Marina Demeshko/iStock via Getty Images

The iShares Core Growth Allocation ETF (NYSEARCA:AOR) is a great example of an ETF that arguably shouldn’t exist. While it’s supposed to be passive, it’s so much so that it in turn holds ETFs, and some of the most diversified ones. The costs of this ETF are higher than the average expense ratios of its constituent parts, and is an inefficient way to establish a bond and stock exposure. Nonetheless, we think investors are right to be looking for other ways to go long the market.

Issues With AOR

Let’s have a quick look at what’s inside AOR.

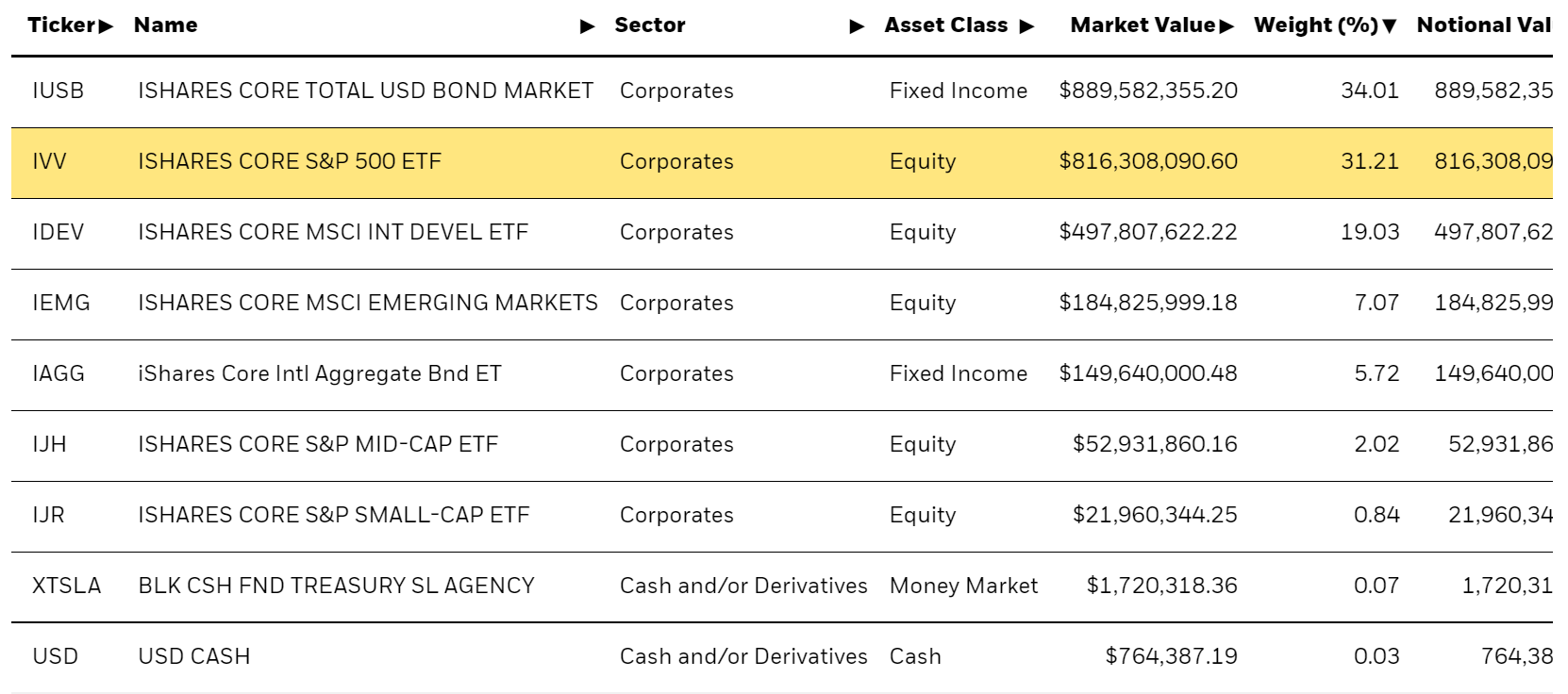

Top Holdings (iShares.com)

AOR just contains other ETFs, the most vanilla ones you could possibly imagine. At 34% is the iShares Core Total US Bond Market (IUSB) and at 31% there is the iShares Core S&P 500 (IVV).

Firstly, you cannot just invest randomly in a broad bond exposure, because in a rate volatile environment you need to account for duration. The IUSB is high duration, meaning sensitive to rate increases. In our view the IUSB may not be so bad given that rates have come up and have been the cause of the discount to both long duration bonds and stocks, given that we believe there will be a reversal. Still, the IUSB carries an opinion on rates, and when going long that opinion is that rates are going to fall.

But the bigger problem with AOR is the expense ratio at 0.15%. It’s not high, but when you look at the expense ratios of its top two largest components, they’re 0.06% and 0.03% respectively. They average at much lower than 0.15%. AOR is relatively expensive then, and it would be cheaper to just buy each of the components in more or less a 50:50 ratio to imitate the exposure. There is certainly no meaningful active component between the stock and bond exposure that I would trust from AOR.

Economic Remarks

However, going long on the US economy is not necessarily ill-advised. There is a strong cumulative argument for starting to build a long position.

- Once we start lapping early 2022 figures, inflation is going to look a lot lower.

- Rents are coming down, which are a dangerous trigger for the wage price spiral when at too high levels.

- Energy prices and commodity prices have come down as Europe slows on supply chain issues, meaning it’ll fold its economy sooner than the US and break the fall for the US as headline inflation eases.

- Real wages are shrinking, again signaling little wage-price spiral risk.

- Market moving categories like tech are beginning to experience record levels of weak performance.

With the rate hikes premised on wage-price spiral risks, once those risks are settled rates can start coming down and markets up.

Of course, things can go wrong. Chinese wallet matters a bit for US companies, and it may not be a useful growth sink anymore as they deal with a tricky reopening. This is a demand side concern. On the other hand, there are still questions around the war in Ukraine. Disruption to grain supply and other resources could be a problem, as well as escalation of the war, which would meaningfully change market narratives if anything akin to a nuke is used. It’s a dangerous market, but things are going to start looking up soon, hopefully with some momentum if nothing goes wrong.

Thanks to our global coverage we’ve ramped up our global macro commentary on our marketplace service here on Seeking Alpha, The Value Lab. We focus on long-only value ideas, where we try to find international mispriced equities and target a portfolio yield of about 4%. We’ve done really well for ourselves over the last 5 years, but it took getting our hands dirty in international markets. If you are a value-investor, serious about protecting your wealth, us at the Value Lab might be of inspiration. Give our no-strings-attached free trial a try to see if it’s for you.

Be the first to comment