Vladimir Zakharov/iStock via Getty Images

Investment Thesis

Alliance Resource Partners, L.P. (NASDAQ:ARLP) results could not have been more timely. There’s a lot of nuances that investors should be mindful of, for example with regards to its decrease in free cash flows. Nevertheless, I charge, as I’ve been doing for months now, that ARLP is a compelling investment opportunity.

Author’s work

The timing of these results could haven’t been better. Particularly given that The Guardian published today a finding that shows that 99% of coal plants are less economically viable than building solar panels and wind turbines.

Guardian article

I recognize that investing in coal can get some investors politically charged. That’s not what I’m interested in. I’m interested in finding compelling opportunities with attractive risk rewards. Hence, with this preamble in mind, let’s get to it.

King Coal Drama

Without a doubt, the geopolitical developments of 2022 revived the coal mining industry. And now, this drama appears to have receded and forced investors to think, what’s next?

For their part, despite investors’ concern that ARLP may only be interested in empire-building and acquiring assets, ARLP asserts that this is not the case.

Yes, ARLP is buying up slightly over $70 million worth of Oil & Gas Royalties in January. And yes, this is on the back of an acquisition that it had already announced in 2022. But the fact that this latest acquisition is within the Oil & Gas sector has investors positively delighted.

Hopefully, 2022 will be the end of ARLP’s “diworsification” into Green Energy projects.

Now, let’s turn our focus to a blemish in its Q4 results.

Free Cash Flows Were Not So Strong

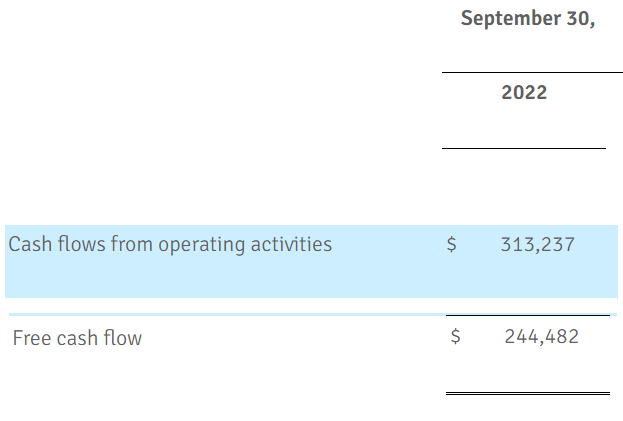

Back in Q3 2022, ARLP saw its free cash flow reach $250 million. This led many investors to presume that more than $1.2 billion of free cash flows could be on the cards in 2023.

ARLP Q3 results

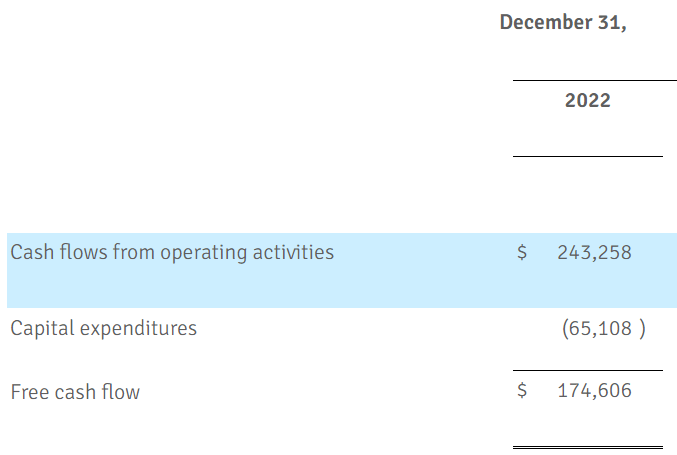

Fast-forward to Q4 results and its free cash flow was about 30% lower than in Q3 2022.

ARLP Q4 2022

Clearly, the business is very cheap. But the speed at which this free cash flow dropped in 90 days is a reminder that commodity companies can have a lot of inbuilt operating leverage.

On the other hand, ARLP holds around $130 million of net debt. Thus, given that ARLP is clearly making close to this figure in free cash flow over a 90-day period, this will go a long way to reassuring investors that ARLP’s 2025 senior notes are evidently not going to cause any concern to the underlying fundamentals.

Despite my concern for ARLP’s unimpressive end to a very successful year, here’s why I’m still bullish on ARLP.

Guidance Sticks Out Like A Sore Thumb

ARLP guides that it will increase production in 2023 by 1 or 2 million from 2022. And on top of this, it also highlights that it has 94% of its production committed at around a 15% higher average realized pricing compared to 2022.

For a business that’s priced at approximately 3x forward free cash flows, I believe that with this ”guaranteed” year already committed, it means that investors getting involved today only need another 2 years – after 2023 – for this investment to be given away for free.

Perhaps, there’s a better way to think about this. ARLP produces primarily low-sulfur coal, which is used in the electric power generation industry.

If we think that in times of distress, the U.S. will still need access to reliable and flexible energy, particularly in times when solar and wind power don’t quite live up to peak demand, then Alliance Resource Partners, L.P. and other thermal coal players will continue to see high demand for their coal.

The Bottom Line

In my prior article in December, I stated:

[…] if ARLP doesn’t have to be as aggressive in paying down its debt in 2023, this would further support my estimate that by this time next year, ARLP’s cash distribution could reach $3.00.

I wouldn’t have assumed that, this close after I wrote those words, Alliance Resource Partners, L.P.’s dividend would already be a run rate of $2.8 per share.

That’s the huge benefit of buying into businesses when you have a wide margin of safety. Things can go wrong, and you still make an attractive return.

Be the first to comment