niphon

Investment Thesis

Advanced Drainage Systems’ (NYSE:WMS) stock price has corrected significantly from its 52-week high of $153.36 made in August and the stock is currently trading in the low 80s. The company is witnessing inventory destocking in its infiltrator segment as well as a shifting of demand to later quarters due to Hurricane Ian. While the company is facing near-term revenue headwinds, its long-term growth drivers are intact. The business is benefiting from secular trends around the transition from concrete pipe and septic tanks to more durable and cost-effective plastic pipe and septic tanks. The stock is trading at a 9.13x EV/EBITDA (TTM) multiple which is at a significant discount to the 5-year average EV/EBITDA multiple of 15.45x. I believe long-term investors can use the current decline to buy this long-term growth story at an attractive valuation.

Long-term growth versus short-term headwinds

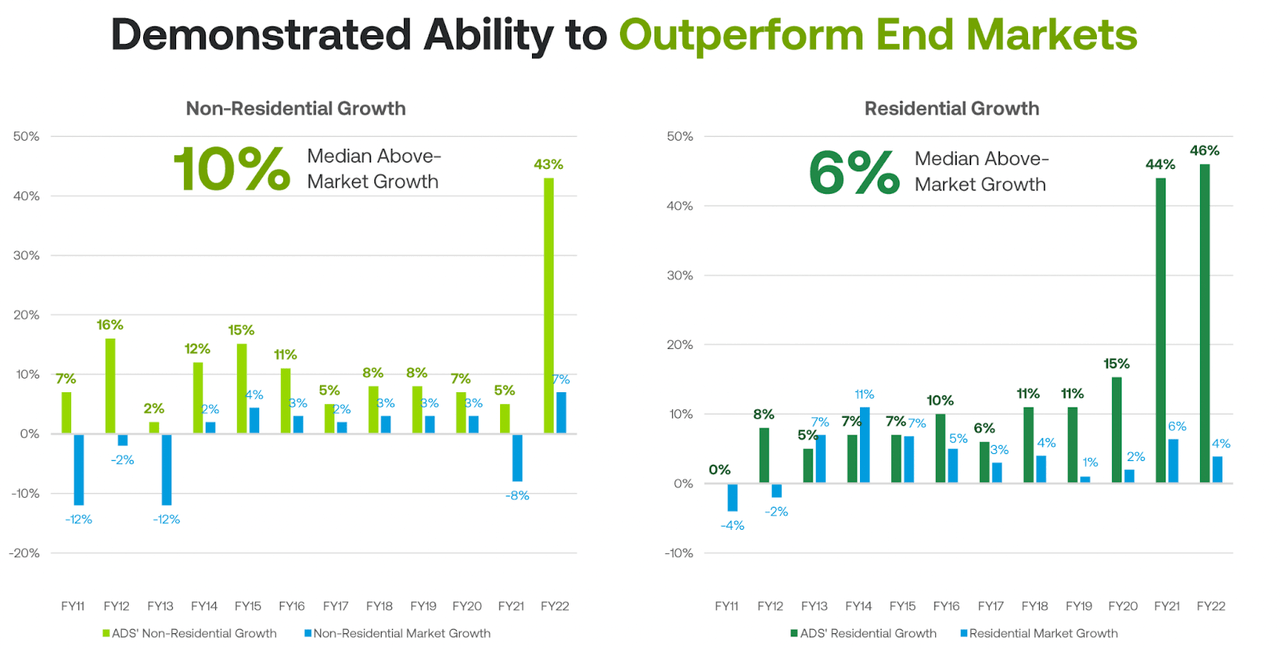

WMS is benefitting from a secular trend around the transition from traditional concrete pipe and tank to high-density polyethylene pipe (HDPE) and plastic-based tank products. These products take less space, are lighter, more durable, and cost-effective. Additionally, the plastic alternatives take half the time to install compared to traditional products, reducing labor costs for its customers. Due to these benefits, plastic products are increasingly used in the wastewater industry and WMS is benefiting from this trend. Over the last 11 years, Advance Drainage Systems outgrew the residential market by 6% and the non-residential market by 10%

WMS Revenue Growth Outperformance (Investor presentation)

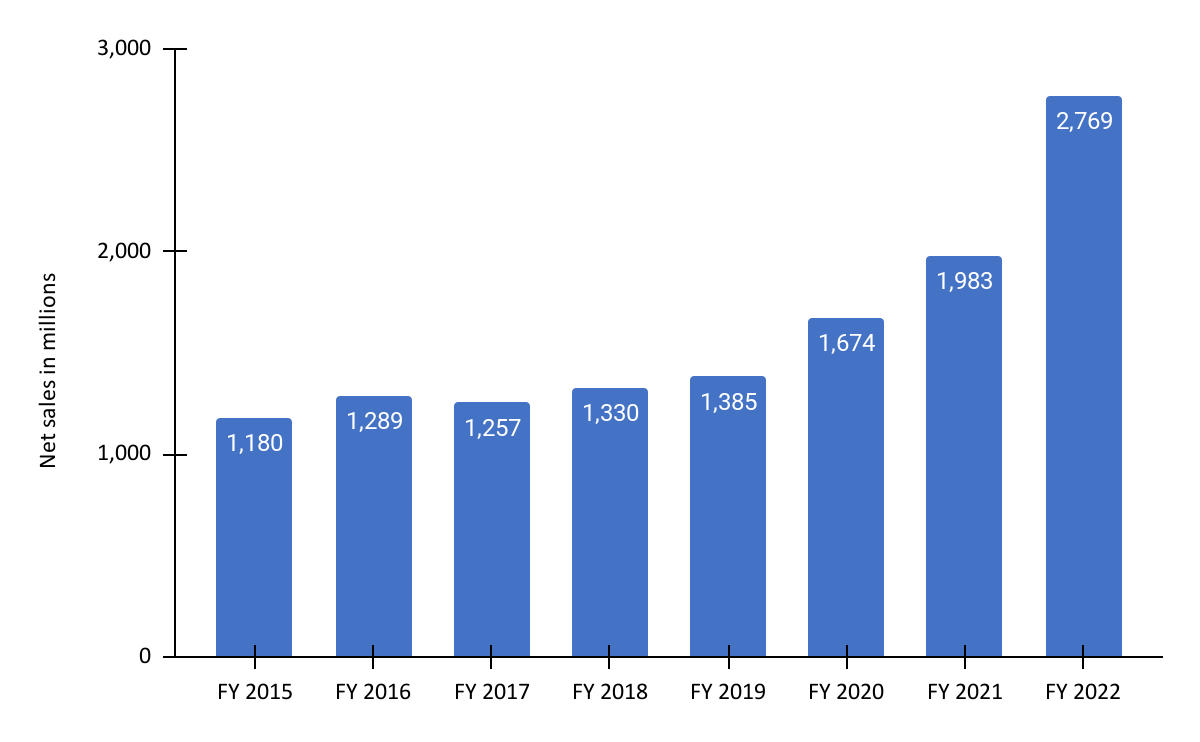

In the last couple of years, WMS’s revenue growth has benefited from the accelerated adoption of WMS’s superior product as well as favorable end markets. This resulted in the company’s net sales growing from $1.67 billion in FY20 to $2.7 billion in FY22. The company’s non-residential business grew 5% in FY21 and 43% in FY22 as compared to the market growth rate of -8% and 7% for respective periods. The Residential business grew 44% in FY21 and 46% in FY22 as compared to market growth rates of 6% and 4% for the respective periods.

WMS Net sales (Company data, GS Analytic research)

The company reported $914 million and $884 million of revenue during Q1 and Q2 of FY23, growing 36.6% and 25.2% Y/Y respectively. While the company reported solid Y/Y revenue growth in Q2, the performance was weak when we look compared sequentially with the revenue decreasing 3.3% from Q1 to Q2. This was primarily due to two reasons: Hurricane Ian and the significant destocking of leachfield products. During the last week of September, Hurricane Ian impacted sales in the central and southwestern parts of Florida and resulting in a 70% decline in shipment volume. Further, the leachfield products which form a significant portion of the Infiltrator segment’s sales saw unexpectedly high destocking from the distributors. The destocking resulted in a 6% sequential decline in revenue for the Infiltrator segment.

Looking forward, Hurricane Ian has resulted in a deferral of demand for two to three quarters as contractors are prioritizing recovery efforts over stormwater projects. Additionally, significant destocking of leachfield products at distributors is indicating weakening demand in the residential end market which represents 37% of the total revenue for WMS. Apart from these two headwinds, the company has a difficult year-over-year comparison, particularly in sales from the northeast and northwest geography. These areas experienced elevated levels of activity last year due to reopening. During the pandemic, these regions had a more dramatic pause. So, when they reopened there was a significant pent-up demand resulting in higher revenues. Hence, the revenue comparisons are tougher in the second half of FY23. This along with other short-term headwinds should result in a Y/Y decline in revenue for the next few quarters.

However, the good news most of these headwinds seem to be already priced in after the steep correction in the stock price. In the long run, management believes that their superior products should continue to gain traction and help the company to outperform the market and generate 2-3% above-market growth rate consistently. Frankly, the company has generated much higher outperformance in recent years and I believe management’s target of 2-3% outperformance versus end markets will likely prove conservative.

Margin Outlook

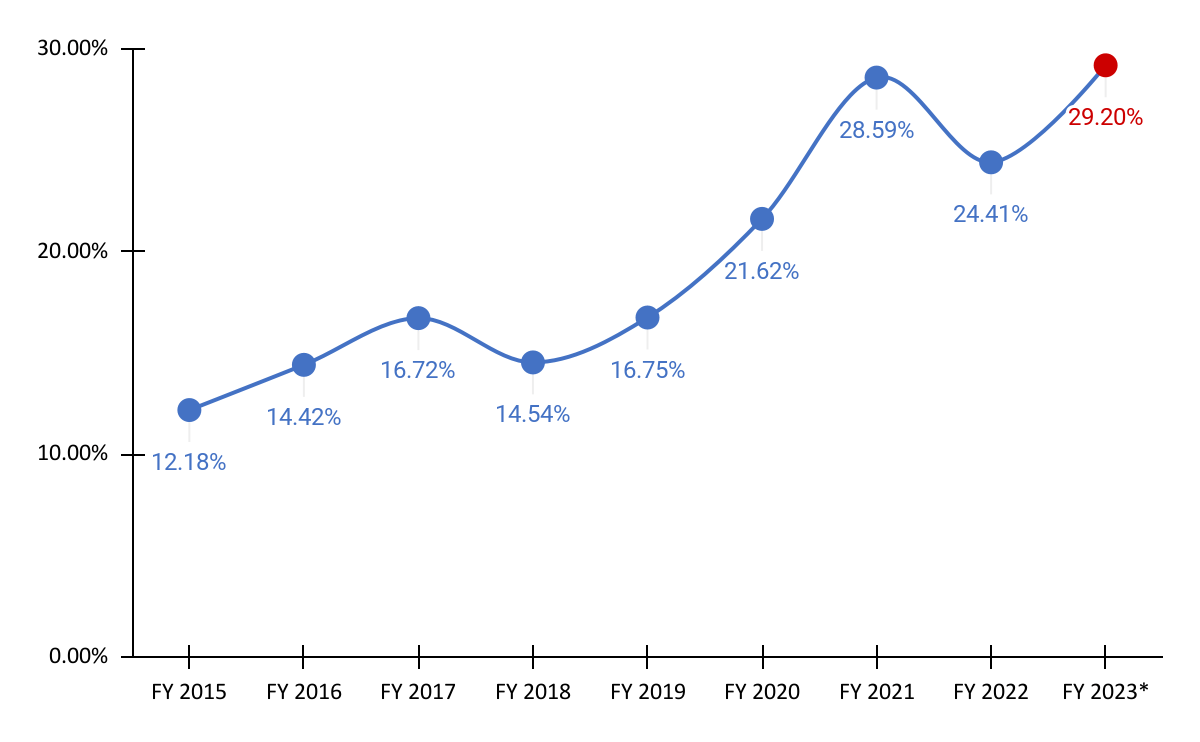

From FY19 to FY21, WMS witnessed an exceptional rise in adjusted EBITDA margin due to favorable pricing, operational leverage, and inclusion of higher profitable Infiltrator business, and the adjusted EBITDA margin increased from 16.8% in FY19 to 28.6% in FY20. However, during FY22 the company faced supply chain issues along with higher raw material prices and higher transportation costs resulting in a 420 bps decline in margins to 24.4%.

WMS Adjusted EBITDA margin (Company Data, GS Analytics Research, FY23 estimate is mid-point of management guidance)

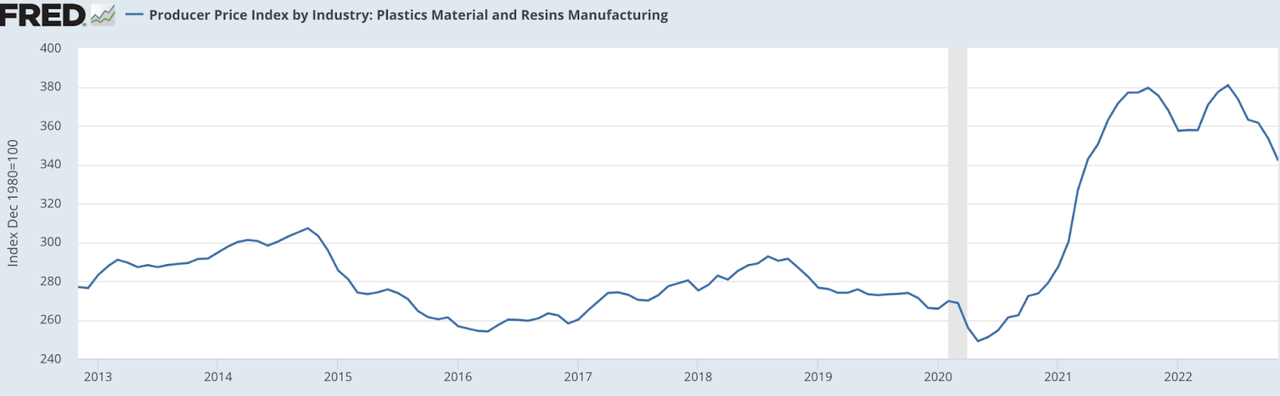

During the first half of FY23, the company witnessed some correction in resin prices which along with the prior price hikes benefited margins positively. The company’s adjusted EBITDA margins improved by 800bps and 644bps Y/Y to 32.7% and 29.8% for Q1 and Q2 FY23 respectively.

Producer price index by industry: Plastic material and Resin Manufacturing (FRED)

Looking forward, while management reduced their FY23 revenue guidance by ~5% due to headwinds described in the prior section, they kept adjusted EBITDA guidance unchanged at between $900 mn and $940 mn. This translates into a 130 bps increase in adjusted EBITDA margin from prior guidance. The management expects the full-year adjusted EBITDA margin to be ~29.2% (at the midpoint) as they expect to reap benefits from the stabilized resin prices while maintaining the price increases.

In the long term, the company’s margins should benefit from increased investments in productivity initiatives. During the last investor day, the company announced that they are going to invest $150 million in production facilities over the next 18-24 months. These investments are higher than the last 10-year average investment of $35-40 million per year. Management is making investments in automation, improving productivity in existing lines, debottlenecking raw material operations, and new production lines. These incremental investments are expected to increase productivity as well as increase production capacity which can contribute to higher operational leverage. Management has a long-term adjusted EBITDA margin target of between 28% and 29%. The company is expected to post margins above this range in the current year and I wouldn’t be surprised if the company’s long-term margin continues to beat this target range given its productivity initiatives and benefits from operating leverage once the short-term revenue headwinds fade.

Valuation and Conclusion

The stock is currently trading at a 9.13x EV/EBITDA (TTM) multiple which is at a significant discount to its five-year average of 15.45x. WMS is an interesting long-term growth story that can deliver an above-market growth rate in the long term. While investors are concerned about near-term headwinds, I believe most of these headwinds are already priced in at the current valuations. I believe long-term investors can consider buying the stock at the current levels.

Be the first to comment