Kyle Benne/iStock via Getty Images

Inflation may be making an unexpected return in January after three months of declining inflation rates. There is mounting evidence that prices for essential commodities and services are again on the rise, which could surprise the markets.

Commodity prices like gasoline, oil, and copper are surging. Meanwhile, used auto prices are rising while the number of people dining out is increasing, possibly elevating the cost of food away from home. These measures are highly correlated to CPI, and if they continue to rise, this will create a significant problem for the Fed and the markets. It will mean that rates will need to stay higher for longer and possibly even higher than projected at the December FOMC meeting if something doesn’t change soon.

Easing Financial Conditions

Blame the easing of financial conditions and the weaker dollar for the sudden surge in commodities and import prices. As measured by the Chicago Fed, financial conditions are now at levels not seen last spring before all of the massive rate hikes from the Fed.

Bloomberg

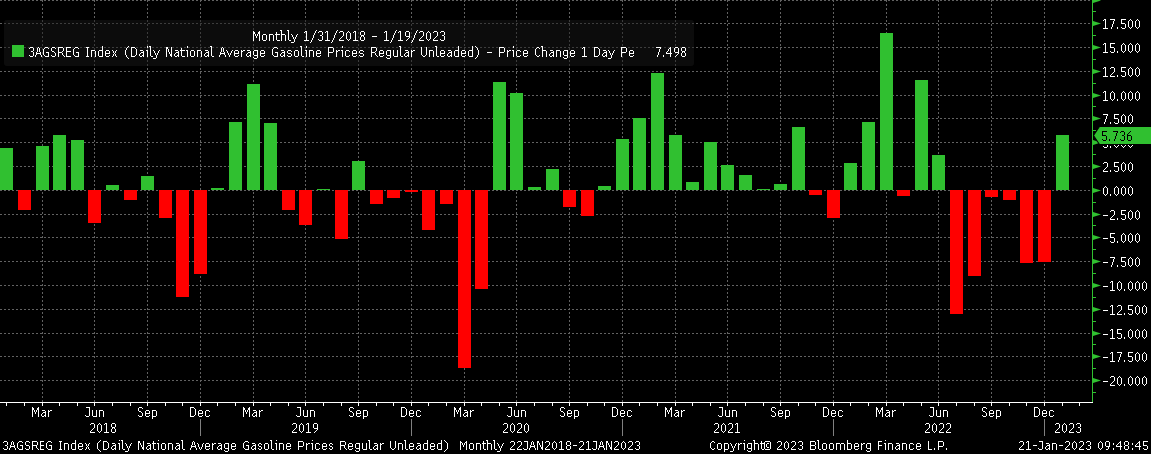

The easing of financial conditions, which includes a weaker dollar, is now showing up in several crucial commodities. The national average of regular unleaded gasoline jumped by nearly 6% thus far in January. It is no small impact either because gasoline has a weight of 3.95% in the CPI, and that could equate to gasoline increasing the CPI month over month by 0.23%

Bloomberg

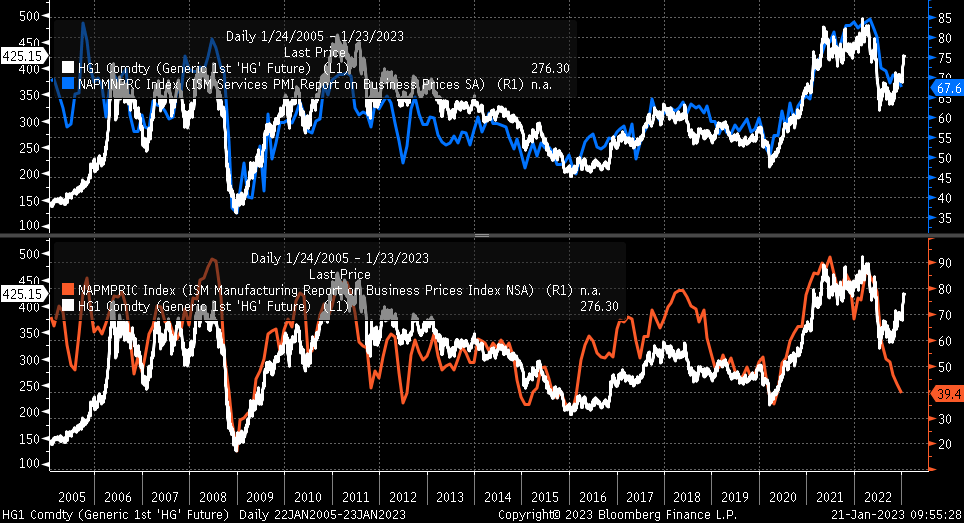

Meanwhile, the risk-on mentality that comes with easing financial conditions and hopes of a smooth China recovery has increased copper prices by almost 12% in January. It is hard to predict the impacts of rising copper prices directly, but it ties into the prices paid by the ISM manufacturing and ISM services indexes. So while the market has cheered the declining ISM prices paid indexes in recent months, those two indexes seem destined to rise again should copper continue to push higher.

Bloomberg

Signs Of Inflation Beyond Commodity Prices

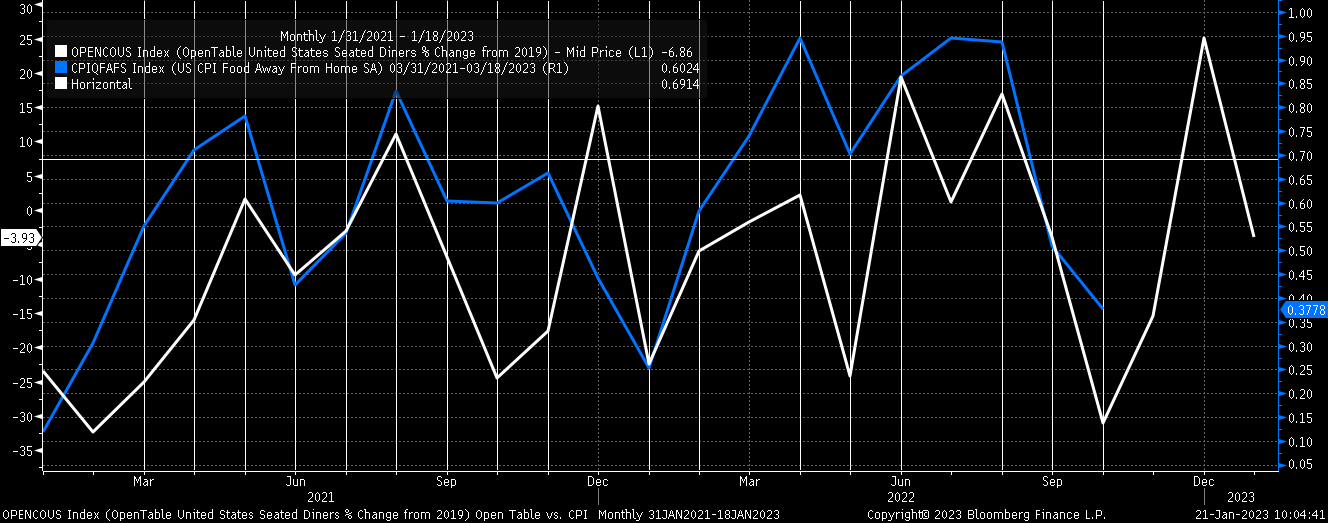

Additionally, the OpenTable seated diners index has been rising recently. That measure of people going out to eat leads to changes in the CPI category for food away from home by roughly two months, which means the food away from home category could rise as soon as the January CPI report. Food away from home is not a tiny category, accounting for a 5.25% weight in the overall CPI.

Bloomberg

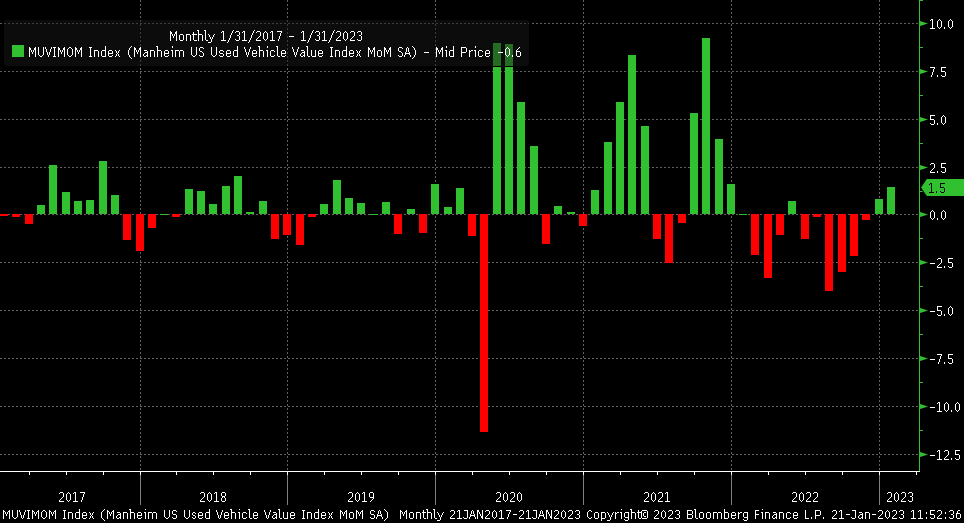

But it doesn’t stop there because, through the first half of January, the Manheim used vehicle index increased by 1.5%, which currently marks the second month in a row that used vehicle prices are rising, a reversal of six months of declines. Used autos account for 3.6% of the overall CPI, and rising used auto prices will also positively impact the CPI in January.

Bloomberg

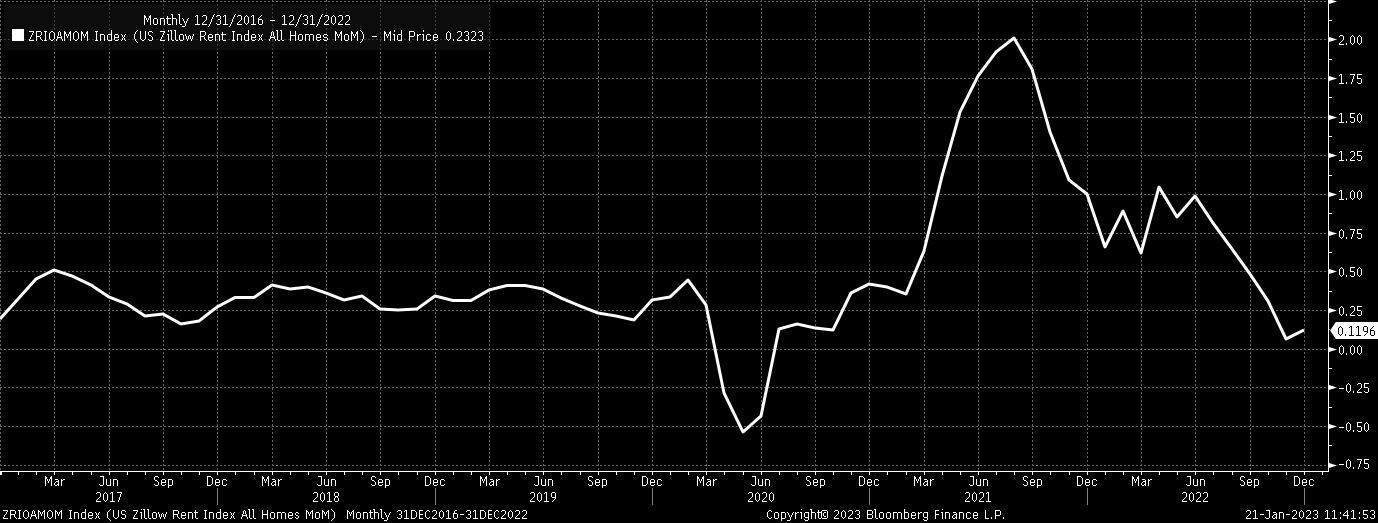

And while many investors are waiting for the rent component of CPI to come down, the Zillow Rent Index rose in December for the first time in many months. It may be a false move higher, as we have seen previously, but it is also possible that it is the start of rents rising again.

Bloomberg

The Effects of The Weaker Dollar

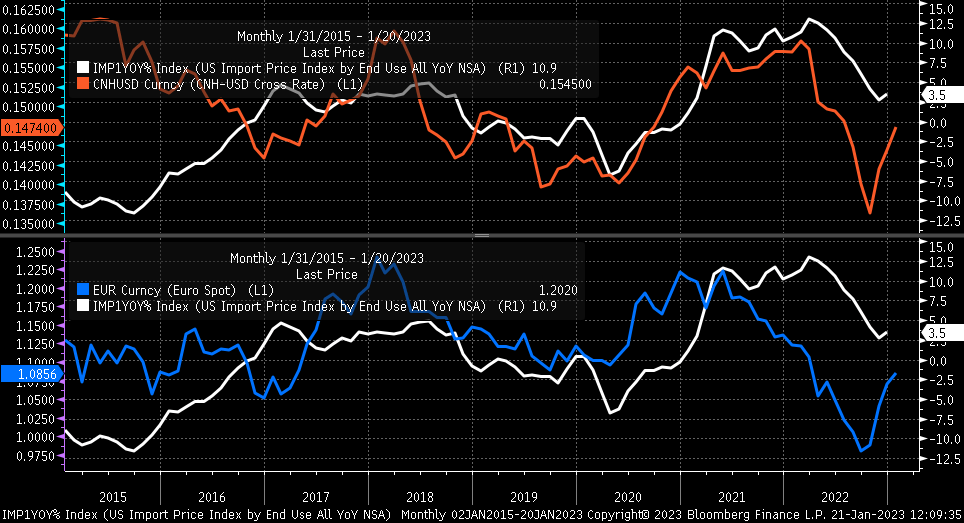

The weaker dollar is also helping ease financial conditions and boost commodities prices, but the weaker dollar also bleeds into import prices. Import Prices rose by 0.4% month over month in December, their fastest increase since May. Import prices had slowed as the dollar strengthened against currencies like the Chinese yuan and the euro. Since October, that has changed, and now the yuan and the euro are strengthening versus the dollar. That means that the US will now be an importer of inflation from China, Europe, and the rest of the world.

Bloomberg

Inflation Swaps See A Higher CPI

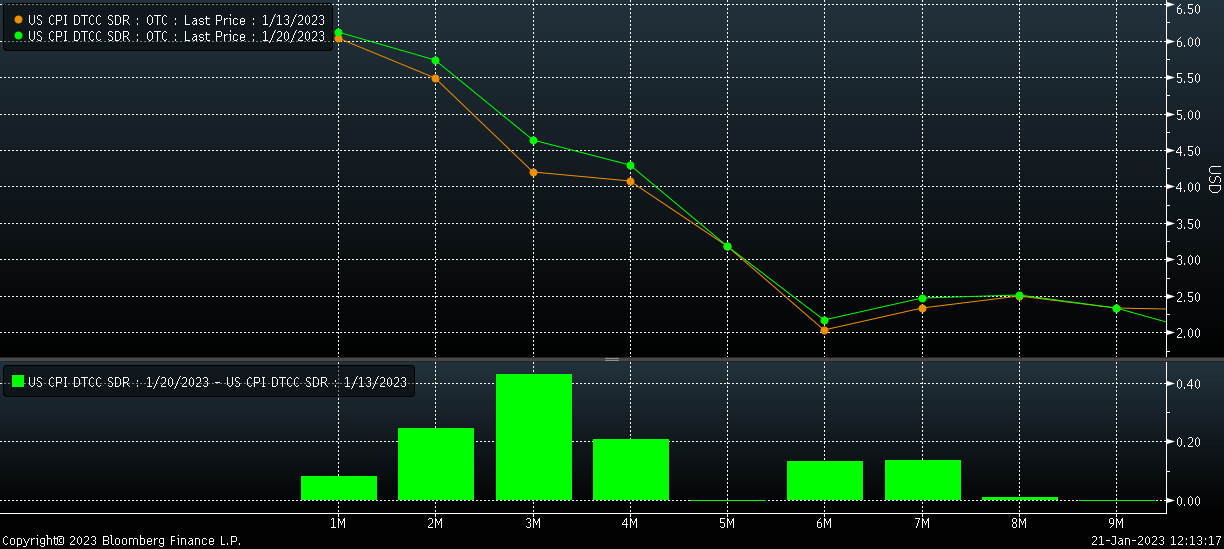

The rising prices are not going unnoticed by all of the markets because CPI inflation swaps for January are on the rise and are currently pricing the CPI to rise by 6.1% on a year-over-year basis. That rate has been steadily climbing after reaching a low of 5.9% at the start of the month. The inflation outlook for February is rising even faster, climbing to 5.7% from roughly 5.2% over the same time.

Bloomberg

The inflation swap curve has shifted over the past week, with the most significant changes occurring between January and April, with March thus far seeing the most significant move higher. The curve still tells us that the inflation rate is slowing, but it also suggests that it will not fall as quickly as the market thought just a week ago.

Bloomberg

Most Important of All

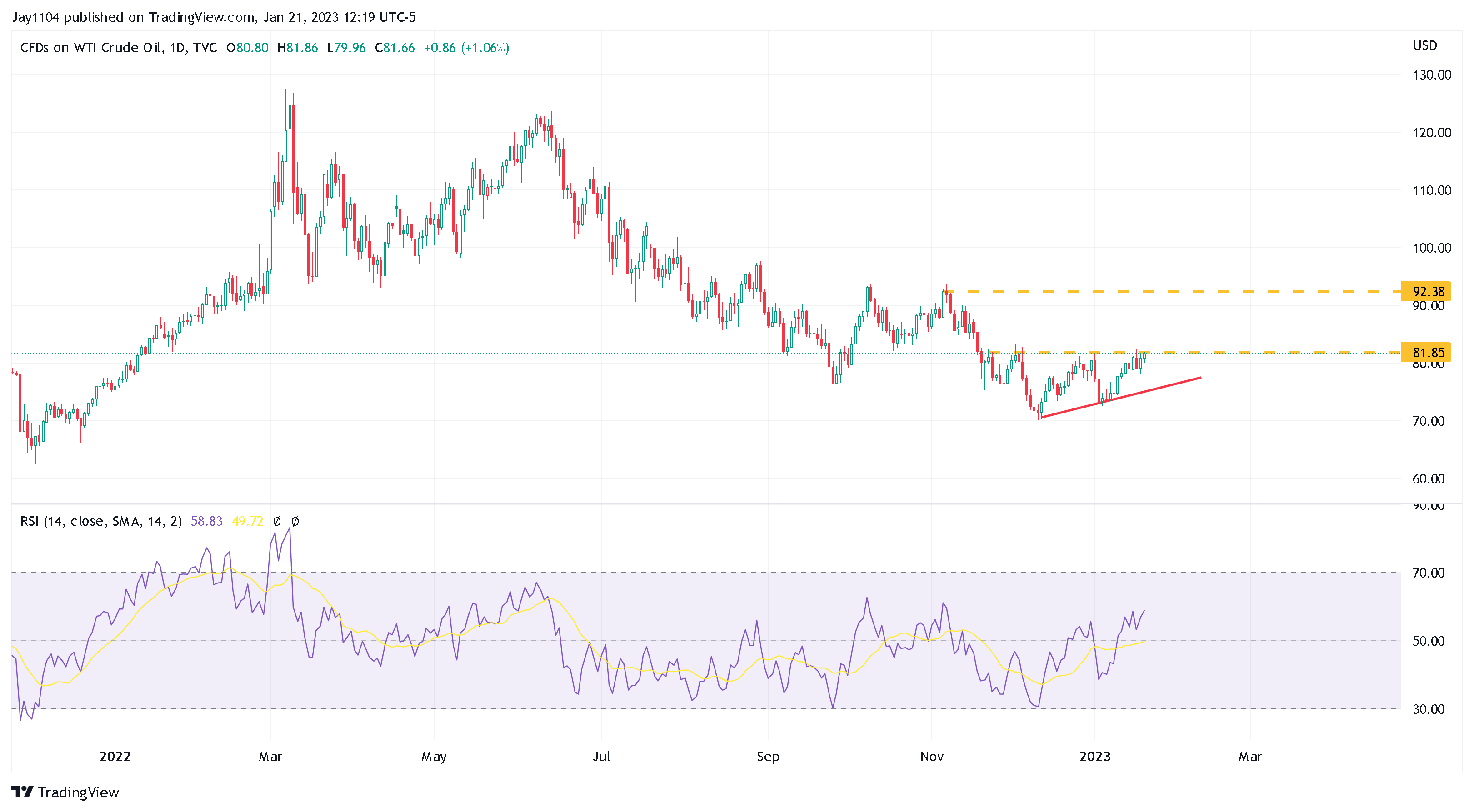

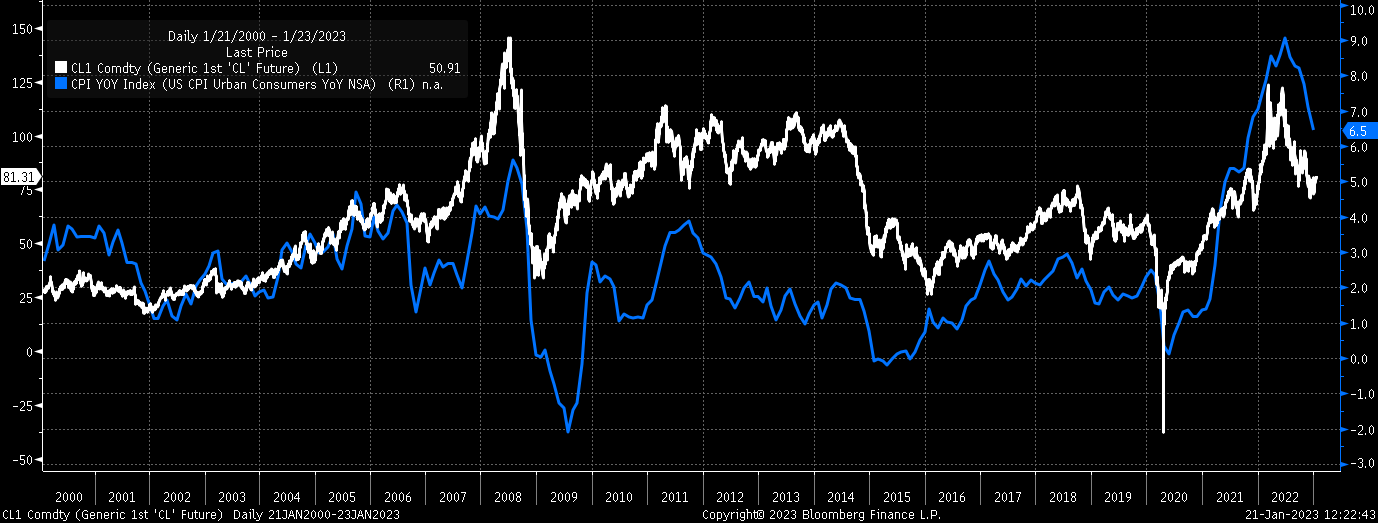

Oil, which is currently up 1.3% in January, will also shape where the market sees inflation heading. But oil could be going much higher, first because of China re-opening and plans for the US to refill the Strategic Petroleum Reserves.

The technical chart for oil also indicates that prices could be heading higher and potentially to around $90 should the oil break above resistance at $82.

TradingView

Changes in the price of oil have the most significant positive and negative impacts on inflation in the US over time. If oil prices head higher in the near term, the pace at which inflation cools will slow even further when adding to all the other factors mentioned above.

Bloomberg

Inflation has hopefully peaked, but the pace at which it will fall is likely to take longer than the market thought. It is also likely to prove that the Fed was correct regarding how high rates go and how long they are likely to stay at those elevated levels.

The more the market fights the Fed and allows financial conditions to ease, the higher rates will need to rise and the longer they will have to stay high.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment