Sjo/iStock Unreleased via Getty Images

Investment Thesis: While the rebound in sales growth for Air France-KLM (OTCPK:AFLYY) has been encouraging – I see little case for upside in the short to medium-term.

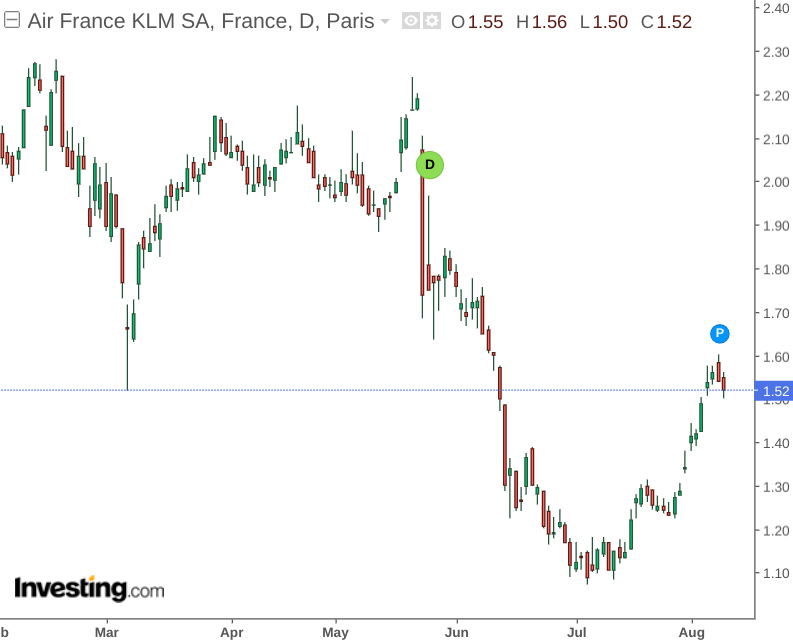

In a previous article back in June, I made the argument that Air France-KLM could continue to see volatility in its stock price as a result of ongoing travel disruptions due to high demand and labour shortages.

I also cited that Q2 figures are likely to give a good indication as to whether the revenue growth that we saw in the previous quarter is set to continue. Investors are also likely to pay attention to debt levels, in order to ensure that the company can finance such revenue growth without having to bolster debt levels.

While we saw the stock decline into July, we have seen a rebound since then:

Investing.com

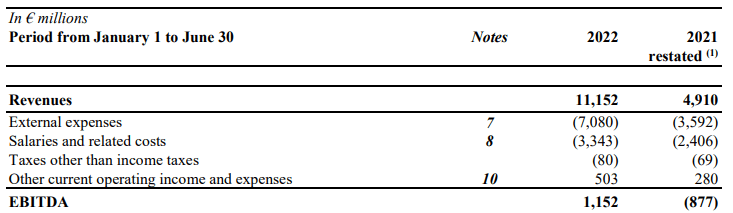

The purpose of this article is to assess whether Air France-KLM could continue to see a rebound in growth based on the two catalysts that I previously cited as potentially boosting the stock – namely a recovery in revenue growth as well as a decline in lease debt levels relative to total assets. Note that the above stock as well as financial statement figures cited in this article are given in euros.

Performance

From a revenue standpoint, we can see a strong boost from levels seen for the first half of 2021:

Air France-KLM: Consolidated Financial Statements January – June 2022

While net income was still negative, the company greatly reduced its net income loss from -€5.87 to -€0.42.

From a cash standpoint, the quick ratio (cash minus inventories all over current liabilities) has declined slightly. While cash and cash equivalents increased – this was accompanied by an increase in total current liabilities. As such, the company has slightly less cash available to fund its current liabilities.

| Dec 2021 | Jun 2022 | |

| Cash and cash equivalents | 6658 | 8173 |

| Inventories | 567 | 654 |

| Total current liabilities | 11726 | 15335 |

| Quick ratio | 0.52 | 0.49 |

Source: Figures sourced from Air France-KLM Consolidated Financial Statements January – June 2022. Quick ratio calculated by author.

While the quick ratio has declined slightly – this is somewhat expected given that servicing the rebound in revenue growth will necessarily incur higher costs. Given that the quick ratio has only fallen marginally – I take the view that investors are more focused on revenue growth at this point in time, and the fact that cash levels themselves have still grown since December is encouraging.

When looking at non-current lease debt relative to total assets – we can see that the ratio has increased – albeit slightly. On the whole, the increase in lease debt has been accompanied by an increase in total assets.

| Dec 2021 | Jun 2022 | |

| Non-current lease debt | 2924 | 3335 |

| Total assets | 30683 | 34350 |

| Non-current lease debt to total assets ratio | 9.53% | 9.71% |

Source: Figures sourced from Air France-KLM Consolidated Financial Statements January – June 2022. Non-current lease debt to total assets ratio calculated by author.

Looking Forward

Overall, Air France-KLM has managed to strongly bolster revenue growth while maintaining its cash reserves and controlling its longer-term debt levels – which is encouraging.

Going forward – while performance in July and August are likely to sustain revenue growth heading into Q3 – the seasonal lull in travel in the winter months may place downward pressure on revenue for the second half of the year as a whole.

Given that Air France-KLM is still technically loss-making – it does not make sense to attempt to value the company on an earnings basis at this time.

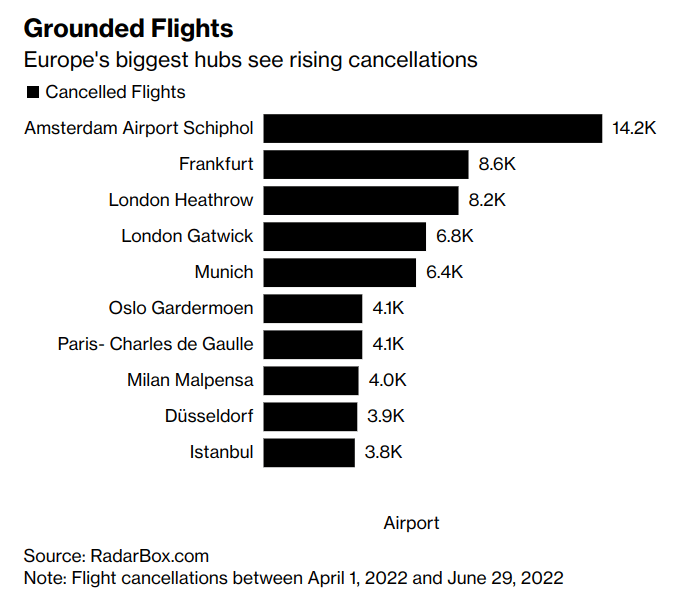

In terms of performance vis-a-vis the company’s competitors – cancellations and travel caps could stand to limit revenue growth for the remainder of the summer months. When looking at cancellations across major airport hubs across Europe – we can see that Amsterdam’s Schiphol Airport (which is KLM’s primary hub) has seen the most cancellations:

Bloomberg.com

Moreover, KLM itself has reportedly cancelled more flights than other major airlines in Europe.

Additionally, the company reports that reimbursing customers for such cancellations has cost the airline over €70 million during Q2 2022.

From this standpoint – while the company has seen a strong uptick in revenue as a result of the rebound in travel demand – there is a risk that the rebound in sales growth could plateau if customers increasingly opt for other airlines due to perceived cancellation risk through booking with KLM.

Conclusion

To conclude, Air France-KLM has seen a strong rebound in revenue growth and has maintained a steady cash position.

However, earnings still remain negative and until we see evidence of a significant reduction in flight cancellations – then I take the view that the stock may have limited upside in the short to medium-term.

Be the first to comment