Direct Line’s crashes create great entry points for Admiral investors. DNY59

Background

Back in July, a small Admiral Group plc (OTCPK:AMIGF, OTCPK:AMIGY) competitor, Sabre Insurance (OTCPK:SBIGY), shocked the London stock market with a profit warning following unexpectedly high motor claims inflation. Alongside the small insurer, the market leaders Admiral and Direct Line Insurance Group plc (OTCPK:DIISF, OTCPK:DIISY) tanked as well, and especially since not much later Direct Line itself issued its own profit warning.

As days went by without Admiral following suit, it dawned on investors that the motor insurer would post decent results – and, in fact, it did.

Librarian Capital, who is doing a great job following the sector, posted his excellent review here on this site.

The stock zoomed higher immediately, came back down together with the market at the end of Q3, but recovered again to roughly the same level. This is where it stood until this morning, when Direct Line shocked the stock market again.

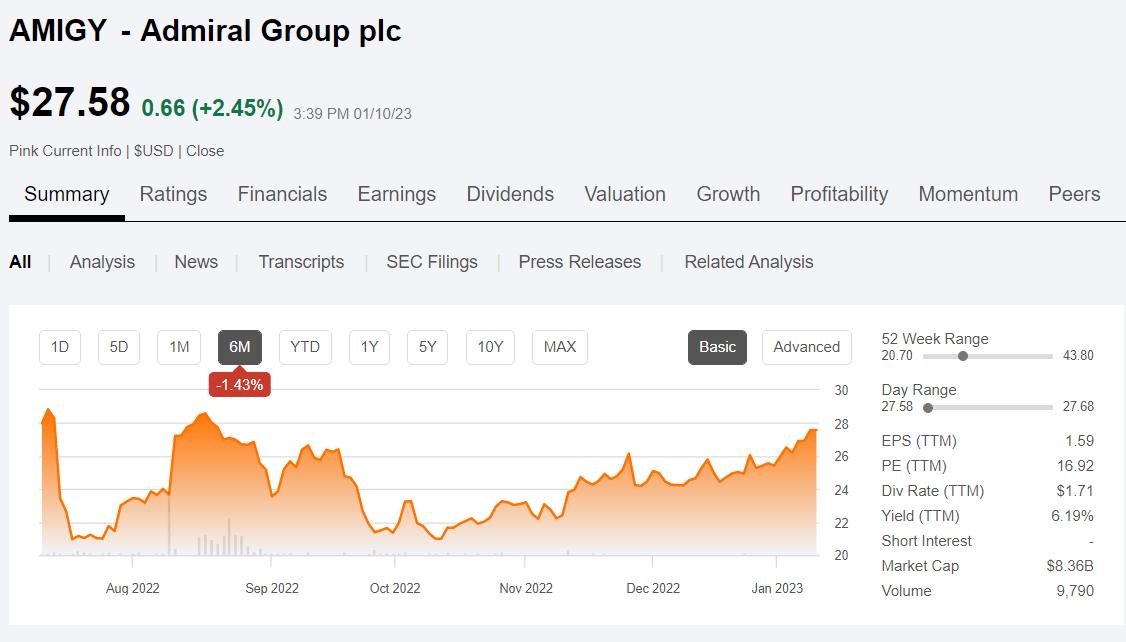

Admiral key metrics (Seeking Alpha)

Direct Line slashes its dividend

It is worth reading today’s news release in its entirety, but here are the key topics:

- Severe cold weather in December impacted household insurance because of burst pipes, water tanks, and similar damage. The company expects total weather claims to be in the region of £140 million for 2022, well above its 2022 expectation of £73 million.

- Motor claims inflation frequency in Q4 also increased because of adverse weather. The company estimates these factors will increase the motor loss ratio in 2022 by around six percentage points.

- As already highlighted in the Q3 trading update, the investment property market has seen a reduction in valuations and Direct Line’s investment property portfolio has experienced a c.15% reduction in values, equivalent to £45 million.

All together, these are significant impacts. Direct Line posted £446m of pre-tax profits for 2021 and, following disappointing updates in 2022, was currently expected to post £270m for 2022.

As a consequence, the company won’t pay its final dividend and instead focus on improving its balance sheet. This is clearly a shocker for investors. For over a decade, Direct Line’s only contribution to stockholders’ returns has been dividends. A bad balance sheet and highly evident bad management decisions clearly indicate that there is not much to expect from this company in the near to medium term. This is why the stock is down 28% as I write.

While this might be a trading opportunity, if you want to speculate on a rebound, personally I am not interested. Instead, this morning I substantially increased my Admiral position, which provides a better risk/return ratio in my opinion.

Why Admiral will be fine

Back in the summer, it was not easy to see why Admiral would do better than Sabre and Direct Line before it actually proved to have the better management. This is because the key issues for both insurers were in the UK motor insurance segment – which is where Admiral makes virtually all of its profits, too.

Today, things are much easier: While Admiral also has a household insurance segment, its contributions to pre-tax profits are very small compared to its large motor segment and represented just ~3% of total EBIT in H1/22. The segment posted just £26m of net premiums in H1/22. Direct Line’s Home insurance segment’s net premiums were over ten times as large, and the segment EBIT was over 7 times Admiral’s. Overall, Direct Line’s Home segment’s EBIT represented over 25% of the group’s total EBIT.

Moreover, in H1/22, Admiral’s Motor segment combined ratio stood at a highly profitable 84%, in contrast to Direct Line’s ugly 105% in H1/22. This is why even a similar 6% loss ratio deterioration shouldn’t push Admiral into the red.

Finally, Admiral does not have exposure to a real estate investment portfolio of any significance.

As a result, I do not expect any significant deterioration of Admiral’s business prospects compared to current expectations.

Valuation

Around GBP2,000, where Admiral trades as I write, it is valued at 14-15x EPS (2023e) and should yield 6-7%. While not super cheap, it is at the lower end of the past few years’ valuation multiples. Just consider that it trades at 2016 levels despite increasing its UK customer base by over 50% since then, while doubling its international customer count.

In addition, the nicely growing ex-UK business is still contributing losses – which means we are actually attributing a negative value to it when looking only at the PER. Notably, the losses are only due to the difficult U.S. market, while the EU operations are roughly at break-even. Overall, Admiral’s ex-UK business insures about 2m customers out of the group’s total 9m. I am sure it would be worth quite a bit of money in a private transaction. Admiral has already executed some profitable exits from unprofitable international expansion attempts (p.e. Germany), so there absolutely is hidden value.

Finally, considering the company’s history (see below) of highly profitable growth, low capital intensity, and robust shareholders returns, a multiple above the sector average is certainly warranted.

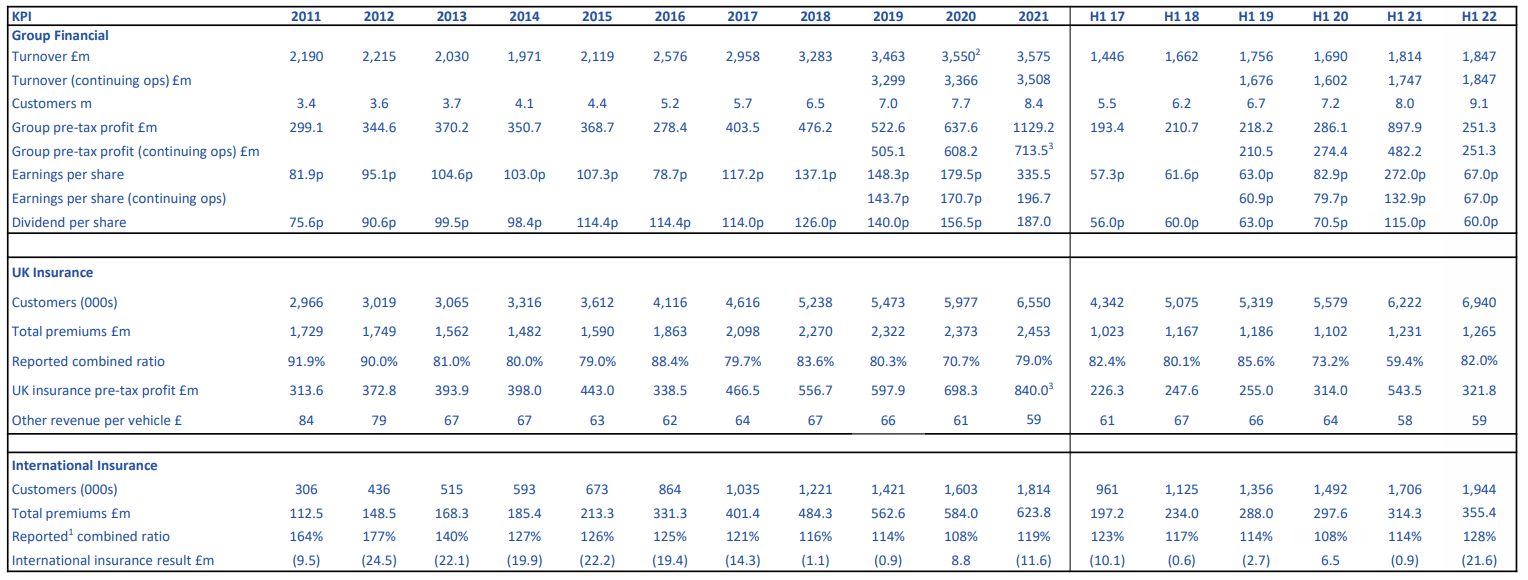

Admiral KPI history (Admiral H1/22 presentation)

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment