shapecharge/E+ via Getty Images

Conversation with BlackRock’s Fixed Income Portfolio Managers

We met with the portfolio managers of BlackRock Strategic Income Opportunities to have a wide-ranging discussion on their approach and why it’s so well suited to the current market environment.

Rick, perhaps you could please start us off by discussing why you think pursuing an opportunistic and unconstrained fixed income approach is particularly important in today’s market environment, and then afterward we can get into precisely what that approach entails?

Rieder: Sure thing. Well, I think the extraordinary turmoil we’ve seen in the economy and markets over the past few years, and the ability of our unconstrained strategy to both open up additional avenues of return generation during that time, while also protecting client capital on the downside, illustrates well some of its benefits versus an approach that is solely tethered to a traditional benchmark, like the Bloomberg U.S. Agg Index. Let me be more specific: in the past few years, investors have gone from being primarily worried about a growing trade war between the U.S. and China to a multi-year global pandemic that we’re still struggling through and an extremely contentious U.S. election, which held huge policy implications.

Now, most recently, the Russian war with Ukraine and its shock to energy and commodity markets, at a time when inflation was already running hot, has added greatly to investor concerns. Further, as a result of inflationary pressures, we’ve seen a fairly abrupt about-face in developed market monetary policy that has sent markets into more turmoil. Throughout all these events, the prospects for economic growth, labor markets, inflation, and monetary and fiscal policy have gyrated wildly. And it’s in that context that an active and flexible approach to fixed income can be most valuable, in my view, and I’m extremely proud about how our team has navigated these varying crosscurrents.

To better understand the current investment landscape, let’s focus on inflation since it’s largely through these dramatic price increases that we’re seeing the turn in monetary policy reaction function and the recent rise in interest rates. With the Federal Reserve focused on inflation, and the market focused on the Fed, it’s not surprising to see meaningfully elevated volatility across many asset classes in recent months. The fact is that these factors, as well as a loosening of policy in China, could prolong the raw material (cost-push) inflation that has made its way into consumption baskets over the last year.

At the same time, higher wages, which are usually a welcome development for an economy, look to be more correlated to broad prices than they have been in decades, threatening a “wage-price spiral” that could keep inflation hotter for longer. Yet, while wages and prices may be correlated, evidence suggests that causation in recent times is more driven by price than by wage, giving us some comfort that wages won’t cause prices to spiral out of control. At the same time, a common saying in the commodity markets seems to be ringing true again, namely that ‘the cure for high prices is high prices.’ As a result, consumer confidence around durable goods purchases is at the lowest level in at least a decade and aggregate credit card spending on electronic and home goods is down from a year ago.

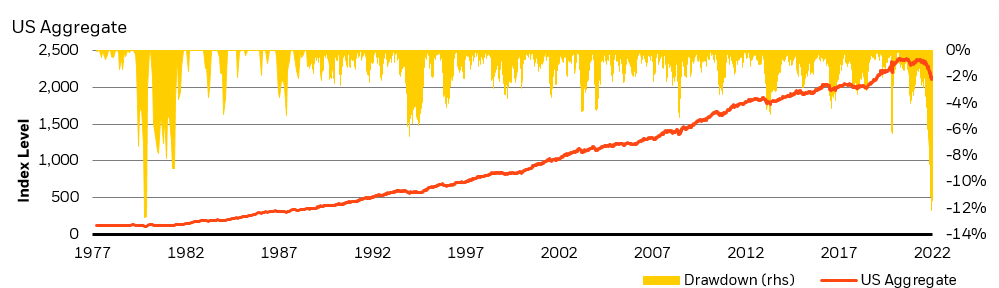

All told, while Fed Funds futures markets are pricing in several policy rate hikes over the next year and a half, or so, it’s not entirely clear the Fed will be able to execute on its plan. In other words, on almost all fronts, we’re witnessing maximum uncertainty. That uncertainty combined with the historically low yields of recent years and the tremendous shocks the market has faced of late (inflation and policy shifts) have led to dramatic drawdowns in fixed income markets (see Figure 1).

Figure 1

For the U.S. Agg Index, only the Volcker shock was greater

Source: Bloomberg, data as of May 16, 2022

In this kind of an environment, the wide-ranging ability of an unconstrained manager to actively adjust duration (interest-rate risk) exposures is particularly attractive. Additionally, volatility in both economic measures and financial markets should provide opportunities for adding more attractive yield to the portfolio, but within a highly risk-aware process that attempts to keep the risks, we take both well-diversified and modestly sized. Indeed, since the inception of our strategy more than a dozen years ago, no single source of alpha has contributed more than 25% to aggregate performance, and over the past decade, our annualized volatility has consistently been below that of the U.S. Agg Index. I’ve emphasized to clients many times that our approach does not rely on taking outsized positions or betting on difficult-to-predict macro moves, but rather on making a little bit of money a lot of times and in that way providing not only a return that hopefully achieves the client’s portfolio goals but via a path that is much easier for them to maintain comfortably. Perhaps Bob would like to flesh out some of the specifics on the process?

Yes, this would be great. Bob, could you tell us a bit more about precisely how the BlackRock Strategic Income Opportunities Fund’s (SIO) approach seeks to attain the goals that Rick has described?

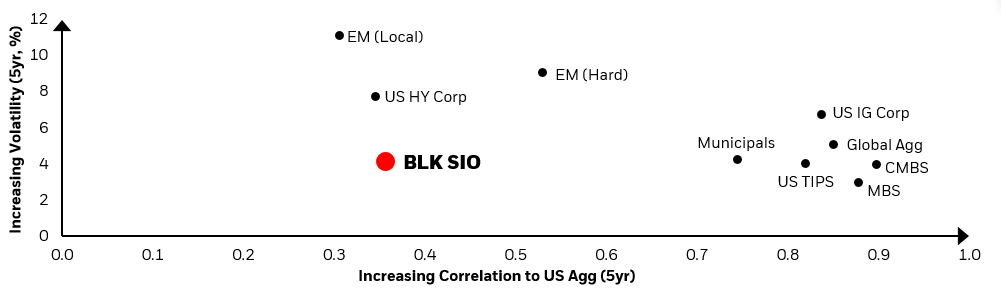

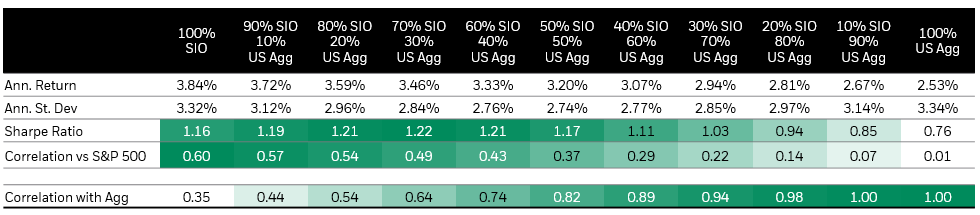

Miller: Of course, at SIO we’re aiming to deliver a consistent, and attractive, risk-adjusted return in all different kinds of market environments, and to do so while maintaining a risk profile that’s analogous to a traditional fixed income investment vehicle. So, to accomplish this goal we utilize an approach that seeks to generate returns from a highly diversified range of fixed income sectors, many of which are outside the purview of most core bond fund managers and are certainly not held in any size within the U.S. Agg Index. By pursuing opportunities throughout the fixed income universe, SIO has historically delivered a return that is diverse, highly differentiated to the Agg index, and further is less volatile than that index (see Figure 2). Also, one of the points that I always make to clients is that we have an extraordinarily well-resourced platform of talent in every subsector of fixed income, globally; and in my experience, it is genuinely best-in-class talent in every portion of the global fixed income markets. Further, in many respects, SIO is the ideal vehicle available to take advantage of that breadth and depth of talent. Said differently, I think one of our “edges” is the platform the firm has allowed us to build over the past decade, and in my view, SIO is the optimal product to utilize that platform.

Figure 2

SIO provides diversification away from the U.S. Agg, with modest volatility

Correlation vs. Volatility

Performance is historical and does not guarantee future results. Data shown is for the BlackRock Strategic Income Opportunities Fund – Institutional Share Class. (Source: Morningstar, data as of April 30, 2022.)

In terms of our process, BlackRock’s SIO strategy combines top-down direction-setting by ourselves, as its portfolio managers, with bottom-up opportunity identification and security selection made by specialists in each sector. Thus, the first step is to determine the current investment regime and establish a macro view of the markets. That view will incorporate a wide range of factors, including interest rates, inflation, labor market conditions, economic growth expectations, and central bank and fiscal policies by country and region, among many other elements. Then, once the aggregate portfolio’s risk level is set, we begin allocating risk across geographies and sectors, based on our macroeconomic views. The sector specialists then draw on that macro view, as well as their own bottom-up credit research, valuation estimates, and expected returns to determine which securities to buy or sell.

In terms of how all this plays out in our current portfolio positioning, as Rick pointed out, we’re facing an extraordinary degree of uncertainty in the macro backdrop today, but one thing we’re reasonably sure of is that it’s important to maintain a defensive posture in rate exposures, relative to tightening central bank regimes around the world. More specifically, as of late we’ve been tactically adding duration at the front and long ends of the yield curve while reducing exposure to the belly of the curve. That has served to reduce top-line duration in the fund since we still think that yields in the U.S. have room to move higher on the back of a hawkish Fed and elevated inflation readings. Further, we’ve reduced the fund’s exposure to non-U.S. sovereign debt, particularly in Europe, as we think the European Central Bank’s (ECB) recent decision to move quicker on tightening made it clear that the central bank will likely take a more hawkish stance than many anticipated.

Also, given the geopolitical concerns that have been top of mind for markets, we’ve also decided to tactically rotate capital across select spread sectors, where we think valuations have become more attractive. Specifically, we’ve modestly trimmed non-U.S. credit exposures, including some Emerging Markets Debt (EM), and have redeployed some assets to our Agency mortgage-backed securities (MBS) holdings, which have reached more attractive valuation levels of late, along with investment-grade corporate credit and U.S. municipal bonds. Finally, we’ve also been holding an elevated level of cash in the portfolio, given the increased volatility we’ve been witnessing in both the rates and equity markets this year, and also because U.S. Treasuries have clearly been a much less effective hedge against risk asset positions this year.

Rieder: Before you ask the next question, I’d just like to elaborate on an aspect of the approach we use that I think is really important. When we talk about establishing a macro viewpoint on the markets, or about allocating risk across different sectors, or geographic regions, it’s easy to lose sight of the fact that this is a tremendously collaborative effort, involving the work of hundreds of analysts, experts, traders and portfolio managers around the fixed income team, and indeed from various other parts of the firm. I’ve been in the money management business for a very long time, but the research, insight, and expertise I routinely encounter here at BlackRock is as impressive as any I’ve seen in this business, and perhaps more so.

In the work that leads up to my monthly markets client call, as well as in the research pulled together for our weekly Investment Strategy Group meetings, the team mobilizes a monumental amount of data and insight, which we discuss at great length to refine our macro outlook. Further, each day members of the team will meet to discuss the latest economic data and market moves, both in the early morning and afternoon, and will meet to discuss portfolio positioning in the context of these recent events. Additionally, we’ll hold periodic deep dives into critical topics we wish to explore further, and we also invite an external macro speaker weekly, to provide their views on markets and the economy. While BlackRock marshals deep resources to provide its investors with an information advantage, we’re also well aware that we won’t have all the answers, so there’s great value in having your views challenged through debate.

Thanks, Bob, for an excellent description of the SIO process/team, and Rick, for your comments supporting the importance of the team that’s been brought together here, and why our collaborative work is vital to the fund’s success.

I’d like to turn now to a question we get a lot regarding SIO, and see what thoughts Dave has about it: Dave, how should we think of SIO in a portfolio context, and how it relates to an investor’s bond portfolio?

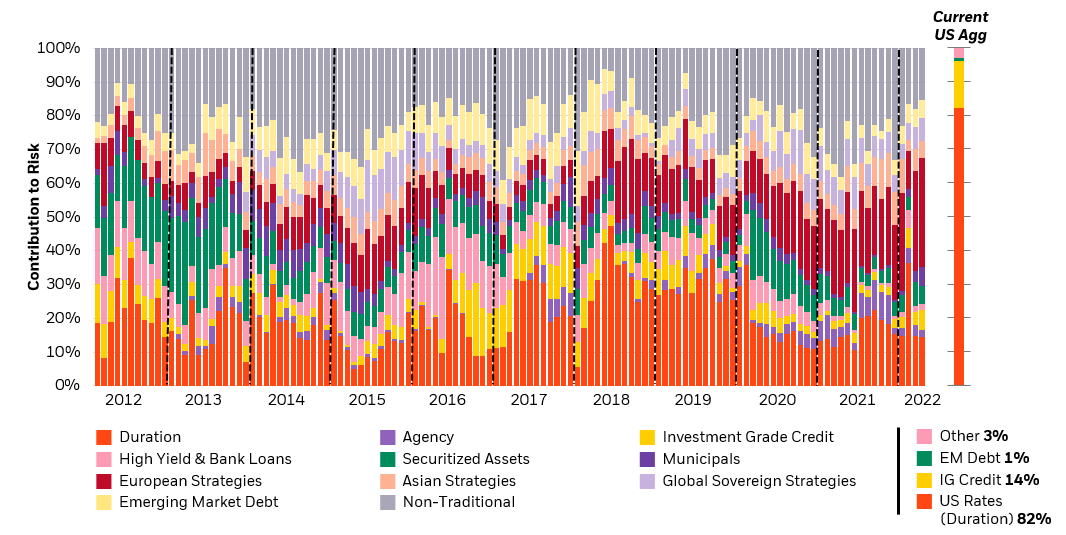

Rogal: Of course, and this is a question we do receive pretty frequently. The fact is that different investor types will own fixed income for different reasons. So, while retirement planners and long-term liability managers often need to take on duration to hedge their long-term liabilities (and may, in fact, welcome some increase in interest rates, as this should reduce those liabilities), they may nevertheless also need a lower-volatility income-producing addition to their portfolios as well. Further, other types of investors might require a liquid, and well-diversified, fixed income strategy that seeks to meet an absolute return target. Historically, the SIO strategy has provided meaningful outperformance versus the U.S. Agg index following the last two times interest rates troughed over the past 10 years, so while timing interest rates can be extraordinarily difficult, taking a structurally more diversified approach to risk (see Figure 3) helps SIO provide a more stable return profile over time.

Figure 3

SIO has the flexibility to adapt to changing markets

Historical contribution to risk by strategy

Source: BlackRock, data as of April 30, 2022

In the current market and monetary policy climate, the ability for an investment manager to actively adjust duration exposure is extremely attractive but equally important is the ability to support an investor’s yield and total return targets and preserve their principal as well. As Rick has discussed in recent calls, there is so much uncertainty in markets today that perhaps an investor’s goal of capital appreciation needs to be balanced with that of capital preservation, at least until more data provides better clarity on the direction of inflation, policy, growth and risk markets. We have considerable data at this stage that suggests that adding SIO to a traditional fixed income portfolio can, in fact, help support both the goals of generating return and mitigating volatility.

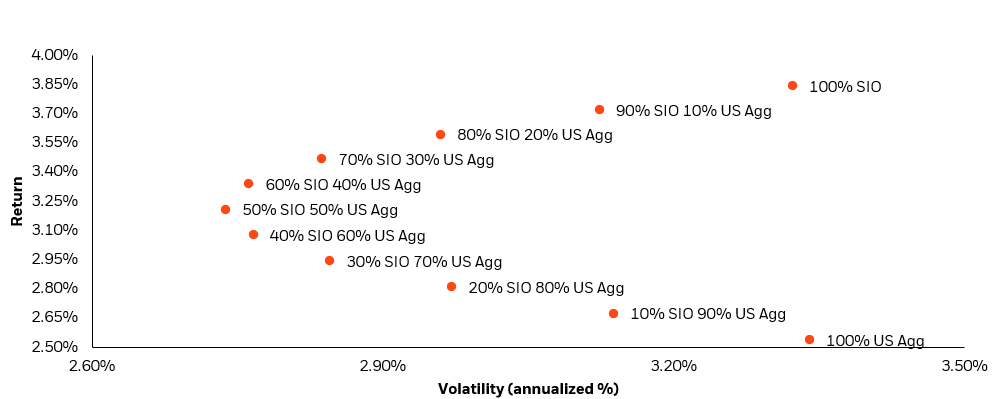

There are therefore several benefits that can be gained by investors pursuing a more flexible and unconstrained approach to fixed income, but of course, we recognize that many investors will want to maintain exposure to traditional fixed income strategies and their attendant index benchmarks. Still, the portfolio-level benefits are illustrated well in the greater than a decade’s worth of data we have in managing SIO and from traditional U.S. bond benchmarks (see Figure 4). In fact, as can be seen in the table, a 60%/40% split between a traditional bond index and SIO, or even a 50%/50% capital allocation between the two strategies, has historically provided improved returns and reduced volatility. Of course, it’s important to not minimize the portfolio benefits of traditional fixed income allocations, which historically have provided hedging benefits versus equity risk, but of course, in the early part of 2022, this was not the case.

Thanks, Dave, and I think that historical lookback brings us nicely to the question of current policy uncertainty, the forward path of interest rates, and why a more flexible approach to fixed income might be particularly important at this point? Bob, your thoughts?

Miller: At a recent International Monetary Fund panel, Chair Powell stated that “there’s something in the idea of front-end loading,” [the policy tightening] and in late March he said: “There is an obvious need to move expeditiously….” These kinds of statements, as well as the fact that the Fed has been running so far behind the curve, suggest to us the desire to bring policy much closer to a neutral stance in short order, in an attempt to gain some traction on the problem of rising inflation.

Chair Powell has signaled the need to move, given the risks of inflation, and most participants have said that they are at least open to being more aggressive with rate hikes. Clearly, the Committee remains committed to fighting inflation. Overall, we think risks remain to the upside, as reflected in the latest Summary of Economic Projections (SEP) as well. The Committee’s views on the economic outlook are also of great interest since now that it is in the process of removing accommodation during a time of considerable uncertainty and risk, revisions to the outlook could have a rapid impact on the anticipated policy path.

Figure 4

SIO can mitigate volatility and enhance return

Adding SIO to a traditional core bond strategy has helped improve return and reduce volatility

This information should not be relied upon as research, investment advice or a recommendation regarding the Funds or any security in particular. This information is strictly for illustrative and educational purposes and is subject to change. This information does not represent the actual current, past or future holdings or portfolio of any BlackRock client. Past performance does not guarantee future results. Calculations using the Institutional share class of fund. (Source: Morningstar, BlackRock as of March, 31 2022, since March 2010 strategy inception of BlackRock Strategic Income Opportunities Fund.)

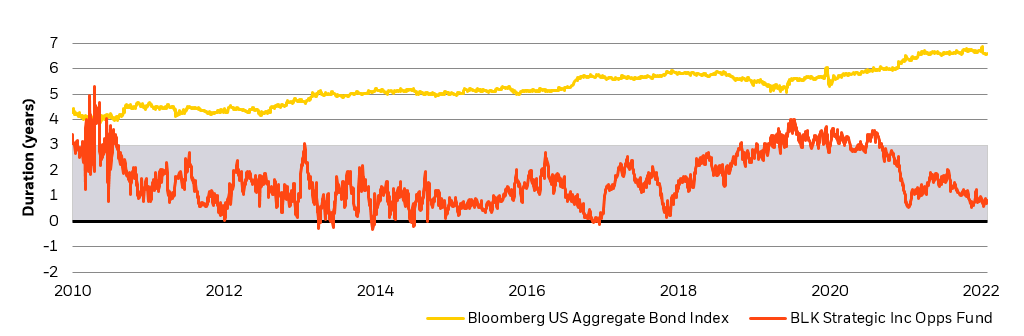

Thus, while it is clear that the Fed has a way to go in a tightening cycle that has only recently begun, the yield curve has already priced in a good deal of this policy work, and as both the European and global economies are slowing, it’s also an open question to what degree the U.S. economy also slows. Again, this suggests to us the importance of being cautious with duration exposures, which have already resulted in a great deal of pain for investors over the past several months. In this context, being able to dynamically adjust the duration exposure of SIO is an incredibly important tool to have available to us and we have certainly used it to the fund’s advantage over the years (see Figure 5).

Figure 5

Flexible duration management in action Duration band:

-2 to +7 years, typically 0 – +3 years

Note: The data is since March 2010, when the Fund’s investment strategy changed. Subject to change. Daily data, March 2010 to April 2022. (BlackRock, data as of April 30, 2022)

Rieder: I agree with all of Bob’s points here, and would only add that the return carnage that we’ve witnessing in high-quality fixed income segments in recent months is due to a combination of very low yields over the last two years and the amount of debt issued at those yields (which provided fixed income markets a historically small cushion to absorb losses), alongside the anticipated tightening of monetary policy. Moreover, a further anticipated tightening by the markets, and/or unexpected withdrawals of liquidity by central banks could potentially make these drawdowns even worse, underscoring the importance of maintaining a defensive posture on duration for the time being.

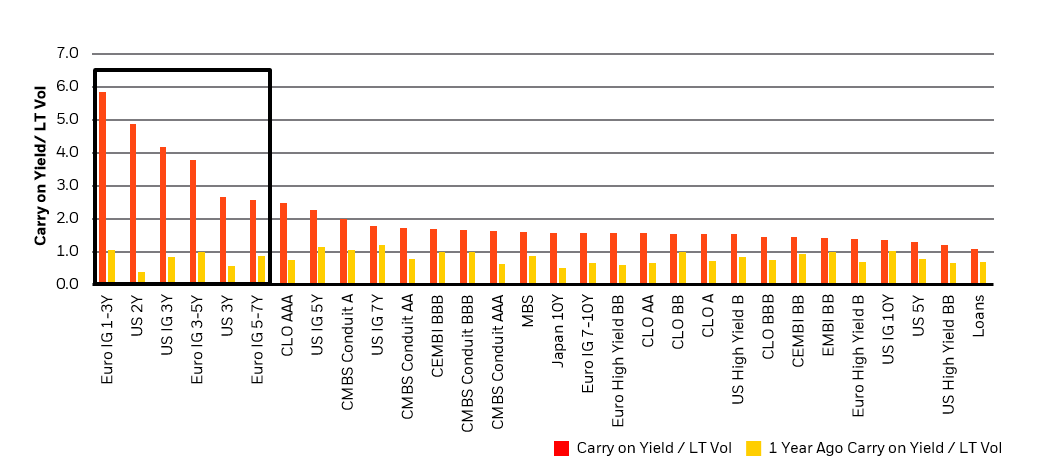

Where then, one might ask, in the capital stack is best suited for a portfolio to balance the need for capital preservation and still some appreciation potential? We would suggest that there are some shorter-duration assets, with some solid yield embedded in them today that have also priced in an awful lot of Fed tightening (see Figure 6). In fact, a set of higher-quality assets today exhibit a carry/volatility profile that suggests they would need to see a -2 standard deviation move in markets to wipe out their carry (assuming a normal distribution), which implies a 95% probability of a positive return over the year ahead. In our view, this looks pretty good in this environment, which is particularly the case at this time of great uncertainty.

Figure 6

After an extraordinary re-pricing, front-end sovereign and high-quality credit assets offer interesting carry

Index returns are shown for illustrative purposes only. It is not possible to invest directly in an index. Past performance is not indicative of future results. (Source: Bloomberg, data as of May 16, 2022.)

Thanks, Rick, Bob, and Dave for a great conversation today, and I think you’ve provided a great argument for why considering a flexible and opportunistic fixed income strategy is of ever-greater importance in today’s market environment.

Annualized Performance

Sources: BlackRock and Morningstar. Data as of March 31, 2022

Performance data shown represents past performance which is no guarantee of future results. Investment returns and principal values may fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than that shown. All returns assume reinvestment of all dividend and capital gain distributions. Refer to blackrock.com for current month-end performance. Institutional shares have limited availability and may be purchased at various minimums. Please see the fund prospectus for more details.

Total annual fund operating expenses as stated in the fund’s most recent prospectus are 0.88% for Institutional shares. Net annual fund operating expenses (including investment related expenses) are 0.82% for Institutional shares. As described in the “Management of the Fund” section of the Fund’s prospectus beginning on page 52, BlackRock has contractually agreed to waive the management fee with respect to any portion of the Fund’s assets estimated to be attributable to investments in other equity and fixed income mutual funds and exchange traded funds managed by BlackRock or its affiliates that have a contractual management fee, through June 30, 2023. In addition, BlackRock has contractually agreed to waive its management fees by the amount of investment advisory fees the Fund pays to BlackRock indirectly through its investment in money market funds managed by BlackRock or its affiliates, through June 30, 2023. The contractual agreements may be terminated upon 90 days’ notice by a majority of the non-interested directors of the Fund or by a vote of a majority of the outstanding voting securities of the Fund.

This post originally appeared on the iShares Market Insights.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Be the first to comment