Agriculture is in turmoil. Crop prices have started to fall off a cliff, pressuring related companies in the business. In this article, I will discuss these developments and explain why Archer-Daniels-Midlands Company (NYSE:ADM) offers investors low volatility exposure to the industry that comes with a dividend. I’ve gotten a lot of questions from (retail) investors who wanted exposure by buying, i.e., commodity exchange-traded funds (“ETFs”) or futures. While none of these options are bad, I think long-term investors should focus on companies like ADM with a well-diversified footprint in the industry, a healthy balances sheet, and long-term dividend growth instead of volatile financial derivatives or ETFs with high expense ratios.

In this article, I will give you the details and discuss the ADM bull case based on current developments.

So, bear with me!

Reasons To Buy Agriculture

There are a few reasons why I try to avoid ETFs as much as possible. One reason is the “Do It Yourself” factor, as finding good investments is pretty much my job. Another reason is that I don’t like the fact that ETF providers have become so powerful. They own large chunks of major companies, allowing them to participate in proxy battles and related corporate governance issues.

A third reason has to do with expense ratios. ETFs charge a fee for allowing investors to invest in their funds. The moment I advise people to buy ETFs, I start to benefit a third party. Sometimes that doesn’t sit right – especially when dealing with a high expense ratio.

With that said, even if “we” don’t invest that much in ETFs, some ETFs are great tools to monitor markets, especially for investors who like to stay away from futures.

One provider of these ETFs is Teucrium. This company offers specific ETFs that allow investors to buy certain crop types. I.e., corn, wheat, and soybeans. The problem is that its wheat ETF (WEAT) has an expense ratio of 1.14%.

Anyway, the reason I’m bringing this up is that Teucrium is making a compelling case for long-term agriculture investments.

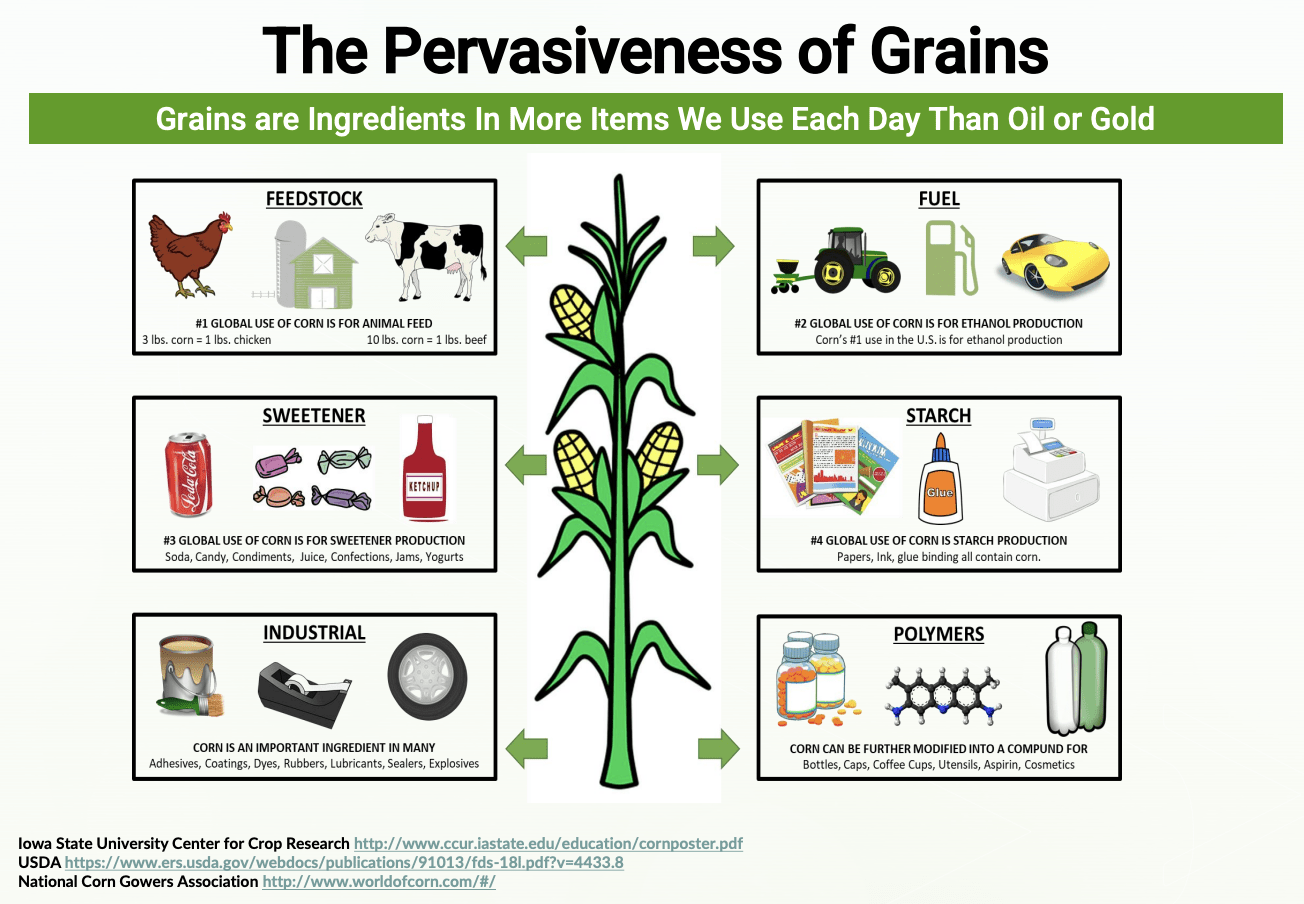

I like the slide below as it shows the impact of corn. Corn isn’t just feedstock for animal feed, but a major input of fuel (ethanol), sweeteners, starch, as well as industrial/chemical applications.

Teucrium

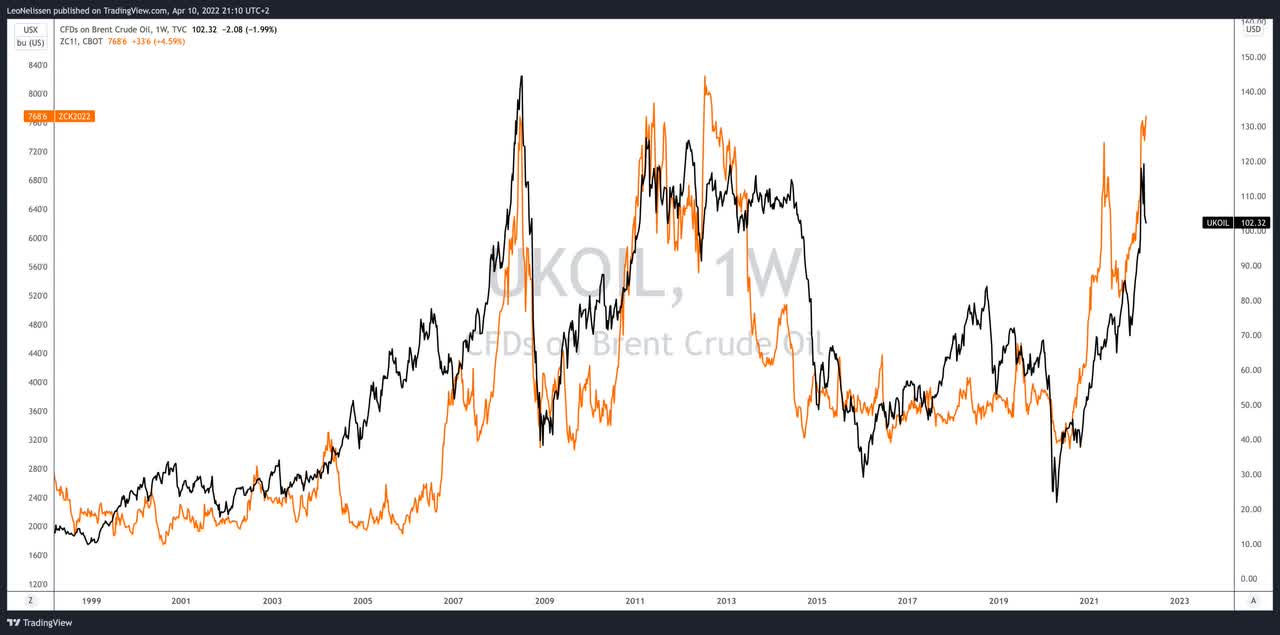

What this means is that agriculture (in this case, corn) is highly tied to other cyclical commodities. For example, the chart below shows a chart I tweeted in April. The black line shows crude oil (Brent). The orange line shows corn prices. This has multiple reasons. Not only is corn an energy input, but higher energy prices also make the production of fertilizers more expensive, pressuring yields (lowering supply estimates).

TradingView

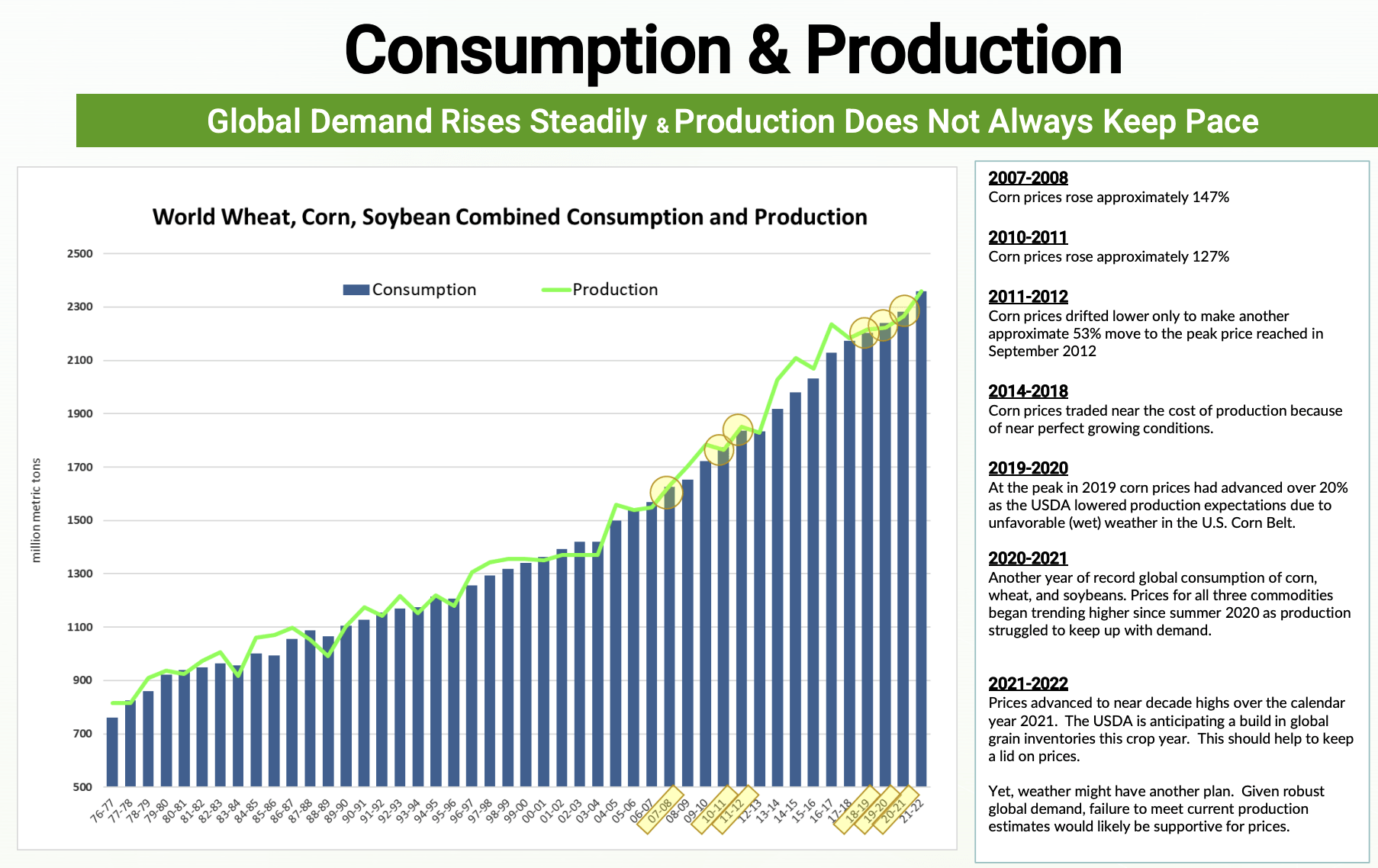

Moreover, Teucrium estimates that the global middle class will reach more than 5 billion people in 2030. That’s up from roughly 3.5 billion in 2018. This means higher consumption. Especially if emerging market middle-classes consume more meat, we’ll see a surge in crop demand.

Since 2018, global crop supply/demand has become tight, with multiple years seeing higher demand than supply among key crops, as the chart below shows.

Teucrium

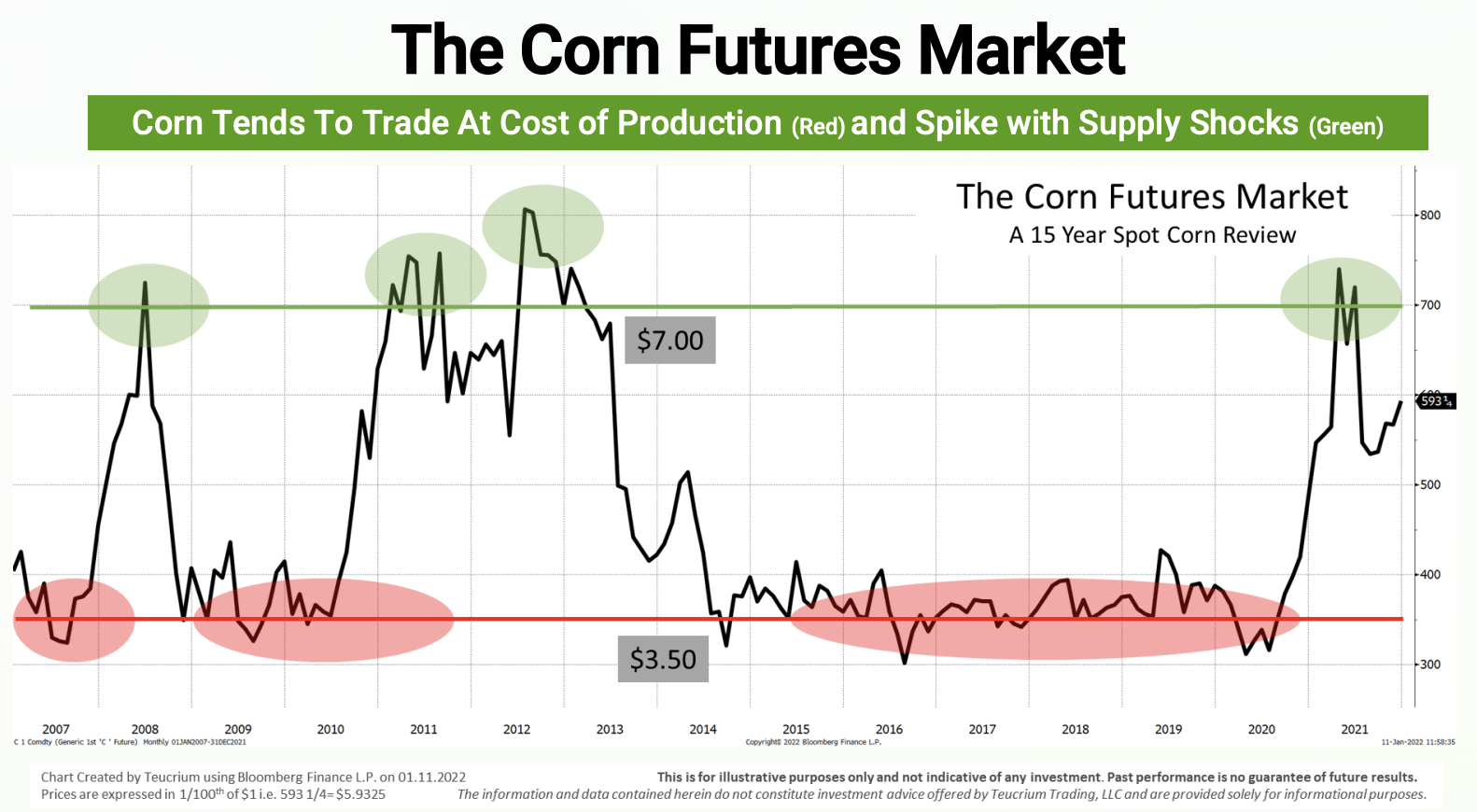

With that said, corn, wheat, soy, or any related crop prices are not in a long-term uptrend like the stock market.

The chart below shows why that is not the case. Please note that other crops show similar developments. More often than not, crop prices trade close to the cost of production. Between 2015 and 2020, corn traded at $3.50 per bushel. During this period, the global middle class grew, the economy expanded, and crop demand rose.

Teucrium

It takes supply shocks to trigger an uptrend in crop prices. Right now, we’re seeing one based on high energy prices, high crop demand, and pressure on supply (caused by the weather and fertilizers).

Right now, corn prices are roughly 22% below their recent highs. Wheat is down more than 30%.

TradingView (Black = Corn, Orange = Wheat)

I believe this is based on a number of reasons:

Energy prices and commodities are suffering as investors are pricing in a recession.

The market was massively overbought after the shock caused by Russia’s invasion of Ukraine.

The Quarterly Grain stocks report was very neutral. All three grain stocks came within 6 million bushels of trade estimates.

So why the selloff in grains today? Typically with a neutral report we will still see prices drift lower, but today’s action was more than that. We are still seeing money flow exit the commodity markets as we are at month end and quarter end. Many traders are liquidating their positions to get a balance of where they ended the quarter. Also, recession seems to be weighing on everyone’s mind as well, spooking investors.

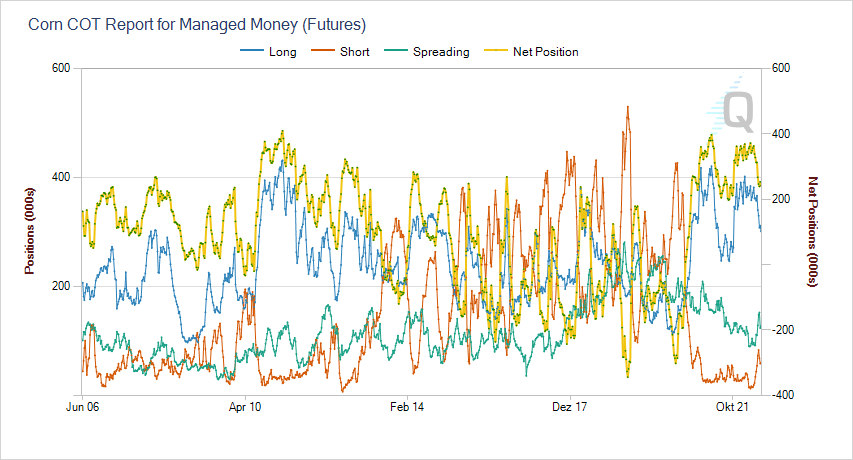

This is what money manager net positions in corn futures look like (the yellow line shows net positions). Money managers are still “very long,” which now provides corn with some downside.

CME Group

Personally, I do not believe that corn prices will come down a lot. Supply is constrained, the situation in Ukraine won’t be solved anytime soon, and energy shortages will keep production costs high.

Yet, I don’t use this as an opportunity to get people to invest in the commodity. No, as the introduction already included, I think ADM is a great way to put money to work on a long-term basis, throughout different economic cycles.

Why I Like Archer-Daniels-Midland

Archer Daniels is one of the largest and most well-diversified agriculture companies in the world. While it doesn’t produce tractors or (a lot of) fertilizers, it does pretty much anything else related to the agricultural supply chain.

ADM is an extremely complex company engaged in all key aspects of the global food supply chain. This Chicago-based company was founded in 1902 and employs close to 40,000 employees. With a market cap of roughly $42.4 billion, it’s the largest company in the farm products industry.

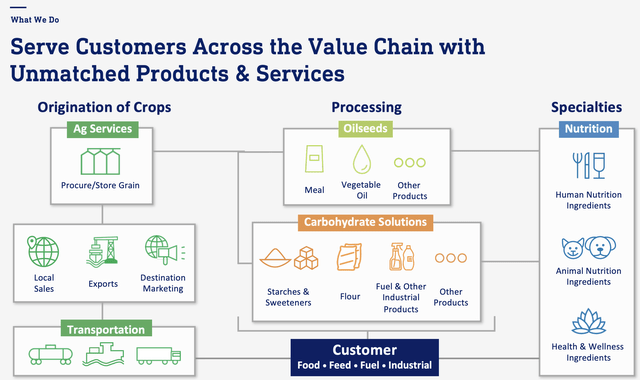

ADM operates a number of business segments.

Ag Services & Oilseeds (77% of 2020 sales)

Carbohydrate Solutions (13%)

Nutrition (9%)

Other (Negligible)

Ag services and oilseeds include operations that take place at the start of the food supply chain. These operations are related to the origination, merchandising, transportation, and storage of agricultural raw materials, and the crushing and further processing of oilseeds (soybeans, cottonseed, sunflower seed, canola, rapeseed, etc.). These products are used food, feed, energy, and industrial feedstock. This includes renewable diesel and more or less everything that comes to mind when thinking of food.

On top of that, the company owns the largest ethanol plants in the United States. According to the data below, the company owns half of the largest ethanol plants in the United States.

The overview below shows the company’s business segments.

ADM

Last year, it was reported that ADM was about to enter sustainable aviation fuels. The company, with a 1.6 billion ethanol capacity, is looking to produce up to 500 million gallons of sustainable aviation fuel at its seven plants.

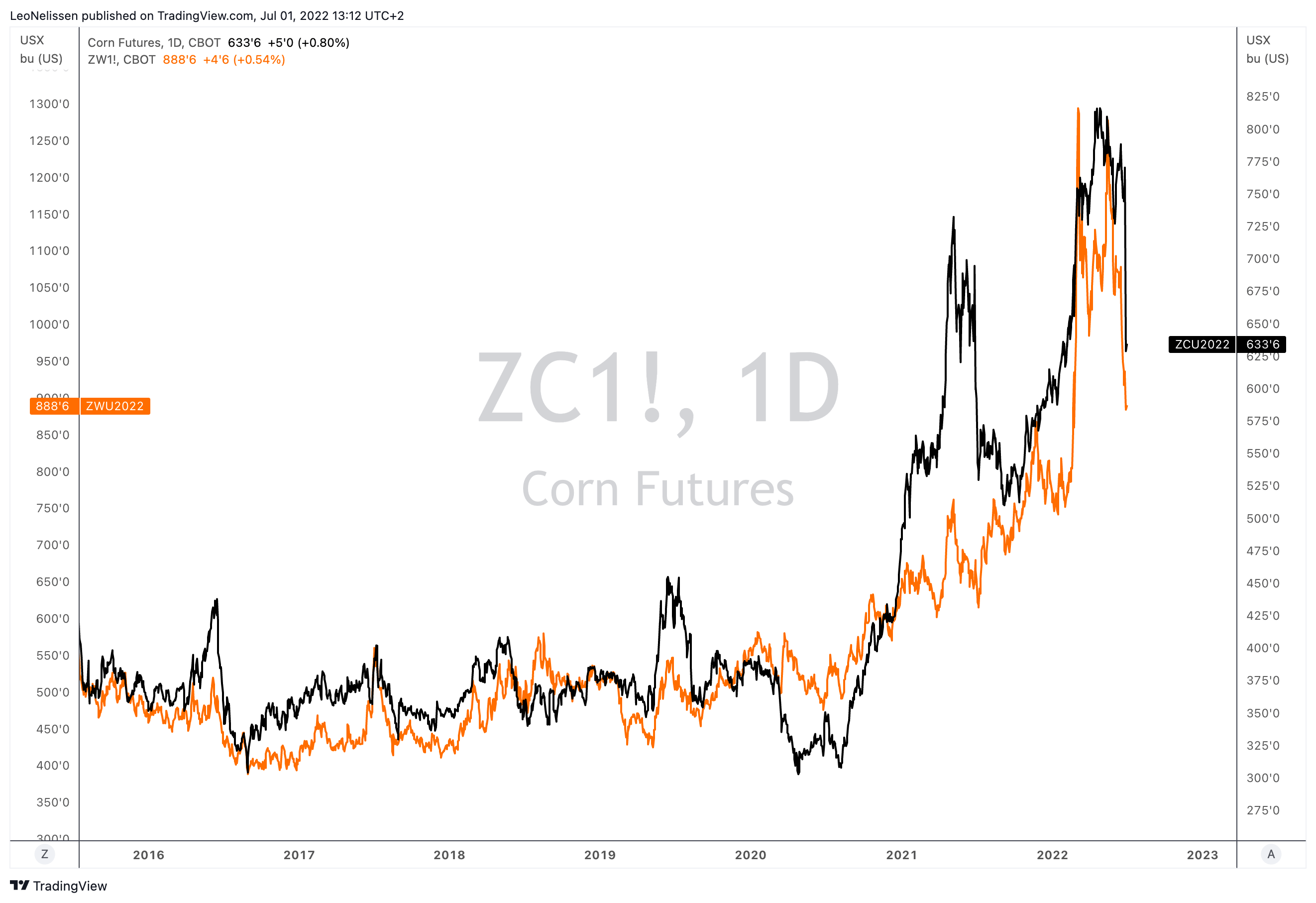

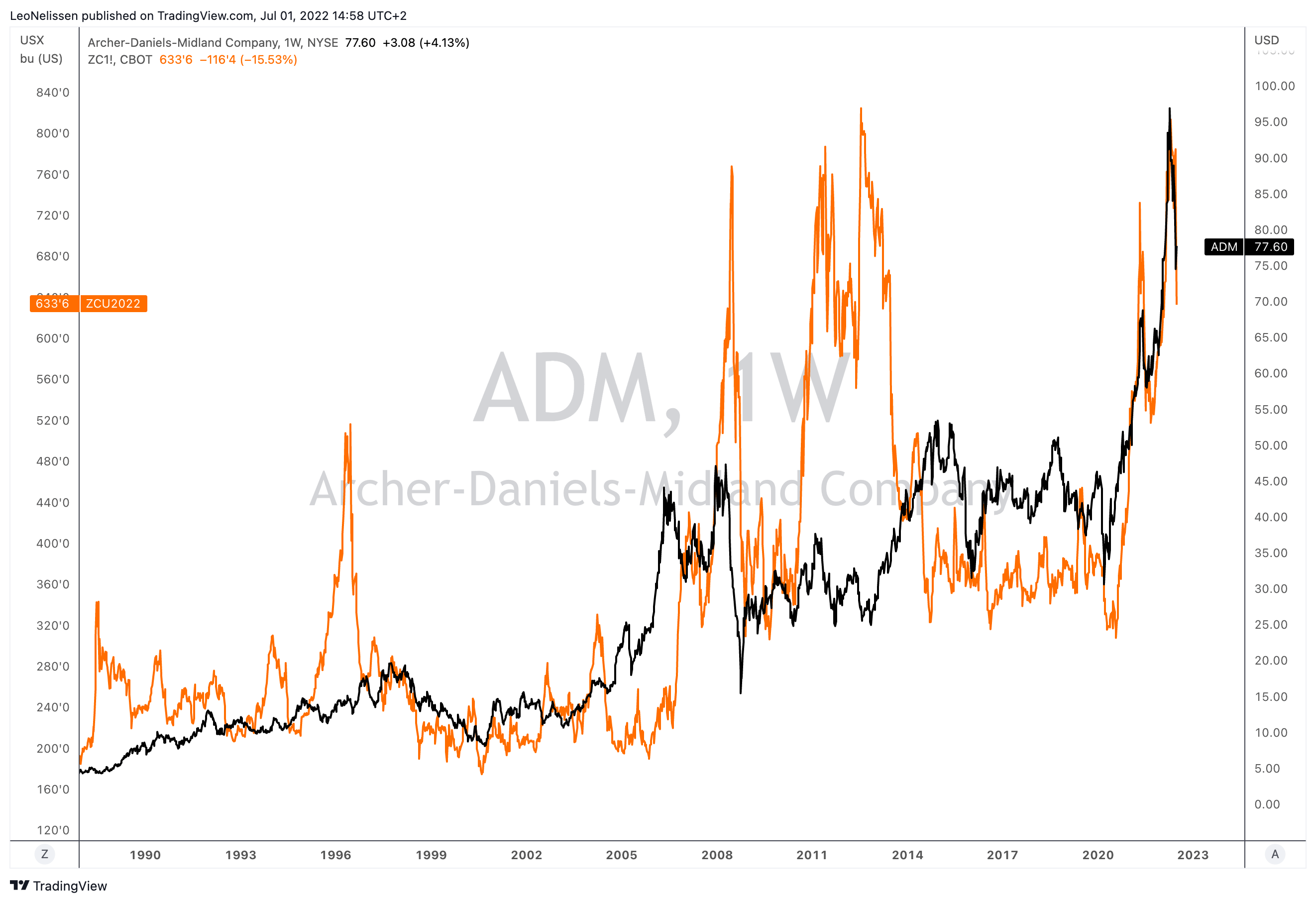

ADM’s exposure to prices and product margins tied to crops causes its stock price to move almost in lockstep with the price of corn – again, I’m using corn here because of its many uses.

TradingView (Black = ADM, Orange = Corn)

I added “almost” to the chart above because the correlation isn’t perfect. For example, during the first 7 years of this decade, the stock exploded despite flat corn prices. Then, when corn accelerated prior to the housing crash, ADM further accelerated.

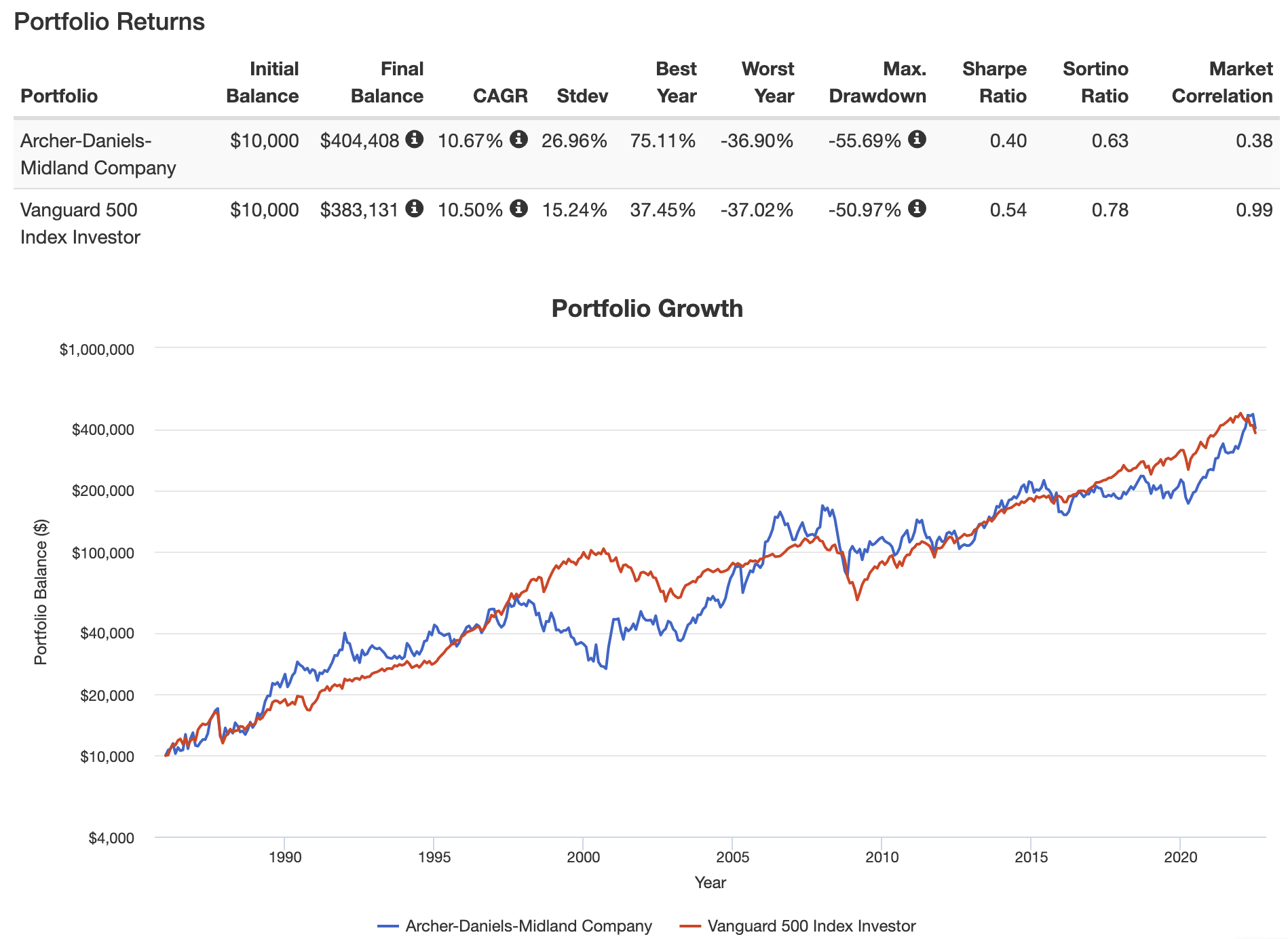

Since 1985, the company has returned 10.7% per year – including dividends. This beats the S&P 500 by a narrow margin. Needless to say, ADM is more volatile. Its standard deviation during this period is 27.0%.

Portfolio Visualizer

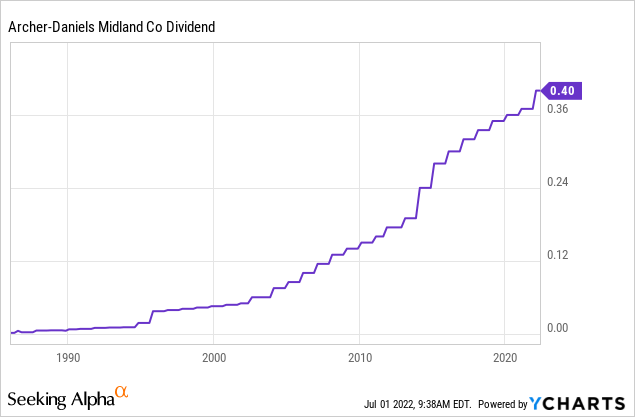

Not only does this performance beat any agriculture commodity, but it also comes with steady cash flow for its investors: the dividend.

ADM pays a $0.40 dividend per share per quarter. That’s $1.60 per year and 2.1% of the company’s stock price. That’s not a very high yield, but it gets the job done.

By “getting the job done”, I mean protecting investors against inflation. The company’s 10-year average annual dividend growth rate is 8.4%. The most recent hike was announced on January 25, when management hiked by 8.1%.

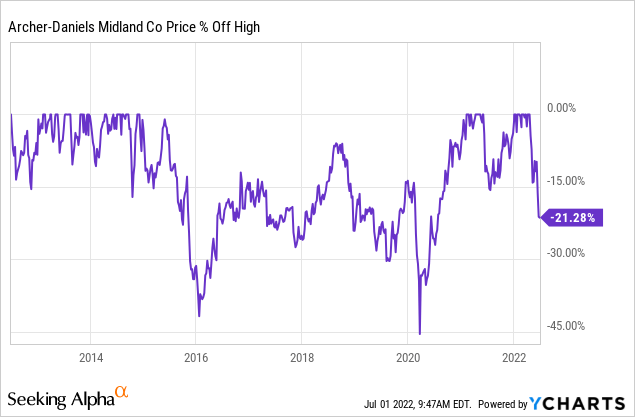

As I wrote in the first part of this article, I believe that investors overreacted. Recession fears were being priced into the market, causing stocks with strong tailwinds to fall. Unfortunately (for the consumer), major issues persist. The energy supply issue is lasting, agriculture is extremely dependent on good weather, and ethanol tailwinds are strong.

The Biden administration in April targeted ethanol as a way to ease rising gas prices, raising the amount that can be blended into gasoline for this summer. U.S. gasoline prices were at $4.93 a gallon as of Friday, up 60% from a year earlier, according to AAA data, after retreating from highs set earlier this month. Americans haven’t adjusted their driving habits despite the increase, which will continue to power ethanol prices, analysts say.

Moreover:

“I don’t think the ride is over yet,” said Dan Flynn, a senior analyst at Price Futures Group, who estimates that a bushel of corn will trade for around $10 by the end of the year. Prices settled Friday at $6.74 a bushel.

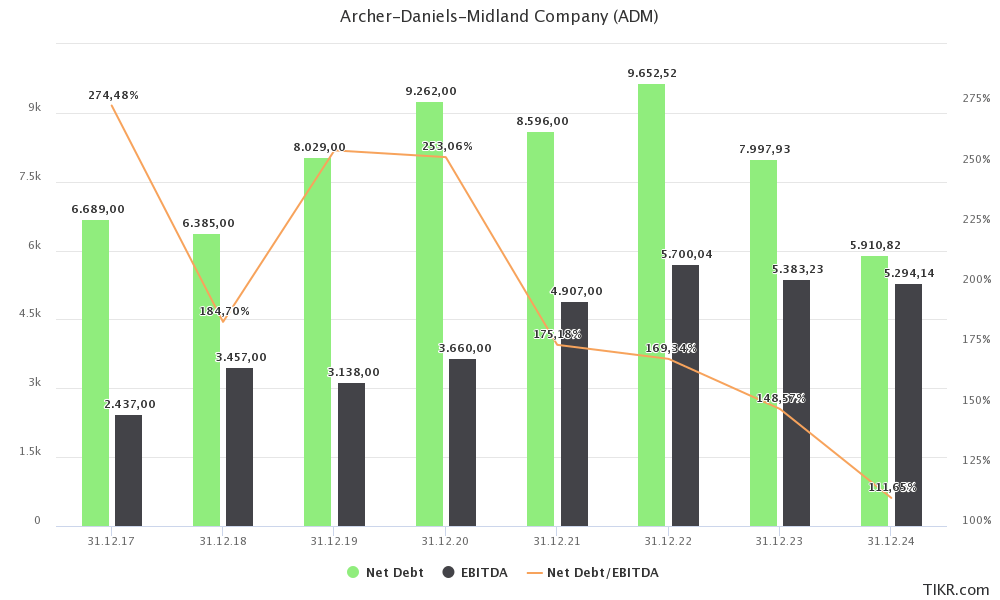

While potential economic headwinds aren’t helping, analysts expect EBITDA to reach $5.7 billion this year, with consistent results of more than $5.2 billion in the years ahead. I believe that 2023 and 2024 will be stronger than expected, but I’m using analyst estimates for now.

TIKR.com

Using the company’s $43.3 billion market cap, $8.0 billion in expected net debt (just 1.5x EBITDA), and $300 million in minority interest gives the company an enterprise value of $51.6 billion. That’s 9.6x next year’s EBITDA.

This valuation makes sense, offering investors opportunities to either add to an existing position or initiate a new position.

Takeaway

Archer-Daniels-Midland is a very conservative stock. It has a massive footprint in the agriculture supply chain, allowing the company to benefit from ongoing tailwinds. Grain demand is high, crop prices remain at high levels despite recent weakness, and energy markets continue to support margins for ethanol and related output products.

While the stock’s dividend yield isn’t very high, dividend growth is satisfying and consistent. Moreover, while ADM is an agriculture play with a high correlation to crop prices, it has a history of high total returns.

The current stock price weakness supports investments in this business, and I believe that ADM has entered an extended period of significant tailwinds and outperforming returns.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment