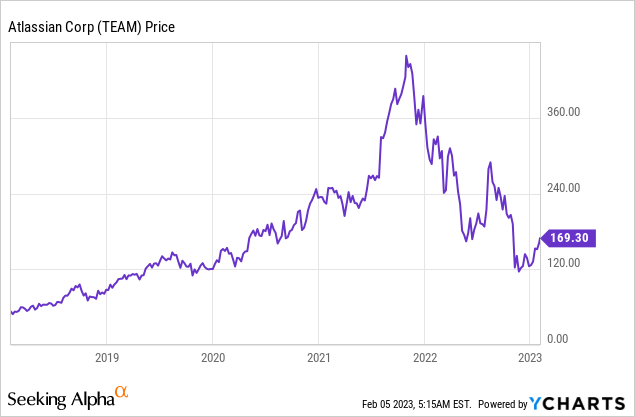

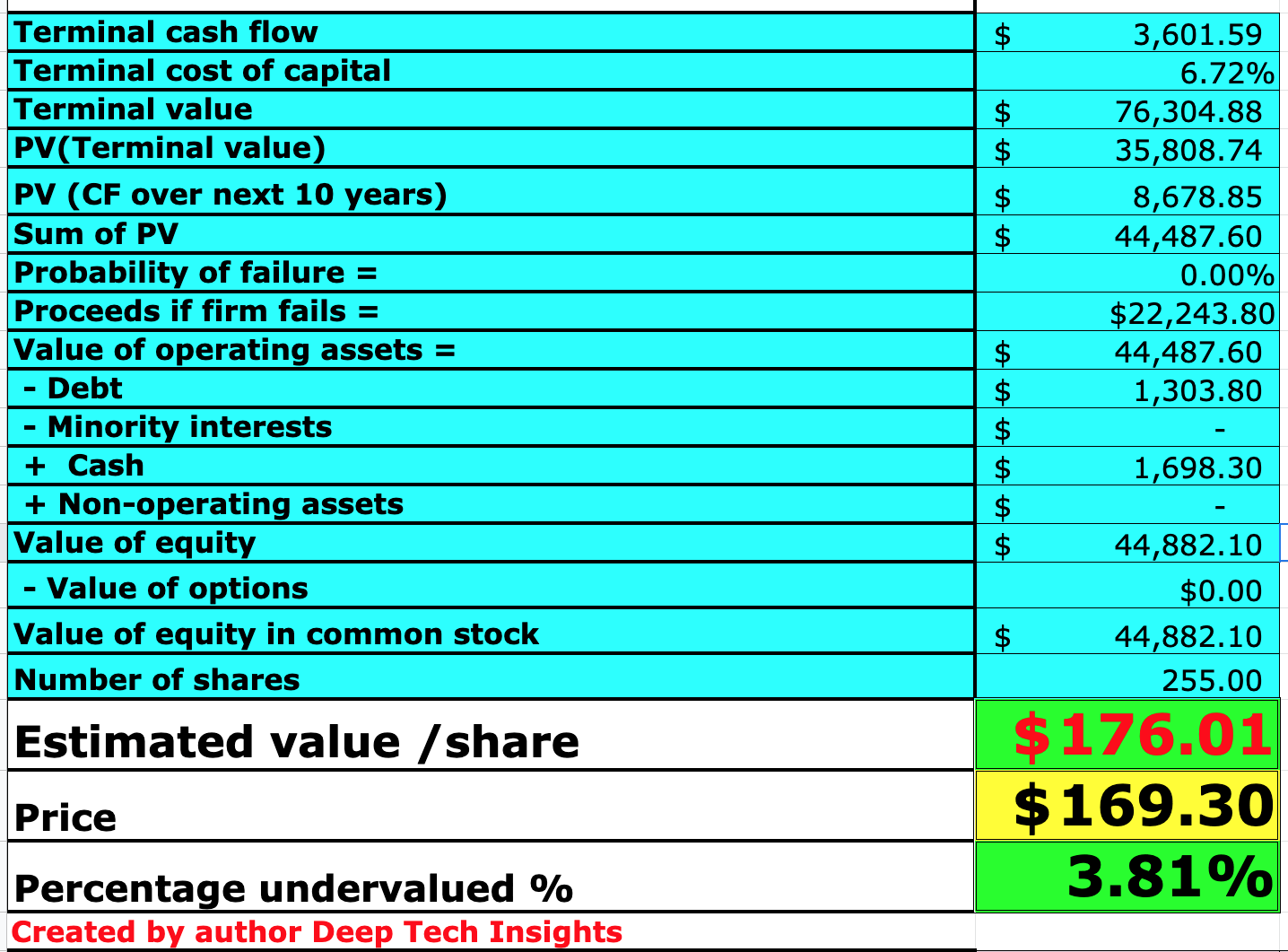

Given these factors I get a fair value of $176/share, the stock is currently trading at $169.3 per share at the time of writing and thus is ~3.81% undervalued. Due to the quality of the company I deem this to be “fair value”.

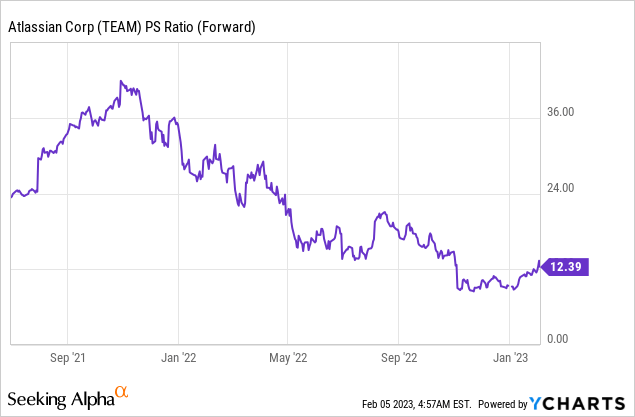

As an extra data point, Atlassian trades at a price-to-sales ratio = 13.56x, which is 47% cheaper than its 5-year average.

Risks

Lower Conversions/Recession

Analysts management has already started to see signs of lower free-to-paid conversion rates for its customers, with particular weakness in the SMB market. I forecast this trend to continue into 2023 as many economists have forecast a recession for the year. The good news is Atlassian still has a strong brand and can continue to “collect” free users, which will be poised to convert to paid as economic conditions improve.

Final Thoughts

Atlassian is a world-class software company that has continued to produce strong revenue growth despite a tough economic backdrop. Its “unprofitable” nature is not so bad when we see the majority of its expenses are related to R&D investments, which when adjusted boosted profitability to the green. Its stock is trading slightly undervalued intrinsically at the time of writing. This doesn’t offer a major “discount” compared to many other technology stocks in the current environment (see my post Google). However, one cannot argue with the quality and potential of this SaaS company to continue to improve its product and expand its margins.

Be the first to comment