NickyLloyd/E+ via Getty Images

Investment Thesis

Airbnb (NASDAQ:ABNB) reported Q4 results that took investors by surprise. Well, let me be honest with you and clarify my stance. It took me by surprise.

Author’s rating on ABNB

Previously, I was unenthusiastic about ABNB. But this set of results made me conclude that my bearishness was overdone.

Consequently, I’m now upgrading my investment rating to buy. Here’s why.

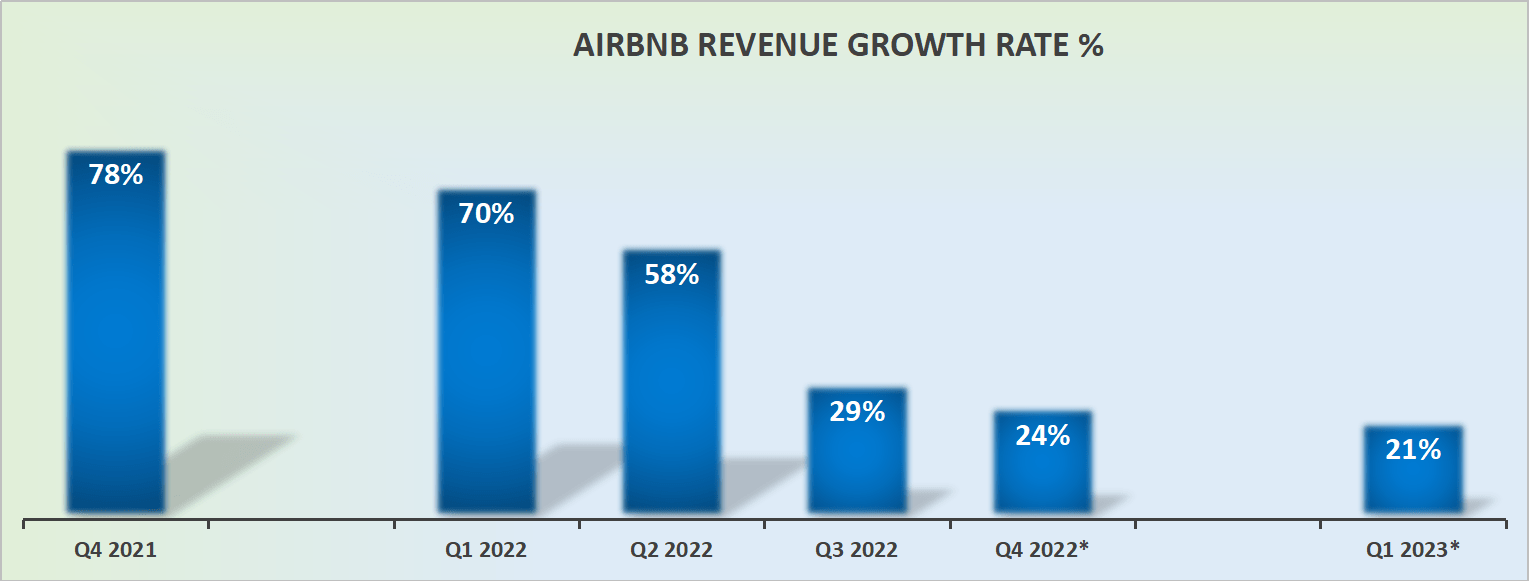

Revenue Growth Rates Impress

ABNB revenue growth rates

Airbnb is no longer a hyper-growth business. And that’s ok. What we see here is Airbnb’s GAAP revenues, not adjusted for FX changes.

The business is set to grow by up to 21% at the high end for Q1. Even if Airbnb doesn’t quite reach the very high end of its guidance and say, ends up growing at 20% CAGR near-term, that’s still dramatically higher than analysts’ estimates.

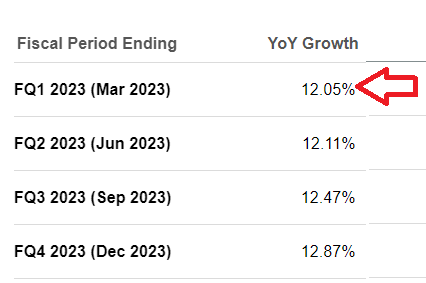

SA premium

Indeed, as you can see above, analysts expected around 12% y/y growth rates for Q1. Whereas ABNB guides for say 20%. That change from a midteens growth company to a ”premium” growth company, one that’s growing at 20% CAGR, is a narrative changer.

Does Airbnb Have A Moat?

The short answer is yes. The expanded answer is it depends.

I’m not talking about people that own the stock and are heavily wedded to the idea of Airbnb – held back through their commitment and consistency biases towards the company and the stock.

I’m talking about travelers that are price sensitive. I believe that Airbnb reaches very well into the middle demographics. Those that seek a high-quality experience, but that Airbnb does not compete particularly well during a cost of living crisis.

That being said, this is something that Airbnb’s management is aware of and expressed their view during the earnings call about the company’s strategy to drive increased affordability to future guests.

Here are some excerpts from the call that echo this sentiment,

So it’s more expensive for guests to stay on Airbnb than frankly, other places.

[…] we are now prioritizing better value listing in search results. So in other words, we’re going to take the total price in the total price into account when we’re prioritizing bookings.

[…] even as ADRs [pricing] might come down modestly through the year through — largely through mix, and maybe some through pricing. It’s just making sure that we’re being really rigorous in our cost structure to kind of support declining ADRs

The three quotes above reflect my argument. On the one hand, Airbnb does have to compete at the lower end of the scale — and the high-end too, of course.

But Airbnb is repositioning itself to gain more market share during a down cycle.

In fact, if you think about it, it’s the ability to gain market share in a down cycle, where a company truly gains intrinsic value. And with intrinsic value in mind, we’ll turn our focus to discussing ABNB’s stock valuation.

ABNB Stock Valuation — 27x This Year’s EBITDA

Throughout its earnings call, ABNB reiterated several times that despite having lower expected pricing power for 2023, ABNB’s ability to streamline costs would allow the company to deliver EBITDA in line with 2022.

Put another way, the company expects approximately $3 billion of EBITDA, leaving ABNB on a 27x EBITDA multiple.

Now, here’s where things get interesting. The way Airbnb’s business model works extremely well is that Airbnb collects upfront cash from the guests. That means that there’s a lag between the cash collection and the payment of the host. Recall, the host only gets paid once the guest checks in.

Consequently, that lag provides Airbnb with negative working capital. Thereby leaving Airbnb priced at approximately 24x this year’s free cash flow (according to my own estimates).

The Bottom Line

In the past 2 years, Airbnb has been a poor stock. The stock has been consistently moving down and as such investors have lost their enthusiasm. Few investors are going to react and reach for this name right now.

Consequently, with the stock now ”derisked”, with its multiple compressed, this is a much better setup. Paying 24x free cash flow for a business with some sort of moat, that’s still growing at +20% CAGR, is a mightily attractive entry point.

Be the first to comment