Mario Tama

It is hard to blame investors if they start seeking a bit of a thrill in early 2023 after the riskier names got slaughtered in 2022. After selling off the first trading day of the new year, stocks have generally held up well since, with riskier names (including profitable tech) having done well compared to stocks like Altria Group, Inc. (NYSE:MO), which is down 4% YTD. Tesla, Inc. (TSLA) is up almost 20% YTD already, while Nvidia Corporation (NVDA) is up 22%. Has the world changed overnight just because the calendar flipped to 2023? I don’t believe so.

In addition, the recent producer price index (“PCI”) reading has sent a shiver down consumer staples as covered here by Seeking Alpha. Altria is down 2.50% as of this writing, and The Coca-Cola Company (KO) is down about the same. The rationale behind this mini-selloff is that pricing power may decline and that consumer staple stocks are trading at high valuations already. It is hard to argue with both these points in general.

But individual stock-picking deviates from the “general” beyond a certain point. At some point, certain stocks become too good to pass. This article is intended to argue why neither recession fears nor valuation should deter Altria investors at the very least, if not bolster their sentiments. Let us get into the details.

Overvaluation theory falls flat on its face

Scroll through the comments section of the Seeking Alpha news item linked above and you will see a few posters painting using a broad brush that consumer staple stocks are overvalued. Sure, some are. I’ve written in a few of my Tesla articles that it was laughable that The Clorox Company (CLX) was trading at a multiple of 30. But not all staples stocks are trading at such valuations, and not Altria in particular, as shown below. The valuation is so depressing that the forward multiple and yield are not that far off from each other.

Altria PE and Yield (Seekingalpha.com)

Not your typical junk high yield

If you shy away from very high yielding stocks in the fear that the yield might just be “junk” and the dividend could be slashed any time, you are doing it right. But Altria, despite the 8.50% yield tag, is far from “junk” as explained below.

- Altria Group, Inc. has a stated dividend payout policy of returning about 80% of its earnings to shareholders.

- The current annual dividend of $3.76 per share is bang on target with this goal using the current forward EPS of $4.81 per share, with a payout ratio of 78%.

- I’ve always extolled the virtue of using Free cash flow (“FCF”) based dividend metrics since earnings may fluctuate due to non-recurring items.

- Altria’s current shares outstanding equals 1.792 Billion

- That means, the company needs $6.73 Billion in annual free cash flow to meet its dividend commitment to shareholders. That is, 1.792 Billion shares times $3.76 dividend per share.

- Altria’s trailing twelve months FCF stands at $8.086 Billion, which gives it an FCF based payout ratio of 83%. This is once again in the range targeted by the company (although their stated goal is based on earnings per share).

Pricing power argument ignores basic Economic principle

One of the first things I learned in my business school was the difference between elastic and inelastic products. Yet, it appears like the market and some times even reputed analysts forget this basic principle that not every product demand goes down in flames during a recession. Altria Group, Inc., luckily for its investors, is selling inelastic products that don’t get impacted as much by recession or change in price or income.

Inelastic (Google.com)

When the Fed has its Zero Interest Rate Policy (“ZIRP”), riskier names were going bananas because borrowing was so easy and savers were penalized basically. It made sense that stocks like Altria were out of favor back then compared to fancier names.

But now, with recession fears looming, what sense does it make for staples to sell off? Especially undervalued staples with healthy dividend coverage. I cannot think of any. Add to that the company sells an addictive product and has a brand that is the best in business. Imagine this. You go to the grocery store looking for bread. You find some name brand selling at a 50% premium compared to the store’s brand. It makes total sense to buy the store brand. Bread is bread, especially when things are tight. Now, all of us know a smoker or two. If I tell my smoker friends that a stick is a stick, I’d get whacked. It makes even more sense to buy the best in brand when it comes to what is generally accepted as an unhealthy product like tobacco.

Risks and Antidotes

To keep things fair and balanced, I do want to acknowledge that Altria is trading at a depressed valuation due to some well known risks like its constant regulatory threats and the fact that it is operating in what is currently an industry in perennial decline.

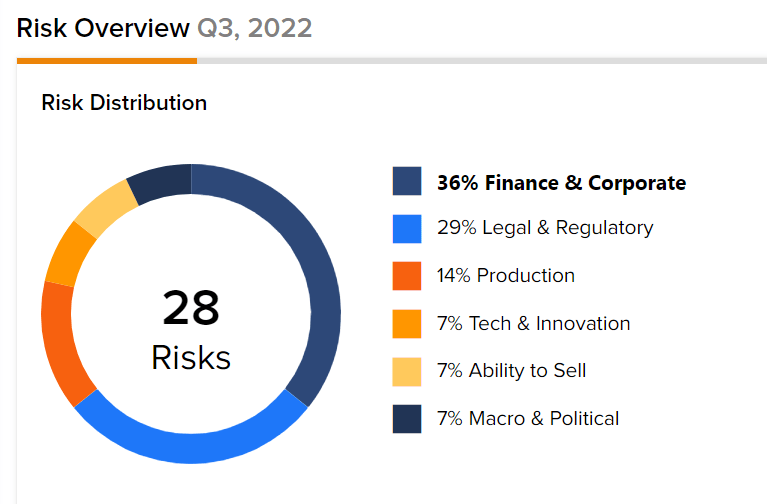

In addition, I’ve recently seen Seeking Alpha authors use the nice feature available on Tipranks.com that shows the risk factors with various companies as shown below. For Altria Group, there are 28 risk factors listed, with each having its percentage, ranging from competition (4% risk) to growth (14% risk).

Going over this list item by item in the page referenced above, it is clear that the top three risk factors are Growth, Debt, and Litigation/Government. And Altria has operated profitably for decades using these three antidotes, in the same order: pricing power, operational efficiency, and lobbying. To expand on those three antidotes a little, the company’s pricing power and brand recognition helps it offset the declining growth. Their relentless focus on shareholder value ensures debt is used for business operations and not excessive compensation and other pitfalls. Lastly, the government needs the billions of dollars it needs in taxes from the tobacco industry, and Altria has always been one of the first to acknowledged that people need to transition from smoking.

Yes, you read that right. Altria’s “Moving Beyond Smoking” initiative is not just a tagline but a conscious acknowledgement that they need to spread their risks as a company. For example, as can be seen on this page, the company’s product development is focused on three things that are key for its future success: nicotine satisfaction with reduced health risks and without the social friction. If that isn’t an indication of a company that knows where it stands and where it is heading, then I don’t know what is.

Altria Risks (tipranks.com)

Conclusion

In spite of the risks mentioned above, basic math tells me that reinvesting in an undervalued, high-yielding stock makes sense in the long term. Altria Group, Inc. is like my homeowner’s insurance, I don’t really appreciate it until I really need it. 2022 was a year where I really needed it and was glad I had some Altria Group shares. 2023 is shaping up a bit different so far, but if and when panic really sets in on recession, I expect more investors to seek shelter here in Altria Group, Inc.

Be the first to comment