Joesboy/iStock via Getty Images

The Investment Thesis

Alpha Metallurgical Resources Inc (NYSE:AMR) is a company operating in the United States, more specifically in Virginia and West Virginia. The company engages in mining, producing, and processing and then sells met and thermal coal. From the end of 2021, the company has a total of 20 different mines all across the states. Besides this, they also own 8 coal preparation facilities.

Looking at the current fundamentals, AMR might look like a steal with such a low p/e. But I think the future is uncertain and unfavorable for the sector. Headwinds are building up and I expect the revenues and bottom line to drop. This forces me to have a sell rating for the company.

Last Earnings Report Highlights

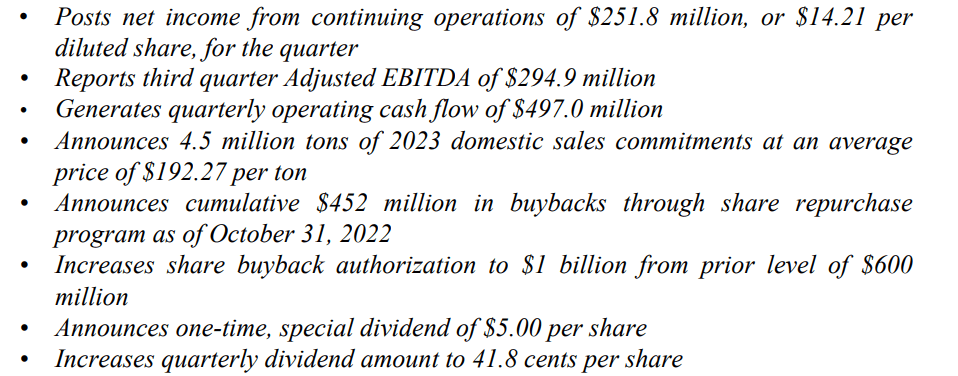

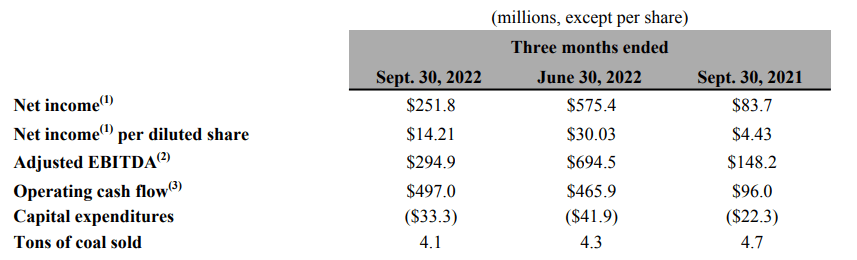

In the latest earnings report, there were plenty of different highlights from the company. The bottom line is perhaps the most impressive growth from the quarter, a 300% increase YoY as the price for the product has increased and the company managed to achieve better profitability too. In fact, the amount of coal the company sold has decreased YoY, from 4.7 million to 4.1 million tons instead.

Earnings Highlights (Q3 Earnings Report)

Some other notable highlight I found interesting was the increase in the share buyback budget the company made. The program was authorized to go from $600 million to $1 billion instead, an impressive increase in my opinion. It seems sustainable too as the company had an operating cash flow of $497 million in the last quarter.

Revenue Statement (Q3 Earnings Report)

Looking ahead, the company expected to sell about 4.5 million tons of coal in 2023 at an average price of $192.7 per ton. This would mean full-year revenues come in at around $864 million. Given the impressive cash flow the company had, they also announced a special dividend of $5 per share.

I am not the only one satisfied with the company’s performance, the CEO David Stetson said “Alphas third quarter results represent another solid performance from our team”.

Sector Outlook

The coal market worldwide is maybe not the faster growing one as there are many different options for energy instead these days. Despite that, the market still grew at an annual rate of 1.1% in the latest surveys and reports. There are plenty of headwinds ahead, however. China being one of the largest consumers in the world is expecting to see a population decline for the first time ever. This will cause the demand for housing to slow down, which relies on steel production which is fueled by coal. The same headwinds happened in the United States where the demand was lowered by 6% as the switch towards gas-fired power generation continued to happen.

What investors will have to look out for is the price of coal. If demand sinks the price will drop and then revenues for companies in the sector will sink with it. It’s a commodity-driven industry. The biggest headwind that the coal sector has is the quick adaptation to other energy sources like natural gas or fuel cells instead. This trend seems to continue and investing in already low-margin businesses could prove dangerous.

Competitors

The coal industries have several different companies involved within it all competing for their share of the market. I think that the competition though is quite slim and there isn’t anything to say one company will hinder another one. Undercutting does perhaps happen a little bit but it’s a free market where everyone is participating.

Instead, I think competition comes down to having the best-run financial department that makes sure there is cash to expand more and not be flooded with debt.

But let’s mention some potential competitors, NACCO Industries (NC) and Peabody Energy Corporation (BTU) are both companies that could be competitors in terms of taking on new mines and therefore generating more revenue than AMR. Valuation wise these companies are all trading at very low multiples as the price for coal has increased and this has made the companies seem like bargains. Instead, I want to look at the leveraged cash flow ratio, where AMR seems to win by a lot with its 21.13% TTM rate.

The Balance Sheet

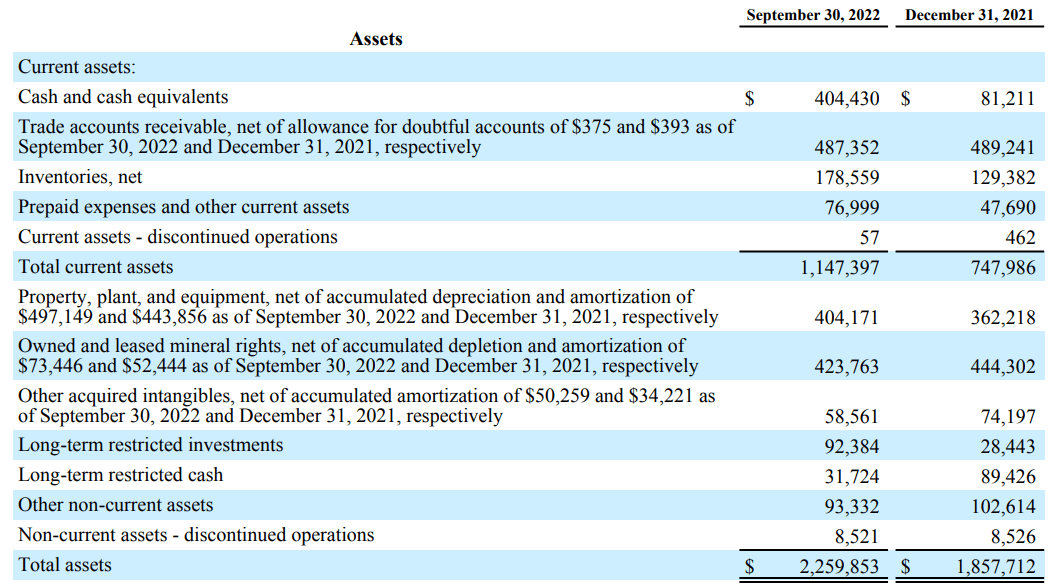

Moving over to the balance sheet I can see that the company has made some important steps in securing a better financial situation. Firstly, the cash position has gone from $81 million in Q3 2021 to $404 million in Q3 2022. I think this represents a responsible move by the management that the coming next few years might be troublesome in terms of revenue, and having a cushion will make that a little bit easier.

Balance Sheet (Q3 Earnings Report)

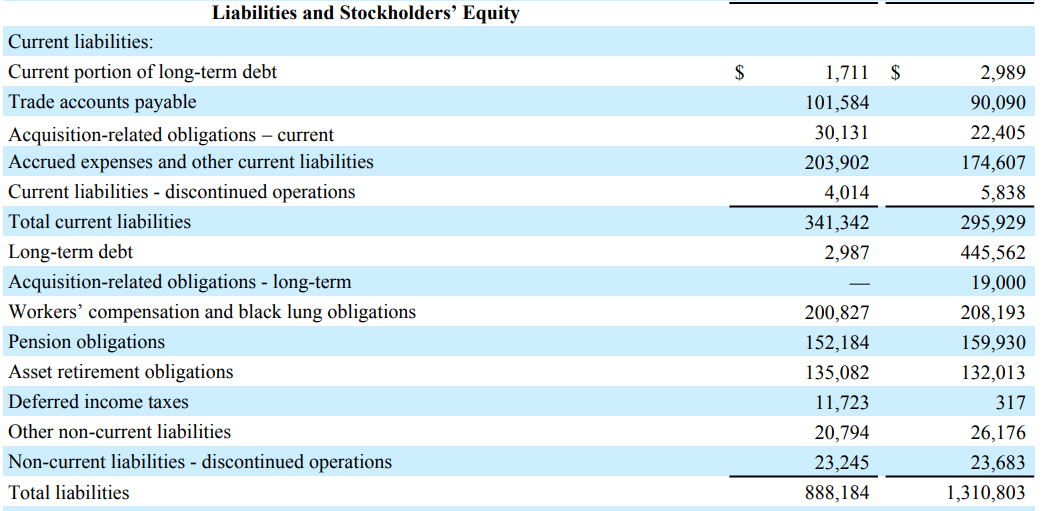

Besides having a fantastic cash position, the company has also managed to have relatively no debt. The current debt is just $1.7 million and the long-term debt comes in at $2.9 million. I have no doubt that the company will be able to pay off any debt due. Especially when they have put so much money into the share repurchase program.

Balance Sheet (Q3 Earnings Report)

The assets have been increasing YoY many thanks to the higher cash position on the back of much higher free cash flow for the company. But besides more cash, the company also has more assets in inventories, amounting to $178 million right now. I don’t expect the company to be struggling to sell this off as there is still demand for coal, even though it’s shrinking a little bit.

I left one of the most impressive moves for last. Looking at the liabilities they have seen a drastic decrease as the company paid off a lot of debt in 2022. Going from $445 million in long-term debt to just $2.9 million is in my book a sign of competent management.

Looking ahead, I don’t think share dilution will be an issue as the company has committed to giving back to the shareholders and not diluting their stake. Cash flow will instead be what I look at. If it’s drastically declining or very volatile I will be worried. I don’t expect the same levels as 2022 has provided, that might be a one-off. But I also don’t expect negative cash flows either. I guess I am trying to say that if the drop is not too drastic I won’t be worried.

Valuing The Company

It’s difficult valuing a company like AMR since you are basically estimating how the market they’re in will perform and what the demand might be like. In the case of AMR, I think there is a case to be made that demand will continue sinking and that will hurt earnings.

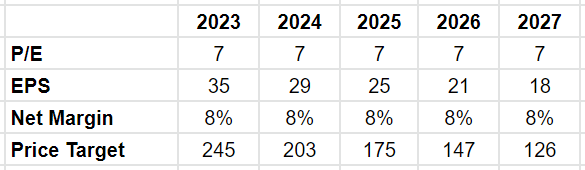

Future Estimates (Author’s Own Calculations)

Right now the company has a TTM p/e of just above 2. Compare that to the sector which has an average p/e of 12. I have used 7 as a terminal value as I think there are a lot of risks with the market outlook. Coal is something that is being used less and less. It won’t happen overnight, but the market is forward-looking and so am I.

I think the current EPS makes the company look like a steal but as I said, I don’t expect the prices of coal to stay at these levels, and with global use decreasing there are plenty of headwinds against the industry.

Perhaps a diminishing EPS of 15% YoY seems a bit harsh, but I would rather be a little bit over with that number than get it wrong and lose money. Risk management is incredibly important when having a portfolio and right now I think AMR is too risky.

Looking at the margins I wouldn’t be surprised if they stay around 8%. The company has a pretty simple business model where they mine for coal and then process and sell it. If they only see less revenue perhaps the bottom line can stay in a similar manner if the management can handle the operating expenses well. I would look out for how the company is building up inventory and if that weighs on expenses by leases for example.

Conclusion

Alpha Metallurgical Resources Inc is a coal mining company in the United States. The company has had very impressive revenues in the last few quarters as the price for coal has gone up and in turn, made AMR look like a steal.

Despite this, the p/e is just 2 right now and it seems the forward p/e is increasing, indicating the current revenues aren’t sustainable. With a decline worldwide in using coal, I think the future seems uncertain.

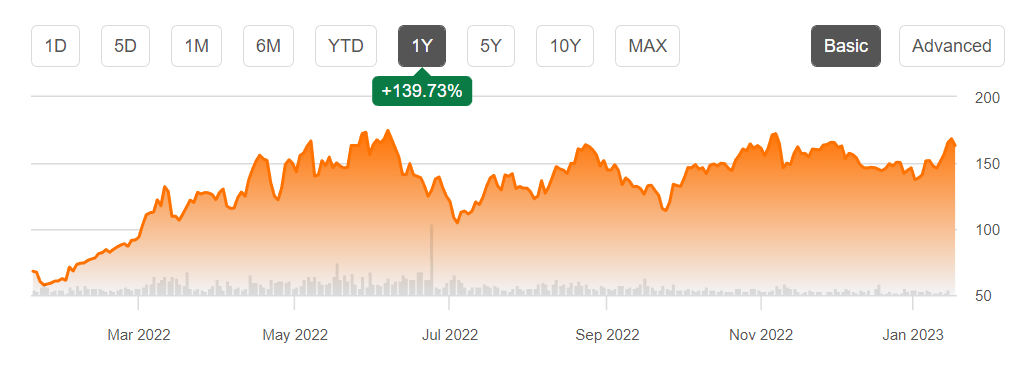

Price Chart (Seeking Alpha)

With everything I have gone over, I don’t think investing in the company is very good. Commodity prices fluctuate and with a very hard shift towards renewable energy instead, I think the headwinds looking forward are too much. Selling shares in the company might be the best.

Be the first to comment