ArtistGNDphotography

What Are They Selling

Ascent Solar Technologies (NASDAQ:ASTI) is a leading provider of CIGS solar technology. They offer cutting edge PV technology for customers. The thin-film solar panels are meant to revolutionize the way people use solar panels and the effectiveness of them too. But with the management burning through cash and share dilution running rampant, the best course of action would be to sell any shares in the company.

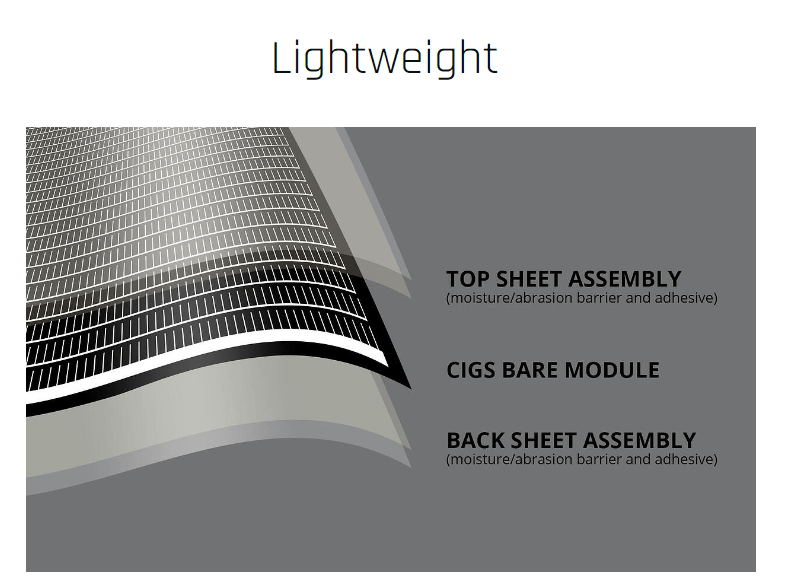

ASTI’s Product (Investors Presentation)

The light and thin film they offer is meant to be sold to companies producing and manufacturing solar modules. With these thin films ASTI argues that the possibilities broaden for companies to innovate the solutions for the solar industry.

With a larger demand for more green and renewable energy I expect more companies to start seeing the positives of getting into the space. This should be a large tailwind for ASTI as the customer base they have at their disposal would be widely larger.

Company Info (Q3 Earnings Report)

But besides providing solar module companies with their technology, ASTI expects to see demand from other directions. They have already partnered with certain companies producing all from high-altitude airships to military fabric-integrated systems. The thin-film product that ASTI offers is meant to easily be integrated and used in a wide array of products.

Company Revenues Are Disappearing

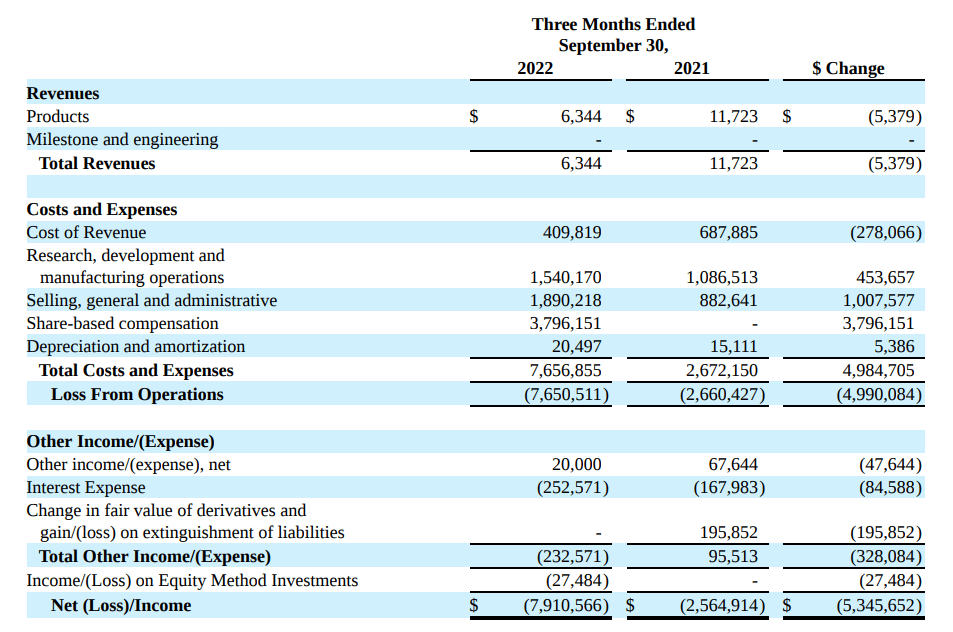

Looking at the revenues they are down 46% compared to last year’s same quarter. In the latest earnings report the company noted this decrease, but I am not a fan of the wording they were using. Being down “slightly” 46% YoY was the phrasing, I feel this is an irresponsible look at the situation.

Revenue Statement (Q3 Earnings Report)

Other notable things on the revenue sheet was the large share compensation that the company made. With $3.7 million in compensation, which was explained in large part due to the company’s new CEO. I think it’s a good idea that management have a vested interest in the company that they are working for, but this number doesn’t sit well with me when they are bleeding cash and seeing decreased revenues.

With the appointment of the new CEO also comes the departure of the last one. That departure came with a $500 000 price tag, something the company accounted for in their “selling, general and administrative” segment. Another thorn in their side as they are already struggling.

With all of the issues I laid out above, this resulted in the company losing over $5.3 million in the latest quarter. The company is bleeding money and it doesn’t seem like they are any closer this year to getting profitable than any other.

The Balance Sheet

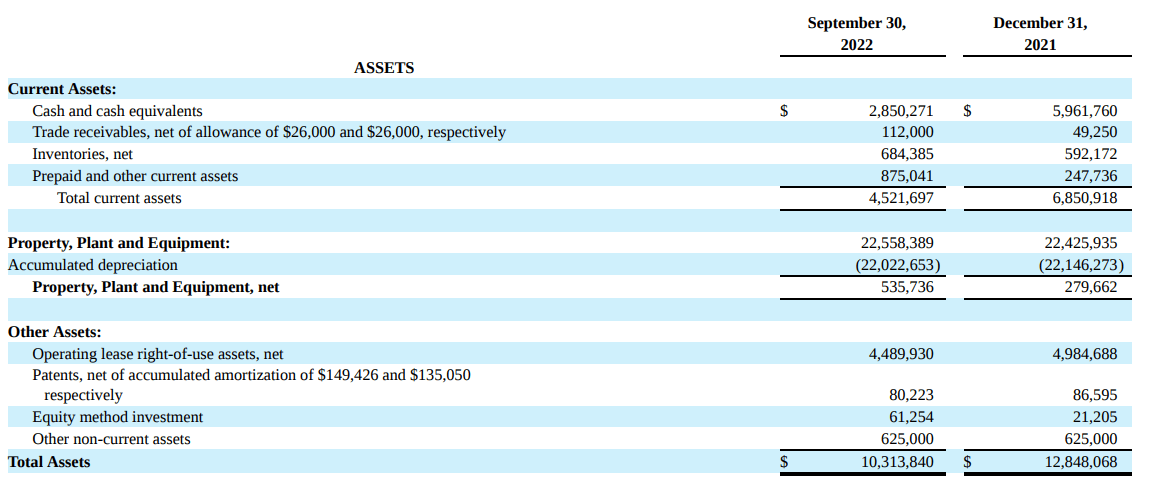

It wasn’t that the company was seeing smaller revenues or still being unprofitable that made me turn away from Ascent Solar Technologies. Instead, it was what I think seems like incredibly irresponsible spending by the company. The balance sheet is riddled with red flags.

ASTI Assets (Q3 Earnings Report)

Let’s begin by looking at the cash position. The company has managed to reduce their cash position by 50% YoY while revenues are nosediving. When I take a closer look it seems Ascent has spent a large sum of money on prepaying down certain other current assets.

Current Liabilities (Q3 Earnings Report)

The only real good thing the company might have going for them is that they are more or less debt free at least. But if we look closer at the liabilities section of the balance sheet then I note that accrued expenses have more than doubled compared to last year. Those are expenses that are yet to be invoiced but something the company has to account for. It scares me that the number has risen so rapidly in just 12 months. That makes me also feel uncertain about the future outlook of the company and any talk of profitability seems out of the picture.

Valuing The Company

I think it’s very difficult to value any company which has not yet been able to prove profitability. Unless they have a proven product and a stable financial ground to stand on, it’s impossible to see the future for them. All you have is the management’s word and it seems they don’t have that much of a vested interest in the company.

I think that the product they offer could be useful in a number of situations and there is a customer base for them to tap into. But I can’t see them having a larger increase in revenues until they get some of their financial issues under control. Share compensation and large administrative expenses might be some one off expenses, but it has a significant impact nevertheless.

ASTI has been able to secure some government contracts which should help provide some stability in terms of getting a growing top and bottom line. But until I see that trend reverse I think it’s very risky right now to have any money invested into the company. Much because the valuation is both at a premium and the downside risk could be immense.

Conclusion

Ascent Solar Technologies is a company producing a one of a kind technology of ultra thin and flexible PV film. They have managed to secure some government contracts and have a pretty niche sector to generate revenues from.

With a balance sheet in shambles and a revenue report that leaves question marks it doesn’t seem ASTI are right now where they could be, with 50% less cash compared to last year because of a departing CEO and investments in current assets. Another part keeping me away is the large increase in outstanding shares. It’s a new company in need of raising capital, so it should be expected. But there are limits.

Outstanding Shares (Seeking Alpha)

I think that investing right now into ASTI is very dangerous as the dilution is incredibly high and the company is not even profitable yet. This makes the valuation very high and creates a large downside risk. I would sell any shares I had if I were invested at these times. Until the company manages to be profitable I think there is too much risk here and therefore will stay away.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment