Geetarism/iStock via Getty Images

Never attribute to malevolence what is merely due to incompetence“― Arthur C. Clarke.

Today we look in on a small cap name that comes up from time to time in comments from Seeking Alpha followers. The company has about as many challenges with the FDA approval process for its primary drug candidate as Dynavax Technologies (DVAX) did with Heplisav-B, before that best of breed hepatitis B vaccine was approved on the third or fourth try. It since has become the standard of care and has rapidly taken market share. A similar outcome seems better than a 50/50 proposition for this concern as well. An analysis follows below.

Seeking Alpha

Company Overview:

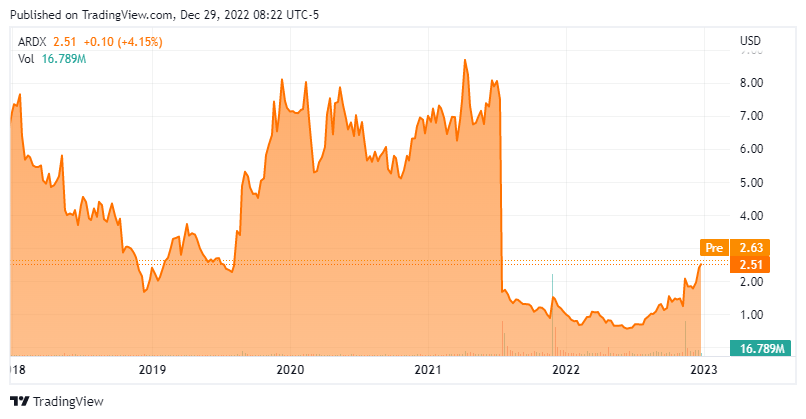

Ardelyx, Inc. (NASDAQ:ARDX) is a Waltham, Massachusetts-based biopharmaceutical company focused on the development of first-in-class remedies that meet significant unmet medical needs. The company’s lead –and for nearly a decade and a half its only – asset is tenapanor, which is approved (as IBSRELA) in the U.S. for irritable bowel syndrome with constipation (IBS-C). Ardelyx has also labored to get tenapanor approved for control of serum phosphorus levels in adult patients with chronic kidney disease (CKD) on dialysis. The company was founded in 2007 and went public in 2014, raising net proceeds of $61.2 million at $14 a share. The stock currently trades just over $2.50 a share, translating to a market cap of approximately $470 million.

September Company Presentation

Tenapanor

The founders’ understanding of the primary mechanism of sodium transport in the intestine led to their discovery of tenapanor, which is a sodium hydrogen exchanger 3 (NHE3) inhibitor approved for the treatment of IBS-C in adults. Obstruction of NHE3 deters dietary sodium absorption in the gut, resulting in increased intestinal transit time and softer stool. It also decreases intestinal permeability and visceral hypersensitivity to reduce abdominal pain.

Owing to these mechanisms of action, ISBRELA is a first-in-class IBS-C med, with the other four approved therapies classified as guanylate cyclase-C [GCC] agonists. The latter drugs promote the secretion of intestinal fluid to soften stool and stimulate bowel movements. However, 30%-40% of patients on GCC agonists do not adequately respond, with 77% continuing to experience residual abdominal and stool related symptoms such as bloating. These four treatments generated FY21 sales of $2.8 billion. Approved in September 2019 and launched in April 2022, ISBRELA accounted for net sales of $4.9 million in 3Q22.

The reason for the two-and-a-half-year lacuna between approval and launch had to do with Ardelyx’s inability to find a commercial partner, which may have been exacerbated by its (to date) failed journey to obtain approval for tenapanor in another indication: hyperphosphatemia. Positioned as a first-in-class phosphate absorption inhibitor for the control of serum phosphorous in patients with CKD on dialysis (and if approved, marketed as XPHOZOA), tenapanor achieved its primary endpoint in three Phase 3 trials – more on them shortly – setting it up for a mid-2021 FDA approval. However, the FDA issued a CRL to Ardelyx in July 2021 (after extending the review period by three months), citing its impact as “small and of unclear clinical significance,” requiring another study to confirm tenapanor’s “clinically relevant treatment effect.“

September Company Presentation

This news astonished the investment community, with shares of ARDX cratering 74% to $2.01 in the subsequent trading session. The shock was not unjustified, given tenapanor clinical performance.

September Company Presentation

In its first Phase 3 study (BLOCK), a 219-patient, short-term monotherapy trial that was readout in 2017, the treatment achieved a statistically significant (p<0.01) difference in least squared mean phosphorous change (0.82 mg/dL) versus placebo and a 1.1 mg/dL reduction versus baseline at week 8.

The second study (AMPLIFY), which was read out in September 2019, targeted patients (n=236) who were already on a stable phosphate binder regime but still had serum phosphorus levels between 5.5 mg/dL and 10.0 mg/dL. (Normal levels are between 2.5 and 4.5 mg/dL with levels above 5.5 mg/dL an indication of increased risk for cardiovascular morbidity and mortality in CKD patients – as it is not readily removed via dialysis – as well as muscle cramps, skin rashes, and joint pain.) Patients were randomized to receive the addition of tenapanor or placebo twice daily with a baseline mean of 6.8 mg/dL. The primary endpoint was achieved with a mean reduction in phosphorus levels of 0.84 mg/dL in the tenapanor arm versus 0.19 mg/dL in the binder arm (p=0.0004) at week 4. Also, 49.1% of patients in the tenapanor arm achieved serum phosphorus of <5.5 mg/dL as compared to 23.5% in the binder arm (p<0.0097).

In its third trial (PHREEDOM) comprising 564 patients and readout in December 2019, tenapanor monotherapy demonstrated a statistically significant (p<0.0001) difference in least squared mean phosphorous change (1.4 mg/dL) versus placebo and a 1.4 mg/dL reduction versus baseline at week 26.

Across the three studies, the only adverse reaction reported in more than 5% of the patients was mild-to-moderate diarrhea (47%), generally occurring briefly at the onset of the trials. It was not treatment limiting. Adding to the shock of the rejection was the fact that hyperphosphatemia is currently addressed through low phosphate diets and phosphate binders, the latter of which is riddled with issues.

First, phosphate binders also attach to calcium, iron, and other essential minerals; thus, requiring supplementation. Second, compliance is an issue as mass quantities of binders are required daily, resulting in a host of significant GI tract irregularities. Hyperphosphatemia patients require a mean of ~19 pills a day versus twice-daily XPHOZOA. Even with this excessive pill burden, many CKD patients (~72%) on dialysis still can’t get their serum phosphorus levels below 5.5 mg/dL. As such, there is plenty of need for a better class of therapy. The FDA apparently didn’t agree.

Ardelyx did not sit idly by. After an End-of-Review Type A meeting in October 2021, Ardelyx filed a dispute resolution request with the Office of New Drugs [OND] in December. In February 2022, the company received an Appeal Denied Letter [ADL] from the OND. Ardelyx responded by filing an appeal to the ADL, to which the FDA agreed to convene its Cardiovascular and Renal Drug Advisory Committee (CRDAC) to reconsider the application. Finally, on November 16, 2022 the CRDAC voted 9-4 in favor of tenapanor as a monotherapy and 10-2 (one abstention) in combination with phosphate-binder treatments.

Then, this morning it was announced that the FDA has granted an appeal to the agency’s complete response letter. Ardelyx now plans to have a follow up meeting and refile its marketing application for XPHOZOA sometime in the first half of 2023.

If approved, with ~440,000 CKD patients in the U.S. on dialysis and requiring treatment for hyperphosphatemia, XPHOZOA’s market opportunity is ~$500 million to $700 million. Add in ~260,000 similar patients in Europe and ~289,000 in Japan and its prospects look even better.

That said, the impact of the FDA rejection on the company has been profound. Ardelyx has implemented two rounds of layoffs resulting in a ~60% reduction of its workforce. And unable to find a marketing partner in the U.S. for the IBS-C indication, it was compelled to launch IBSRELA on its own.

Furthermore, while the tenapanor drama was unfolding, Ardelyx’s other clinical asset, potassium secretagogue RDX013, was unable to separate from placebo treating hyperkalemia (elevated potassium) in CKD patients not on dialysis during a Phase 2 study, which was readout in April 2022.

Balance Sheet & Analyst Commentary:

In addition to the effect on its operations, the FDA saga with tenapanor significantly impacted Ardelyx’s balance sheet. If its NHE3 inhibitor had been approved for hyperphosphatemia as anticipated in mid-2021, management would have likely leveraged the positive news into a lightly dilutive capital raise for its commercial launch — given that no partner had been found at that time. Instead, with its share-price meltdown subsequent to the initial rejection, the company elected to utilize an ATM facility to sell stock quietly into the market. Since the initial CRL letter, Ardelyx has raised gross proceeds of $79.0 million under its ATM but at the expense of 68.8 million shares (as of September 30, 2022), diluting shareholders by ~50%. The company also entered into a debt facility in February 2022, providing it with an additional $27.5 million. At the end of 3Q22, Ardelyx held cash and investments of $90.6 million with its runway a function of the ramp of IBSRELA and the impending decision on XPHOZOA.

With all the back and forth regarding tenapanor, the sell-side analyst community still leans positive on Ardelyx. Piper Sadler upgraded the stock from hold to outperform and raised its price objective from $3 to $8 after the CRDAC vote. The analyst firm reiterated that rating on December 18th. It is the only one to offer commentary since that positive development. In total, the Street now has one outperform and three buy ratings against two holds. Price targets range from $1 to $10. Given this morning’s news, I would expect more analyst firms to chime in around Ardelyx in the coming week.

Board member David Mott is clearly bullish, having purchased 567,000 shares at 1.76 on November 17, 2022 – the day after the CRDAC vote.

Verdict:

To characterize the FDA’s actions in relation to XPHOZOA as “head scratching” would be generous. As such, the outcome of the FDA approval is by no means a slam dunk, but it is trending more positive. That said, Ardelyx is a coin flip: tails it becomes a sub-$1 stock, save IBSRELA sales skyrocketing; heads and tenapanor (as both IBSRELA and XPHOZOA) has a shot at blockbuster status by the end of the decade, meaning its stock is worth likely in the high single digits. That asymmetrical risk-reward profile renders Ardelyx a speculative buy worthy of a small holding.

I established a small position in ARDX when I published this research exclusively to Biotech Forum members just less than a month ago, about half via straight equity and the rest through covered call orders. I have updated this investment thesis to account for the news since then, but that is the investment approach I would continue to take around the stock

It happens; incompetence is rewarded more often than not.”― Jeff Lindsay, Darkly Dreaming Dexter

Be the first to comment