Michael Vi

A biotechnology pioneer grown to a $145 billion cap Big Pharma, Amgen (NASDAQ:AMGN) is established as one of the 30 stocks comprising the Dow Jones Industrial Average index. Prior to 2022, there were no major changes to its commercial lineup since the last portfolio coverage except for the $13.4 billion acquisition of worldwide rights to Otezla in 2019. Sadly, with $2.20 billion sales in 2020 and $2.25 billion in 2021, the company has yet to reach the halfway point of breaking even and will be fortunate to notch $2.30 billion for 2022. However, two key acquisitions and strong adult and pediatric data for Otezla last year bode well for investors hoping for a boost to Amgen’s topline for 2023.

Otezla is the first and only oral therapy FDA approved in adult patients with plaque psoriasis across all severities (mild, moderate and severe). Two positive Phase 3 trial results were presented in September. The 16-week SPROUT study of pediatric patients aged 6 to 17 years with moderate to severe plaque psoriasis inadequately controlled by or intolerant to topical therapy met its primary endpoint (“PEP”) of Physician’s Global Assessment (sPGA) response, which was higher in the Otezla group compared to placebo (33.1% versus 11.5%; P<0.0001). Similarly, the 16-week DISCREET study in adult patients with moderate to severe genital psoriasis achieved its PEP with greater responses in the Otezla group on the sPGA of Genitalia scale (38.7% vs 19.1% for placebo; P=0.0003). If regulatory agencies such as the FDA allow these data to be included in the prescribing information, insurance plans will be more likely to cover Otezla than if it was for off-label use. Management believes there might be 1.5 million more patients in the mild to moderate setting after transitioning from the first-line topicals. This is more than double the 700,000 already treated with Otezla, and increased usage could propel it to Amgen’s #2 spot in sales (Table 1).

Table 1. Worldwide net product sales (in millions) for the three months ended September 30, 2022.

|

U.S. |

Rest of World |

Total |

|

|

ENBREL |

$1,086 |

$20 |

$1,106 |

|

Prolia |

590 |

272 |

862 |

|

Otezla |

529 |

98 |

627 |

|

XGEVA |

363 |

132 |

495 |

|

Aranesp |

128 |

230 |

358 |

|

Repatha |

142 |

167 |

309 |

|

KYPROLIS |

217 |

101 |

318 |

|

Neulasta |

205 |

42 |

247 |

|

Nplate |

162 |

126 |

288 |

|

MVASI [Avastin] |

$139 |

70 |

209 |

|

Vectibix |

106 |

141 |

247 |

|

EVENITY |

136 |

65 |

201 |

|

BLINCYTO |

84 |

58 |

142 |

|

EPOGEN |

136 |

136 |

|

|

AMGEVITA [Humira] |

117 |

117 |

|

|

Aimovig |

103 |

4 |

107 |

|

Parsabiv |

61 |

39 |

100 |

|

KANJINTI [Herceptin] |

58 |

14 |

72 |

|

LUMAKRAS |

61 |

14 |

75 |

|

NEUPOGEN |

21 |

14 |

35 |

|

TEZSPIRE |

55 |

55 |

|

|

Sensipar/Mimpara |

4 |

13 |

17 |

|

Corlanor, AVSOLA [Remicade], IMLYGIC, RIABNI [Rituxan] |

80 |

34 |

114 |

|

Total product sales |

$4,466 |

$1,771 |

6,237 |

|

Other revenues |

415 |

||

|

Total revenues |

$6,652 |

||

|

TEPEZZA |

$491 |

$491 |

|

|

KRYSTEXXA |

192 |

192 |

|

|

RAVICTI |

84 |

84 |

|

|

PROCYSBI |

58 |

58 |

|

|

UPLIZNA |

31 |

12 |

31 |

|

ACTIMMUNE |

34 |

34 |

|

|

BUPHENYL |

2 |

2 |

|

|

QUINSAIR |

0 |

0 |

|

|

Inflammation Products |

21 |

21 |

|

|

Total Horizon product sales |

$913 |

$12 |

$925 |

Unfortunately, it is difficult to assess the near-term prospects of TAVNEOS included in the $3.7 billion acquisition of ChemoCentryx. It was last seen generating $5.4 million sales in the first quarter of 2022 and the Q2 earnings call was canceled due to the merger. While also approved in Europe, Vifor Pharma has commercialization rights in markets outside of the U.S. Further down the road, several analysts, Jefferies’ Michael Yee and SVB Securities’ David Risinger, as well as Stifel’s Dae Gon Ha, each gave TAVNEOS a good shot of achieving at least $1 billion in peak sales based on comparisons to other complement inhibitors and likely from the first indication alone. One prevalence estimate puts ANCA vasculitis occurring in 3-4 children per million, meaning a total addressable market of 1,000-1,200 affected individuals in the U.S. If Amgen pegs the wholesale price at $200,000 for a year of treatment, TAVNEOS needs to maintain 500 patients in remission for blockbuster status.

The $27.8 billion acquisition of Horizon Therapeutics was Amgen’s most expensive, and the largest pharma M&A transaction in 2022. Q3 sales of Horizon products are listed above. Horizon had raised guidance of KRYSTEXXA to >$1.5 billion peak sales and ex-U.S. peak sales of TEPEZZA to $1 billion. There were no advanced pipeline candidates from either of those two deals. However, there are 2 ongoing Phase 3 trials evaluating UPLIZNA for myasthenia gravis and for the prevention of flare in patients with IgG4-related disease.

Wall Street currently expects $27.23 billion in revenue for 2023. This is beatable. Amgen won’t be reporting figures for the Horizon products until the deal closes around mid-year, and Horizon’s inflammation segment may be disregarded as all of the agents (PENNSAID, RAYOS, DUEXIS and VIMOVO) face generic competition. However, 99% of Q3 2022 sales came from the U.S., as only UPLIZNA had been approved elsewhere. Amgen should be expected to exert its marketing muscle in Europe, where UPLIZNA was granted a Centralised Marketing Authorization in April 2022. Patients already on the other Horizon products still need to be on it, and because the drugs are for rare diseases, Amgen can afford to absorb the small specialized sales force and their prescriber contacts.

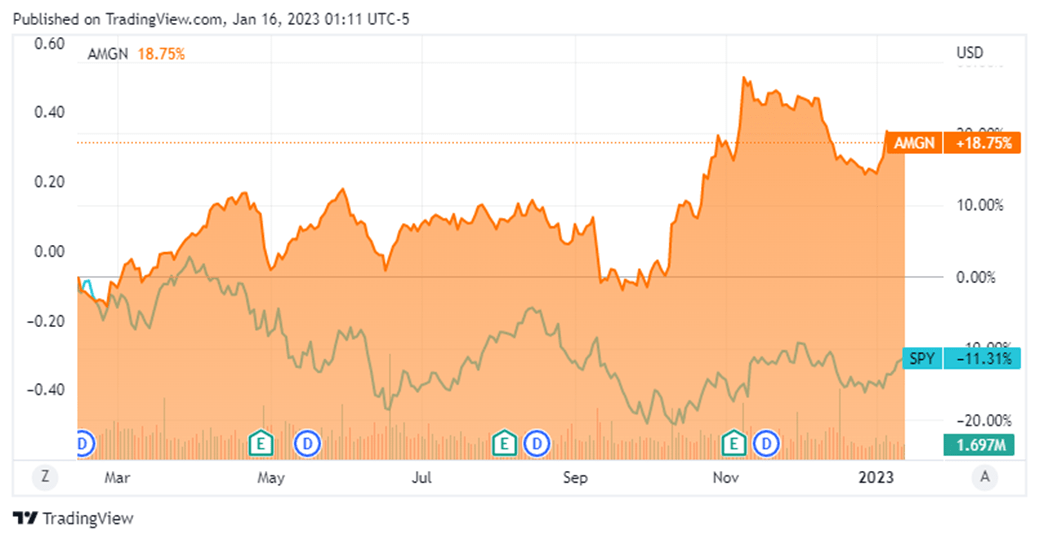

To conclude, Amgen is a good buy as a defensive healthcare sector stock in a bear market, with consistent earnings growth and positive cash flows (a net $2.1 billion in Q3 2022). The stock has handily outperformed the reference SPDR S&P 500 Trust ETF (SPY) the past 52 weeks (Figure 1). The recent mergers and acquisitions add long-term value with 3 potential blockbusters that can be seen to offset the mounting debt that includes a total $4 billion in loans from December. Furthermore, a $2.13 per share dividend for Q1 2023, a 10% increase from the $1.94 paid in each of the previous four quarters, is available to investors who buy shares by the close of business on February 15, 2023. The dividend raise ensures that Amgen will keep its preferred place among Seeking Alpha contributors who like to tout dividend aristocrats.

Figure 1. NASDAQ:AMGN chart by TradingView

TradingView

Be the first to comment