Focus Design/iStock via Getty Images

Description

I recommend buying Accel Entertainment (NYSE:ACEL). ACEL has a unique business model that enables it to better ride on the secular tailwinds that are driving the industry growth. In addition, ACEL has a strong track record of M&A that gives me further confidence they are able to continue growing the scale of its business, which enables it to repeat its roll-up strategy. All in all, I think the current valuation is not demanding, so long as management can grow high-single-digits and maintain margins, we should see good upside.

Company overview

ACEL is a business that offers online gaming as a service. The company offers retail outlets with slot machines, redemption machines, and amusement devices.

Gaming industry

ACEL is a participant in the U.S. distributed gaming industry, which involves the placement and maintenance of slot machines in locations that are not licensed casinos. In my opinion, the regulatory green light is the biggest tailwind for the distributed gaming industry. On the other hand, gaming’s increasing mainstream popularity in the United States is a key factor in the industry’s expansion (both online and digital gaming). Finally, there is a growing segment of the population that values the ease of having access to gaming entertainment in their own homes because they are getting older. A larger pool of players and a wider selection of high-quality game profiles will likely emerge as a result of the proliferation of jurisdictions that have legalized distributed gaming.

Unique business model

ACEL’s business model deviates from that of a traditional casino or slot machine operator. It’s a platform for online gaming as a service. In my opinion, there are a number of benefits to adopting this method of doing business. This business operates on a B2B model and generates revenue through long-term, exclusive contracts, leading to consistent, recurring income and minimal customer loss. This success is bolstered by ACEL’s minimal need for CAPEX. When comparing the financial performance to that of casinos, which offer more capital-intensive entertainment options, this difference becomes clear.

ACEL’s ability to collect data via this platform is also noteworthy because it allows the company to better advise its licensed establishment partners on how to increase their profits. As a result, ACEL will be in a prime position to increase its presence in the area and begin capturing market share there. Since it has a very localized footprint, it is less vulnerable to disruptions in its feeder markets than regional casinos, which advertise to customers who may live several hours away.

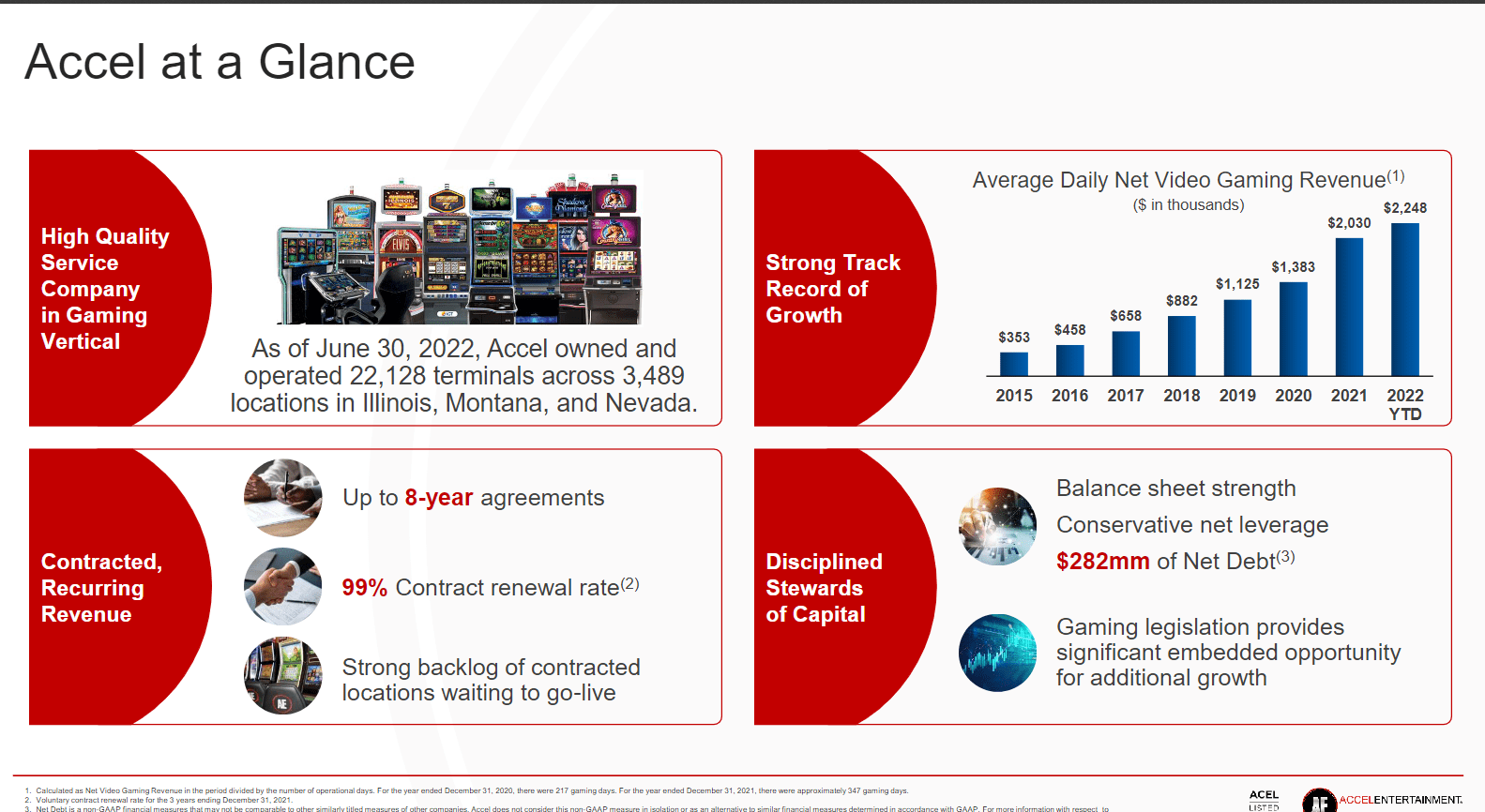

3Q22 presentation

Strong relationship with stakeholders within the ecosystem

Since the company’s inception, building trustworthy partnerships with end-channels (licensed partners) has been at the top of Accel’s list of priorities. To achieve this goal, it assigns a dedicated relationship manager to each of partner, who is responsible for managing and retaining those partnerships. Accel takes great pride in the fact that the quality and quantity of its education and support services has contributed to an uptick in the number of referrals made by its partners. I think one of the things that sets ACEL apart from the competition is the fact that its relationship managers consistently pre-renew contracts with their licensed establishment partners well in advance of their expiration.

In addition to its dominant market position, ACEL also enjoys solid ties to the industry and its equipment providers. Accel’s position as a market leader also helps it negotiate for better terms when purchasing essential gaming equipment. In another words, Accel is in a position to rapidly rotate machines to licensed establishment partners in areas of its operating footprint where they are most needed because of its easy access to machines and parts. All of this means that Accel’s equipment is used more efficiently and for longer periods of time, and thus lasts longer.

Organic growth opportunities

There is still plenty of room for VGT to expand throughout Illinois, and I think there is especially promising opportunity in the state’s primary local markets, including Springfield, Bloomington, and Decatur. I believe ACEL can also broaden its distribution options beyond just entering new markets by forming partnerships with corporations that own and operate multiple licensed businesses, such as chains stores. The larger operators who have invested heavily in compliance infrastructures and who can also provide industry-leading services are the ones that stand to benefit most from the corporate market, in my opinion. Although such businesses have been “second movers” in adopting video gaming, working with players like ACEL could make VGT deployment an easier and more reliable process. Also, ACEL’s market position positions it to benefit from regulatory changes in Illinois, such as an increase in the permitted number of VGTs per business.

Proven track record of M&A

For further expansion, I think ACEL can pursue both organic and M&A strategies. ACEL has a history of finding competitive operators at value-accretive terms and integrating them into their business successfully. Accel has expanded its portfolio of licensed establishment partners to 3,489 as of 3Q22 by acquiring several operator companies since becoming a terminal operator (includes Century). ACEL ability to acquire peers on favorable terms is bolstered, in my opinion, by its standing in the industry, size, and history of generating revenue synergies. In short, I think ACEL is the best option for any operator looking to part ways.

Solid 3Q performance reaffirms bull case

Revenues for 3Q22 were $267 million, which were below the consensus estimate of $270 million. In addition, EBITDA came in at $41.1 million, which was in line with the consensus estimate of $42.5 million. In addition , I think many investors were pleasantly surprised to see Century expand both its store count and unit count in the third quarter. ACEL also provided some upbeat analysis of October’s trends, which improved sequentially and showed no effect from inflation or the macro environment. The most important news is that ACEL has reiterated its projections for stores, VGTs, sales, and EBITDA for FY22.

ACEL’s large pipeline of licenses or partners in Illinois, which gives it excellent visibility into future expansion and revenue growth, is something I believe is undervalued. Assuming no additional sales initiatives, ACEL has enough locations in the pipeline to support its growth for several more months, and the company expects to bring online a further 18-24 additional locations during this time. In addition to these, I anticipate that the Century acquisition will begin to pay off in the form of contributions from upgraded machinery and improved distribution arrangements.

Valuation

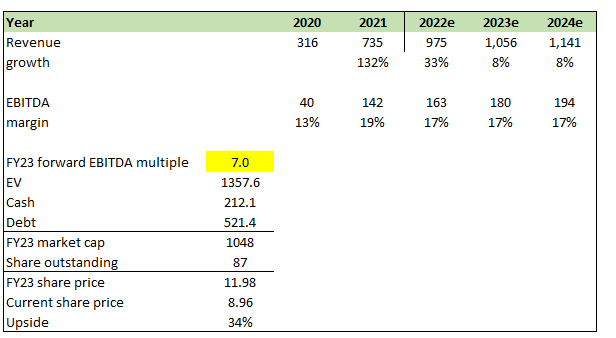

In FY23, I believe ACEL is worth USD11.98, which translates to 34% upside. My model is based on management FY22 guidance, and a stable high-single-digits growth rate moving forward, and the forward EBITDA valuation that ACEL is trading at today.

I believe the 3Q22 earnings have cleared some doubts regarding ACEL’s acquisition of Century – which is showing better-than-expected results. Moving forward, as ACEL continues to integrate Century business, and grow the business organically, I believe ACEL is set to continue growing at a stable pace.

Own estimates

Key risks

Concentration in Illinois

The vast majority of ACEL’s revenue is generated in Illinois, which exposes the company to regulatory changes and regional consumer preference swings.

Macro risk

The VGT market could face challenges, such as a rise in the rate of store closures and a possible decrease in spending per machine, if there is a sharp drop in discretionary spending.

Summary

ACEL’s distinctive business model positions it favorably to capitalize on the secular tailwinds that are driving industry expansion. Further reassuring my faith in ACEL’s ability to repeat its roll-up strategy and grow the size of its business is the company’s impressive history of mergers and acquisitions. All things considered, I do not believe the current valuation is overly demanding; if management can grow by high single digits while keeping margins stable, we should see good upside.

Be the first to comment