Andrew Burton/Getty Images News

We continue to be bullish on Alibaba (NYSE:BABA). We expect China’s rapid reversal of its COVID restrictions to drive Alibaba’s stock further as the company’s main geographic source of revenue, China Commerce, recovers. We believe Alibaba is a Chinese stock that provides an attractive profile amid the tightening and volatile macro environment in the rest of the world.

Since we first published our buy rating on Alibaba in late November, the stock rallied 36% to date. We recommend investors ride the upward trend while the stock’s valuation is attractive. We see Alibaba outperforming toward 2H23 as China’s reopening serves as a key growth catalyst for Chinese stocks, and Alibaba is no exception.

The following graph outlines our rating history on BABA.

SeekingAlpha

Bull market for Chinese stocks materializing

We believe Asian-Pacific stocks are entering a bull market fueled by China’s rapid reopening, and expect Alibaba stock to continue to rally in response. In our previous note on Alibaba, our thesis was centered around Alibaba cloud and diversified revenue sources abroad. We now add another layer to our bullish sentiment: China’s efforts to rapidly exit the lockdown environment.

Bloomberg Economics expects China’s abrupt reversal of its COVID policy to pave the way to a full reopening by mid-2023. We expect China’s reopening to be a growth driver for Alibaba, as the company derives 65% of its total revenue from its China Commerce segment. In 2Q23, the company reported a 1% Y/Y decline in its China Commerce revenue. We believe China’s reopening and Chinese New Year festivities will boost revenue growth and fuel Alibaba’s recovery. We believe Alibaba and others in the e-commerce space, including JD.com (JD), will see demand tailwinds in 1H23. According to Pattern research, during the Chinese New Year, Chinese retail and e-commerce companies’ historical sales rose for “more than a decade until the COVID-19 pandemic struck in 2020.” We believe Chinese stocks will experience a rebound in sales this Chinese New Year as China’s economic slowdown becomes history. Sales of the Lunar New Year specialty, nianhuo, already surged 30% Y/Y on the company’s online retail platforms, Tmall and Taobao marketplace, in the first two weeks of January. Part of our bullish sentiment on Alibaba is based on our belief that domestic consumption will help revive the company’s revenue growth in 1H23.

Asian-Pacific’s leading index, the MSCI Asia Pacific index, already rose 7.2% this year as of February 9th, after declining 20% in 2022. In mid-January, the MSCI Asia Pacific Index grew nearly 21% from its 52-week low in October, according to data from Refinitiv. We believe this is a forward indicator that Chinese stocks are gradually entering a bull market, and we recommend investors buy Alibaba as an entry point into Chinese stocks.

We also believe Alibaba’s effort to launch a rival to ChatGPT is a good sign that the company’s headed in the right direction for long-term growth. The company will be among the latest in the tech space to join the chatbot bandwagon. We believe Alibaba has a long way to go before competing meaningfully with OpenAI’s ChatGPT or Alphabet’s (GOOG) new “Bard” tool. Still, we believe Alibaba working internally on cutting-edge innovations within the generative AI space has the potential to be a long-term growth driver, as the generative AI market is estimated to grow at a CAGR of 27% between 2023-2032.

Cloud is a slowly but surely long-term growth driver

We like Alibaba’s position in the cloud-computing space and its steps to invest $1B in its Alibaba cloud segment, but we expect the company’s cloud business to face near-term headwinds. We’re constructive on Alibaba’s cloud segment as it competes with the top players in the cloud-computing space, mainly Microsoft’s (MSFT) Azure, Amazon’s (AMZN) AWS, and Alphabet’s Google Cloud. Our concern regarding Alibaba’s cloud segment is not due to any shortcomings from the company, but due to the weaker spending environment resulting from macroeconomic headwinds. We believe inflationary pressures and heightened interest rates have materialized, weaker IT spending from corporate customers. We believe corporations are stingier when allocating budgets during current macroeconomic headwinds, with Canalys reporting that cloud computing’s “annual growth rate fell below 30% for the first time” in 3Q22. We don’t believe Alibaba is immune to the weaker spending environment and expect the company’s cloud business to be pressured in the near term.

The stock rallied after cutting voting power on Ant Group

We believe co-founder of Alibaba, Jack Ma’s decision to lower his stake in Ant Group is another positive growth catalyst. Alibaba stock rose by more than 2% after Ma’s exit from Ant Group on Monday. We believe Ma’s decision to cede control of Ant Group is positive for Alibaba and positions the company for more growth as it slowly ends the Chinese government’s crackdown on tech companies. We believe Ma’s been there for Ant Group’s woes, specifically back in 2020 with the last-minute cancelation of Ant Group’s $37B IPO. The cancelation took place after Ma made some comments about the Chinese regime. We expect Ma’s decision will likely improve Chinese authorities’ regulations on the tech space and even may suggest that China’s tech crackdown is over.

Valuation & Word on Wall Street

We believe Alibaba’s stock is relatively cheap. Based on Alibaba’s current enterprise value and its revenue TTM ending September 30th, the company’s EV/Revenue is 1.78x, while Amazon’s EV/Revenue is 2.1x. We expect Alibaba to be in an upward trend and recommend investors buy the stock at current levels.

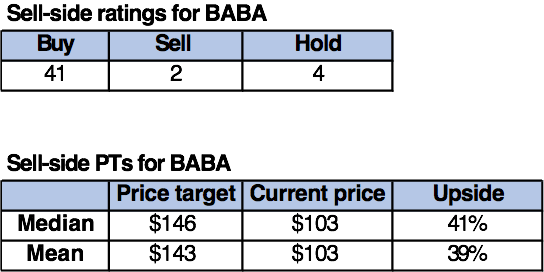

Wall Street shares our bullish sentiment on Alibaba. Of the 47 analysts covering the stock, 41 are buy-rated, four are hold-rated, and the remaining are sell-rated. The stock is currently priced at $103. The median sell-side price target is $146, and the mean is $143, with a potential upside of 39-41%.

The following table outlines the sell-side ratings and price targets for BABA.

TechStockPros

What to do with the stock

We’re bullish on Alibaba; we expect the stock to be driven higher as China lifts COVID regulations and moves towards a full reopening by mid-2023. We believe Alibaba is better positioned to grow meaningfully in 2023 as it expands its revenue sources and simultaneously regains revenue growth at home in its China Commerce segment. We also believe the stock is too cheap to ignore, providing a favorable entry point at current levels. The stock is up nearly 42% from its 52-week-low of $60.25. While investors are often hesitant about jumping into Chinese stocks, we believe Alibaba is worth the investment, as we expect Chinese stocks to enter a bull market in 1H23. We recommend investors buy the stock before it rallies further.

Be the first to comment