FroggyFrogg

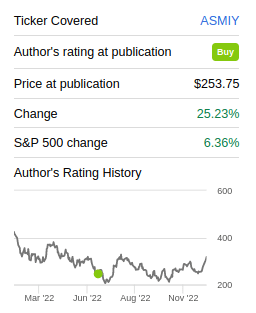

ASM International (OTCQX:ASMIY) is one of our favorite companies in the semiconductor manufacturing equipment sector. It is one of the companies helping keep Moore’s Law alive, and as such it has been growing rapidly. We started coverage with a ‘Buy’ rating, and since then shares have significantly outperformed the market. Unfortunately, the company is now facing increased headwinds that could lead to a slowdown in growth, and the valuation is less attractive. As a result we are now updating our rating to ‘Hold’ from ‘Buy’ previously.

Seeking Alpha

In our previous article we covered the company in more detail, so we recommend readers not familiar with it to go back to that article to get an idea of what the company does. As a quick reminder, ASM is focused on enabling deposition technologies, and it is a leader in the ALD market, which is expected to grow by a CAGR of 16%-20% from 2020 to 2025. The company is also expanding its position in the Epi market which is expected to have a CAGR of 13%-18% from 2020 to 2025. The company also recently acquired LPE to enter the high-growth silicon carbide Epi market.

Increasing Headwinds

The company delivered solid Q3 2022 results, posting record-high revenue of €610 million. Its gross margin in the quarter was 48.1% and operating margin was 26.2%. The company ended the quarter with a solid cash position of €670 million and no debt.

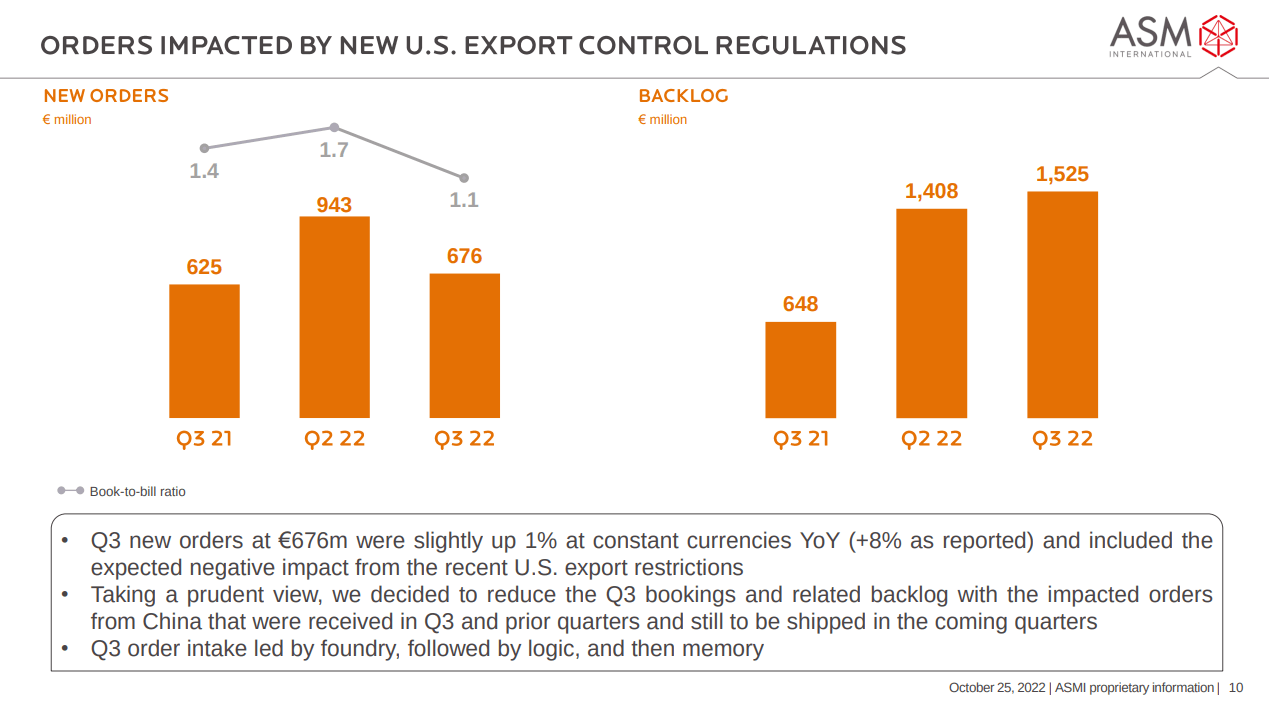

Nevertheless, Q3 new orders were €676 million, down considerably compared to the €943 million in Q2. Orders were adjusted to reflect the expected negative impact of the recent US export restrictions to China. Excluding the reduction of impacted orders from China, the decrease in the company’s Q3 orders compared to Q2 would have been much more moderate. Another increasing headwind is the wafer fabrication equipment market being forecasted to be down in 2023, as the semiconductor end-market is slowing down with weaker global economic growth.

ASM International Investor Presentation

Guidance

The company guided sales for Q4 to be between €600 million and 630 million, which includes a negative impact from the new US export regulations. The revenue guidance includes the revenue contribution from the LPE acquisition which closed on October 3, 2022. The company still expects to finish the year with an elevated backlog.

Valuation

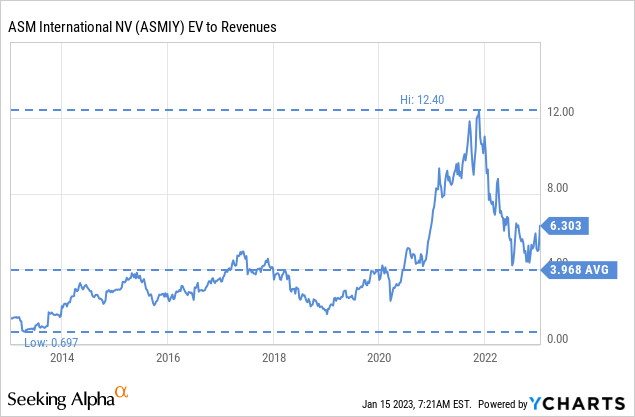

We believe the combination of increased headwinds with a more expensive valuation means the shares are no longer a ‘Buy’, but not expensive enough to rate them a ‘Sell’ either, so we are adjusting our rating to ‘Hold’. The current EV/Revenues multiple is around 6.3x, more than 50% higher than the ten year average.

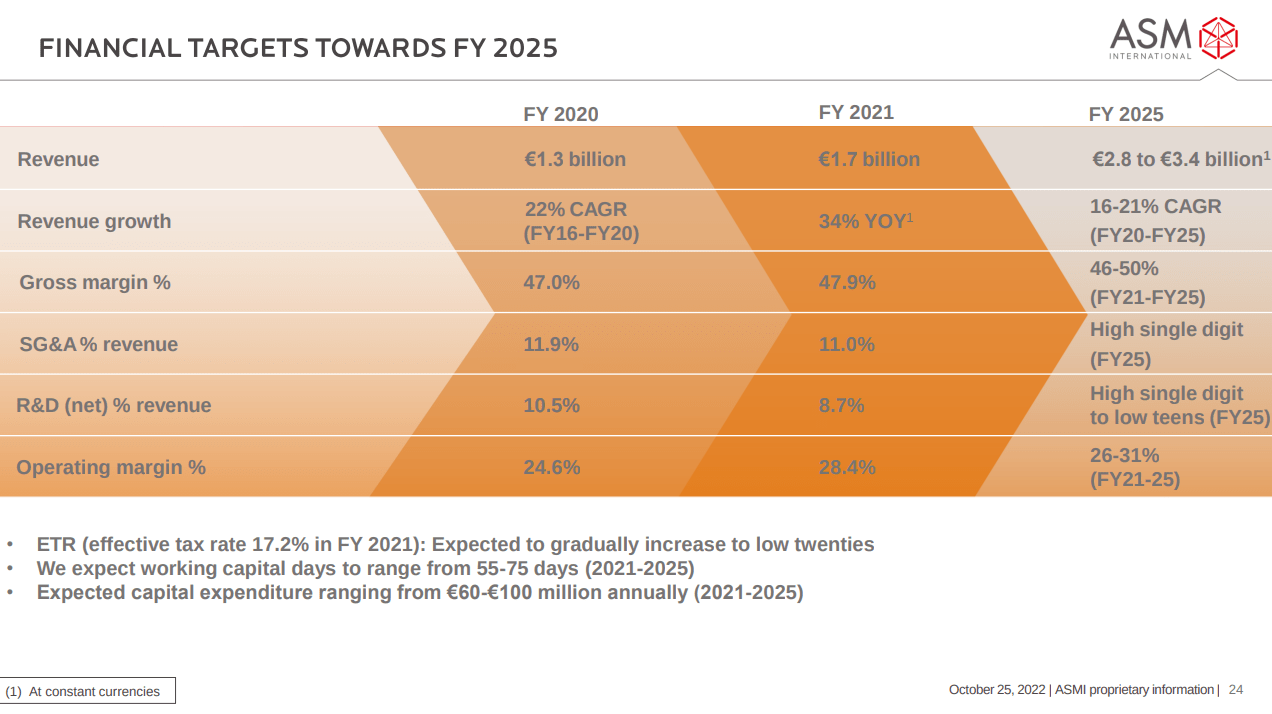

The company has an earnings model that targets fiscal year 2025 revenue between €2.8 billion and €3.4 billion, and an operating margin between 26% and 31%.

ASM International Investor Presentation

Using this model and some other assumptions we estimate a net present value of the future earnings stream of ~$254, when using a 10% discount rate. Given that shares are currently trading at ~$317, we believe they are slightly overvalued. At current levels we believe shares are priced to deliver returns in the high single digits for long-term investors.

| EPS | Discounted @ 10% | |

| FY 23E | 10.70 | 9.73 |

| FY 24E | 14.05 | 8.84 |

| FY 25E | 17.39 | 8.04 |

| FY 26E | 18.96 | 9.59 |

| FY 27E | 20.66 | 10.80 |

| FY 28E | 22.52 | 10.70 |

| FY 29E | 24.55 | 10.60 |

| FY 30E | 26.76 | 10.51 |

| FY 31E | 29.16 | 10.41 |

| FY 32E | 31.79 | 10.32 |

| FY 33E | 34.65 | 10.22 |

| Terminal Value @ 3% terminal growth | 521.92 | 166.30 |

| NPV | $276.06 |

Risks

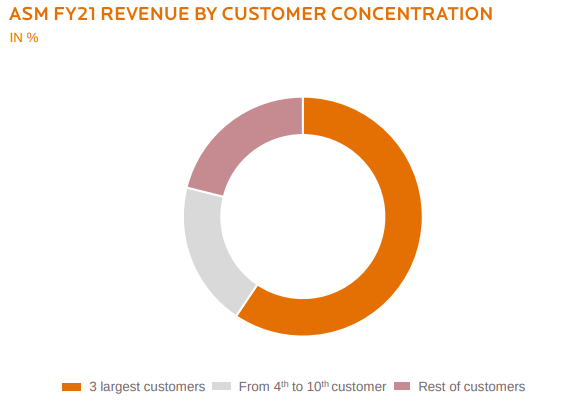

There are a few important risks to consider with respect to ASM International. One is that the valuation already assumes a good amount of growth in the next few years. There is also significant customer concentration. The 10 largest customers accounted for about 79% of revenue in FY 2021, with the 3 largest representing approximately 59%. The three largest customers are probably Intel (INTC), TSMC (TSM), and Samsung (OTCPK:SSNLF).

ASM International Investor Presentation

There is also an important risk that a large semiconductor equipment manufacturer could be attracted to the ALD market. Currently ASM is the market share leader in ALD and has a solid position in Epi, but companies like Lam Research (LRCX) or Applied Materials (AMAT) could decide they want to challenge ASM International.

Conclusion

We continue to like ASM International, but have become less optimistic about their short/medium term prospects. Increasing headwinds could lead to a slowdown in growth and make it difficult for the company to meet market expectations. At the same time, shares have gone up in price, making the valuation less attractive. We are therefore updating our rating from ‘Buy’ to ‘Hold’ as we believe it would be wise for investors to wait for a better entry point before buying shares.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment