magnez2/iStock Unreleased via Getty Images

Investment Thesis

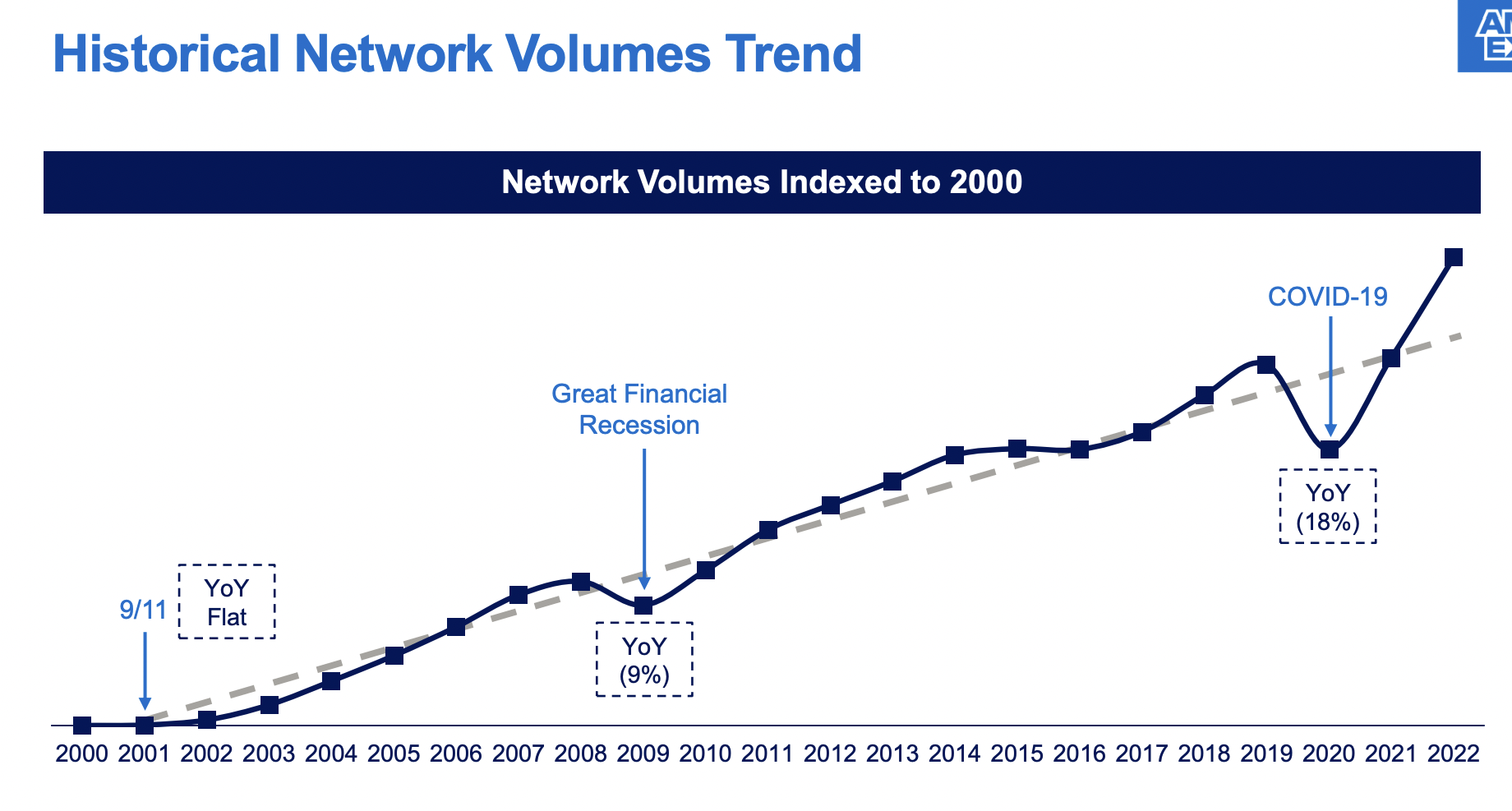

American Express (NYSE:AXP) is an excellent GARP (growth at a reasonable price) company with one of the strongest branding in the world. The company took a huge hit during the pandemic due to lockdowns but has bounced back quickly, with volume now back above pre-pandemic levels. As countries continue to re-open (most notably China and Japan as of late), travel demand and spending are now stronger than ever. Elevated goods and services pricing caused by inflation is also a tailwind, as it boosts overall transaction volume. This is reflected in the latest Q4 earnings result, with the company reporting impressive revenue growth and better-than-expected guidance. Its current valuation is also attractive, as multiples are below credit card peers and its own historical averages. I believe there is further upside potential considering the valuation and growth. Therefore, I rate the company as a buy.

American Express

Q4 Earnings

American Express recently announced its fourth-quarter earnings and the overall results are solid, especially on the top line and guidance.

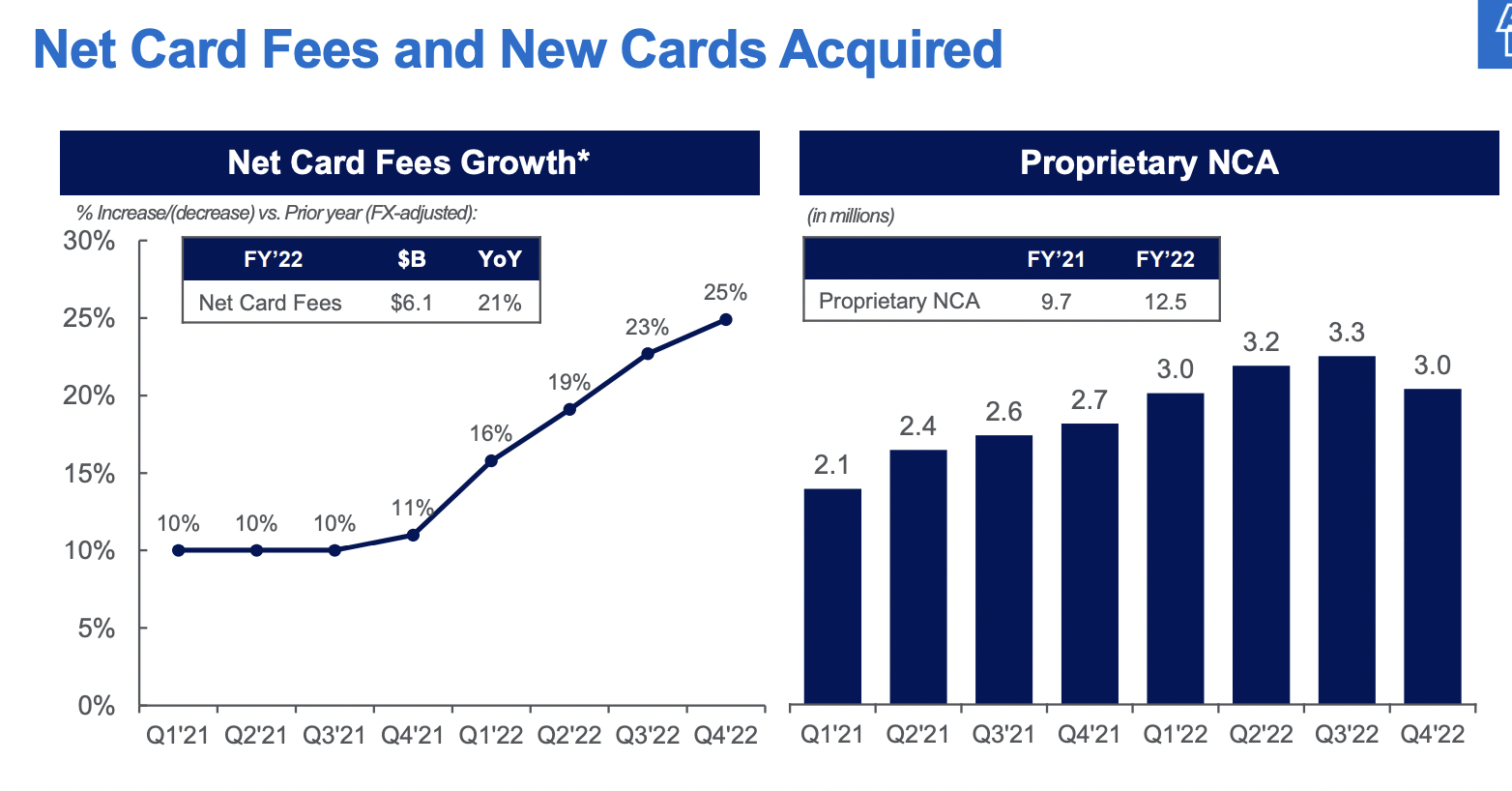

The company reported revenue of $14.2 billion, up 17% YoY (year over year) from $12.1 billion. Total network volume increased 12% YoY from $368.1 billion to $413.3 billion. The growth is mainly driven by higher card spending, increased card fees, and higher net interest income. Discount revenue (merchant fees) was $8.2 billion compared to $7.1 billion, up 14% YoY. This is led by strong momentum in the travel and entertainment space, which grew by 38%. Net card fees increased 21% YoY from $1.3 billion to $1.6 billion, as it acquired 3 million new card members during the quarter. Net interest income also increased 31% YoY from $2.1 billion to $2.8 billion thanks to higher interest rates.

American Express

The bottom line appears to be underwhelming, but it is largely caused by non-operational impacts. Operating expenses actually grew slower than revenue, which increased by 15% YoY from $9.8 billion to $11.3 billion. This is largely due to increased card member services expenses and salaries & employee benefits, which were up 32% and 23% respectively. The net income for the quarter was $1.57 billion, down 9% YoY from $1.72 billion. This is impacted by a $234 million net loss in its Amex Ventures strategic investment portfolio. It is also having tough comps due to sizable credit reserve releases in 2021. On a pre-tax and pre-provision basis, this quarter’s net income was up 23% YoY.

Jeff Campbell, CFO, on net income

As I have said throughout the year, year-over-year comparisons of net income have been challenging due to the sizable credit reserve releases we had in 2021. Because of these prior year reserve releases, we have also included pre-tax pre-provision income as a supplemental disclosure again this quarter. On this basis, pre-tax, pre-provision income was $11.8 billion for the full year and $2.9 billion in the fourth quarter, up 27% and 23% respectively versus the prior year, reflecting the growth momentum in our underlying earnings.

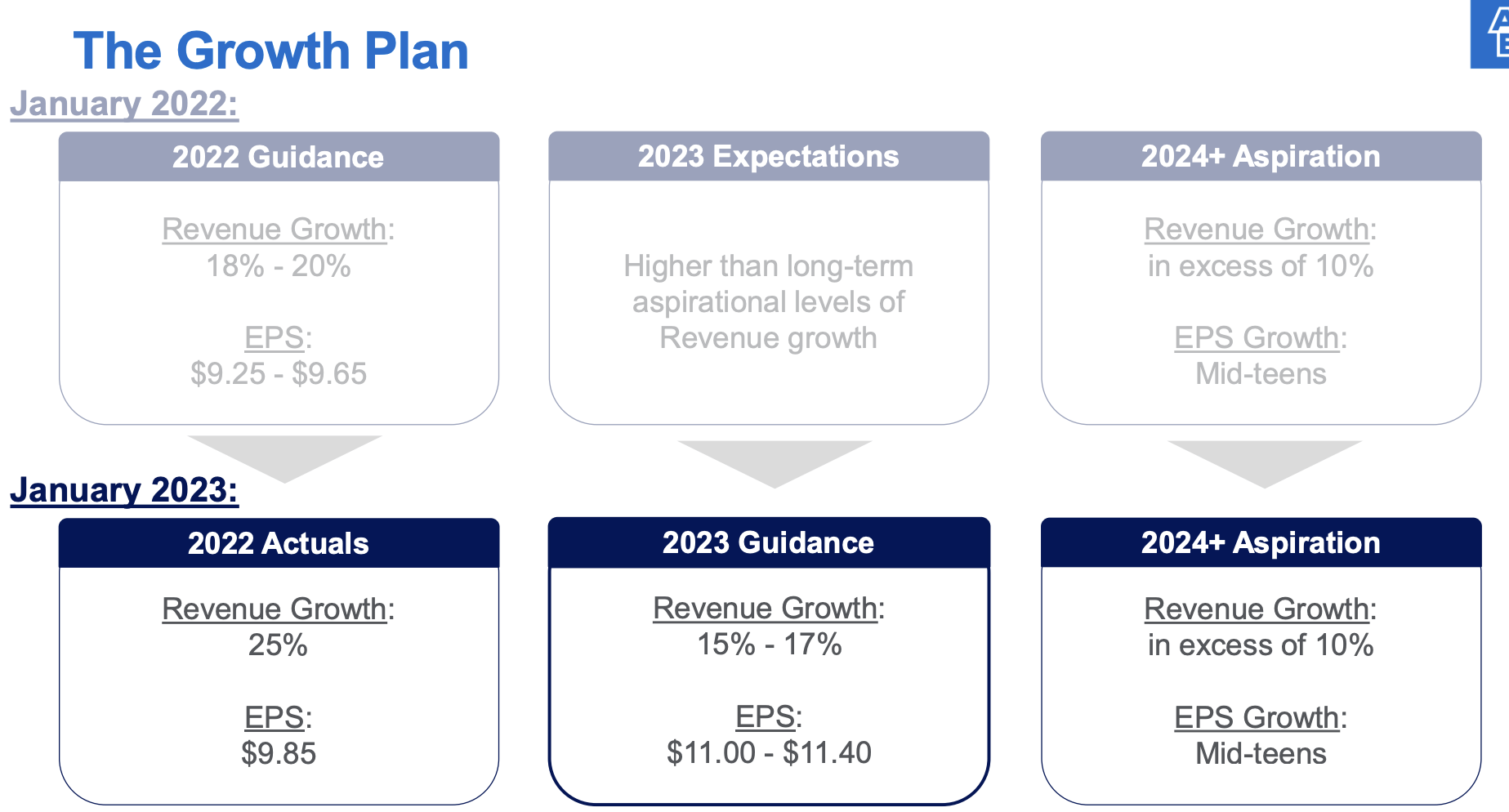

The company also initiated very upbeat guidance for FY23. It guided revenue growth to be between 15% to 17% and EPS growth to be between 12% to 16%, which is roughly 5% above consensus. This is quite unexpected as most people expect spending will slow down in the coming months but apparently, the momentum is still very strong. Given the strong results, management also boosted the quarterly dividend by 15% from $0.52 to $0.60.

American Express

Valuation

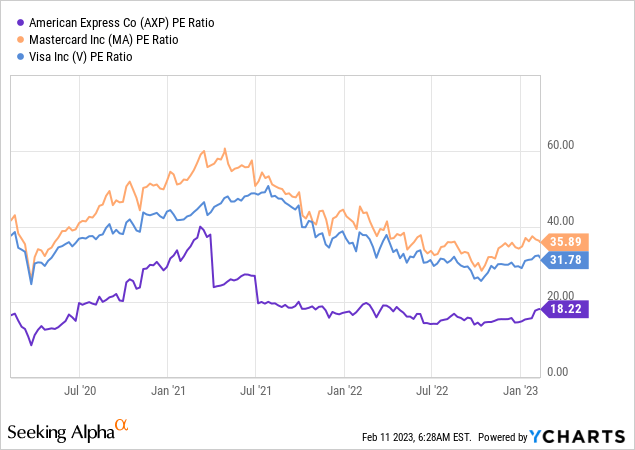

The company’s current valuation is quite compelling in my opinion, especially when considering its growth rates and guidance. It is trading at a PE ratio of 18.2x, which is pretty cheap given its quality. From the chart below, you can see that this is way below credit card peers such as Mastercard (MA) and Visa (V), which have a PE ratio of 35.9x and 31.8x respectively. Not to mention, it is actually growing revenue at a faster pace as well. Of course, their business is slightly different, as American Express does take on credit risks while the two above only handle the issuing and processing part. But this still gives you an idea of the discount the company is trading at. It is also undervalued on a historical basis, as the current PE ratio is 9.3% below its 5-year average of 20.4x. With the company expecting long-term double-digit growth on both the top and bottom line, I believe there is room for multiples expansion and should offer meaningful upside potential.

Investors Takeaway

I like American Express at the current price. The recession is definitely a potential risk, but I am not too worried at the moment. Unemployment rates are very low, and consumer spending is still at healthy levels. The company’s relatively affluent demographic should also show better resilience during downturns. I will start to be more cautious if we see a jump in unemployment numbers. Currently, the spending momentum is still strong, especially in the travel and entertainment space. The fourth quarter’s earnings and guidance defiantly signaled this and showed management’s confidence in the current state of the economy. I believe the company has solid upside potential as its valuation remains discounted while growth continues to be strong. I rate the company as a buy at the current price.

Be the first to comment