Ulet Ifansasti

The share price of pharmaceutical major AstraZeneca (NASDAQ:AZN) was having a hard time until recently. It lost 10% of its value in just a little over a month into 2023. It was not surprising, though. There was a rotation to beaten-down stocks and AZN is anything but beaten down. Over the past year, it is still up by 17.5% and over the last five years, it has more than doubled investors’ money.

But recently, it proved itself once again. There was a discrete jump in its share price when it released its Q4 2022 and full-year 2022 results and has now gained 7.1% since. In other words, it has almost made up for the loss in value seen up to the start of February. Clearly, the cancer specialist has shown once again that it’s a good investment.

But let’s not jump the gun. Here, I take a closer look at its financials to assess if all is indeed going great for the company. This article also looks at its dividend yield and, importantly, its market multiples to see how much upside there is for the stock.

Double-digit growth in 2022

The company doesn’t really need any introduction. It became a household name when in collaboration with the University of Oxford it developed one of the first COVID-19 vaccines back in 2020. But AstraZeneca’s strength has always been in its cancer treatments. And they continue to drive its progress forward.

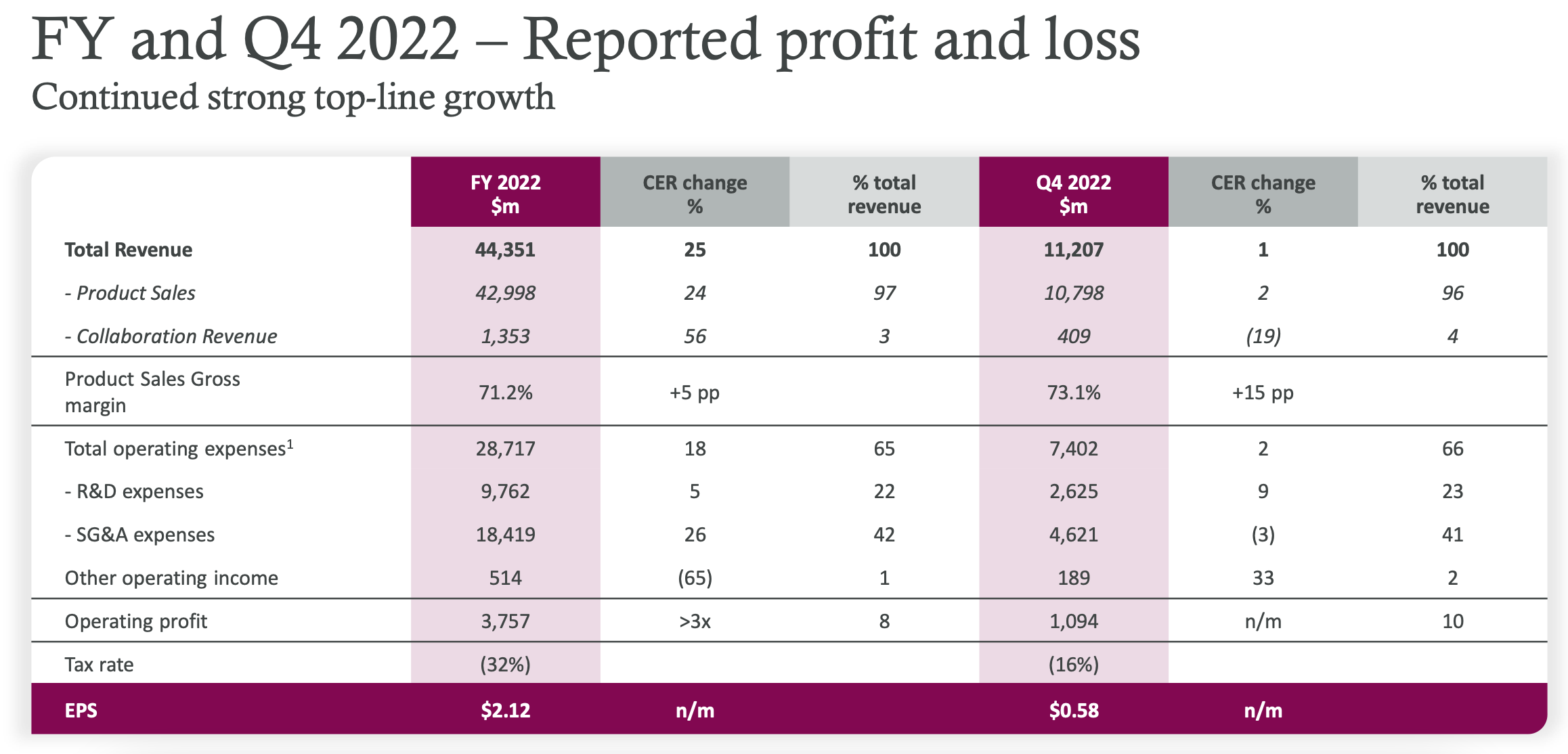

For the financial year 2022, the company saw 19% year-on-year (YoY) revenue growth at market exchange rates and an even higher 25% growth at constant exchange rates. Oncology and biopharmaceuticals, its two biggest segments with a share of 33% and 21% in total revenue respectively, showed strong growth of 13% each.

While this is the highest growth seen among all the segments, at first look, it’s curious because it’s clearly lower than overall growth. Turns out though that there’s a technical reason for this. As it happens, the rare diseases segment has seen just 4% growth because its tumour treatment Koselugo revenues have been added to 2021 revenues as well for comparison. In actual fact, rare disease revenue is up by 129%, which is reflected in total revenue growth.

Source: AstraZeneca

AstraZeneca’s fourth quarter (Q4 2022) revenue has fallen by 7%, but this is not a cause for alarm either, since this is on account of a decline in its COVID-19 vaccine sales. It anything, this is good news, since it reflects that we are likely to put the pandemic behind us now. The company’s Q4 revenue growth ex-Vaxzevria, as it is now called, is a healthy 17%.

Its operating profit has seen a huge growth of over 3x in both actual exchange rates and at constant currency, following from its strong revenue growth in 2022. Its earnings per share [EPS] have also shown strong growth, with an increase in the Core EPS of 26% to $6.66 in 2022. It is over 3x the reported EPS, because of costs related to the inclusion of rare diseases Alexion, which AstraZeneca acquired in 2021 as also amortisation, impairment and restructuring charges. There’s nothing to flag in its balance sheet or cash flow statement either.

Tempered progress expected in 2023

The company’s guidance is also positive, as it shows continued expectations of growth. It does however expect revenue growth to slow down to a “low-to-mid single-digit percentage” compared to last year’s guidance for 2022 of a “high teens percentage”. Interestingly though, at least part of it is driven by the company’s exchange rate expectations. In his statement, the company’s CEO Pascal Soriot says that they expect “double-digit revenue growth at CER”. The company reports its figures in US dollars, for which exchange rates so far in 2023 indicate an adverse impact in results at market exchange rates in 2023. Also, there will be a negative impact from a continued the fall in COVID-19 treatment sales.

AstraZeneca

Similarly, it expects Core EPS growth to slow down to a “high single-digit to low double-digit percentage” compared to last year’s guidance of a “mid-to-high twenties percentage.”

More upside to AZN

Analysts however are more optimistic for AstraZeneca’s 2023 EPS than the company, with consensus estimates at $4.59, which is more than double the reported number seen this year. With this figure, it has a forward price-to-earnings (P/E) ratio of 14.7x. This isn’t high by any stretch. Over the past decade, the company has had a median P/E of 39x.

Admittedly, this refers to the twelve months trailing [TTM] P/E, but it does offer some comparison. Also, in the same vein, its P/E after the 2022 earnings release is at 32.5x as per my calculations, which is also lower than its average P/E. To trade at its historical average, the stock still needs to rise by almost 21%, which suggests the kind of upside there is to it.

Consider the dividends

It also pays a dividend, which is something to consider. Don’t let its present dividend yield of 2.1% fool you, the company’s stock price has been rising over time. For anyone who bought the stock five years ago, the present yield would be over 8%. There’s something to be said for its dividend history too. It has consecutively paid dividends for the last, wait for this, 23 years.

What next?

Frankly, I am at a loss to find anything not to like anything about AstraZeneca. And I have not even touched on its pipeline of treatments underway, which includes a spate of approvals for its upcoming cancer treatments and for conditions that include asthma and other respiratory infections as well as heart failure.

There could be a short-term weakness in its share price if investor interest stays firmly focused on consumer stocks, as it has recently. But that hardly takes away from AZN’s long-term potential. It has proven its mettle as a stock over time, and its dividends are worth considering too. I’d buy it.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment