maybefalse/iStock Unreleased via Getty Images

Alibaba Group Holding Limited’s (NYSE:BABA) shares have been languishing in the last two years, dropping more than 62% from their all-time high of $317.14. Since November, however, shares of Alibaba have moved into a new up-leg and have more than doubled. The renewed optimism about Alibaba relates to the planned opening of the Chinese economy and the involvement of an activist investor: meme-stock billionaire investor Ryan Cohen reportedly bought a large stake in the Chinese e-Commerce company in 2022 and is pushing for aggressive stock buybacks to help Alibaba’s ailing stock. Alibaba has the free cash flow to execute a much bigger stock buyback, which could be, together with a full reopening of the Chinese economy, a potent catalyst for Alibaba’s shares!

Ryan Cohen investment in Alibaba and potential for higher stock buybacks

The Wall Street Journal last week reported that activist investor Ryan Cohen bought a stake worth hundreds of millions of dollars in Alibaba in the second half of 2022. Ryan Cohen is also apparently pushing the company to execute a large stock buyback in order to reverse Alibaba’s depressing stock trend.

While it was not reported what size of stock buyback Ryan Cohen is looking for, Alibaba does have the free cash flow necessary to do a lot more when it comes to stock buybacks. The e-Commerce company increased its stock buyback authorization from $15B to $25B in the first quarter of 2022 — which I have called a game-changer for the e-Commerce firm — largely in order to appease shareholders that were concerned about Alibaba’s moderating post-pandemic top line growth.

Alibaba has since purchased a considerable amount of its shares, but the company has the free cash flow to ramp its stock buybacks up much more. Alibaba repurchased 49.81B Chinese Yuan ($7.34B) of its shares in the first nine months of 2022. In Alibaba’s FQ2’23, the e-Commerce company repurchased 13.80B Chinese Yuan ($1.94B) of its shares.

Source: Alibaba

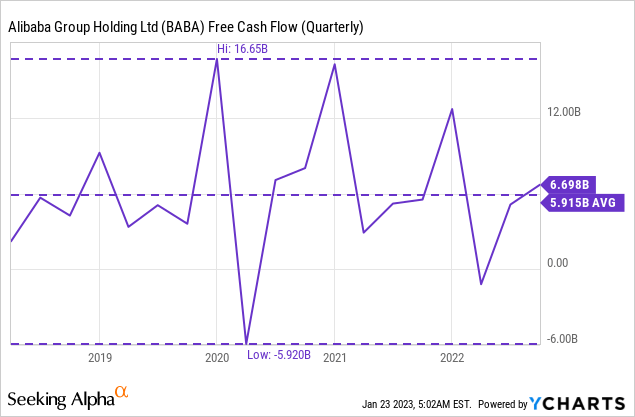

Alibaba can afford a major up-size in its stock buyback

Alibaba’s FY 2022 was not a great year for the e-Commerce company, considering the extent and length of COVID-19 lockdowns in China which drove Alibaba’s revenue growth down to zero in the June quarter. However, even in last year’s deteriorating operating environment, Alibaba generated 98.87B Chinese Yuan ($15.60B) in free cash flow. In FY 2020 and FY 2021, Alibaba reported free cash flow of 130.91B Chinese Yuan ($18.49B) and 172.66B Chinese Yuan ($26.35B). So, Alibaba could generate $5B a quarter or 20B a year in free cash flow relatively easily under the assumption that the Chinese economy reopens and pent-up demand is unleashed for Alibaba’s ailing Chinese commerce business. Alibaba’s Cloud business also has a lot of potential in the long term. Once the Chinese economy fully reopens, I believe Alibaba could relatively easily generate $5B a quarter in free cash flow… which is even less than its 5-year average free cash flow of $5.92B.

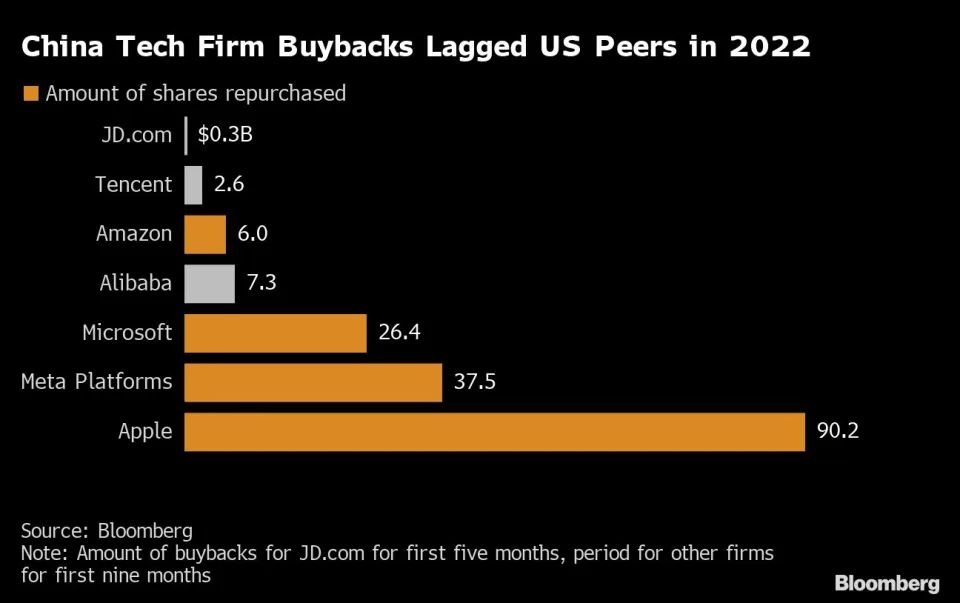

With $20B in annual free cash flow (“FCF”), I could see Alibaba announce a $50B stock buyback that would be the equivalent of just two and a half years’ worth of FCF. Compared to other tech companies, Alibaba has not paid as much attention to stock buybacks, but it should, considering how cheap the stock still is.

Source: Bloomberg

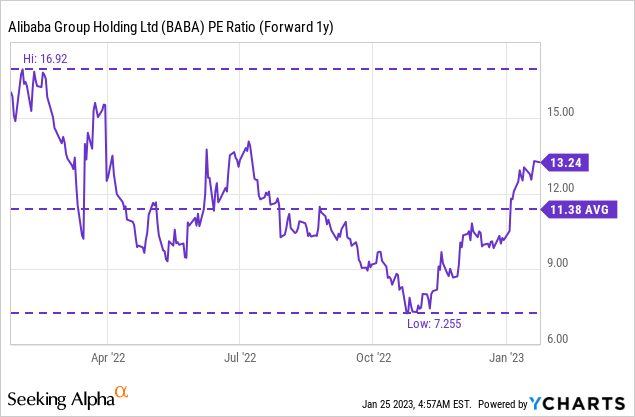

Stock buybacks could still be executed at a very favorable valuation

An increase in the stock buyback authorization would obviously make a lot of sense for Alibaba, since the company’s earnings prospects are valued at a P/E ratio of only 13.2 X. The stock, however, trades slightly above the 1-year average P/E ratio of 11.4 X. At such a low earnings multiplier factor, stock buybacks create value for Alibaba and its shareholders, and the company clearly has sufficient free cash flow to fund a stock buyback.

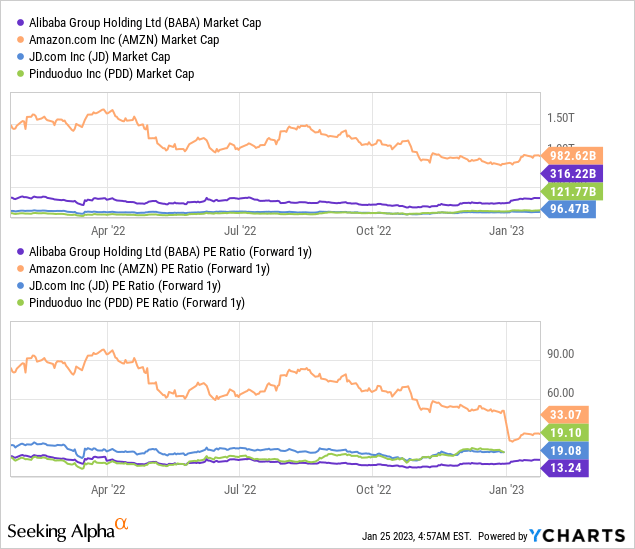

Alibaba’s e-Commerce prospects are also cheap relative to those of other e-Commerce firms in China as well as Amazon (AMZN). Alibaba has the lowest P/E ratio even when compared against other Chinese e-Commerce firms such as JD.com (JD) and Pinduoduo (PDD), suggesting that Alibaba’s downward revaluation has gone too far.

China reopening could be a major catalyst for Alibaba’s e-Commerce business

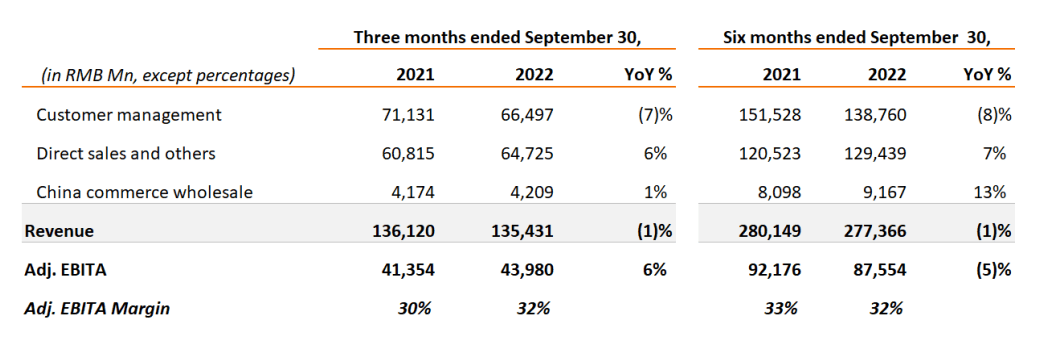

China is opening up its economy again, which could be a potent catalyst for Alibaba’s China-focused commerce business. The segment has seen a serious slowdown in FY 2022 due to Beijing’s draconian lockdown policies, but things could now finally be improving. In the September-quarter, Alibaba’s China commerce revenues declined 1% year-over-year, to 135.4B Chinese Yuan, and a reopening could reinvigorate the company’s e-Commerce sales. Alibaba’s commerce business accounted for 65% of consolidated revenues in the September-quarter, and no other segment even came close regarding revenue contribution.

Source: Alibaba

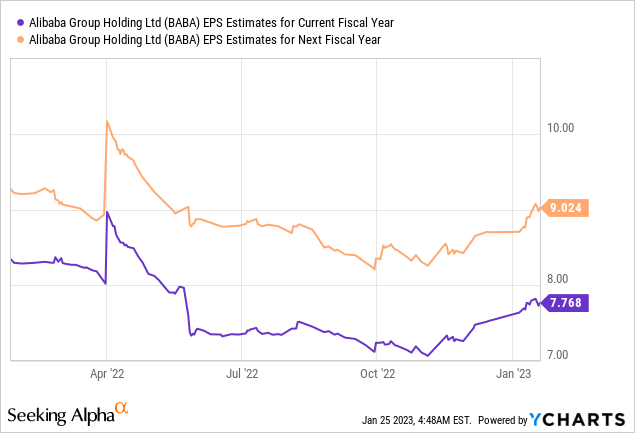

A reopening of China after 3 years of isolation could yield a surge in retail spending from which Alibaba would benefit handsomely. The EPS estimate trend is also improving, which I attribute to brighter earnings prospects for Alibaba in the context of a full economic reopening.

Risks with Alibaba

Alibaba Group Holding Limited stock has seen renewed upward momentum since November, likely in anticipation of a full reopening of the Chinese economy. However, challenges still exist and range from the possibility of new COVID-19 lockdowns in light of a surging number of COVID death to Alibaba’s dependency on the Chinese market for revenue regeneration. What would change my mind about Alibaba is if China’s economic reopening were to be delayed and if the company saw a steep decline in its free cash flow due to an economic slowdown or growing domestic competition.

Final thoughts

Almost exactly one year ago, Alibaba Group Holding Limited announced an increase in its stock buyback from $15B to $25B. It often takes an outside investor with significant clout to push for changes at a company whose stock price is languishing and an up-sized stock buyback could be a game-changer for Alibaba.

With the involvement of activist billionaire investor Ryan Cohen, Alibaba could announce a large buyback in 2023 and the e-Commerce firm has more than just one good reason to double down on stock buybacks: shares are cheap and investors are looking for a management statement of confidence in Alibaba.

Additionally, the impact of a higher stock buybacks could be compounded by a general reopening of China’s economy and the unleashing of pent-up demand that could support the firm’s ailing China-focused commerce business. Alibaba Group Holding Limited could easily afford to pay for a, say, $50B stock buyback financed by the company’s significant free cash flow!

Rating clarification: I currently have a hold rating on Alibaba, but I am prepared to upgrade my rating to buy/strong buy if the Chinese reopening proceeds as expected and Alibaba avoids a negative growth quarter in FQ3’23!

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment