imaginima

The commodity business is often like a game of chess where the person who wins is usually the one who “made the second last mistake.” Antero Resources Corporation (NYSE:AR) has had their fair share of decisions that management wished they never made. But it is clear that some decisions have dominated to build a very successful and large business.

I worked in the commodity food business for much of my working years. Many managements were called “lucky” by commenters and articles. Rarely were they called “good.” That is because there is ample opportunity to mis-guess the future and many focus upon those missteps. Instead, the focus should be upon reasonable projections with a habit of being right more than wrong.

For example, when I first followed Antero Resources Corporation, it was hedged roughly five years in advance. This benefitted the company immensely when natural gas prices unexpectedly declined for a far longer period than anticipated. Such a stance could have easily cost dearly had that price decline not happened. Instead, management raked in literally billions of dollars in hedging dollars as sales prices declined (as I wrote about this through the years).

There is also the decision to have more connections to pipelines out of the basin for better pricing. Now, the cost of this was charges for unused capacity that could not be sold. But there were profitable periods like winter storm Uri that appear to have justified such a strategy.

Going Forward

All of this and more appears to have left the company in the following position.

Antero Resources Current Market Pricing Strategy And Industry Position (Antero Resources December 2022, Corporate Presentation)

Management has positioned themselves to take advantage of a very strong commodity price market. Antero Resources Corporation long ago focused upon a liquids-rich strategy that much of the industry now embraces. When earnings come out on February 15 post-market, this is not likely changing materially.

Even more important was the ability of management to get superior pricing that has persisted throughout the time I followed this company. The interesting thing about the pricing policy was that it gave the company a persistent margin advantage that allowed the company to do reasonably well even during times of hostile commodity prices.

Many companies focused upon cost-cutting and operations optimization. But it appears that the technology advances did not produce the margin advantages that the marketing strategy produced as shown above. This management did manage to keep up with technology advances. But the clear emphasis has always been on prices received. That is a very unusual strategy throughout the industry.

Interestingly, getting a premium price can lower a company’s breakeven point for the benchmark prices just as effectively as low costs. In this case, the company receives such a commanding premium that it had decent cash flow ever since it went public even if that cash flow came from non-traditional sources (like taking the midstream business public and periodically cashing in hedges).

Now the cash flow is very traditional. But it has the benefit of all that forward thinking. Managements that think ahead in the past tend to keep doing that. Not only that, but such managements are rare and, therefore, hard for the market to evaluate.

Most companies that I follow take whatever price is offered in the area. The idea that another market or basin would have superior pricing is rarely, if ever, discussed. Here you have an early ability to export commodities that much of the industry is now rushing to do. I repeatedly report that companies will benefit from stronger world prices in the future for a lot of companies. But this company already benefits from it.

What is even more interesting is that when management does hedge, they will still send natural gas and other products to a stronger market, pay the hedges and pocket a couple of pennies difference on the margin.

Shareholder Alignment

But Antero Resources Corporation management does not stop with marketing. They have found other ways to save a lot of money for shareholders.

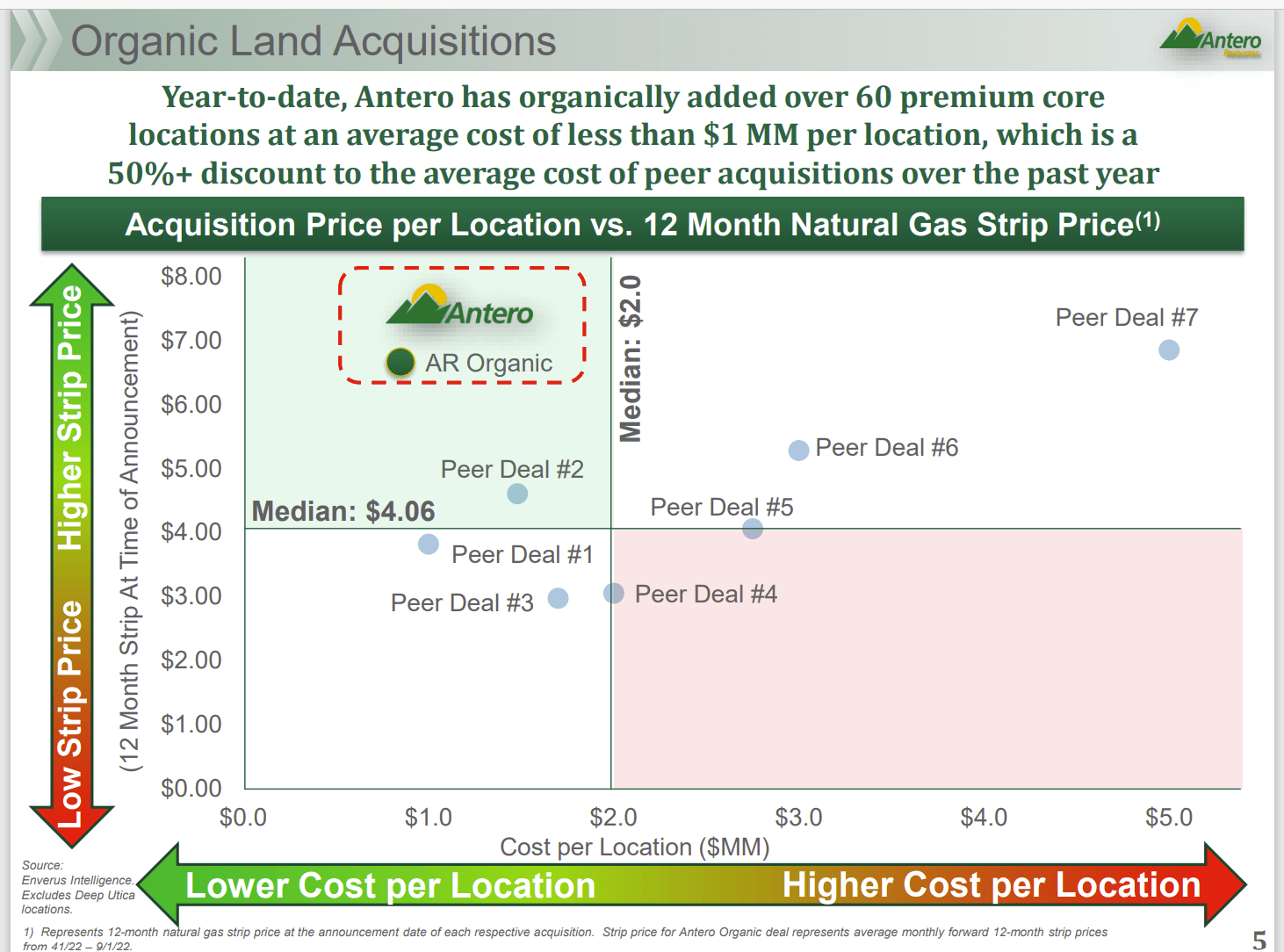

Antero Resources Land Acquisition Strategy And Acreage Deal Costs (Antero Resources Third Quarter 2022, Earnings Conference Call Slides)

This management has engaged in a tedious strategy that is almost “guaranteed” to save a lot of money. Management is purchasing mostly “bolt-on” acquisitions. Each acquisition is usually suboptimal as a standalone holding. So, it is not worth much to any competitive buyer. It is worth something to Antero Resources management because they combine these purchases either with company holdings or into larger plots that are more valuable. The larger property can often allow for more profitable drilling and midstream servicing than a smaller lot.

Far more important is the location cost of this strategy. As shown above, it can rarely be beat. Rarely is the location cost ever part of the breakeven that management presents to shareholders. Now since the location cost is a sunk cost, it is not a proper cost in the decision to drill or not drill. However, it is part of the corporate profitability. Even if that cost is paid in cash or with stock, that cost still needs to be recovered in the eyes of shareholders (even if it does not depreciate). Those kinds of costs often show up as a reduced reported profitability percent.

In this case, Antero Resources Corporation management is reporting a cost that can easily be recovered by many wells drilled in the current robust pricing environment. But when that cost climbs past two million dollars per location, then the reduction in company profitability (and likely future growth) is likely to be noticeable when doing a competitor comparison.

Cost Focus By Mr. Market

There is often a lot of “lip service” paid by many managements to “lowest cost” or “lowering costs.” But as shown above, there is so much more to “lower cost” and “lowest cost” when reporting above average margins and corporate profitability. That makes for the difference between “good enough” management and superior management.

Antero Resources Breakeven Location Detail (Antero Resources December 2022, Corporate Presentation)

The breakeven price shown above is dependent upon the prices received for the other products generated from the wells. When those prices were depressed, the breakeven was often $2.30 MCF or even higher, depending upon the situation. Now, it has gone as low as $.50 MCF (depending upon assumptions). So, it is clear that the breakeven discussion depends upon a matrix of prices that constantly change.

It also appears that management in the past has generated a superior margin to many basin operators. That should continue into the future even if the reason for that superior margin is subject to debate. But again, the key in most commodity industries is to be sure the right decisions far outweigh the wrong ones (now and well into the future).

Conclusion

The commodity business moves at such a fast pace, that “right decisions” can look really bad “next week.” Coming up with a strategy that proves to be overall superior throughout time appears to be a rare gift. The key measure is more good than bad, and that has to be all the time. That is what makes commodity such a tough industry in which to compete.

It is, therefore, understandable when management with good inventory decide to just maintain production, pay dividends, keep debt low, and report above-average profits from that inventory because growing a commodity business takes a talent that few possess. Therefore, some managements know a good thing when they have it and just chose to “stand pat” with what they have knowing the market will think they are “good managements.”

Antero Resources Corporation management appears driven enough to keep growing even if that growth will be gradual. There is the gradual addition of acreage as well as the volumes from the joint venture. In addition, margins appear set to expand from the growing ethane market (used in plastics in the green revolution).

The chief risk for Antero Resources Corporation will be the management after the current management retires, because management like this is very rare. But in the meantime, the next years should be like the past, with continued overall outperformance of the industry. That should be very good news to Antero Resources Corporation shareholders.

Be the first to comment