FG Trade

Some nights are made for torture, or reflection, or the savoring of loneliness.”― Poppy Z.Brite

Today, we are going to take an in-depth look at a small cap name whose stock looks beyond dirt cheap on the surface. However, the company has a couple of significant issues that prevent consideration for a large stake at the moment. This is especially true given the uncertainty and volatility of the overall markets at the moment. However, the shares seem worthy of a small ‘watch item’ holding and make a decent covered call candidate as well. An analysis follows below.

Seeking Alpha

Company Overview:

Amneal Pharmaceuticals, Inc. (NYSE:AMRX) is a Bridgewater, New Jersey-based producer and marketer of generic and branded specialty drugs with manufacturing operations in the U.S., India, and Ireland. The company’s portfolio contains more than 250 generic medicines and ten specialty pharmaceuticals, encompassing a broad spectrum of delivery systems and dosages. Amneal was formed in 2002 and went public when it merged into publicly-traded Impax Laboratories in 2018, with its first trade transacted at $17.00 per share. Its stock trades around $2.25 a share, equating to a market cap of approximately $680 million.

The company is capitalized by two classes of stock. The 151.4 million publicly-traded Class A shares bestow economic interest and one vote per share. The 152.1 million privately-held Class B shares bestow no economic interest, one vote per share, and are transferable into Class A shares.

Operating Segments

Amneal splits its operations into three segments: Generic; Specialty; and AvKARE.

May Company Presentation

The company’s Generic division is one of the top five domestic retail generic manufacturers in terms of prescriptions written, featuring over 225 meds. It also features 25 injectable products and plans to enter the biosimilar market in 4Q22 with the launch of three oncology products that should collectively generate peak sales of $200 million. With an increasing focus on more complex, higher barriers to entry generics (i.e., away from oral pills), Amneal launches approximately 25 to 30 products annually and expects to launch another ~40 injectables between 2022 and 2025 – the latter aided by a $93.0 million acquisition of a manufacturing facility in India in November 2021. Generic currently derives more than half its revenue from the sale of endocrine and central nervous system meds. It generated 1H22 operating income of $167.7 million on revenue of $672.9 million, or 65% of total.

May Company Presentation

Specialty consists of ten approved products mostly in neurology and endocrinology, including recently acquired ($84.7 million in 4Q21) and launched (2Q22) Lyvispah (baclofen) oral granules for the treatment of muscle stiffness, spasms, and pain arising from multiple sclerosis. On August 31, 2022, Amneal submitted an NDA for IPX203, an oral formulation of carbidopa/levodopa that is part granules and part extended-release levodopa-coated beads. The novel delivery system is designed to increase ‘on’ time in Parkinson’s Disease patients without dyskinesia (movement disorders). This technology is already employed in another one of its Parkinson’s drugs (Rytary), which delivered 1H22 net sales of $83 million. If approved, IPX203 will provide Amneal with its biggest opportunity in branded specialty, with peak net sales estimated at $300 million to $500 million. The company anticipates this segment to be a key source of future growth, launching at least one branded new drug per year through 2026. Specialty provided Amneal with 1H22 operating income of $25.6 million on net sales of $184.6 million, or 18% of total.

AvKARE came courtesy of two acquisitions near the onset of FY20 in which Amneal received 65.1% ownership interests of AvKARE and R&S Northeast for an aggregate purchase price of $294 million. The former provides pharmaceuticals, as well as medical and surgical products to government agencies, while the latter is a national wholesale distributor of meds and medical supplies to institutional customers in the U.S. The segment generated 1H22 operating income of $4.2 million on net sales of $170.7 million or 17% of total.

Approach & Marketplace

As stated previously, Amneal is trying to pivot away from low-margin, oral-pill generics to more complex generics, injectables, biosimilars, and specialty meds to provide it with a more stable base for top-line growth and better gross and EBITDA margins – the latter of which it hopes to increase from ~23% in FY22 to ~27% longer term. Although its generic segment revenue split is ~50/50 in terms of oral solids/non-oral solids, its pending abbreviated new drug application (ANDA) filings reflect 57% non-oral solids, and its pipeline currently consists of 87% non-oral solids. That said, retail generics and institutional injectables are slow-growth opportunities with a total domestic market size of $24.7 billion in FY21 that is only expected to increase to $27.0 billion by FY25, meaning Amneal will have to expand market share for these lines to be sources of growth. To that end, injectables’ net sales are expected to surge 35% to ~$170 million for the company in FY22.

May Company Presentation

By contrast, biosimilars represent a significant growth opportunity. Depending on the report referenced, biosimilar sales were anywhere from $13.0 billion to $27.5 billion in FY21 and are expected to grow at a mid-teens CAGR throughout the decade. Like its first three biosimilars, the company will continue to in-license to get a toehold in the market, after which it expects to become vertically integrated with U.S. manufacturing capabilities.

May Company Presentation

The neurology and endocrinology specialty pharma opportunity is expected to accelerate from $6.7 billion in FY21 to $8.5 billion in FY25, with IPX203 representing the best peak sales opportunity in the company’s pipeline.

The market size for selling meds and surgical supplies to government agencies is not an area of meaningful growth, only expected to expand from a $2.1 billion opportunity in FY21 to a $2.3 billion market in FY25. The acquisitions that provided Amneal an entrée into this market are frankly head-scratching.

May Company Presentation

Amneal generates no revenue internationally but is expected to enter China in early 2023, with Europe and India expected to follow.

May Company Presentation

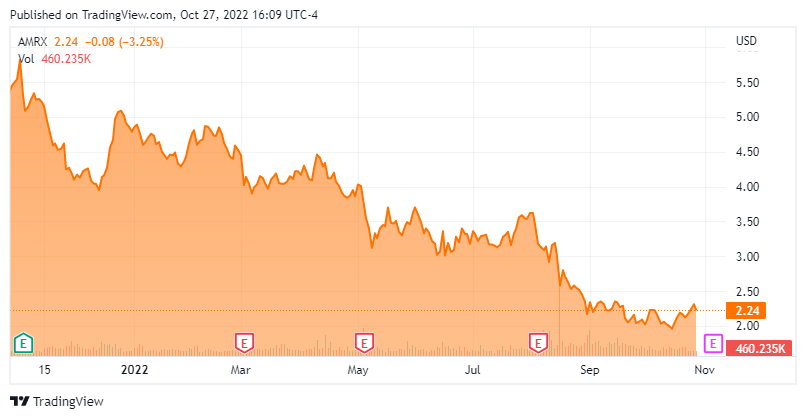

Stock Price Performance

When the Impax-Amneal merger closed in 2018, management foresaw double-digit annual growth in non-GAAP earnings, Adj. EBITDA, and net revenue over the subsequent three years based on already filed new product launches. Additionally, at the deal’s consummation, the combination had net leverage of 4.0 with a longer-term target guided to ~3.0, which was to be achieved partially from $200 million of deal synergies by year 3. However, none of these forecasts came to pass. After earning $0.98 a share (non-GAAP) and Adj. EBITDA of $584.1 million on net revenue of $1.86 billion in FY18, Amneal is now expected to earn $0.68 a share (non-GAAP) and Adj. EBITDA of $510 million on net revenue of $2.2 billion in FY22 (based on range midpoints). Keep in mind that the FY22E top-line figure is boosted ~$400 million to reflect the addition of AvKARE. Furthermore, based on its most recent guidance, leverage based on FY22E Adj. EBITDA is 5.3, with a longer-term target now set at 3.5. Not surprisingly, Amneal’s stock has sold off 92% from its all-time intraday high of $24.35 in August 2018 to an all-time closing low of $2.04 on September 27, 2022. There is one other reason for this dreadful performance, which will be addressed shortly.

2Q22 Earnings & Revised Outlook

The most recent guidance was provided as part of the company’s 2Q22 financial report on August 5, 2022. Amneal reported earnings of $0.19 a share (non-GAAP) and Adj. EBITDA of $134.6 million on net revenue of $559.4 million versus earnings of $0.23 a share (non-GAAP) and Adj. EBITDA of $142.9 million on net revenue of $535.1 million in 2Q21, representing declines of 17% and 6% and an increase of 5%, respectively. Although the earnings were essentially in line with Street expectations and net revenue represented a fairly significant $24.6 million beat, management was compelled to lower its FY22 non-GAAP earnings forecast from $0.83 a share to $0.68 a share and its Adj. EBITDA outlook from $550 million to $510 million (based on range midpoints) while maintaining its net revenue projection at $2.2 billion. The revisions were blamed on an accounting policy change for R&D milestone payments ($15 million hit to Adj. EBITDA) and a delayed launch of anti-viral Ritonavir ($25 million).

Litigation Risk

Amneal exited 2Q22 with concerning net leverage of 5.4. Part of the rise was attributable to money set aside in the quarter as a down payment on a $262.8 million settlement that ends a nearly decade-long legal case arising from Impax anticompetitive practices regarding pain med Opana ER. The company paid $100 million in 2Q22 and will render another installment of $31 million in 4Q22, with the balance split between FY23 and FY24. However, the legal headaches don’t end there. With Amneal deriving some of its top line from the sale of opioids, it has been named as a defendant in 119 state and 915 federal cases regarding their sale. Additionally, it is entangled in metformin lawsuits. Based on its balance sheet, Amneal has set aside $112.5 million as a contingency for these yet to be settled trials. However, until settled, a cloud of uncertainty will continue to menace it and its stock.

Balance Sheet & Analyst Commentary:

The company exited June 30, 2022, with cash of $92.0 million and debt of $2.78 billion (not including legal liabilities for which the company has $275.3 million stashed). Most of the debt – $2.6 billion specifically – matures in May 2025 with half fixed at 4.905% and the balance floating at LIBOR + 3.5%. It also has an untapped revolver of $350 million that can be increased up to $500 million.

Although seven analysts follow Amneal, only Goldman Sachs and Barclays have rendered commentary in the past year, respectively reiterating buy and outperform ratings and lowering price targets from $4.50 to $4 in August 2022 and from $8 to $7 back in April 2022. Overall, there are two buy and two outperform ratings against one hold and one underperform. On average, they expect Amneal to earn $0.83 a share on revenue of $2.31 billion in FY23, representing 20% and 5% improvements over FY22 estimates, which are essentially the company’s guidance from the 2Q22 report.

Verdict:

Amneal is trying to transform itself from a generic pill company to one that manufactures injectables, complex generics, biosimilars, and specialty pharmaceuticals – products with higher gross margins that are less susceptible to price erosion. From an operational standpoint, this transformation is obviously taking place; from a financial perspective, it seems as if the company is running in place. However, near $2 a share, the valuation becomes more compelling. It is trading at a microscopic PE of around 2.5 based on FY23E EPS and a price-to-FY23E sales of under .3. Debt and leverage are a concern, but with an EV/FY22E Adj. EBITDA of 6.8, Amneal’s share price also represents solid value on that metric as well. As such, with expected biosimilar and specialty pharmaceutical launches over the next twelve months expected to generate peak sales of $700 million, this small cap concern appears worthy of a small investment at current trading levels.

Cowards make the best torturers. Cowards understand fear and they can use it.”― Mark Lawrence

Be the first to comment