MarianVejcik/iStock via Getty Images

Intro

Align Technology, Inc. (NASDAQ:ALGN), a prominent player in the Health Care Supplies industry, is based in Tempe, Arizona, and boasts a workforce of 24,020 employees. The company’s primary focus lies in the field of orthodontics, specifically in the area of teeth straightening. ALGN has gained recognition for its innovative product, Invisalign, which offers a preferable alternative to traditional wire braces that are often associated with discomfort and unease during the middle and high school years. Invisalign utilizes transparent aligners, allowing consumers to discreetly achieve teeth straightening. As a result, ALGN has emerged as a leading provider of clear dental aligners, revolutionizing the orthodontic landscape.

This article aims to conduct a comprehensive analysis of ALGN’s financial performance and growth prospects. We will delve into the company’s revenue trends, profitability indicators, and its ability to generate free cash flow. Additionally, we will evaluate ALGN’s strategic position within the orthodontic industry and offer an outlook for its future. By examining these key factors, investors can gain valuable insights into the company’s potential and determine its attractiveness as an investment opportunity in the current market environment.

Track Record

Strong financial performance ensures the long-term viability and growth of a company. It allows the company to generate consistent profits, reinvest in its operations, and pursue strategic initiatives. This, in turn, enables the company to expand its market presence, invest in research and development, and seize new growth opportunities.

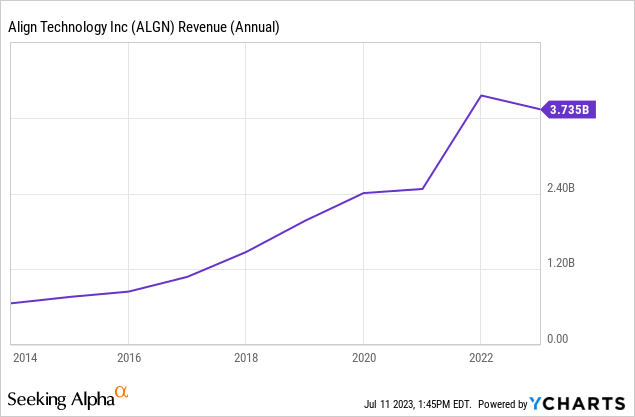

Align Technology has demonstrated remarkable revenue growth over the past decade, with a total growth of 465.67% and a compounded annual growth rate (CAGR) of 18.92%. This growth has been driven by the company’s strong product portfolio and its expanding global reach. A high growth rate is important as it reflects the company’s capacity to capture market share, invest in strategic initiatives, and potentially outperform competitors.

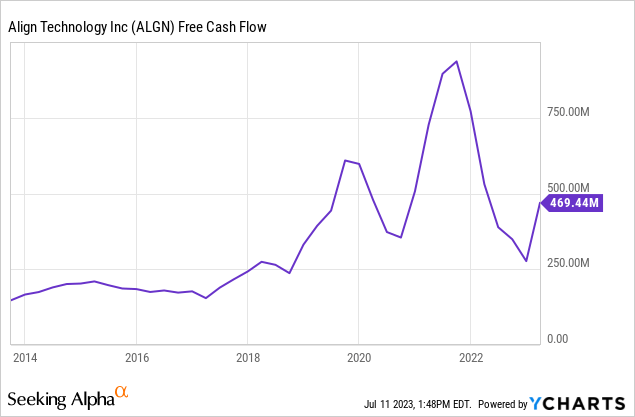

While ALGN has experienced robust revenue growth, it faced a significant decline in free cash flow in 2022. The company reported a free cash flow of $276 million, down from $771.45 million in the previous year. The significant drop in free cash flow can be attributed to a decline in operating cash flow, which can be attributed to ongoing macroeconomic uncertainty, weakened consumer confidence, and unfavorable foreign exchange rates affecting various currencies. It is important for ALGN to address this decline and ensure healthy cash flow generation to fund future growth opportunities.

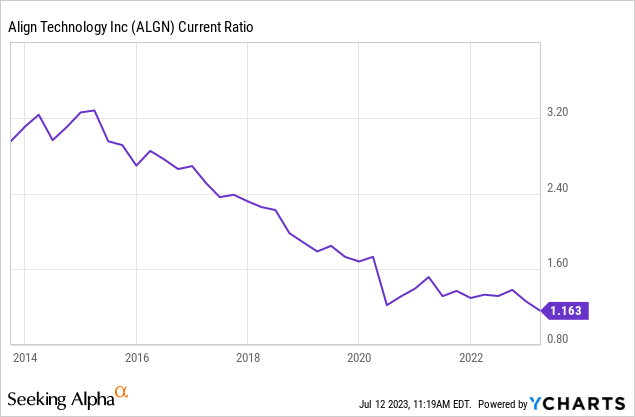

Analyzing ALGN’s balance sheet indicators reveals some concerns about the company’s financial health. The current ratio of 1.16 indicates a relatively low level of short-term liquidity, raising questions about ALGN’s ability to meet its near-term liabilities in a timely manner. This low current ratio is concerning for the company’s liquidity position, as it suggests that ALGN may face challenges in accessing necessary funds and managing its short-term obligations effectively. ALGN’s low current ratio is even more concerning considering that this is the company’s lowest current ratio in a decade and the overall trend doesn’t look great.

However, it is worth noting that the debt-to-equity (D/E) ratio of just 0.03 is a positive indicator, highlighting ALGN’s conservative capital structure with minimal debt. This implies a lower level of financial risk compared to companies with higher D/E ratios. The low D/E ratio suggests that ALGN has maintained a healthy balance sheet and is less susceptible to financial strain.

While the low D/E ratio is a good indicator of a healthy balance sheet, the low current ratio remains a concern. A higher current ratio would provide ALGN with better short-term liquidity, enabling the company to navigate economic downturns more effectively, secure capital at favorable rates, and pursue growth opportunities.

Considering these factors, investors should approach ALGN’s financial situation with caution. While the low D/E ratio provides some reassurance, the low current ratio raises legitimate concerns about the company’s liquidity and ability to handle short-term financial obligations. It is essential for ALGN to address these liquidity challenges to ensure its financial stability and support future growth.

ALGN has shown a solid record of profitability, as evidenced by its return on equity (ROE) figures over the years. Although the company experienced fluctuations in ROE, the average 10-year ROE stands at an impressive 24.89%. Comparing ALGN’s average ROE to the Healthcare Equipment & Supplies industry average ROE of 7.12%, it is evident that ALGN has consistently outperformed its industry peers in terms of efficiently utilizing capital to generate profits.

ALGN’s high ROE over the years can be attributed to a couple of factors. First, as the original inventor of clear aligners technology, ALGN’s Invisalign brand is one of the most recognized brands in the orthodontics industry. This gives the company a significant advantage over its competitors. Additionally, the company has expanded its reach over the decade, ALGN has a global presence, with operations in over 100 countries. This gives the company a broad customer base and helps to mitigate the risk of economic downturns in any particular market.

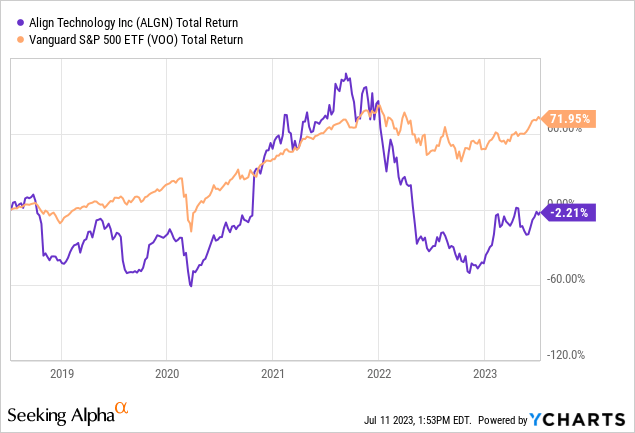

ALGN’s 5-year total return of -2.21% presents a challenging picture compared to the S&P 500’s 5-year total return of 71.95%. This underperformance indicates that ALGN has faced significant headwinds and struggled to deliver value to its investors during this period. However, it’s worth noting that total returns can be influenced by various factors, including market conditions and investor sentiment. Overall, with the poor performance of ALGN’s stock over the recent years, investors are left wondering if the company can turn things around.

2023 and Beyond

Despite ALGN’s poor stock performance over the years, the company is off to a great start in 2023. ALGN beat earnings and revenue expectations for the Q1 of 2023. The company’s earnings per share (EPS) of $1.82 beat expectations by $0.13, and revenue of $943.15 million (-3.09% Y/Y) beat expectations by $39.94 million.

ALGN’s better-than-expected results were driven by favorable average selling prices (ASPS) in both its Clear Aligner and Systems and Services segments. The company’s ability to pass on higher costs to customers indicates successful pricing strategies aligned with market dynamics. Alongside favorable ASPs, ALGN experienced continued growth from its Invisalign Doctor subscription program and Vivera Retainers. The subscription program offers flexibility for doctors in aligner purchases, while the Vivera Retainers provide a popular retention solution for maintaining treatment results.

However, it is important to highlight that ALGN faced challenges in its total case volumes both domestically and internationally. Furthermore, the systems and services segment witnessed a decline in scanner sales compared to the previous year. These factors contributed to the overall decrease in ALGN’s total revenue year over year, despite the favorable ASPs and growth from the Invisalign Doctor subscription program.

The decline in case volumes and scanner sales can be attributed to the impact of a weakening macroeconomic environment, characterized by rising inflation and higher interest rates. These factors have influenced consumer sentiment and negatively affected ALGN’s business, which predominantly sells higher-priced products and services. We are concerned about the company benefitting from higher ASPs. While higher ASPs may offer short-term benefits, it is not a sustainable long-term strategy as there is a limit to how much customers are willing to pay, eventually affecting overall volumes.

Looking ahead, ALGN shows promising prospects in its earnings growth and market position. Analysts estimate that ALGN’s earnings per share for the fiscal year ending in December 2023 will reach approximately $8.29, reflecting a year-over-year growth rate of 6.84%. This positive projection indicates expectations for continued profitability and success in the coming year. Furthermore, revenue estimates for the same period suggest an expected revenue of around $3.94 billion, with a year-over-year growth rate of 5.61%. These estimates demonstrate ALGN’s potential to expand its top line and capitalize on market demand.

One encouraging trend for ALGN is the increasing number of teenagers opting for orthodontic treatment with Invisalign Clear Aligners. There was a 3.9% year-over-year decline in total Clear Aligner case volume, while the case volume for teenage patients using Clear Aligners saw a 3.8% year-over-year increase. This growth signifies the effectiveness of ALGN’s marketing efforts and the growing acceptance of Clear Aligners among younger patients which we see as large growth driver for the business in the future as most teenagers still use traditional metal braces. It bodes well for ALGN, particularly as the summer season, which is an important period for this demographic, approaches.

In addition, ALGN maintains confidence in its large under penetrated global market opportunity. ALGN has 21 million annual case starts per year while the overall market is estimated to be 500 million. We believe ALGN’s digital products and technology have the capacity to transform smiles and improve the lives of millions of people worldwide and ultimately take share from traditional braces and its competitors in clear aligners industry.

There are some risks associated with investing in ALGN. One significant concern is the expiration of ALGN’s patent for its Invisalign clear aligners in 2017, which has opened the door for increased competition in the market. With the absence of patent protection, competitors have emerged, posing a potential threat to ALGN’s market dominance. Increased competition, especially from players offering lower pricing, can impact ALGN’s market share and profitability.

ALGN has experienced remarkable sales growth even in the face of increased competition following the expiration of its patents. Since 2017, when the company’s patents expired, ALGN has more than doubled its revenues. This success can be attributed to the company’s robust brand presence, which is reinforced through annual investments exceeding $300 million. By dedicating substantial resources to the growth and maintenance of their brand, ALGN has effectively serviced a significant customer base of approximately 14.5 million satisfied individuals each year. This strong brand foundation has been instrumental in driving ALGN’s sales expansion and solidifying its position in the market.

Additionally, ALGN is investing in new technologies to drive future growth. ALGN has made investments in digital tools, apps, and clinical education events. ALGN reiterated its dedication to innovation and digital dentistry by developing digital tools, apps, and clinical education events. The company highlighted the increasing adoption of its My Invisalign consumer and patient app and other digital tools like ClinCheck and Live Update. ALGN’s investments in education centers and participation in industry events showcase its commitment to advancing the digital orthodontic field.

During ALGN’s 2023 Q1 earnings call, CEO Joe Hogan emphasized the significance of education events in the company’s strategy.

Earlier in the quarter, we hosted the second align’s symposium on the digital practice, a smaller align event from the most engaged in experience Invisalign orthodontists in the world. It was an amazing opportunity to come together with long-term global partners and thought leaders in orthodontics to see how we are driving the digital transformation of dentistry together. By our participation in each of these events and opportunities, we continue to reinforce the importance of peer-to-peer clinical education and our investments in the orthodontic specialty.

Based on ALGN’s strong performance in Q1 2023, positive growth projections for earnings and revenue, and the company’s commitment to investing in new technologies, we believe that ALGN will have a strong Q2 2023 earnings report, which is expected to be released on July 26th. There are plenty of tailwinds for ALGN including higher average selling prices in both the Clear Aligners and Services segments, growth from the Invisalign Doctor subscription program and Vivera Retainers, and an increasing number of teenagers and children opting for Invisalign Clear Aligners.

Valuation

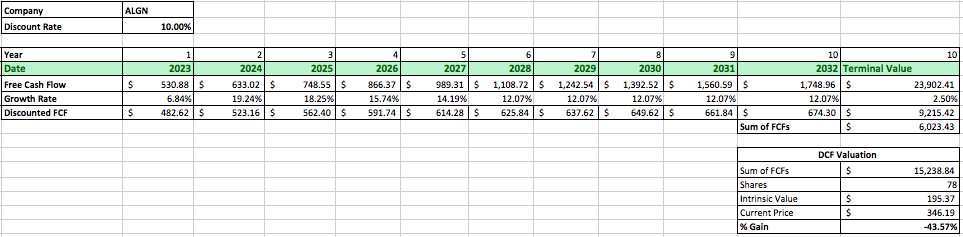

We will utilize the discounted cash flow (DCF) analysis, a preferred method for assessing a company’s value, to evaluate ALGN’s intrinsic worth. By determining the present value of ALGN’s projected future cash flows, we can derive its intrinsic value.

To initiate the analysis, we will start with the average of ALGN’s previous five years of free cash flows, which stands at $496.89 million. We use the average of the last five years of free cash flows since the company’s free cash flow declined so drastically in 2022, such a drastic decline may not provide the best starting point for a discounted cash flow analysis.

Based on average analyst estimates, we will apply an initial growth rate of 6.84% for 2023, followed by growth rates of 19.24% for 2024, 18.25% for 2025, 15.74% for 2026, and 14.19% for 2027. It is important to note that predicting future free cash flows for ALGN beyond the next few years can present challenges due to uncertainty and limited visibility so we will use a second growth rate of 12.07% for years 6-10 based on the average of the free cash flow and revenue compounded annual growth rate over the last 10 years.

Using a discount rate of 10%, which accounts for the long-term return rate of the S&P 500 with dividends reinvested, and a conservative terminal growth rate of 2.5%, we calculate ALGN’s intrinsic value to be $195.37. This suggests that ALGN may currently be substantially overvalued, potentially offering investors a potential loss of -43.5% compared to the company’s current market price.

Author’s Work

Takeaway

In conclusion, despite ALGN’s strong start in 2023 and positive growth projections for earnings and revenue, we recommend giving ALGN a sell rating based on its expensive stock valuation. While the company shows promising prospects with higher average selling prices, growth from subscription programs and retention solutions, and increasing demand from teenagers and children, its current market price appears to be substantially overvalued. Our discounted cash flow analysis suggests that ALGN’s intrinsic value is significantly lower than its current market price, potentially indicating a downside of -43.5% for investors. Therefore, caution is advised when considering ALGN as an investment opportunity in light of its stock’s high valuation.

Be the first to comment