JHVEPhoto/iStock Editorial via Getty Images

Aramark (NYSE:ARMK) is a Fortune 500 company with a diversified range of high-quality food and facilities management services across the world. ARMK continues to show some recovery from the pandemic, especially while looking at its record net new business performance in FY ’22 resulting in a better retention rate performance and continued margin expansion. The company has a strong presence in North America and is ranked third in the food and facilities services market. In fact, they continued expanding and acquired Union Supply, enhancing its food service capabilities. Additionally, ARMK is well-known for its Uniform business, which ranks second in North America. Despite the management’s plan to spin off its Uniform business, ARMK will continue to operate in a large and diverse market, with a total addressable market estimated to be worth over $500 billion. Considering these factors, as well as its improved balance sheet, ARMK remains stable and appealing, particularly in light of its probable pullback.

Company Overview

Aramark’s revenue continues to improve; it finished FY’22 with a total revenue of $16,326.6 million, up from $16,227.3 million in FY’19. Despite today’s challenging operating environment, this success is being driven by maintained high retention rates and consistent new business gains, as quoted below.

Aramark’s strong growth performance was broad-based coming from multiple lines of business and geographies, as well as from clients with large and small, annualized gross new business wins exceeded $1.6 billion, representing 10% of pre-COVID fiscal 2019 revenues and retention rates were once again about 95% as we sustained a step change improvement. Source: Q4’22 Earnings Call Transcript

Also, as stated below, they are now one step closer to achieving their 2025 goal.

This exceptional level of net new business represents nearly 5% of our pre-COVID fiscal 2019 revenues, already at the top end of the 4% to 5% range provided in our Analysts Day financial algorithm. Source: Q4’22 Earnings Call Transcript

Another value-adding catalyst, this top line growth is mainly driven by volume recovery and the management sees continued demand pick-up next fiscal year.

Performance is driven by strong net new business, pricing pass-through and ongoing recovery of COVID-related volumes, which is just over 90% of pre-COVID levels for the year progressed each quarter from an estimated 85% in Q1 and about 95% in Q4. Source: Q4’22 Earnings Call Transcript

This is a perfect recipe for ARMK to generate $780 million in adjusted operating income and 4.87% adjusted operating margin on a constant currency basis, up from 2.44% in FY’21.

Considering the potential spinoff of its uniform business will allow Aramark to focus on its core food and facilities management services, as well as potentially attract new partners, bringing efficiency and attracting new clients.

Over the course of the year, we’ve been gradually able to transition back to preferred suppliers and products as fill rates improved. While there’s still much more to go, this year was an important step for a return to normal supply chain operations.

In addition, as the supply chain settles, and our net new business growth significantly increases our manage spend, we work to renegotiate current deals to achieve next generation savings is beginning, and we’re encouraged by the opportunity in front of us in this area. Source: Q4’22 Earnings Call Transcript

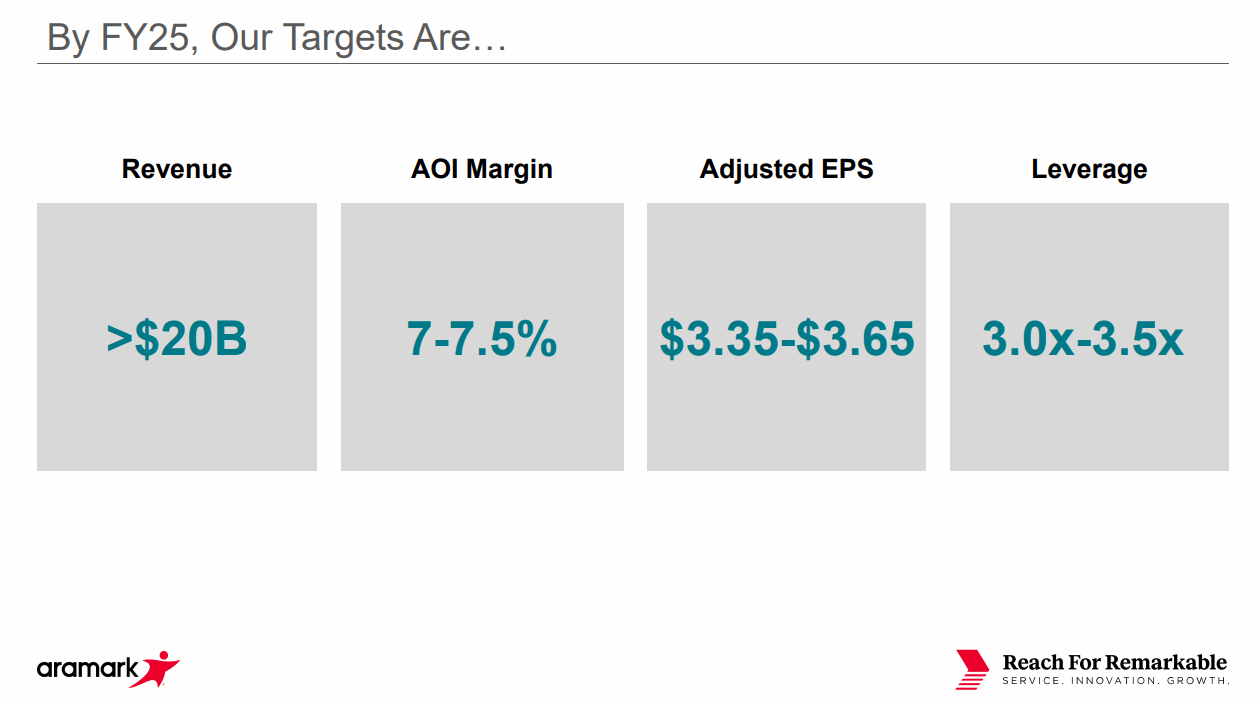

With today’s performance, ARMK might meet its 7%-7.5% adjusted operating income target for FY25.

Remains Appealing Despite Its Plan to Spin off Its Uniform Business

Despite its plan to spin-off its Uniform business into a separate publicly traded company, ARMK remains attractive, especially looking at its asset turnover without Uniform Business.

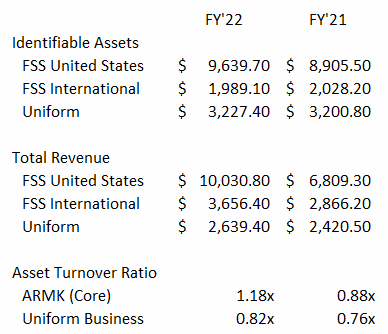

ARMK: Asset Turnover Ratio (Source: Data Source from Q4’22 Report. Prepared by the Author )

Potentially without its Uniform Business, ARMK continues to improve, as seen by its asset turnover of 1.18x, up 33% from 0.88x in FY’21, when compared to its Uniform Business, which grew just 8% year over year. ARMK will retain around 77% of its total assets, allaying fears about substantial deviations from delivering its 2025 target, as shown in the image below.

ARMK: 2025 Target (Source: ARMK Analyst Day Presentation)

In fact, management has given reassurance that they still intend to realize their leverage target of less than 3.5x in FY25 and vowed to continue share buybacks as their leverage improves. ARMK also flexed its liquid balance sheet, with no significant debt maturities until FY25, as seen below.

Our strong cash flow performance combined with significantly higher earnings resulted in an improved leverage ratio of 5.3 times compared to 7.4 times at year end fiscal 2021. We remain on track to reduce leverage below 3.5 times as mentioned at analyst day, and we believe we are well-positioned to navigate the current environment with a net debt portfolio of more than 80% fixed rate instruments inclusive of swaps, no significant maturities until 2025 and over $1.8 million in cash availability of fiscal year end. Source: Q4’22 Earnings Call Transcript

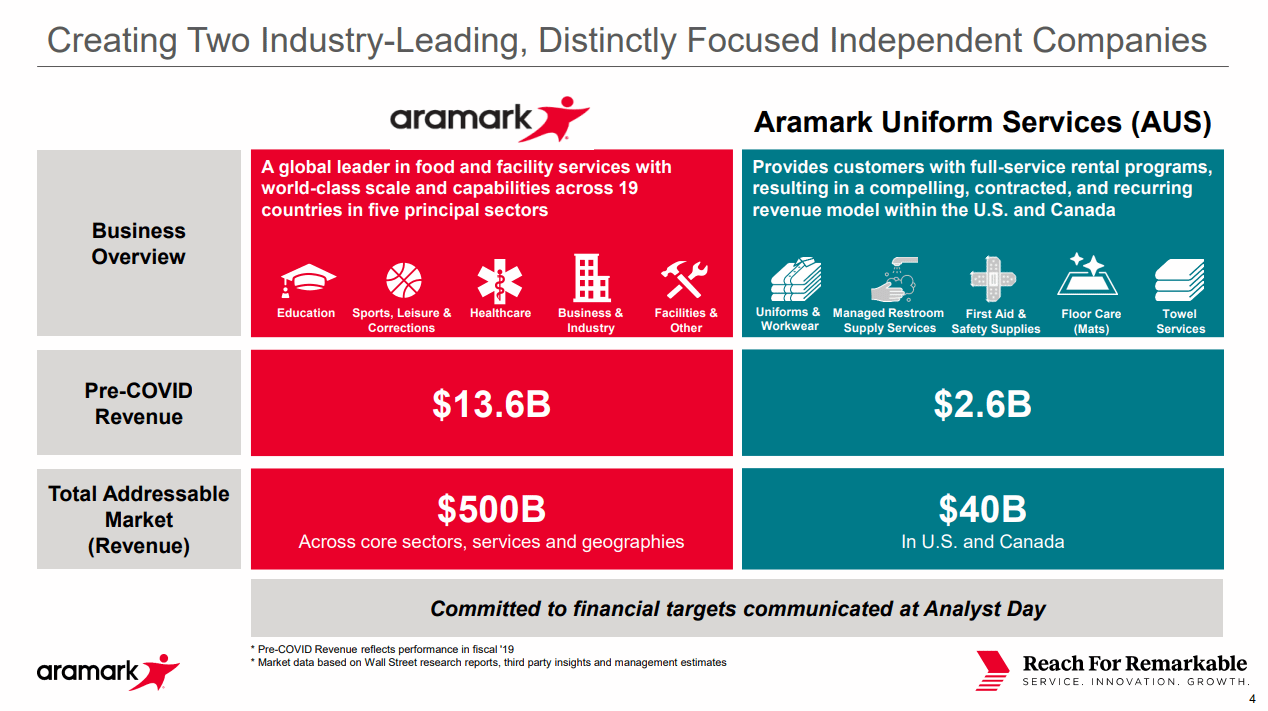

ARMK: Updated TAM (Source: Aramark Investor Update Presentation)

Management reassured that ARMK will continue to operate in $500 billion total addressable market. Hence, it is most likely that management will cut its FY’25 total revenue target to approximately $18.5 billion and estimated earnings per share of $3.1 or a forward P/E of 14.2x, relatively cheaper than its 5-year average of 22.18x. With this catalyst in place, I believe ARMK remains attractive, especially during pullbacks. Additionally, looking at the street’s target of $55, I believe we might see potential new highs next fiscal year.

Consolidation Near All-Time High

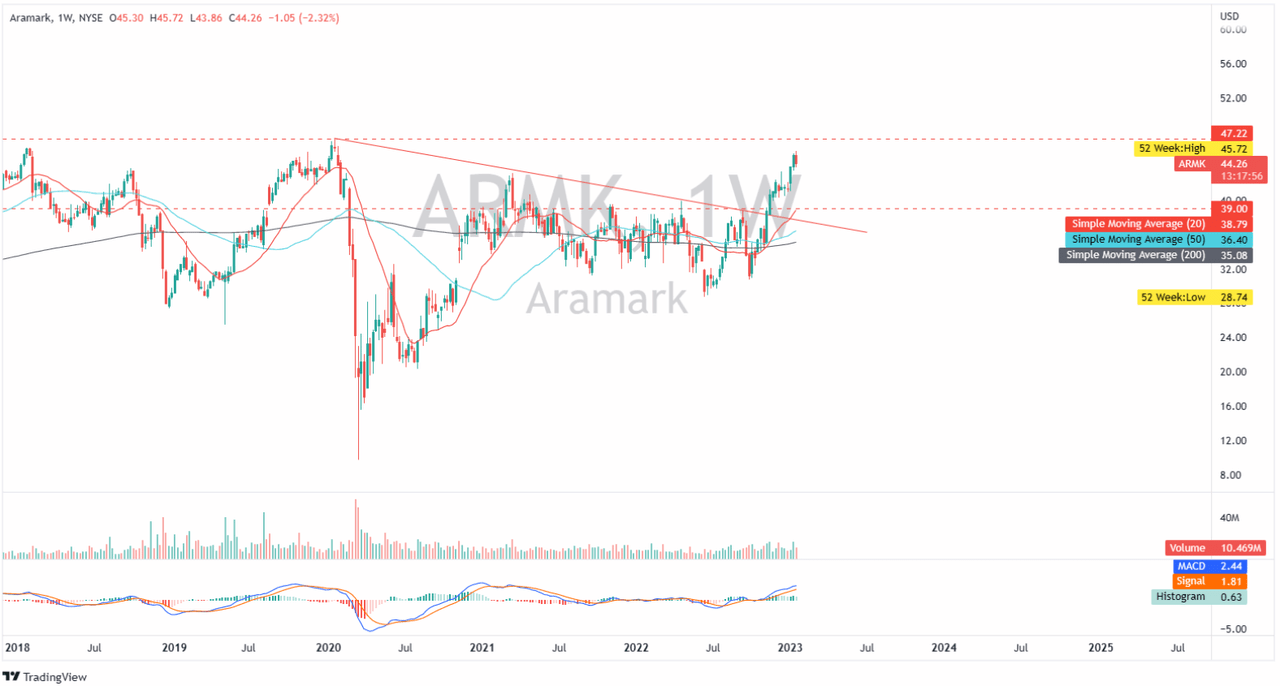

ARMK: Weekly Chart (Source: Author’s TradingView Account)

Looking at the chart above, we can see that ARMK has just broken out of its multi-month trend line, indicating a strong bullish move. However, the price is approaching its 52-week high and indicating some price action weakness, potentially printing red candles in the next weeks. If this occurs, I would want to see another consolidation above the $39 support level before attempting to break out to new highs. Despite today’s weakness, MACD remains above zero, providing another chance to buy ARMK at a cheaper price. ARMK may retest the $30 level if the price breaks below its $39 level and is accompanied by bearish catalysts such as poor execution on their margin expansion plan.

Conclusive Thoughts

On the other hand, I question the timing of ARMK’s intended spin-off since it would incur unnecessary costs and maybe impairment charges as a result of the spin-off, thus dragging its bottom line down. In fact, management forecasted better free cash flow (“FCF”) of $475 million to $525 million in FY’25 before the payment of deferred payroll taxes and related spin-off costs, and guided lower FCF amounting to $300 million to $350 million after specific charges.

First, we will make the last, but two deferred FICA payments associated with the Cares Act. Like last year, and as previously articulated, we expect to make this payment of approximately $65 million in the first quarter.

Second, we anticipate a cash flow impact of approximately $100 million to $120 million related to restructuring charges, public company costs and transaction fees associated with a uniform spin. After these specific items, we expect free cash flow to be in the range of $300 million to $350 million. Source: Q4’22 Earnings Call Transcript

With $265.44 million in adjusted operating income and a 10.06% adjusted operating margin for the Uniform business segment at the end of FY’22, this segment remains a significant contributor to the company’s overall financial performance. Additionally, if the Uniform business spin-off proceeds, I believe ARMK will benefit from fewer human resource-related expenditures, lower depreciation expenses, and a deleveraged balance sheet, as indicated below.

Aramark Uniform Services intends to raise debt that would result in a one-time dividend of cash to Aramark that is expected to be used to pay down outstanding Aramark debt. Aramark may also retire a portion of its existing debt by means of an exchange of Aramark Uniform Services debt securities for outstanding Aramark debt securities. Source: Here

Finally, Aramark has been growing its core business segments, such as healthcare, education and Sports, leisure and correction, which have been showing steady growth and are expected to continue growing in the future. The company has also implemented cost-saving measures and has been leveraging the use of technology to improve efficiency and drive growth. These efforts could help offset the loss of the high margin Uniform segment and ultimately help the company achieve its long-term financial goals. This makes ARMK fundamentally attractive and a buy on its potential pullback.

Thank you for reading and good luck everyone! Cheers!

Be the first to comment