SHansche

Atlas Corp. (NYSE:ATCO) has entered into an agreement to be acquired by the Poseidon Consortium, led by former Chairman David Sokol. The definitive agreement came after an initial offer was raised ~7% to $15.50. The bump came on Nov 1, 2022, with the initial bid for $14.45 cash per share on Aug 5, 2022. Fairfax Financial (OTCPK:FRFHF), the Washington Family, and David L. Sokol own/control nearly 70% of the Atlas shares already and are rolling these over into the deal.

The spread is still meager in absolute terms. But there is 4.4% upside from $14.84 to the buyout offer. The meeting to get shareholders to vote for the deal has been set for February 24.

The company also pays a $0.125 quarterly dividend. My understanding is that shareholders get a prorated portion of that quarterly dividend. This prevents “unlucky” timing, where the deal closes before the record date. The company set a record date and payment date for its upcoming dividends as follows:

ATCO dividend dates (ATCO dividend PR)

If the deal closes, the upside is 5.28% to the deal price and includes the dividend. What’s so great about that is that the return can be realized in less than a month. I expect it to close soon after shareholder approval.

The merger is somewhat contentious. Some Atlas Corp. shareholders are arguing the company is being taken private too cheaply. There will be a vote of the minority shareholders, and if a majority of that minority votes against it, the merger is off.

I rechecked a shareholder list put together by Morningstar. The buying shareholders list includes a lot of hedge funds with strong reputations. Including hedge funds with a history of fighting hard to improve deals when companies are being taken private, like Pentwater Capital. However, it also includes several funds I’d qualify as quant funds. What stood out to me this time is the number of arb funds in the deal. That could be a function of the spread that has improved as time has progressed. This increases the IRR of the deal, making it more attractive to arbs without the deal being improved. The latter categories (quant and arbs) are doubtful to vote against the deal.

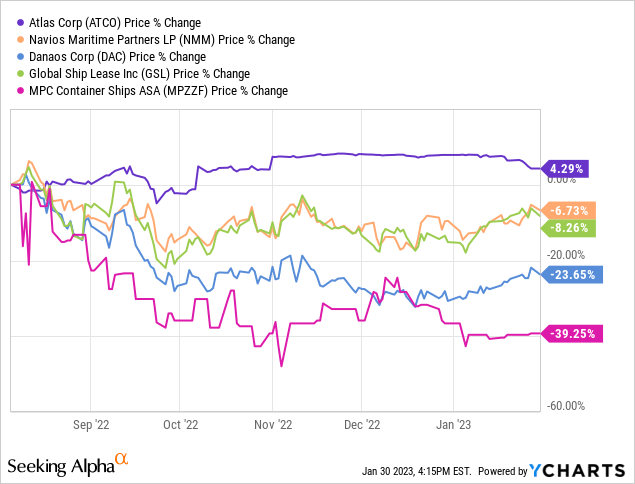

ATCO traded at around $11 when the initial offer was made. ATCO is mostly a container company. This segment makes up 2/3rd of earnings last quarter. Another important segment is APR energy, which operates a mobile fleet of gas turbines. It is good for ~1/3rd of earnings in the last quarter. I pulled up several container peers, and these have been hurt fairly bad since the deal has been announced.

Interestingly, since my last article on this deal, I’d say the container peers mitigated some of the losses while ATCO actually declined.

This does suggest the break price could be in the $8 – $10 range. A bit worse than you’d think by just looking at the pre-deal price. In my previous article, I talked about selling it above $15.33.

Because the spread widened quite a bit, my position is different now. This trade idea will likely have been resolved 30-40 days from now. At the current price and given the expected timeline ahead, I think it is an attractive enough merger. It is not a top position, but I think it adds value to my portfolio. If it fails, Atlas Corp. is perhaps not the worst company to get stuck with for some time.

David Sokol is an investor with a value investing background, and Fairfax can be characterized as a firm with a value investing ethos. The forward P/E of around 8x and the buyout team suggest substantial value here for Atlas Corp.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment