Solskin

The past year has not been particularly pleasant for shareholders of agilon health, inc. (NYSE:AGL). Over this window of time, shares are down around 81%. This is despite rapid growth that the company has achieved from both a revenue and membership perspective. The business that it’s in does have excellent potential in the long run. But this doesn’t mean that the company makes sense to buy into.

Despite attractive revenue growth, profitability remains a major issue. In 2023, the company booked a massive net loss and saw significant cash outflows. The good news is that the company does have cash on hand to work with. On top of this, some key metrics are showing nice signs of improvement. But given how much cash flow the company would need to generate to be even fairly valued, it could take a long while before it becomes a decent prospect, even after the massive decline in price.

agilon health – An interesting business in a fascinating space

Ever since I took a healthcare economics class while in graduate school, I found the structure and function of the U.S. healthcare system to be fascinating. I long for the day that we can have a universal single-payer system. But meanwhile, it’s important to note that there are companies out there seeking to make a positive difference for the industry in the form of quality care and cost-cutting. It just so happens that agilon health is one of these firms.

According to management, the company focuses on catering to Medicare recipients, specifically Medicare Advantage recipients. What it does is form what it calls RBEs (risk-bearing entities) based on geographic areas. The company essentially partners up with physicians and physician groups to create a model where they take over the costs of health care so that physicians can focus on providing the best care they can without regard to being incentivized to provide suboptimal or unnecessarily costly care. The company, in turn, partners up with insurance companies, mostly those that offer Medicare Advantage programs, and agrees to essentially cap the exposure of those insurance companies to an agreed upon capitated monthly payment for each member. This shifts the risk from both insurers and physicians onto the firm.

This business model is based on the idea that, in the U.S. healthcare system, there’s a lot of waste. For instance, as opposed to universal single-payer systems that often prioritize preventative care, the U.S. is reactionary. We often wait until something goes wrong before we act on healthcare because of a desire to save money and the hope that nothing horrible will happen to us.

Imagine it like a car. You can drive around and never do anything to it other than fill up the gas tank. But if you don’t take care of it, eventually you will have some critical failure that renders you immobile or that causes a crash. But if you get the oil changed regularly, replace the tires as you should, take it in when you hear an odd noise in the engine, and get the brakes checked, your short-term costs may be higher, but your long-term costs could be far lower.

By taking on the risks associated with healthcare from payers and physicians, agilon health hopes to benefit from this long-term cost reduction. In addition to this, they believe that the entire process of managing these RBEs will also reduce operational costs associated with their partners. And they hope to essentially capture some spread between the cost of taking care of those activities and the benefit in the form of reduced expense that comes with specialization.

Some of the patients that the company covers fall under its ACO REACH model. Under this system, the Centers for Medicare & Medicaid (the CMS) contract directly with ACOs (Accountable Care Organizations) in a scenario that allows each ACO to select risk sharing and fee payment options for fee-for-service Medicare beneficiaries. Until 2025, physicians will bill the CMS at an applicable rate for their services, with the CMS then paying back to the physician, with some remaining portion payable to the ACO itself. This is based on a fee-for-service setup.

But by next year, that fee-for-service model will disappear and a guaranteed per beneficiary per month payment will be made for each Medicare patient to the ACO, with the ACO remitting a portion of that payment to the physician in question.

For those who are skeptical about this business model, it’s worth noting that there is a lot of evidence in favor of this and the broader concept of value-based care. For those not familiar, value-based care is a form of health care that rewards providers based on the health of the patients in question. Instead of focusing on one specific issue, it focuses on their broader health overall. And this goes back to the idea of offering preventative care.

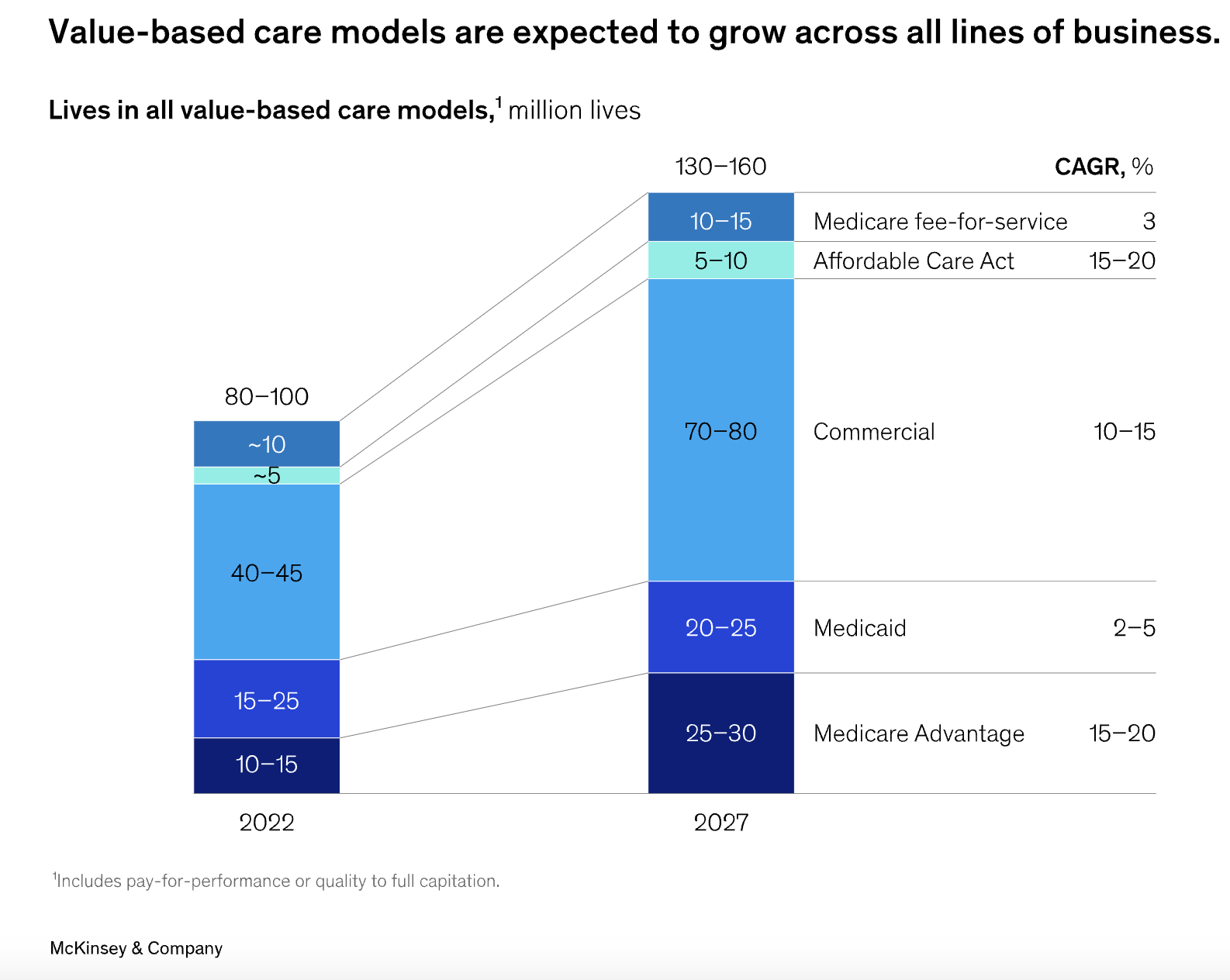

According to one source, investments in this space have risen significantly. Between 2019 and 2021, for instance, investments into value-based care more than quadrupled. Private capital inflows into value-based care assets jumped from 6% of all capital investments that were made in hospitals to approximately 30% in that two-year window of time.

McKinsey

This surge was due in part to the pandemic. The idea of consistent and stable cash flows at a time when elective surgeries and procedures that did not need to be done immediately dried up because of the pandemic appealed to the medical space. But it was more than just that. According to some estimates, value-based care can save significantly when it comes to healthcare costs, with some savings estimates coming in as high as 20% of overall costs. That same source also indicated that the margin from value-based care adoption could grow to as high as $1 trillion by 2027, with the largest chunk of that involving the Medicare Advantage space.

In fact, it is so attractive that it’s believed that value-based care models will become more popular across all lines of business in the medical space. For instance, as measured by the number of lives covered, it should grow from between 40 million and 45 million in the commercial space in 2022 to between 70 million and 80 million by 2027. Some of the fastest growth, however, will involve Medicare Advantage, with the number of lives under this system growing from between 10 million and 15 million to between 25 million and 30 million. That would imply an annualized growth rate of between 15% and 20%.

agilon health

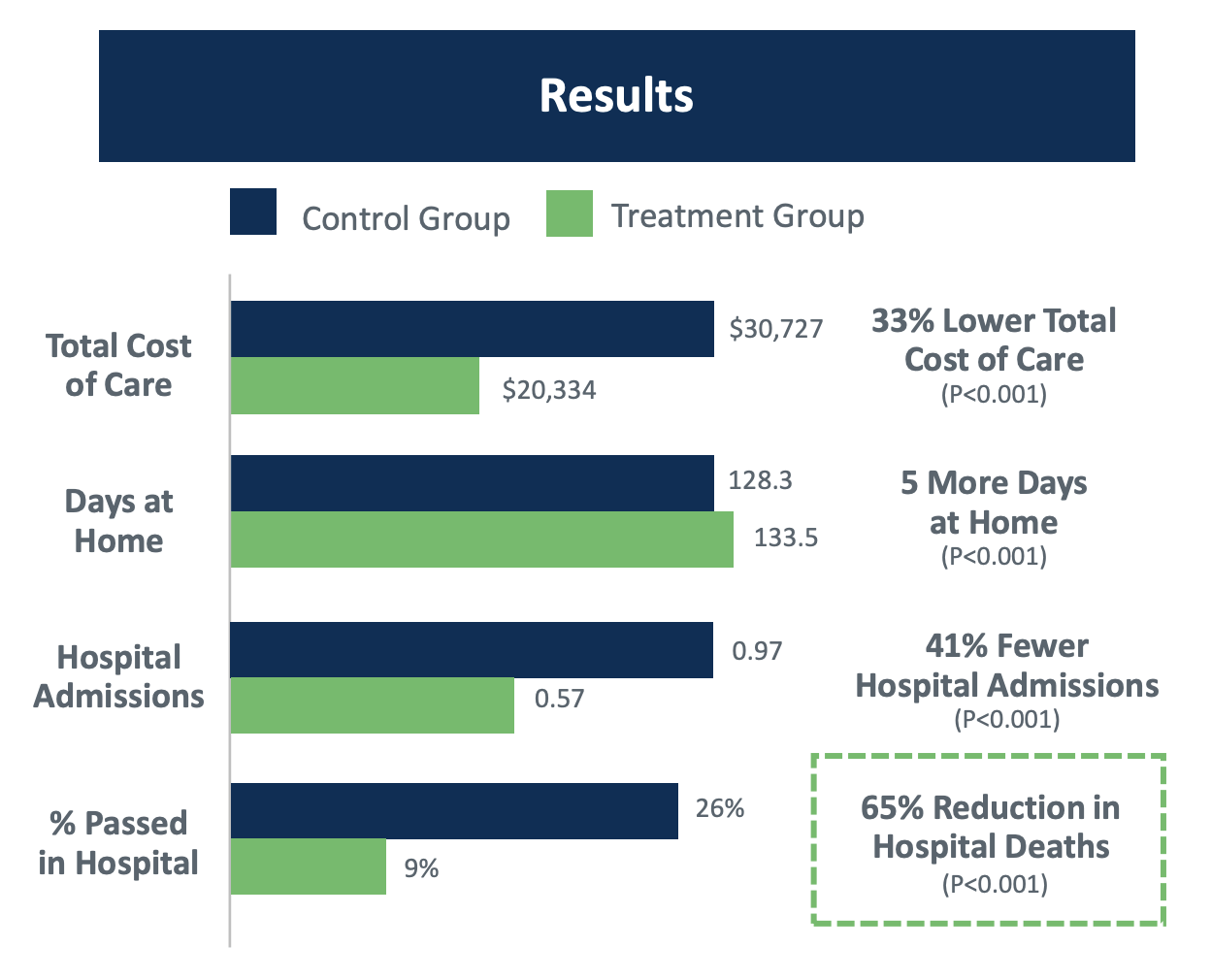

When it comes to investing, we can often get fixated on the economic argument. But this isn’t just about cost-cutting. It’s also about health outcomes. According to estimates provided by agilon health, using a total cost of care model like what it employs can reduce overall cost of care by roughly 33%. It means 5 fewer days each year in the hospital for Medicare recipients and results in 41% fewer hospital admissions. You would think that this would result in some negative consequences. However, it’s also associated with a 65% reduction in hospital deaths.

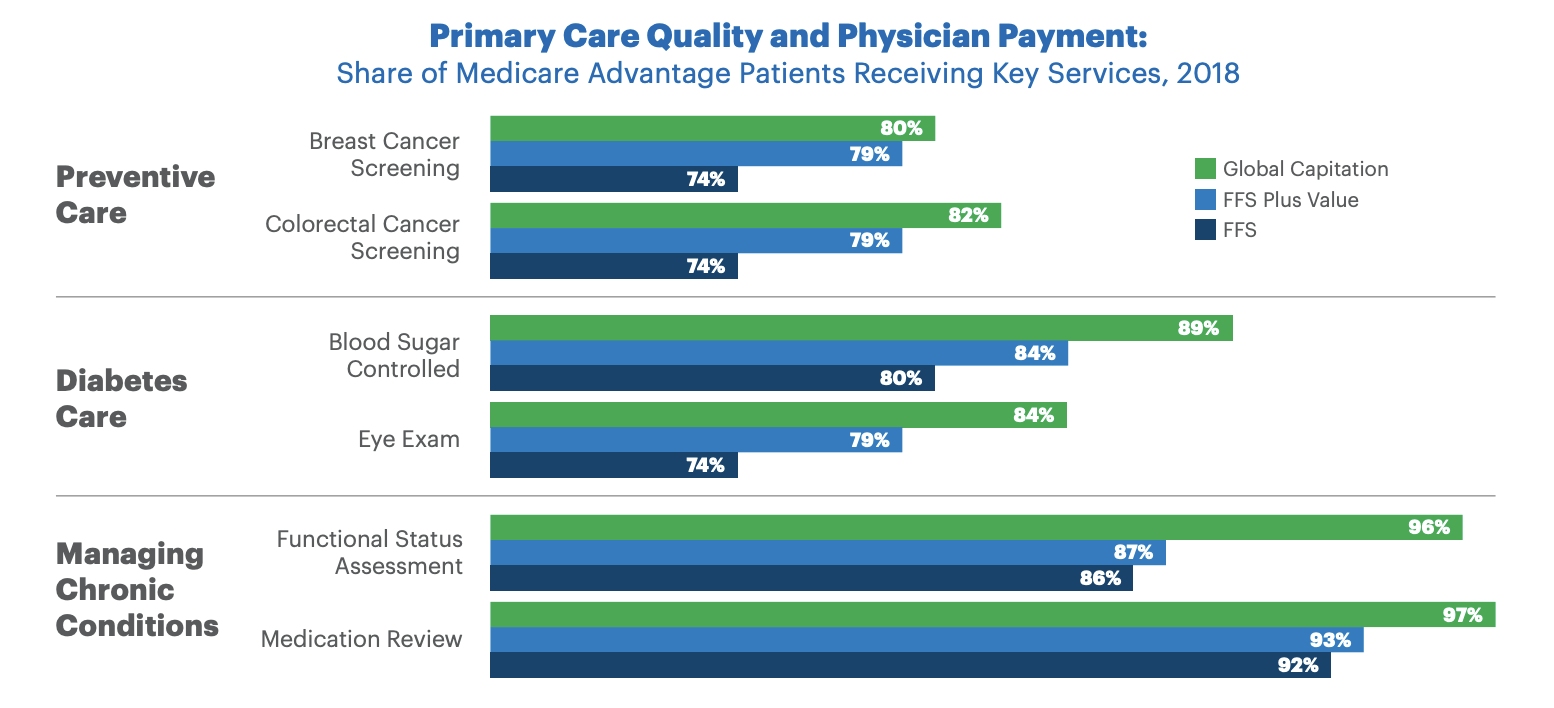

Another firm, UnitedHealth Group Incorporated (UNH), has provided some of its own calculations regarding a global capitation system like what agilon health employees. Under this system, 80% of Medicare Advantage patients that should receive breast cancer screening ultimately do. This compares to 79% for those that are under a fee-for-service plus value system, and it’s up from 74% compared to just fee-for-service ones.

In the image below, you can see some similar results when it comes to colorectal cancer screening, blood sugar control, eye exams, and other factors. In short, patients get the services they need to prevent getting really sick. And in the long run, that cuts expenses. Despite all of these positives, one negative is that this model does tend to compensate primary care physicians at a rate that is lower than alternative means. The hope is that, as cost-cutting becomes more effective, this problem will be mitigated or disappear entirely. But it is a problem nonetheless.

UnitedHealth

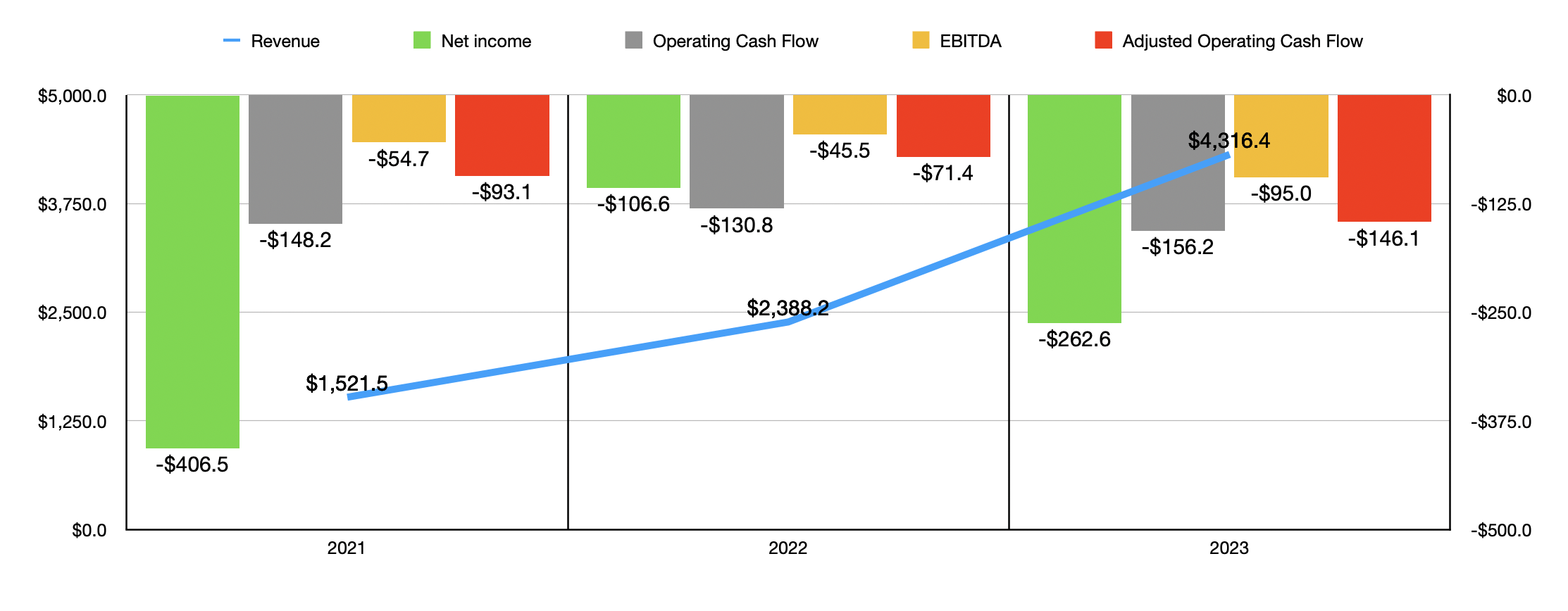

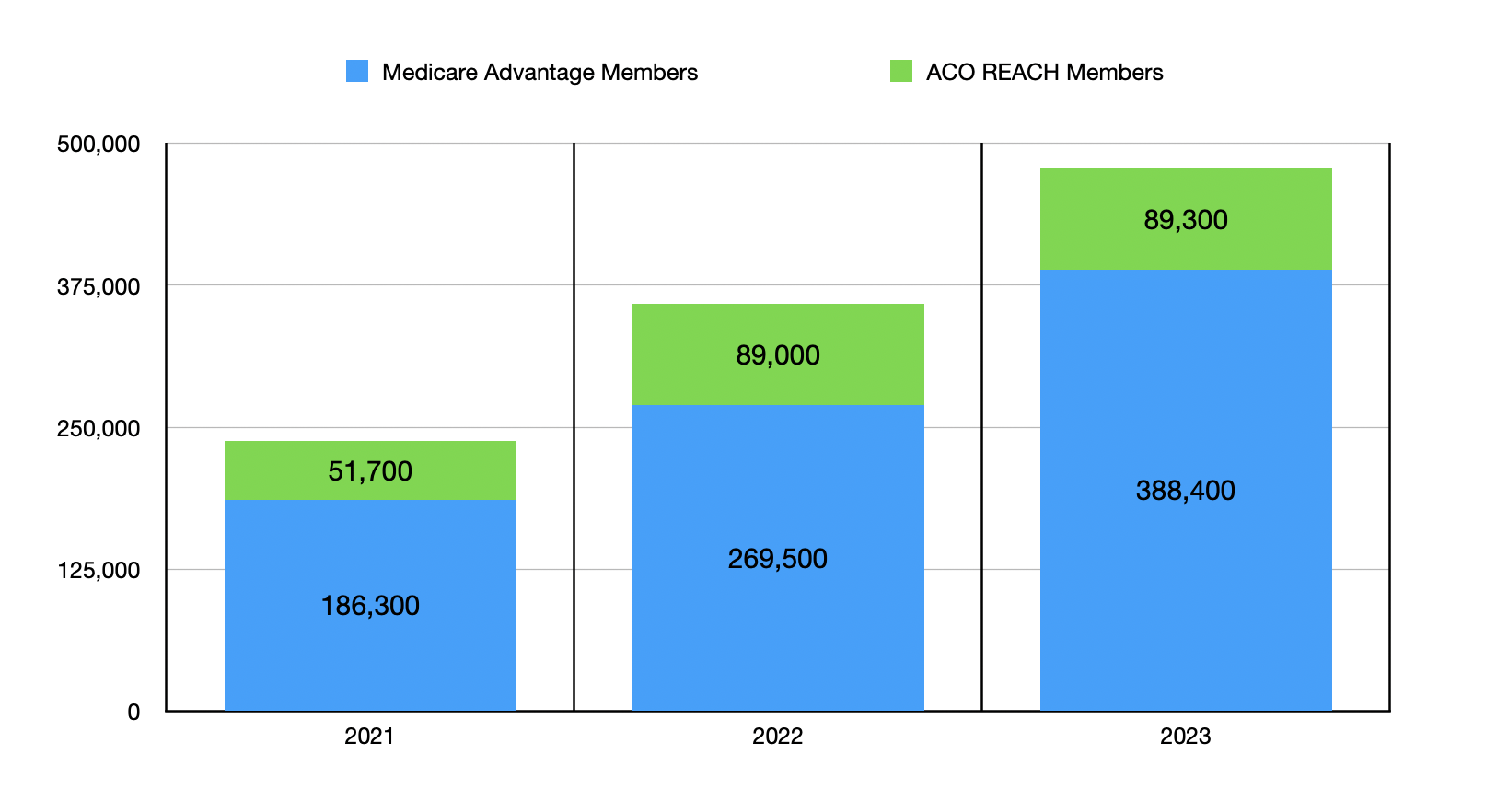

When it comes to agilon health on its own, the company has done really well lately. The business went from generating $1.52 billion worth of revenue in 2021 to $4.32 billion in 2023. This growth occurred as the number of patients that it has exposure to jumped from around 238,000 in 2021 to 477,700 in 2023. Over the same window of time, the number of primary care doctors under this arrangement jumped from 800 to 1,700.

Unfortunately, a growth in revenue does not necessarily mean that the bottom line for the company is going to improve. It is true that net income went from a loss of $406.5 million in 2021 to a loss of $262.6 million last year. But the 2023 figure was actually worse than the $106.6 million loss generated in 2022.

Author – SEC EDGAR Data

Other profitability metrics have also been disappointing for the most part. From 2021 to 2023, the company saw operating cash flow worsen marginally from negative $148.2 million to negative $156.2 million. But if we adjust for changes in working capital, we would see the outflow expand from negative $93.1 million to negative $146.1 million. Meanwhile, EBITDA for the business went from negative $54.7 million to negative $95 million.

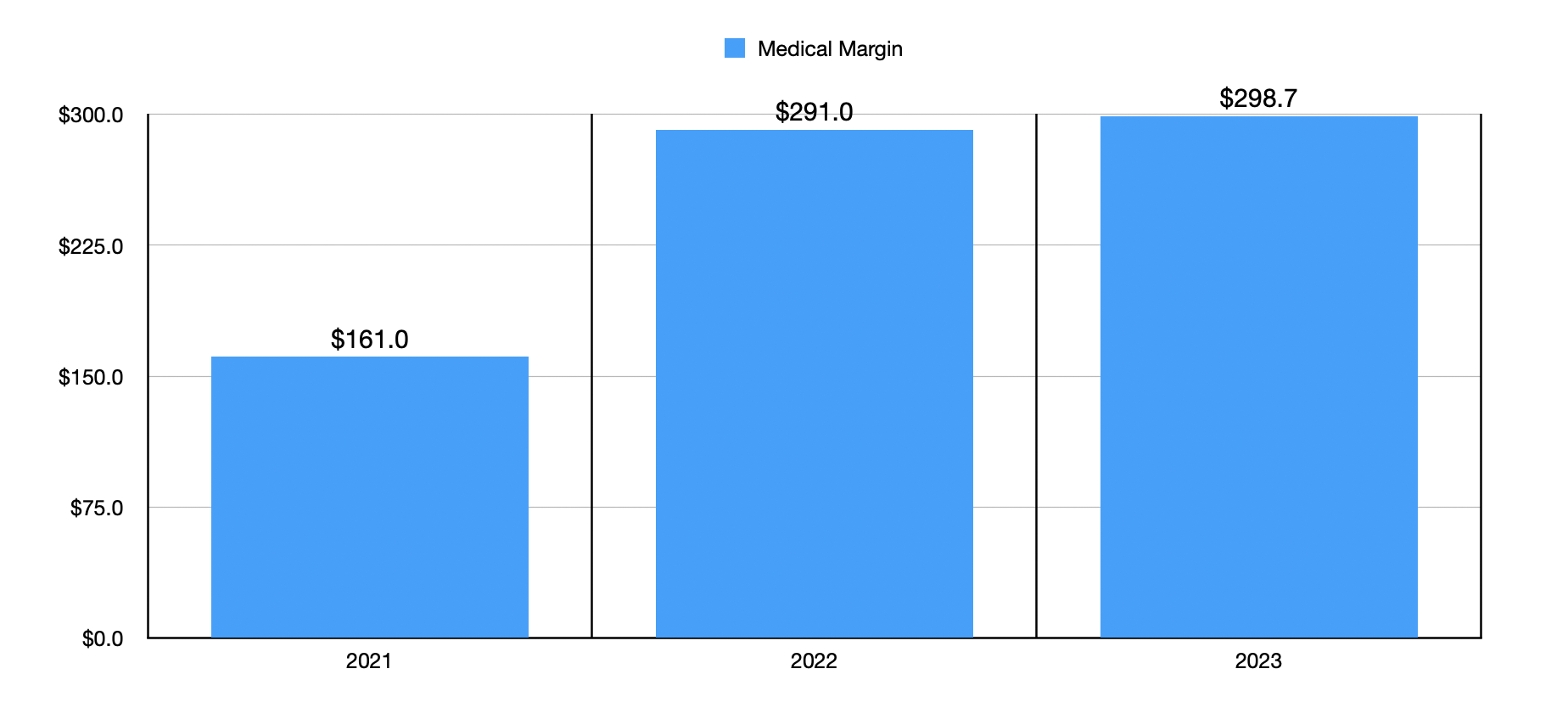

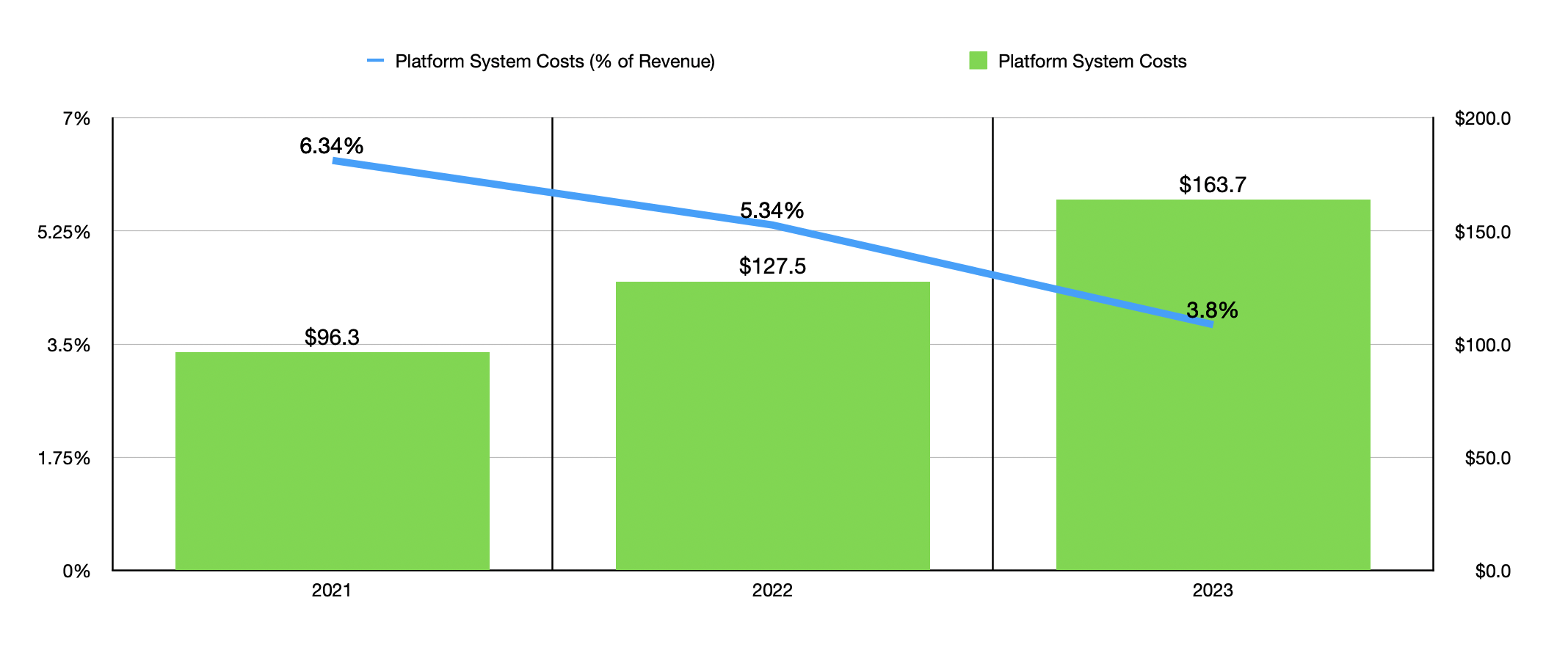

This is not to imply that there weren’t improvements elsewhere. In actual dollar amounts, the medical margin achieved by the company went from $161 million to $298.7 million. This is essentially the spread between revenue and the actual medical expenses that the company has to pay out. In addition to this, while the platform support costs of the business grew from $96.3 million to $163.7 million, that actually represents a decline from 6.34% of sales to 3.80%. This means that the company is seeing some benefit from an increase in its size.

Author – SEC EDGAR Data Author – SEC EDGAR Data

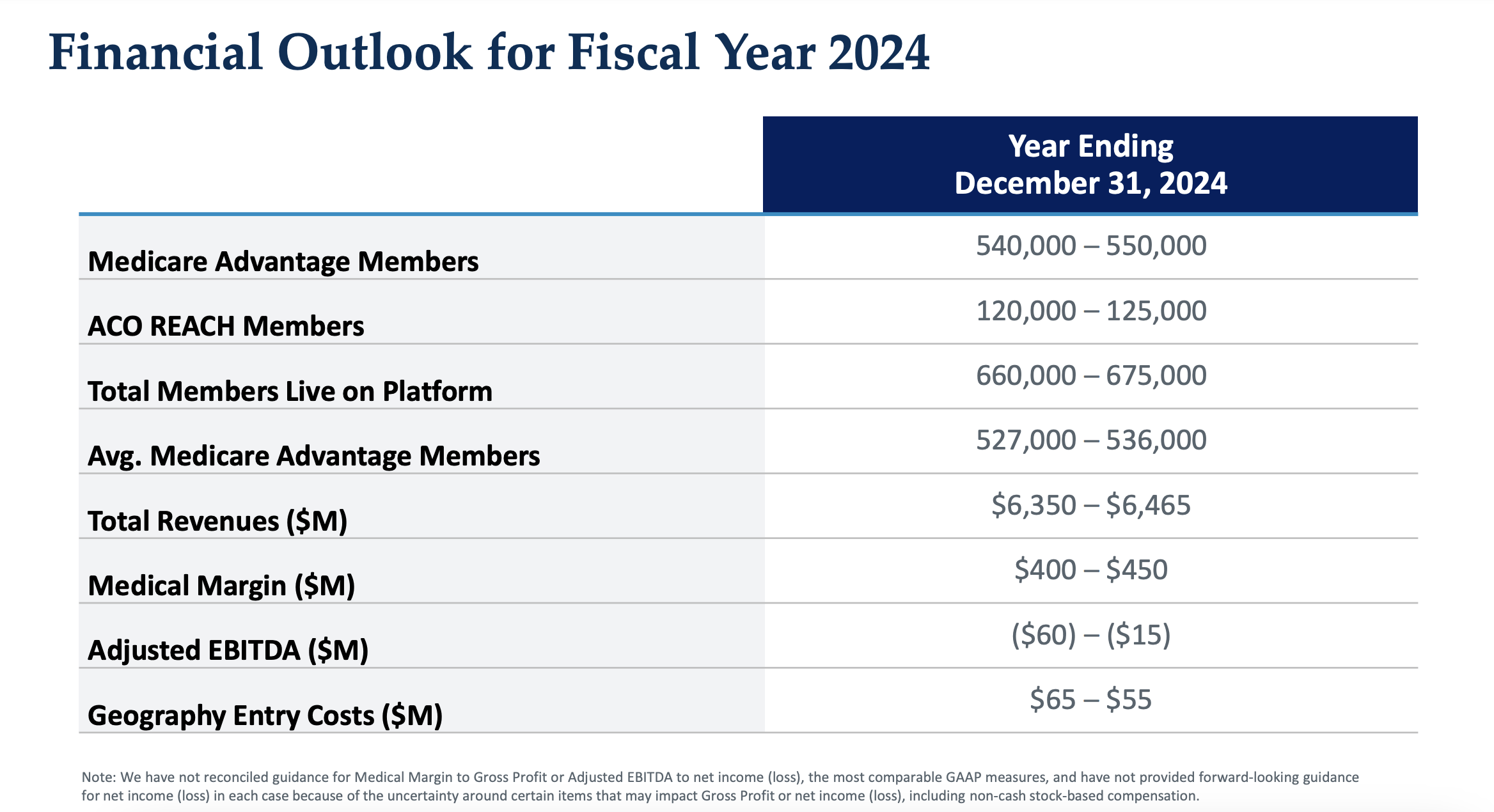

When it comes to the future, management seems quite optimistic. They believe that, this year, their model will cover around 667,500 patients at the midpoint, with around 545,000 of them being Medicare Advantage members and the remaining classified as ACO REACH. But this doesn’t necessarily translate to profitability. It ultimately depends on what the costs are. And so far, the company is still bleeding cash.

The good news is that, even after factoring in debt, it has excess cash of $456.5 million. That does help to reduce the risk for shareholders, especially those in it for the long haul. But it does not translate into the company, making for an appealing opportunity.

Author – SEC EDGAR Data

Author – SEC EDGAR Data

*$ in Millions.

The reason why I say this is that, even if the company were to achieve cash flow neutrality, the stock as it would likely be overvalued. In the table above, you can see how much operating cash flow the company would need to generate to trade at a price-to-operating cash flow multiple of either 10 or 15. And you can see the same thing for EBITDA using the EV-to-EBITDA approach.

It is true that the company is starting to move in that direction. This year, for instance, it’s expected to generate between $6.35 billion and $6.47 billion worth of revenue. That should allow a medical margin of between $400 million and $450 million, with EBITDA that would be negative by between $15 million and $60 million. That is significantly above what the company is accomplishing today.

Meanwhile, there are plenty of other healthy companies out there that don’t have cash outflows and other growth pains. And those trade at reasonable multiples.

agilon health

Takeaway

Fundamentally speaking, I’m not a huge fan of agilon health. I think its business model is interesting and this is a space where a lot of money can be made for the right firms. Assuming that the company doesn’t eventually run out of cash, I think it probably will reach the point of being a successful enterprise that is cash flow positive.

But that could take a couple of years still and, in that time, the upside for investors elsewhere could be more significant. Because of this, I am assigning this a speculative “hold” rating. This means that I am bearish about the agilon health, inc. fundamentals, and the opportunity for investors to get good returns for the foreseeable future. But I am bullish about the agilon health, inc. business model and growth prospects in the long run.

Be the first to comment