bodnarchuk

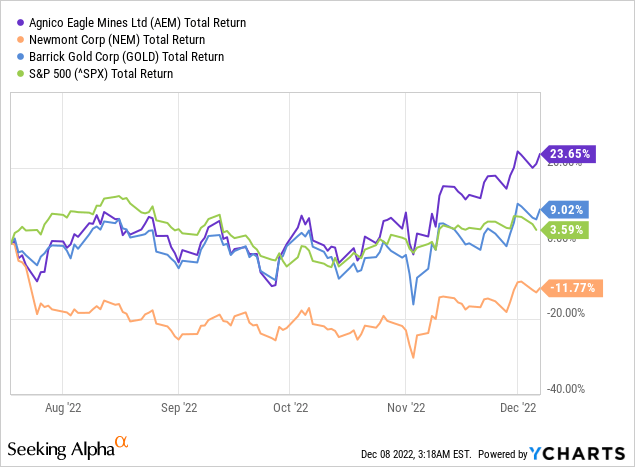

It has been less than six months since I outlined my investment thesis for Agnico Eagle Mines Limited (NYSE:AEM). While the broader market remained relatively flat during this period and many tech giants struggled, AEM delivered nearly 25% return.

Not only that, but investing in high quality producers also paid off on a relative basis, with Agnico outperforming both Newmont Corp. (NEM) and Barrick Gold (GOLD) during the period.

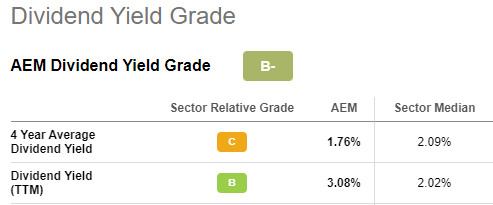

It is also worth noting that AEM also pays one of the highest dividends within the sector with its current dividend yield standing above 3%.

Seeking Alpha

Not only is this impressive for the highly cyclical industry, but AEM has been paying dividends for 38 years which makes it attractive even for investors looking for consistent passive income.

To have growth potential from existing mines and a high quality exploration program, I think you’ve seen that we have largely built this company over many decades through the drill bit and we’re continuing to do that. And a long history of capital returns, 38 years of dividend payments without missing a beat. And we’re very proud of that.

My investment thesis for AEM, however, does not solely rely on the high quality business model and what is in my view best-in-class long-term strategy. The current macroeconomic environment is also favorable for the price of precious metals and gold in particular which could provide a major tailwind on Agnico’s back.

The Attractive Cash Flow Perspective

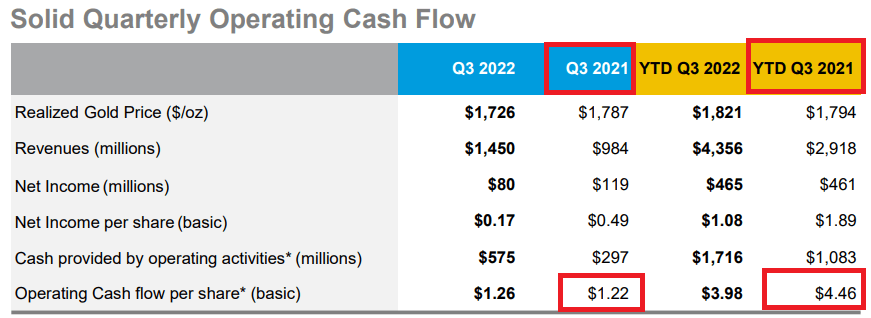

Agnico is already delivering strong results, following the recent merger with Kirkland Lake Gold and the recent offer for Yamana Gold was well-received by the market. During the last quarterly results, AEM reported $1.22 of operating cash flow per share. On an annualized basis this results in cash flow per share at around $5, when AEM trades just slightly $50.

Agnico Eagle Mines Q3 2022 Presentation

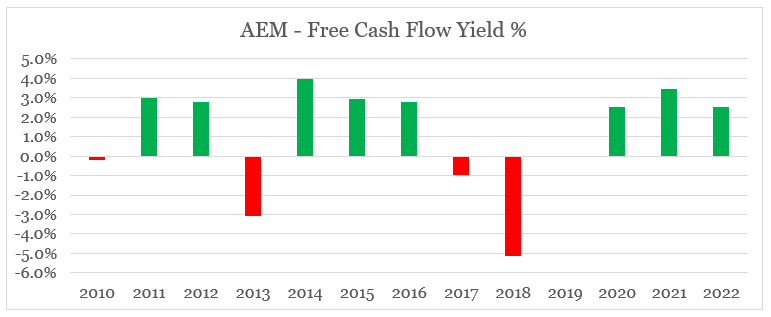

As a result, AEM still trades at very attractive levels on a free cash flow basis.

prepared by the author, using data from SEC Filings

The high free cash flow comes in spite of the strong pipeline of both expansion projects and drill initiatives.

Agnico Eagle Mines Q3 2022 Presentation

Operating costs also remain under control with AISC per ounce still expected to be within the previously provided guidance and well below those of Agnico’s major peers.

Due to cost inflation in 2022, total cash costs per ounce and AISC per ounce are now expected to be near the top end of the guided ranges of between $725 and $775 and $1,000 and $1,050, respectively.

Source: Agnico Eagle Mines Q3 2022 Earnings Release

High Dividend, Low Debt

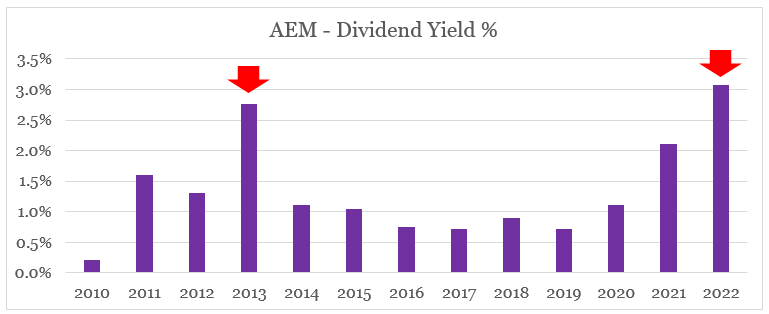

As I mentioned earlier, AEM pays one of the highest dividends within the sector with current dividend yield standing at above 3%. The last time the dividend yield was that high was back in 2013 when Agnico’s share price hit near rock bottom at around $26 per share.

prepared by the author, using data from Seeking Alpha and SEC Filings

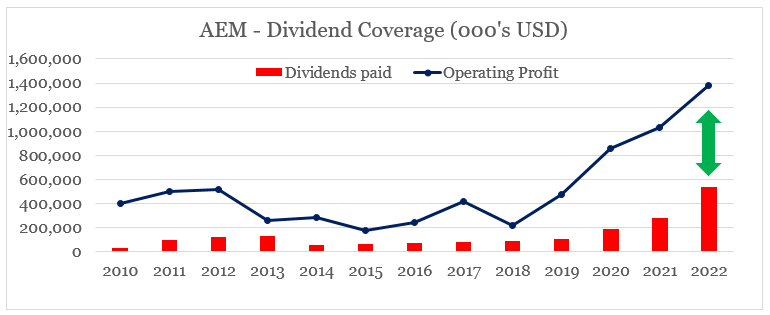

The highly cyclical nature of the industry will always overshadow high dividend yields within the sector, however, in the case of AEM the management has remained prudent with the amounts distributed to shareholders relative to profits.

prepared by the author, using data from SEC Filings

When talking about risk, there are two very important areas that should always be mentioned:

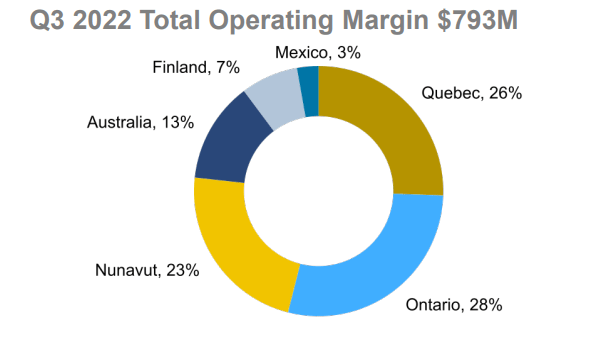

- the first is the company’s exposure to primarily low-risk jurisdictions;

Agnico Eagle Mines Q3 2022 Presentation

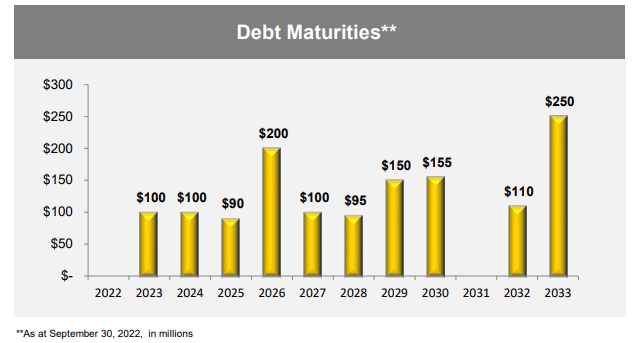

- and second, is the relatively low leverage of the company with debt maturities evenly spread through 2033.

Agnico Eagle Mines Q3 2022 Presentation

The management also remains committed to slowly paying down its debt through the use of internally generated cash flow.

Financial position remains very strong. We have paid down another $100 million of debt as it came due. We told all of you we are planning to pay our debt as it comes due through cash flow and that’s what we’re doing.

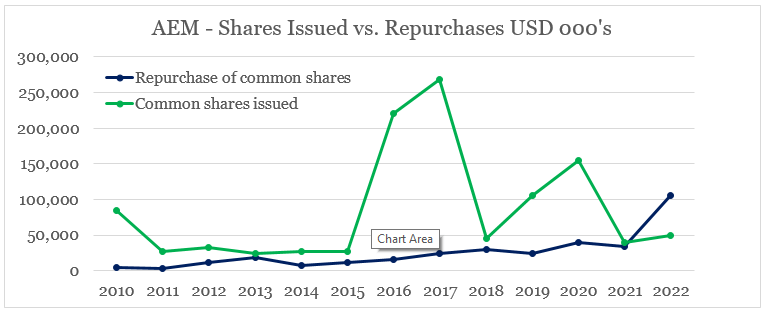

Last but not least, shareholders have been pleasantly rewarded by the company’s recent share repurchase program. As we see from the graph below, AEM management has not engaged in share repurchases in a very long time and the total amount spent on buybacks now significantly outpaces the amount received from share issuance.

prepared by the author, using data from SEC Filings

* common shares issued includes proceeds on exercise of stock options

Conclusion

In my view, Agnico Eagle Mines is one of the most attractive investment opportunities in the gold mining sector from a risk-reward point of view. The disciplined capital allocation approach results in low costs per ounce, while at the same time the company has a strong pipeline of future projects. High cash flow generation also allows for increased shareholder disbursements in the form of both dividends and share repurchases. It should also be mentioned that the management has achieved all that without loading up on debt and most importantly, without compromising the low jurisdiction risk of the company.

Be the first to comment