JHVEPhoto

One of the biggest mistakes for investors is to get caught up in market exuberance on a particular stock. This appears to have been the case with a number of big pharmaceutical names in 2022, as investors prized their cash rich and inflation resistant nature, and all the while bidding up their prices.

This includes Amgen (NASDAQ:AMGN), whose share price traded as high as $296 in recent months, before crashing down to its present level, as shown below. In this article, I highlight why this crash presents a good opportunity for value investors to layer into this moat-worthy stock.

AMGN Stock (Seeking Alpha)

Why AMGN?

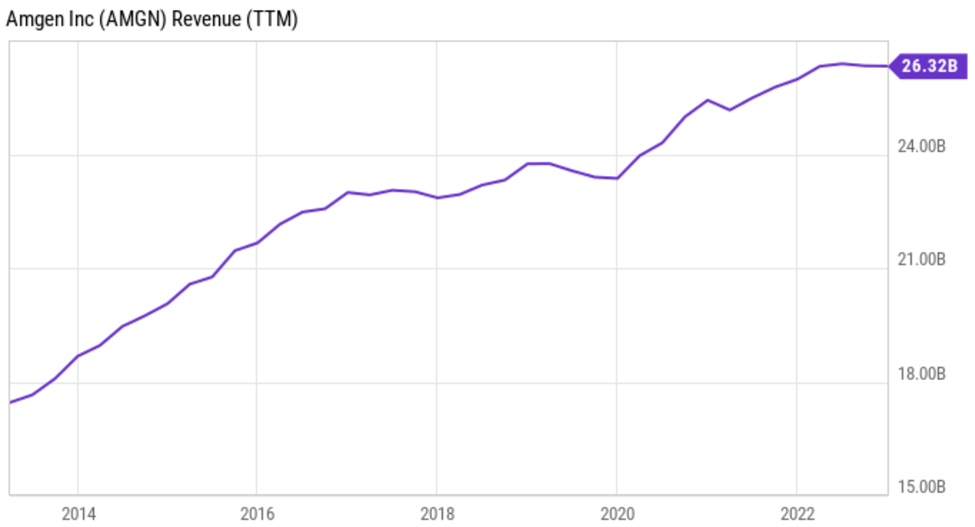

Amgen is one of the largest global biotech companies, after having been one of the pioneers in this space since 1980. It’s also a member of the prestigious Dow 30 companies, with expertise in inflammatory diseases, oncology, and biosimilars. As shown below, AMGN has demonstrated a rather strong and steady revenue growth trajectory over the past 10 years.

YCharts

AMGN recently closed a fourth quarter that looked lackluster on the surface. This includes total revenue growth of just 2%. This was driven by 9% product volume growth that was partially offset by 5% and 2% foreign exchange headwinds. Pressures around pricing were driven by competition around AMGN’s cholesterol-lower drug Repatha, migraine drug Aimovig, and immunology drugs Enbrel and Otezla.

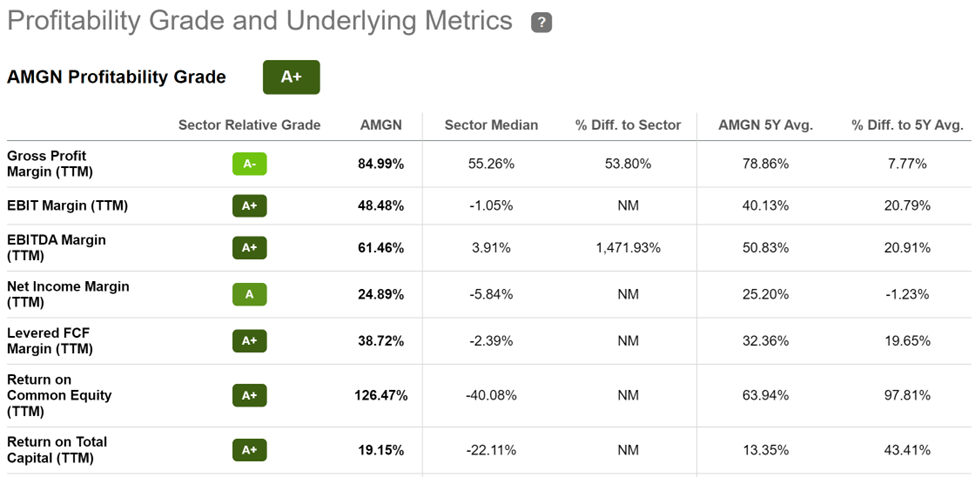

Nonetheless, AMGN remains a solidly profitable enterprise with an A+ grade for profitability, as it retains significant pricing power on its drugs that remain on exclusivity and from its emerging portfolio of biosimilars. As shown below, AMGN generates a very high EBITDA margin of 61% and coverts plenty of sales into cash, with a 39% FCF margin over the trailing 12 months.

Seeking Alpha

Plus, long-term investors should be rewarded, as AMGN’s long-anticipated biosimilar version of the world’s #1 selling drug, HUMIRA, has just come to market this month. AMGEVITA is the leading biosimilar to HUMIRA internationally, and it has a 5-month lead over the next entrant, giving it plenty of time to establish a competitive footing.

Beyond HUMIRA, AMGN has six more biosimilars launches planned in the U.S. and worldwide between now and the end of 2030, giving plenty of long-term growth visibility. Plus, biosimilar development is far less risky than developing a new drug, as they intend to replicate the success of the original drug. Biosimilars also come with some degree of pricing power, since unlike traditional generic drugs, no two biosimilars have the same biologic profile and must each go through a rigorous FDA review before approval.

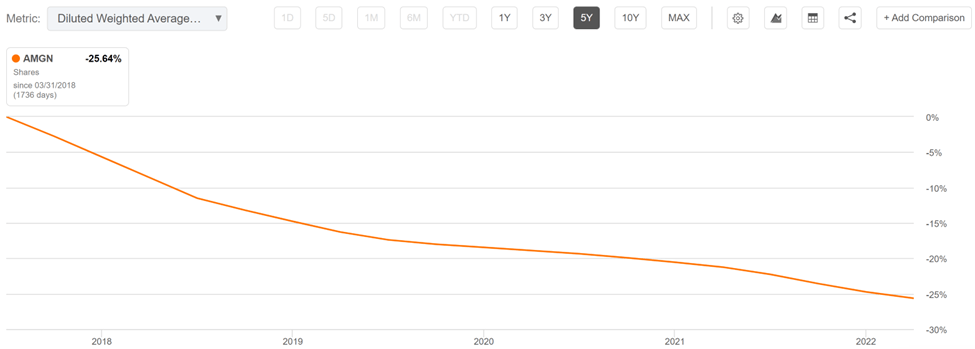

Meanwhile, the downturn in AMGN’s share price is actually a mixed blessing for long-term investors. That’s because management has a strong track record of buying back shares, and as total return investors know, it’s far more accretive to buy back cheaply valued shares than expensive ones. At the current forward PE of 13.6, shareholders are getting a 7.4% earnings yield for every share that’s repurchased by the company.

As shown below, AMGN has significantly reduced its share count, with a 25.6% reduction in its outstanding float over the past 5 years.

AMGN Shares Outstanding (Seeking Alpha)

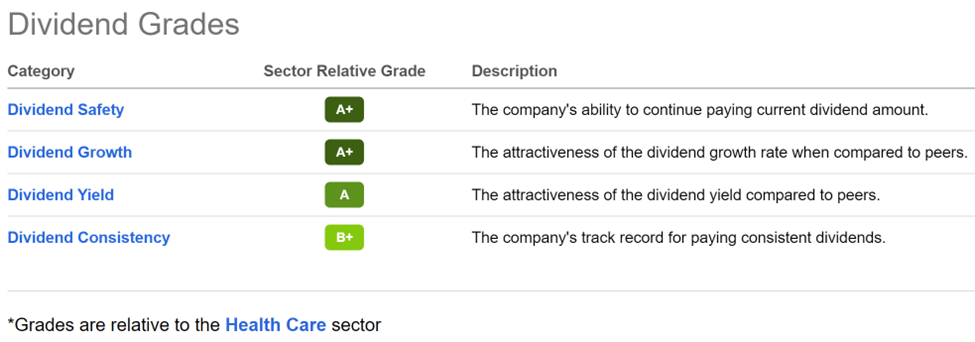

Moreover, AMGN maintains a BBB+ rated balance sheet and pays a respectable 3.5% dividend yield that’s well-protected by a 44% payout ratio. It’s also grown its dividend an a robust 5-year CAGR of 11% and has 11 years of consecutive growth. As shown below, AMGN scores mostly A grades for dividend safety, growth, yield, and consistency.

Seeking Alpha

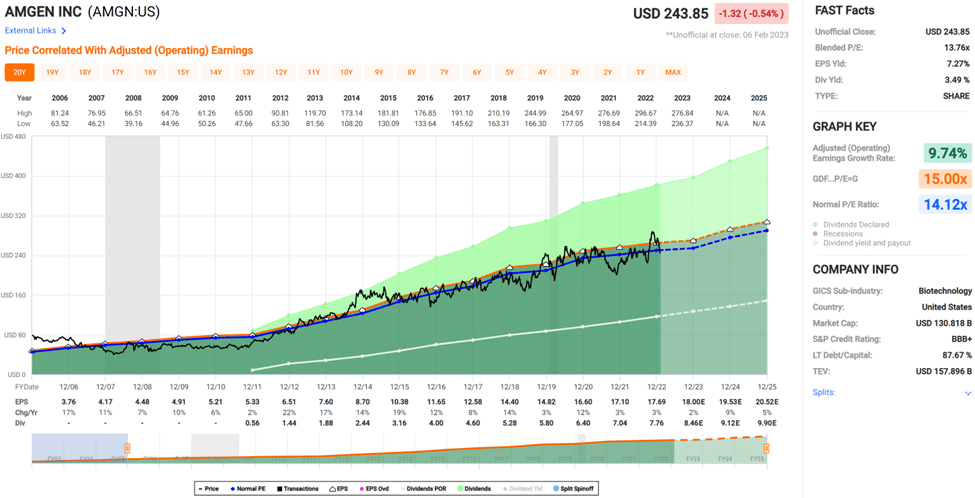

Lastly, AMGN appears to be attractively priced at $243.85 with a forward PE of 13.6, with analysts estimating 7% EPS growth next year. Analysts have an average price target of $259 and as shown below, AMGN has had a fairly predictable pattern of peaks and valleys and an overall upward trajectory. It’s currently trading in a valley with a PE that sits comfortably below its normal PE of 16.3.

FAST Graphs

Investor Takeaway

Amgen is currently a great choice for long-term investors looking to add a quality drug maker to their portfolios. Its share price has fallen materially over the past couple of months, making it attractive for value investors. Moreover, AMGN has strong long-term revenue growth prospects with its burgeoning biosimilar portfolio. These factors, combined with its strong track record of dividend growth and share repurchases make it a compelling buy on the drop.

Be the first to comment