PonyWang

First of all, we must consider that for many investors, Applied Materials (NASDAQ:AMAT) stock is something of an obvious buy.

Why so? Because, they see that most of the semiconductor industry might experience a business activity trough during H1 2023, followed by a rebound from H2 2023 onwards. Since we’re just 6 months away from such possible rebound, many investors think now is the time to position for it and buy.

The thesis that there might be a semiconductor rebound in activity in H2 2023 isn’t hard to understand. What we’ve been seeing for a few months is that there’s an attempt to destock (eliminate excessive inventories) in many areas of the market, including PC chips, memory, etc. This might last for 2 quarters more.

During a destocking process, customers buy fewer chips than they’re actually using in their end-customer products. Hence, as soon as inventories normalize, just matching the quantity of chips bought to those incorporated in products shows up as an increase in semiconductor business activity (higher demand for chips). This happens even if end-demand for the products isn’t showing growth. And of course, most expect some growth in end-markets as well, adding to such a dynamic.

All of this makes it “easy” to bet on a semiconductor recovery. So investors and speculators bet. And when it comes to semiconductor, investors treat everything the same — or just bid on ETFs which, themselves, buy the entire industry including Applied Materials.

The Problem

The problem is, Applied Materials isn’t the same as a company producing and selling chips to be incorporated in an end-product. Instead, Applied Materials sells equipment for chip manufacturers to produce chips with. That is, Applied Materials sells additional production capacity to its customers. As I explained in my article titled “Applied Materials Is Not Safe, And The Problem Isn’t China”, this fact creates a very different dynamic for Applied Materials’ business.

Instead of Applied Materials’ business increasing when its customers’ business increases, it only tends to increase by the amount of extra capacity its customers need, to fulfill their end-customers’ demand.

For instance, if a customer sees the need to sell an additional 1000 units in one year, and another additional 1000 units the next year, the semi equipment maker will see 0% growth from one year to the next, even though the customers’ business grew in both years. This is explained in more detail in my previously-linked article. There are exceptions to this, of course, mostly from advanced nodes needing new capacity, as well as productivity increases in old nodes, but the underlying mechanics still dominate.

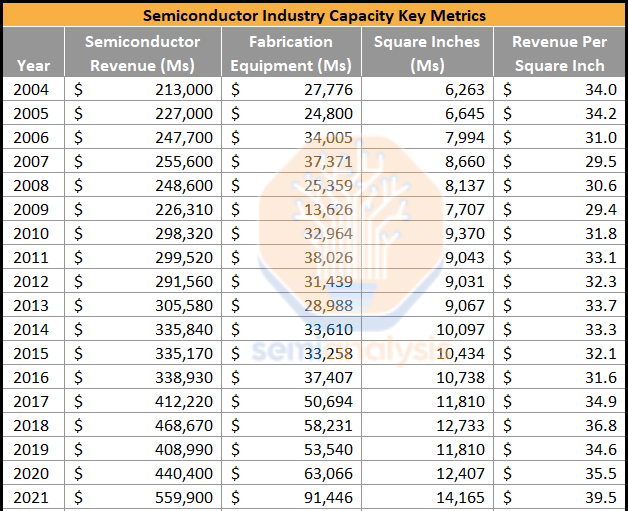

Now, this might all seem too theoretical for my readers. So, I’m going to exemplify it with actual, historical, experience. Below is a nice table published by SemiAnalysis.com (a website I highly recommend for all things semiconductor):

SemiAnalysis.com

Pay attention. There is a very interesting insight to be gleaned from this table. Focus on the 2006/2007 period, and the “Fabrication Equipment” column. You can see the WFE (Wafer Fabrication Equipment) market was $34-$37 billion at the start of this period. Now look down. The market only truly surpassed those values after 2016! That’s 10 years of semi equipment famine!

What could possibly have happened? Look now to the column titled “Semiconductor Revenue”. It goes from $248 billion in 2006 to $339 billion in 2016. That’s 36.9% growth in semiconductor revenues – which created no growth for semi equipment. This perfectly illustrates what I’m saying. It’s fully possible to have growth in semiconductor markets without such growth happening in semiconductor fabrication equipment markets. This tends to happen because during the intervening period, yearly growth in semiconductors never exceeds the largest jump in the past… so capacity additions (what Applied Materials sells) tend to remain smaller than they were at some such growth peak in the past.

Indeed, this is the most likely thing to happen now, especially after a large jump in semiconductor fabrication equipment, such as happened recently. It’s most likely, because this large jump corresponds to a large jump in the capacity to make semiconductors. A jump whose size isn’t likely to be exceeded soon — even though the peak in semiconductor sales will, itself, be exceeded handily like it was in that previous 2006-2016 period. Hence, “not as fast” growth in semiconductors will lead to stagnation or shrinkage for the semiconductor equipment industry. And two things more:

- The large recent jump in semi equipment sales corresponded to an unusual jump in demand for semiconductors following the COVID epidemic. Such a similarly-sized jump in demand is unlikely, even as demand for semiconductors will happily surpass the size of the demand which happened during and after COVID.

- And furthermore, when semiconductor factories reduce capacity utilization (such as now), just going back to prior utilization rates doesn’t even create any additional need for more fabrication equipment. Hence, just going back to “usual rates of production” in H2 2023 won’t even create a need for further semiconductor fabrication equipment, never mind growth.

Chinese Restrictions – Unintended Consequences

Although the ban on selling advanced semiconductor equipment to China has led most companies (including Applied Materials) to reduce their guidance, there are a couple of notable observations to be made:

- First, the initial bans hit US companies harder than foreign ones. Now there’s an attempt to plug this (by extending the ban to other countries), but in the meantime US companies, such as AMAT, will have lost share to foreign suppliers.

- Second, since the ban applied first to advanced nodes and not older ones, Chinese companies actually increased their demand for older equipment. This can produce some (positive) surprises, especially for foreign suppliers. It might also add some temporary demand for US suppliers on older nodes, though, in an unpredictable fashion.

A Final Word On The State Of The Market

In my previous Applied Materials article, I showed how 6 months before, all WFE segments had, in Applied Materials’ earnings call, been deemed to be growing.

Then, I showed how at the then current time, in Applied Materials latest conference call, the memory segment was said to be weak, but all other segments were still growing. I also indicated that this wouldn’t last, and that things would sour for all segments:

Yet, 6 months later, we’re staring at a huge 50% drop in capex commitments for memory production. I think the same “surprise” is going to happen, only slightly later (and to a smaller, but still large, extent) in “logic, foundry and other”. This is for the obvious reason that memory isn’t some kind of product in itself. It’s just something that’s added (and in the same or greater quantities as before) to nearly every other product out there using semiconductors and logic.

Well, two weeks ago, during the Lam Research (LRCX) earnings call, we got validation for my prediction. Lam Research confirmed weakness had spread to all segments (bold is mine):

As we look forward into 2023, however, we see a substantially weaker demand environment and the corresponding need to make prudent changes to our near-term operations and priorities. Customers across all segments are exercising caution, especially those in the memory markets. Inventory levels in both NAND and DRAM remain very high, and customers are not only reducing new capacity additions, but also lowering fab utilization levels to bring excess inventory into balance as quickly as possible. In addition, the U.S. government’s new restrictions on sales of equipment, parts and services for specific technologies and customers in China are further impacting equipment demand in a declining market.

What Lam Research said is likely to be confirmed by Applied Materials when it reports earnings on February 16. Hence, since this is a large change from what Applied Materials said before, we can expect it to come with a revised, lower, guidance (versus consensus) as well.

Conclusion

Based on what I described in this article, I have the following predictions:

- Applied Materials’ activity (as well as that of most of the semiconductor equipment sector) will materially disappoint over several years, given that the high watermark growth rate in semiconductor demand which took place in 2021 will likely not be surpassed for many years looking forward – a situation analogous to what happened between 2006/2007 and 2016. Of note, the size of the semiconductor market will surpass its 2021 level. But the change in demand in a short period over a previous high in demand (2021) won’t exceed what happened from 2020 to 2021 for a long while — and that’s the most important thing which needs to happen for the semiconductor equipment market to clearly exceed its previous 2021/2022 records as well.

- Applied Materials will, in my opinion, guide down below consensus when it reports earnings on February 16th. And this won’t be the last reduction in guidance looking forward, either. This is so because the slowdown in demand has now spread from mostly memory, to all segments.

Given the above and what it implies for future prospects, I believe Applied Materials has to trade at much lower multiples. A cyclical under a durable cyclical downturn typically trades for single-digit peak earnings multiples, not 14-15x peak earnings, like Applied Materials does. Applied Materials is a Sell.

Be the first to comment