Onfokus/E+ via Getty Images

Thesis Summary

Apple, Inc. (NASDAQ:AAPL) has been one of the best-performing tech stocks in the last year. While the likes of META (META) and Alphabet (GOOGL) have seen their share price fall by over 60% and 30%, respectively, over the last year, Apple is down a mere 1% in the last 12 months.

Investors seem to have fled into the “safety” of Apple’s balance sheet and more predictable earnings, but I don’t think this situation will last. The company is now significantly overvalued compared to peers, and the next earnings will show what we all already know, that we are heading or already in a recession.

With that said, Apple is still a long-term hold, as it has numerous levers it can pull to increase growth and profitability.

The Apple Bond

In times of turmoil, investors flee to what they perceive as safer assets, and Apple has gained this perception amongst investors. The company is a well-established international brand with diversified revenue streams and an impenetrable moat. There is only one Apple, and though there are other phones in the market, the iPhone creates its own demand.

For this reason, Apple is comparable to high-grade investment bonds and even pays out a modest dividend of around 0.6%. And on top of that, the company boasts a strong balance sheet:

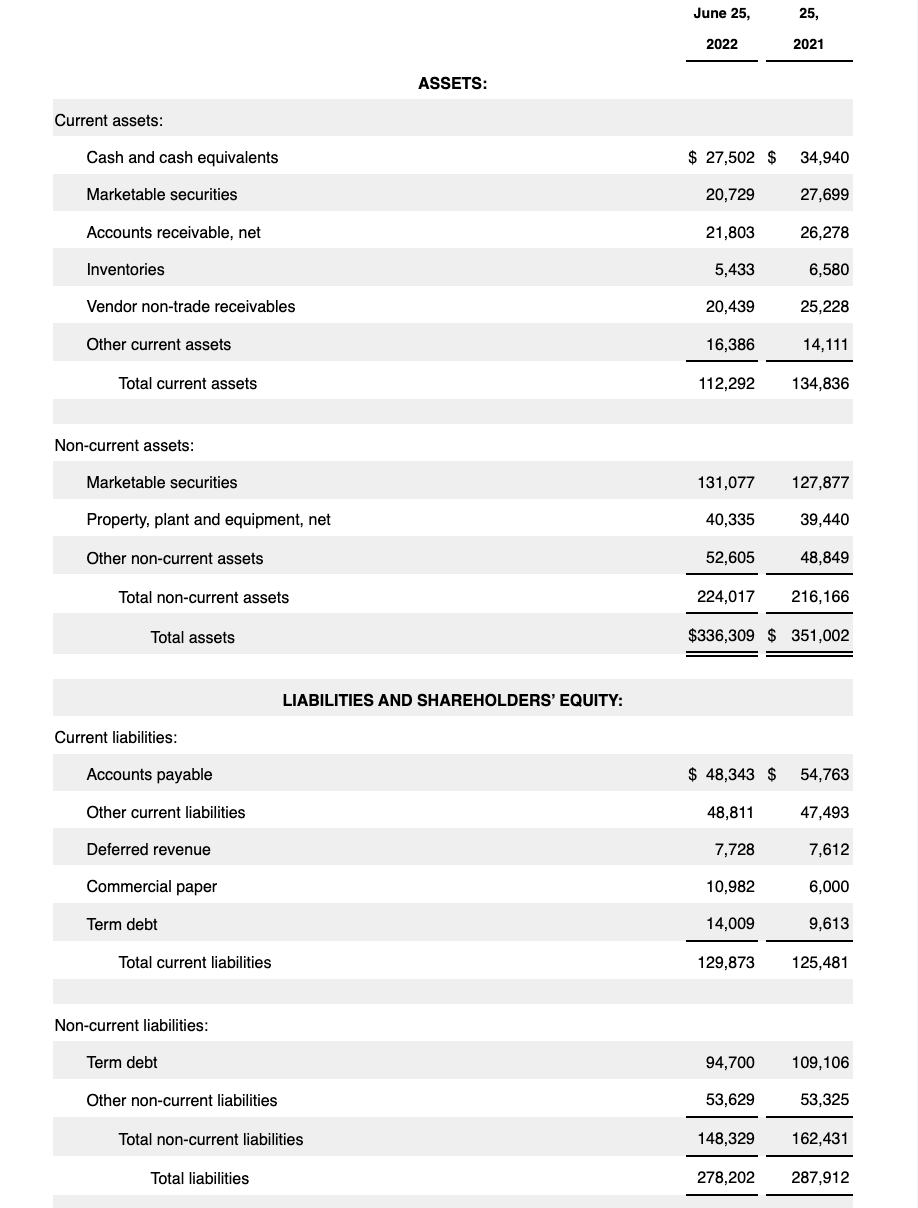

Apple Balance Sheet (10-Q)

Apple has over $330 billion in assets, which is around 20% more than its total liabilities. What’s more, the company has $27 billion in cash and another $20 in marketable securities.

With those numbers and its long track record of profitability, it’s not surprising that risk-averse investors are happy to park their money in Apple. However, and though I still hold some Apple shares myself, I believe the company will see new lows in 2023.

The Earnings Recession Is Just Starting

It’s a well-established fact that the Federal Reserve’s policies take between 6-12 months to have a real effect on the economy. In 2022, we have seen valuation multiples contract as liquidity has been sucked out of the system. In 2023, I expect we may finally see the effects of higher rates in the real economy.

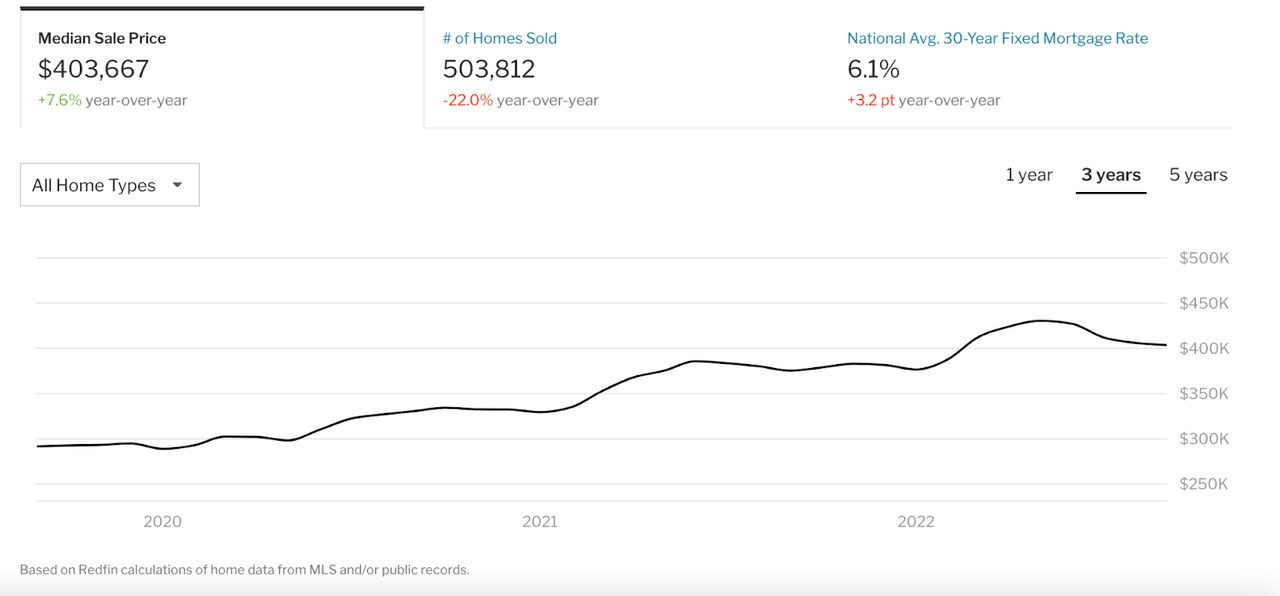

The first sign of this is the cooling down housing market:

Housing Price in USA (Redfin)

The chart above shows median house prices in the USA, which peaked back in May, according to Redfin. We can also see that the number of houses sold is down significantly.

The other red flag we are seeing now is the slow-down in Job creation. Though top-line numbers still look good, with a 3.7% unemployment rate, the rate of employment creation is slowing down. Also, in October, annual wages grew at their slowest rate in over a year, and the employment-to-population ratio for prime-age workers fell significantly.

The foundation of the labour market strength story fades a little when you pull back the tarp and look more closely at the details. The report to us looks like payroll jobs growth will falter in coming months as companies batten down the hatches as the Fed continues to take away the economy’s punch.

Source: Christopher Rupkey, chief economist at FWDBONDS in New York.

Over the past year, we have seen the effect of multiple contraction in the market, but over the past month, we have seen the effect of lower earnings, which I expect will continue into 2023, and I don’t think Apple will be able to escape it.

Ultimately, Apple makes most of its revenues from selling high-end phones and hardware, and it depends on the strength of consumer spending. On top of that, Apple continues to face Supply chain issues, and JPMorgan has already revised iPhone shipments downwards for the holiday quarter.

Comparative Valuation

Apple has held up so well in recent months that it is now overvalued compared to some of the other large tech companies.

|

AAPL |

GOOGL |

META |

TSLA |

|

|

P/E GAAP (TTM) |

24,27 |

18,98 |

10,86 |

58,86 |

|

Price/Sales (TTM) |

6,10 |

4,46 |

2,63 |

7,91 |

|

PEG Non-GAAP (FWD) |

2,21 |

1,11 |

4,84 |

1,45 |

|

Price to Book (TTM) |

46,65 |

4,89 |

2,45 |

15,13 |

|

Price/Cash Flow (TTM) |

19,31 |

13,35 |

5,60 |

37,61 |

Many other factors are coming into play here that separate Apple from Alphabet, Meta and Tesla, Inc (TSLA) but I don’t think they justify Apple’s current overvaluation.

The company has a much higher P/E than GOOGL and META, and a P/S ratio comparable to Tesla, which is growing at a rate of 50%. The PEG is twice as high as Google’s, which is my favorite stock.

Worst of all, Apple has a crazy high Price to Book ratio and is much more expensive than GOOGL and META when we look at cash-flows.

So what’s the rationality behind owning Apple right now? Sure, there are some compelling reasons to hold long-term, but it seems like there are much better bargains out there.

Other Considerations

While I expect Apple to suffer in the next few months, I concede that there are many long-term things to be excited about. Namely, the fact that Apple is expanding beyond the sales of phones into services like Apple TV and the Apple Card.

In fact, a recent press release by Apple stated that iPhone users will soon be able to receive interest on their Apple card funds. This could be a huge money maker for Apple in the future. Even if iPhone sales go down this year, the Apple ecosystem is here to stay, and as our lives become more integrated with technology, Apple will find new ways of monetizing its consumers.

Final Thoughts

In conclusion, though I like Apple, I think the company is set to make lower lows in the coming months due to weaker consumer demand. With that said, I will be using that opportunity to add more shares.

Be the first to comment